How to House Hack: The FHA Loan Strategy Explained

Buying a house right now feels like a rigged game. With interest rates hovering at brutal levels and standard down payments sitting at a massive 20%, most working professionals feel completely locked out of the real estate market.

If you try to save $80,000 in cash to put down on a standard starter home, inflation and rising home prices will likely eat your savings faster than you can accumulate them. You cannot out-save a hot housing market. But you do not have to play by the traditional rules. You can bypass the massive down payment barrier entirely.

What if you could buy a half-million-dollar cash-flowing asset, put down a fraction of the standard cost, and have someone else pay the monthly mortgage for you?

It sounds like a late-night infomercial scam, but it is actually one of the most reliable, mathematically sound wealth-building strategies on the planet. If you want to break into real estate without a trust fund or a Wall Street salary, you need to learn exactly how to house hack.

Here is the ultimate operational blueprint, the hard mathematical realities, the exact FHA loan loophole, and the hidden traps of learning how to house hack your first investment property.

What is House Hacking?

At its core, understanding how to house hack is incredibly simple: you buy a property, live in one part of it, and rent out the other parts so that the rental income covers your mortgage, property taxes, and insurance.

You become a landlord, but instead of buying a property across town and hiring a management company, you sleep under the exact same roof as your tenants.

There are three primary ways to structure this investment:

1. The Single-Family Hack (The Co-Living Model) You buy a standard 3-bedroom, 2-bathroom suburban house. You live in the master bedroom and rent out the other two bedrooms to roommates, traveling nurses, or young professionals. Their combined rent pays the bulk of the mortgage. While this is the easiest entry point for how to house hack, you have to share a kitchen and living space with your tenants, which can be exhausting for older professionals or couples.

2. The Multi-Family Hack (The Gold Standard) This is the holy grail of real estate investing for beginners. You buy a small multi-family property—specifically a duplex, triplex, or fourplex. You live in one dedicated apartment unit and rent out the other units to traditional tenants. You get your own kitchen, your own front door, and total privacy, while the tenants next door pay down your massive mortgage.

3. The ADU Hack (Accessory Dwelling Unit) You buy a single-family house that has a detached guest house, a finished basement with a separate entrance, or a livable space above the garage. You live in the main house and rent out the ADU (or vice versa). This offers great privacy without the premium price tag of a traditional multi-family building.

The Secret Weapon: The FHA Loan Loophole

To understand why learning how to house hack is the ultimate wealth cheat code, you have to look at the raw financial leverage it provides.

If you walk into a bank and tell them you want to buy a $400,000 duplex strictly as an investment property, the commercial lending department will classify you as a high-risk investor. They will demand a 20% to 25% down payment. That is $100,000 in cold, hard cash just to close the deal. Most regular people do not have $100,000 sitting in a checking account.

This is where the federal government steps in to help. Enter the FHA Loan.

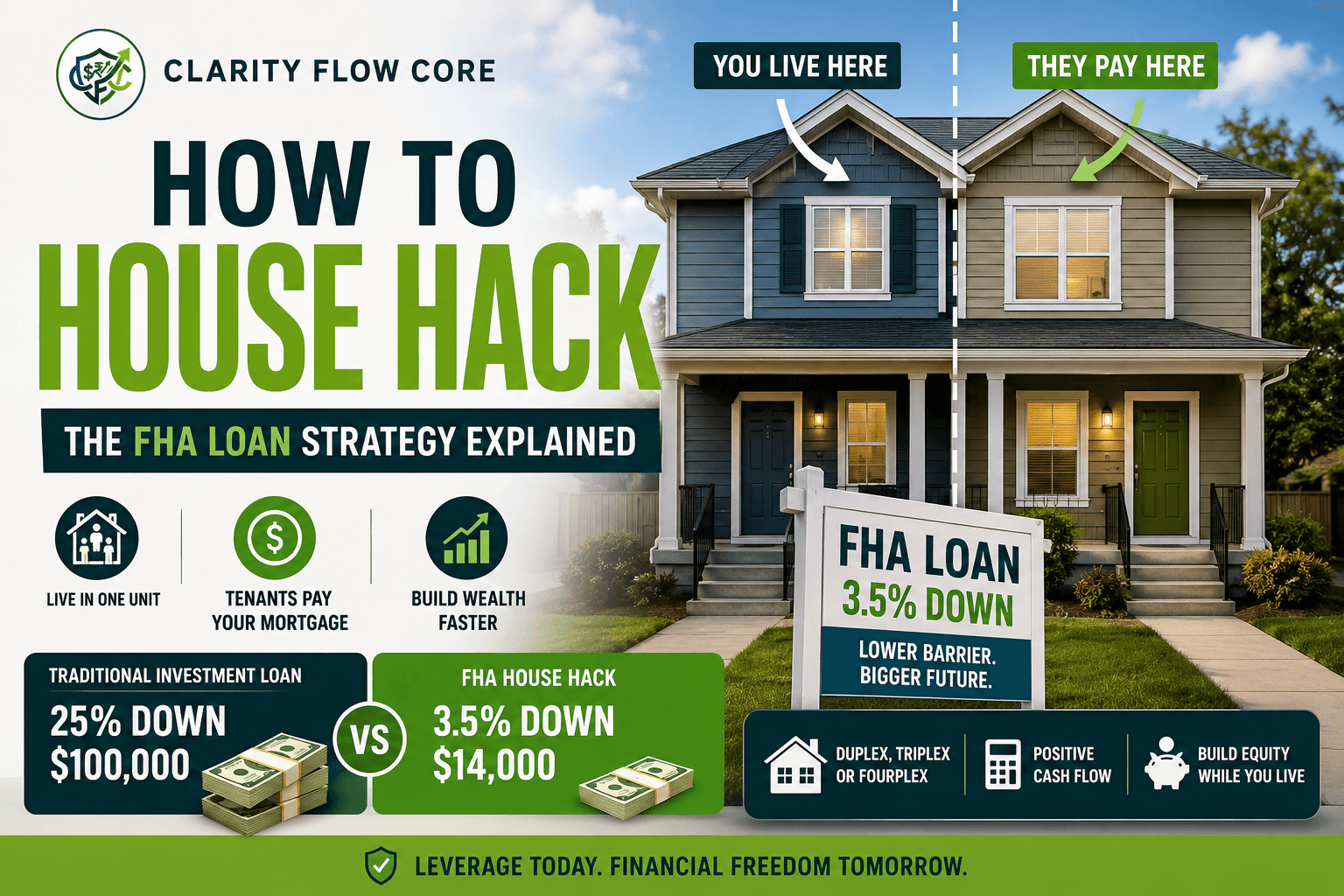

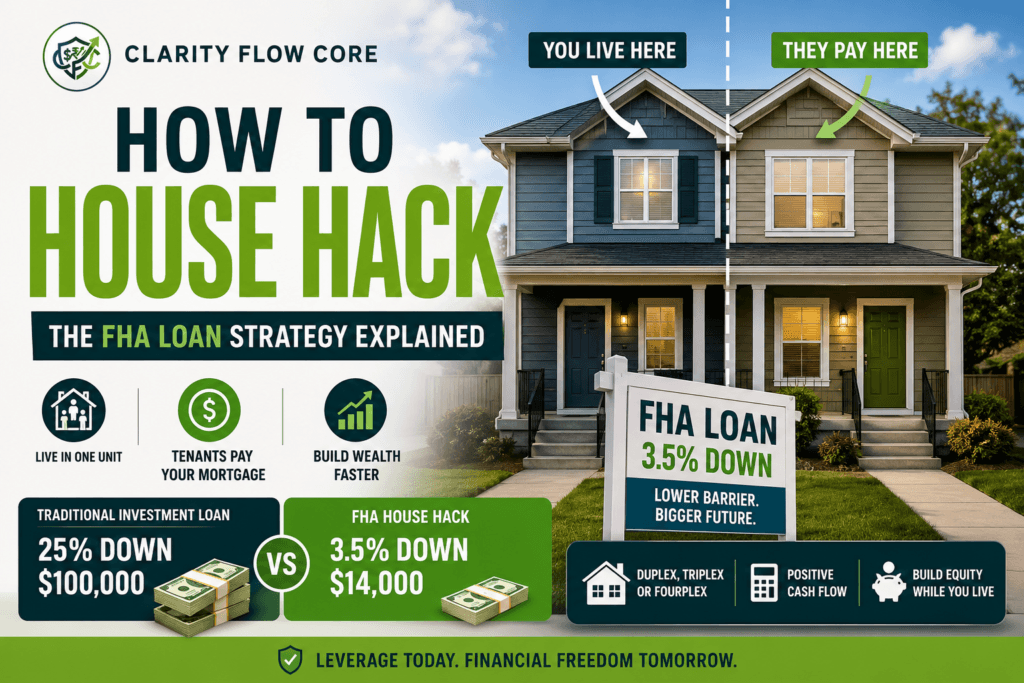

Because you are planning to physically live in the property (even if it is just one unit of a fourplex), the government classifies the entire building as your “primary residence.” This single legal classification allows you to use an FHA (Federal Housing Administration) loan, which is designed to help everyday Americans buy homes.

An FHA loan only requires a 3.5% down payment.

Suddenly, the barrier to entry collapses. Look at the mathematical difference on a $400,000 property:

| Financing Strategy | Required Down Payment % | Cash Due at Closing (Down Payment) |

|---|---|---|

| Traditional Investment Loan | 25% | $100,000 |

| Standard Conventional Loan | 20% | $80,000 |

| The FHA House Hack | 3.5% | $14,000 |

If you have been practicing the 7 Everyday Saving Habits That Can Make a Real Difference, saving $14,000 is an entirely realistic goal. You are controlling a $400,000 asset with just $14,000 of your own money. The bank puts up the other $386,000, but you get 100% of the appreciation, the tax write-offs, and the equity build-up.

The Advanced Rule: The FHA Self-Sufficiency Test

If you are researching how to house hack a larger property (specifically a 3-unit triplex or a 4-unit fourplex), there is a massive FHA rule that most beginners get completely blindsided by: the Self-Sufficiency Test.

To prevent buyers from taking on massive mortgages they cannot afford, the FHA requires that 3- and 4-unit properties be “self-sufficient.”

The Rule: 75% of the total appraised rental income of all units in the building (including the unit you plan to live in) must equal or exceed the total monthly mortgage payment (including taxes and insurance).

If a fourplex has a monthly mortgage payment of $4,000, the gross market rent of all four units combined must be at least $5,334 a month. (75% of $5,334 = $4,000). If the math falls even one dollar short of this test, the FHA will flat-out deny your loan, no matter how good your credit score is.

(Note: This test does not apply to single-family homes or 2-unit duplexes. This is why a duplex is the most popular starting point when figuring out how to house hack).

Execution Strategy: The 4-Step Operational Plan

You cannot just blindly buy a house and hope it works out. A successful venture into how to house hack requires militant preparation and cold, hard math. Here is your operational game plan.

Step 1: Fix Your Financial Foundation

Before a bank hands you nearly half a million dollars, your financial house must be flawless.

- Credit Score: You legally need a minimum FICO score of 580 to qualify for an FHA loan, but a score of 680+ will secure a much better interest rate and lower fees. If your score is struggling, read FICO vs. VantageScore: Why Credit Scores Differ Between Apps and aggressively clean up your file.

- Debt-to-Income (DTI): The bank will look at your monthly debt payments compared to your gross monthly income. If you are choking on 24% interest credit cards, use the Debt Avalanche vs. Debt Snowball method to clear them out before applying for the mortgage.

⚖️ Will the Bank Approve Your FHA Loan?

Before you start hunting for a duplex, you need to know if you actually qualify. Plug your gross income and current monthly debts into our free Debt-to-Income (DTI) Analyzer to calculate your exact ratio and find out how an FHA underwriter will view your file.

Step 2: Find a “Turnkey” Multi-Family Property

You are looking specifically for a duplex, triplex, or fourplex. Do not buy a 5-unit building. The moment a building has 5 or more units, it is legally classified as commercial real estate, which completely voids the 3.5% FHA residential loan strategy.

Unless you are a professional contractor, do not buy a completely destroyed “fixer-upper” for your first deal. When learning how to house hack, you want a property that is already in livable condition. You need to be able to move in and immediately start collecting rent from the other units, not spend eight months pulling permits, failing inspections, and replacing drywall.

Step 3: Run the Hard Math (Net Operating Income)

Never buy a property based on emotion or because it has a nice kitchen island. You are buying a business. You must run the cash flow math.

A fatal trap in how to house hack is ignoring the hidden operational costs of property ownership. You cannot just compare the mortgage to the incoming rent. You must account for Vacancy (when the unit sits empty between tenants) and CapEx (Capital Expenditures, like saving for a new roof or water heater).

Free Tool: FHA & Mortgage Affordability Calculator

Before buying a multi-family property, run the hard numbers. Instantly calculate your estimated monthly PITI, required FHA MIP (insurance), and closing costs.

Here is the operational math on a highly realistic $350,000 Duplex Hack:

| Monthly Expense / Income | Operational Math | Total |

|---|---|---|

| Gross Rental Income (From Unit 2) | 1 Unit @ $1,800/mo | +$1,800 |

| Mortgage (P&I, Taxes, Insurance) | Estimated FHA Payment | -$2,400 |

| CapEx & Maintenance Reserve | Save 10% of Rent | -$180 |

| Vacancy Reserve | Save 5% of Rent | -$90 |

| Net Out-of-Pocket Cost to You | -$870 / month |

In this scenario, your tenant is paying $1,800 of your $2,400 mortgage. Your actual out-of-pocket housing cost drops to just $870 a month. You are living in a $350,000 property for cheaper than you could rent a studio apartment. When you eventually move out after a year and rent your unit to a second tenant, the property will cash flow positive.

Step 4: Master Tenant Screening

The success of your investment hinges entirely on who you let live next door. Do not trust your “gut feeling.” You must have a strict, emotionless screening process.

- Income Verification: Require applicants to make at least 3x the monthly rent in gross income. Ask for their last two pay stubs.

- Credit and Background: Use a service like SmartMove or Cozy to run a hard background check. Look for past evictions. An eviction on a record is an immediate, non-negotiable disqualification.

- The Handshake Rule: Never rent to a friend, a coworker, or a family member. When money gets tight, they will leverage your relationship to avoid paying rent, and it will destroy both your friendship and your bank account.

When This Strategy Backfires

Real estate “gurus” on social media sell how to house hack as a flawless, passive income fantasy. It isn’t. You are running a highly regulated business, and if you are naive, the business will crush you. Here is exactly when and why this strategy backfires:

1. The FHA “MIP” Trap

Because you are only putting 3.5% down, the government considers you a high-risk borrower. To protect the lender, the FHA forces you to pay a Mortgage Insurance Premium (MIP) every single month. This can add $150 to $300 to your monthly mortgage payment. Furthermore, on modern FHA loans, this insurance rarely falls off. You often have to completely refinance the property into a conventional loan years later to get rid of the fee. You must include this massive fee when running your cash flow math.

2. Underestimating CapEx (The Furnace Failure)

If you buy a duplex and the furnace dies in January, you cannot tell your tenant to “wait until next payday.” By law, you must provide heat. A new furnace costs $5,000. If you drained your entire bank account to pay the 3.5% down payment and have zero cash reserves left, you will be forced to put that furnace on a high-interest credit card. Mastering how to house hack requires keeping a fully funded cash buffer completely separate from your real estate money.

3. Committing Mortgage Fraud

The FHA loan has a strict owner-occupancy clause. You are legally required to move into the property within 60 days of closing, and you must live there as your primary residence for a minimum of exactly one year. If you buy the duplex with an FHA loan, never move in, and immediately rent out both units, you are committing federal mortgage fraud. The bank can call the loan due immediately and demand the full $400,000 balance in 30 days.

Setting Boundaries as an On-Site Landlord

The hardest part of learning how to house hack isn’t the math; it is the psychology. You are the landlord, the property manager, and the neighbor, all at the exact same time.

If you are too friendly, tenants will take advantage of you. They will knock on your door at 9:00 PM on a Tuesday to complain about a lightbulb. You must establish strict, professional boundaries from day one.

Use dedicated property management software (like Buildium, TenantCloud, or Apartments.com) where tenants log in to pay rent and submit maintenance requests. Never collect rent in cash. Furthermore, many successful investors never tell their tenants that they actually own the building. They simply introduce themselves as the “on-site property manager.” This creates a psychological buffer. When a tenant asks for a break on rent, you simply say, “I wish I could help, but I have to check with the owner.”

Your First Move

House hacking is not a passive investment. You are buying a part-time job.

That means when the toilet breaks, you are responsible for it. When someone is late on rent, you have to initiate the eviction process. But if you are willing to deal with a few leaky faucets and give up a little bit of total privacy for a year or two, mastering how to house hack will fast-track your net worth faster than almost any other strategy on earth.

Your first move is not to aggressively call real estate agents. Your first move is to get your own financial operations in order. Clean up your credit, automate your savings using a Split Direct Deposit, and build that 3.5% cash reserve. Stop paying your landlord’s mortgage, run your math, and go buy your first duplex.

Sources & References

- Federal Housing Administration (FHA) – FHA Loans – Learn about FHA loan requirements, minimum down payments, owner-occupancy rules, and Mortgage Insurance Premium (MIP).

- U.S. Department of Housing and Urban Development (HUD) – Buying a Home – Official homebuyer resources covering FHA financing, homeownership responsibilities, and housing counseling.

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Guidance on mortgages, closing costs, escrow accounts, monthly housing expenses, and managing home loans responsibly.

- Fannie Mae – HomeView® Homebuyer Education – Educational resources explaining mortgage qualification, budgeting for homeownership, and preparing to purchase a home.

- Freddie Mac – My Home by Freddie Mac – Learn about buying multi-family properties, mortgage affordability, and the ongoing costs of homeownership.

- Internal Revenue Service (IRS) – Publication 527: Residential Rental Property – Understand the federal tax rules, deductible expenses, depreciation, and reporting requirements for rental property owners.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.