Real Estate Investing for Beginners: Starting Small with Rental Property

There is a massive, toxic myth floating around the internet: you need to be a multi-millionaire, wear a tailored suit, and have a direct line to Wall Street bankers to buy investment properties.

That might have been true fifty years ago, but today, the game has completely changed. Real estate remains one of the single most powerful vehicles for creating long-term, generational wealth, and it is more accessible right now than it has ever been. You do not need a trust fund. You just need the right education, a solid operational foundation, and a willingness to treat your investments like a real business.

⚡ Quick Answer

Real estate investing allows beginners to build wealth through rental income, appreciation, tenant-paid mortgage reduction, and tax advantages. Common starting strategies include house hacking, REITs, rental properties, syndications, and wholesaling.

Whether you want to generate a few hundred dollars to cover a car payment or build a portfolio of apartment buildings, your success relies on conservative math and strict operational boundaries.

Navigating real estate investing for beginners just comes down to knowing which specific strategy fits your current bank account.

Whether you want to generate passive income or replace your 9-to-5 salary entirely, here is your ultimate masterclass. We are going to break down exactly how the math works, the best entry points, and how to protect yourself from the biggest risks in the market.

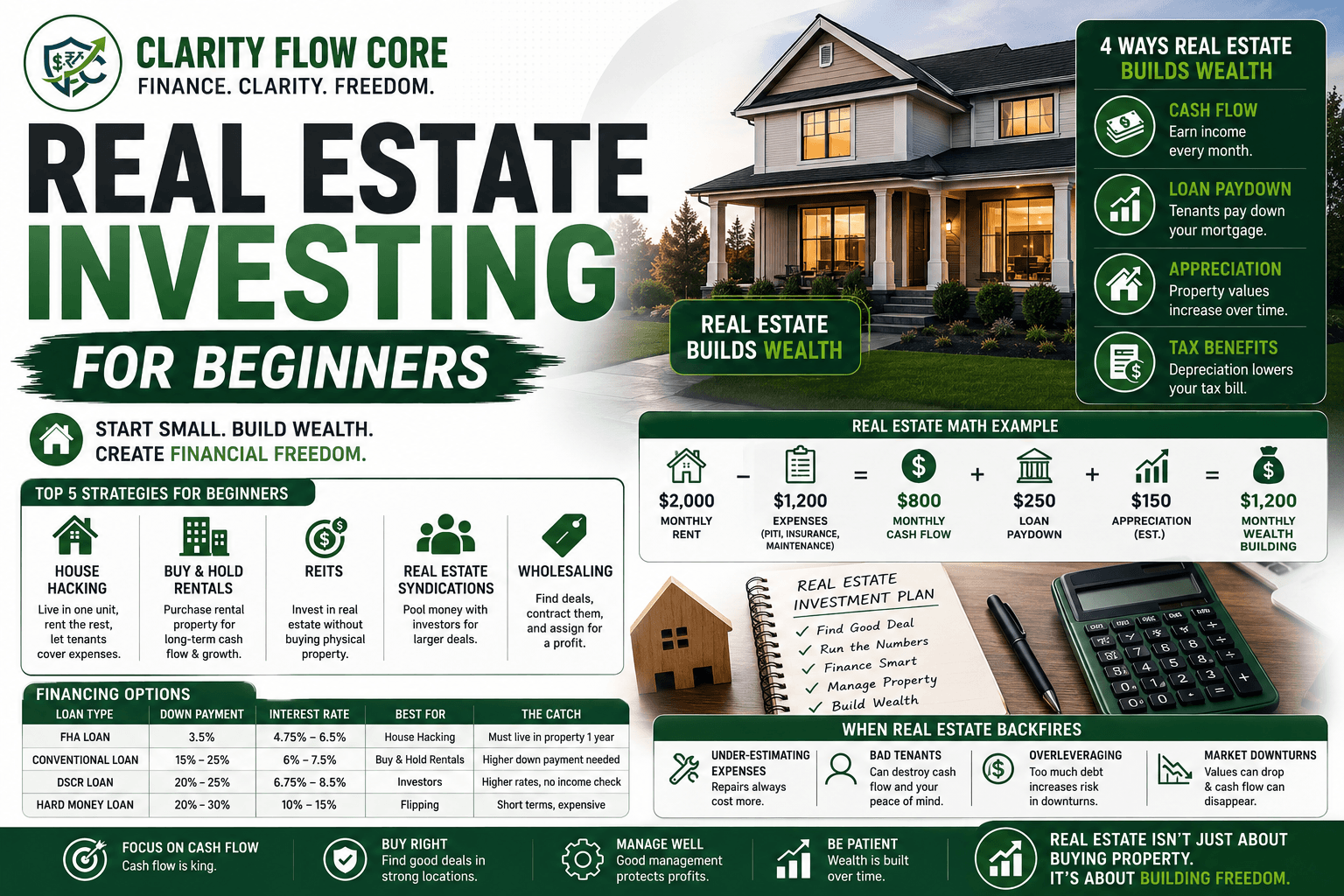

The 4 Wealth Generators of Real Estate

Before we look at how to buy a property, you have to understand why it is the greatest wealth-building tool on the planet. When you invest in the stock market (like buying Index Funds vs. Mutual Funds), you rely on one thing: the asset going up in value.

Real estate, however, pays you in four completely different ways simultaneously.

1. Cash Flow

This is the money left over at the end of the month after all your bills are paid. If your tenant pays you $2,000 a month in rent, and your mortgage, taxes, insurance, and maintenance reserves total $1,500, your cash flow is $500. This is pure, passive income that drops into your bank account every single month.

A Realistic Cash Flow Example:

- Monthly Rental Income: $2,000

- Mortgage (Principal & Interest): -$1,100

- Taxes & Insurance: -$250

- Maintenance Reserve: -$150

- Vacancy Reserve: -$100

- Net Monthly Cash Flow: $400

2. Loan Paydown (Amortization)

When you buy a house with a mortgage, a payment is due to the bank every month. But when you own a rental property, your tenant is making that payment for you. Every month they pay rent, a portion of that money physically pays down the principal balance of your loan. Your debt decreases while your equity automatically increases, and you didn’t have to lift a finger.

3. Appreciation

Over the long term, real estate values go up. While there are certainly market dips, inflation and population growth practically ensure that a house will be worth more in twenty years than it is today. If you buy a property for $300,000 and it appreciates at a highly conservative 4% per year, it will be worth over $440,000 in a decade.

4. Tax Benefits (Depreciation)

The U.S. tax code heavily incentivizes real estate investors. The government allows you to write off the “wear and tear” of your physical building over 27.5 years through a process called depreciation. This means you can legally tell the IRS you lost money on paper, even if your property is cash-flowing thousands of dollars a year. (To ensure you are fully compliant with these advanced write-offs, review What Happens During a Tax Audit?).

Active vs. Passive Investing: Choose Your Path

The biggest mistake people make when exploring real estate investing for beginners is buying a property without deciding if they want a second job or a passive investment.

- Active Investing means you are the one swinging the hammer, finding the deals, screening the tenants, and answering the phone when the toilet breaks at 2:00 AM. It requires a massive time commitment, but the financial returns are significantly higher. Flipping houses and managing your own short-term rentals are prime examples.

- Passive Investing means your money is doing all the heavy lifting. You deploy your capital into an asset, and someone else handles the operations. You sacrifice a portion of your total returns to pay for property managers or syndicators, but you gain complete time freedom.

Top 5 Strategies in Real Estate Investing for Beginners

You do not need to invent a new way to make money in real estate. The blueprints have already been drawn. Here are the five most proven strategies in real estate investing for beginners.

1. House Hacking (The Ultimate Entry Point)

If you have very little cash but want to own physical property, house hacking is your holy grail. (We have an entire deep-dive on this strategy: House Hacking Explained: Using an FHA Loan to Lower Housing Costs).

The concept is brilliantly simple. You buy a multi-family property (like a duplex or triplex) using a low-down-payment primary residence loan. You live in one unit and rent out the others. The rent from your neighbors covers your entire mortgage, allowing you to live virtually for free.

2. REITs (Real Estate Investment Trusts)

Do you want the financial benefits of real estate without dealing with tenants or fixing leaky roofs? Look into REITs.

A REIT is a massive corporation that owns and operates income-producing real estate—think shopping malls, hospitals, or 500-unit apartment complexes. You can buy shares of a REIT on the public stock market exactly like you buy shares of Apple. By law, they must pay out 90% of their taxable income to their shareholders as dividends.

Warning: While REITs are highly accessible, they are still market investments. Share prices can fluctuate wildly during economic downturns, and dividend payments are never guaranteed. Always research the underlying assets.

3. The Classic Single-Family Rental

If you have saved up a 20% down payment and want steady, predictable wealth, buying a traditional single-family house to rent out is a fantastic strategy.

The key here is math, not emotion. You are not buying a house you want to live in; you are buying a math equation. Single-family homes typically attract long-term families, which means less turnover, less wear-and-tear, and fewer headaches for you compared to college-town apartments.

4. Real Estate Syndications

A syndication is simply a fancy word for “crowdfunding.” Let’s say a developer wants to buy a $10 million apartment complex, but they only have $1 million. They will act as the General Partner (doing all the work) and bring in Limited Partners (everyday investors) to fund the rest. As a Limited Partner, you get a percentage of the monthly cash flow. It is completely passive, but it usually requires a minimum investment of $25,000 to $50,000.

5. Wholesaling (High Hustle, Low Cash)

Wholesaling is often pitched as the “no money down” trick in real estate investing for beginners. While you don’t need money, you need an insane amount of hustle.

Your job is to find deeply distressed properties. You get the house under contract for a heavily discounted price—let’s say $100,000. Before the contract closes, you sell the rights to that contract to an experienced house flipper for $110,000. The flipper gets a cheap house to renovate, and you walk away with a $10,000 “assignment fee” without ever actually owning the house.

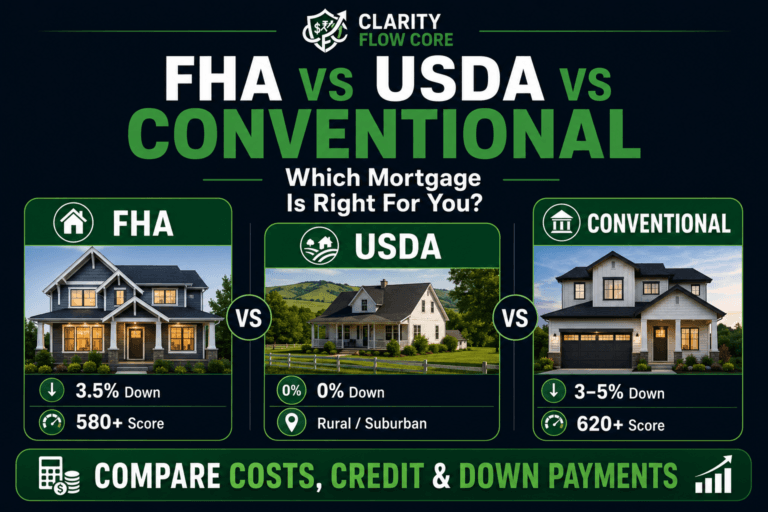

The Math: How to Finance Your First Deal

The biggest hurdle in real estate investing for beginners isn’t finding the property; it is figuring out how to pay for it. Real estate relies heavily on leverage (using the bank’s money to magnify your returns).

| Loan Type | Typical Down Payment | Best Use Case | The Catch |

| Conventional Investment Loan | 20% to 25% | Buying a dedicated rental property you will not live in. | Requires massive upfront cash and strict DTI limits. |

| FHA Loan | 3.5% | House Hacking (You live in one unit). | You must live in the property for at least 12 months. |

| Hard Money Loan | 10% to 20% | Fixing and flipping a destroyed, uninhabitable house. | Astronomically high interest rates; due in short timeframes. |

When you run your financing math, you must account for all hidden costs. Before applying for leverage, review exactly How Mortgage Pre-Approval Actually Works to ensure your debt-to-income ratios meet banking standards.

5 Beginner Real Estate Investing Mistakes

Watching a few reality TV shows about flipping houses can give beginners a dangerous amount of false confidence. Avoid these five critical errors to protect your net worth:

- Buying Based on Emotion Instead of Cash Flow: Do not buy a property just because the kitchen has nice granite countertops. If the math yields a negative monthly return, it is a liability, not an asset.

- Underestimating Repair Costs: Contractors almost always cost more and take longer than expected. Always add a 20% buffer to any renovation estimate.

- Ignoring Vacancy Expenses: Tenants will move out. If your model assumes 100% occupancy for 12 months a year, you will eventually miss a mortgage payment.

- Having No Emergency Reserve: Houses break. If you drain your entire bank account to cover the down payment, a broken water heater will ruin you.

- Overpaying for a Property: You make your money when you buy real estate, not when you sell it. If you pay full retail price in a competitive market, you leave yourself zero margin for error.

When Real Estate Backfires

Real estate is not a get-rich-quick scheme. It is a get-rich-slowly-and-systematically business. If you treat it like a casino, you will lose your shirt. Here is exactly when and why real estate investing for beginners blows up:

1. Underestimating CapEx and Repairs

Beginners always look at a renovation and assume it will take a month and cost $10,000. In reality, it takes three months and costs $25,000. Furthermore, beginners forget to budget for “CapEx” (Capital Expenditures). A roof lasts 20 years. An HVAC lasts 15 years. If you do not have a robust cash reserve—read How Much Emergency Fund Do You Really Need?—a $6,000 AC failure in July will instantly put you into credit card debt.

2. Bad Property Management

A terrible tenant can destroy your profit margins in a matter of weeks through unpaid rent, evictions, and property damage. If you are self-managing, you must run rigorous credit, criminal, and background checks on every single applicant. Never rent to a friend or family member based on a handshake.

3. Over-Leveraging

If you borrow too much money at a high interest rate, a slight dip in rent prices or a prolonged vacancy means you cannot pay the bank. The bank will foreclose, and you will lose everything. Always ensure your cash flow equation is highly conservative. If a property only makes sense if the rent is absolutely maxed out and nothing ever breaks, it is a bad deal.

Frequently Asked Questions (FAQs)

How much money do I need to start investing in real estate?

The amount depends on your strategy. House hacking with an FHA loan may require as little as 3.5% down, while traditional rental properties often require 20% to 25% down.

Is real estate investing risky?

Yes. Risks include vacancies, unexpected repairs, market downturns, and poor tenant selection. Proper cash reserves and conservative financing can dramatically reduce these risks.

What is the easiest real estate investment for beginners?

Many beginners start with REITs because they require very little capital and involve zero property management responsibilities.

Can I invest in real estate without owning property?

Yes. REITs, real estate crowdfunding platforms, and syndications allow investors to participate financially without directly owning or managing the physical buildings.

How do real estate investors make money?

Investors typically earn through a combination of monthly rental income, long-term property appreciation, loan paydown by tenants, and massive tax advantages like depreciation.

Your First Move

Real estate rewards the patient and the meticulously prepared. Your first move in real estate investing for beginners isn’t to start aggressively calling real estate agents.

Your very first move is to get your own operational house in order. You need to build a rock-solid emergency fund and pay off your toxic, high-interest consumer debt. (If you have credit card debt, use the Debt Avalanche vs. Debt Snowball framework to eliminate it immediately).

Once your personal cash flow is protected, you can figure out exactly how much capital you can comfortably deploy. Get your math right, pick your entry strategy, and start building your empire.

References & Trusted Sources

To ensure your investment strategies align with federal lending laws and tax codes, verify your plans using these official resources:

- Consumer Financial Protection Bureau (CFPB) – Mortgages

- U.S. Department of Housing and Urban Development (HUD)

- Federal Housing Administration (FHA) Loan Guidelines

- Internal Revenue Service (IRS) – Tips on Rental Real Estate Income and Deductions

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.