Why Your Escrow Payment Increased Suddenly (And How to Fix It)

⚡ Quick Answer:

If your fixed-rate mortgage payment just jumped, your bank did not raise your interest rate. Your escrow payment increased suddenly because either your local property taxes went up, your homeowner’s insurance premium spiked, or both. Because the bank underestimated these costs last year, your escrow account is now in a deficit. Your new, higher monthly payment is forcing you to pay back last year’s shortage while simultaneously funding the new, higher baseline for next year.

You walk to the mailbox, open an envelope from your mortgage lender, and your stomach immediately drops. You have a 30-year fixed-rate mortgage, but the letter declares that starting next month, your monthly payment is jumping by $500.

The immediate reaction is absolute panic and anger. You specifically chose a fixed-rate loan so your housing costs would be locked in. You assume the bank made a massive clerical error or is illegally altering your interest rate.

They aren’t.

“The bank is not raising your interest rate — it is collecting for taxes and insurance.”

When you see that your escrow payment increased suddenly, it is a highly operational math problem driven by external forces. Your mortgage lender actually makes zero profit off this increase; they are simply the middleman passing the bill along to you.

When I bought my first property, I received one of these “Escrow Analysis” letters nine months after moving in. My payment skyrocketed, completely wiping out my monthly savings margin. I felt blindsided because I was completely blind to The Hidden Costs of Buying a Home: What the Bank Won’t Tell You.

If you are staring at an unexpected mortgage hike and wondering How Much of Your Income Should Go Toward Housing Costs, you must understand the math immediately. Here is the definitive, operational breakdown of why your escrow payment increased suddenly, the brutal math of an escrow shortage, and the exact action steps you can take to fight back.

The Foundation: What is an Escrow Account?

To understand why the bill went up, you must understand what an escrow account actually does.

When you send your mortgage payment to the bank every month, it is not a single lump sum going toward your debt. A standard mortgage payment is divided into four distinct parts, known in the banking industry as PITI:

- Principal: The money that actually pays down your loan balance.

- Interest: The bank’s profit for lending you the money.

- Taxes: Your local municipal and county property taxes.

- Insurance: Your homeowner’s insurance premium.

If you have a fixed-rate mortgage, the Principal and Interest components are locked in stone for 30 years. They will never change.

However, the Taxes and Insurance components are highly variable. Instead of trusting you to save up and pay these massive bills yourself at the end of the year, the bank forces you to pay 1/12th of the estimated annual cost every month. They hold this money in a neutral vault called an Escrow Account. When the city sends the tax bill in December, the bank takes the money out of your vault and pays the city on your behalf.

When your escrow payment increased suddenly, it means the bank looked at the vault and realized there was not enough cash inside to pay the incoming bills. Here are the three distinct reasons why the vault ran dry.

Reason 1: The Property Tax Reassessment Shock

This is the number one reason an escrow payment increased suddenly, and it crushes almost every single first-time homebuyer.

When you were running your numbers through a Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to see what you could afford, you likely looked at the property’s tax history on real estate apps. You saw that the previous owner was paying $3,000 a year in property taxes. Your lender used that $3,000 estimate to set up your initial monthly escrow payment.

This is a fatal mathematical trap.

The previous owner may have purchased the house a decade ago for $150,000. In many states, property taxes are capped and based on that old, lower valuation.

You just bought the house today for $450,000.

Once the deed is recorded, the local municipal tax assessor gets notified of the sale. They see the new purchase price and execute a “Tax Reassessment.” They legally update the value of the home on the county records to match your $450,000 purchase price.

The following year, your property tax bill doubles from $3,000 to $6,000. When the city sends that massive new bill to your bank, the bank drains your escrow account to pay it, triggering a massive shortage.

Reason 2: The Homeowner’s Insurance Crisis

If you have owned your home for several years and your escrow payment increased suddenly, you are likely a victim of the current insurance market.

Homeowner’s insurance is not a fixed cost. Over the last few years, the cost to insure a property has skyrocketed globally due to two primary factors:

- Replacement Cost Inflation: The cost of lumber, copper piping, roofing materials, and construction labor has surged. If your house burns down today, it costs the insurance company vastly more to rebuild it than it did three years ago. They raise your premiums to cover this inflated risk.

- Catastrophic Weather Events: As natural disasters (hurricanes, wildfires, massive hail storms) become more frequent and expensive, insurance companies suffer massive corporate losses. To stay solvent, they aggressively raise rates across the board—even for homeowners who live in safe areas and have never filed a claim.

If your insurance premium jumps significantly, the bank is short on cash every month. They must raise your escrow payment to cover the new, inflated premium.

Reason 3: Losing a Tax Exemption

Sometimes, an escrow payment increased suddenly because you lost a legal tax shield that the previous owner had perfectly maintained.

Most states offer a “Homestead Exemption,” which significantly lowers the taxable value of your property if it is your primary residence. There are also specific, heavy tax discounts for senior citizens, military veterans, and disabled individuals.

If you buy a house from a disabled veteran, their property tax bill was likely incredibly low because of their protected legal status. When you buy the home, those specialized exemptions do not automatically transfer to you. The tax bill resets to full retail price.

Furthermore, if you forget to file the basic Homestead Exemption paperwork with your county during your first year of homeownership, you will be taxed at the maximum possible rate, triggering an immediate and severe escrow deficit.

The Math: Why the Increase is So Aggressive (The Double Whammy)

This is the hardest part of the process to understand. When your escrow payment increased suddenly, you might notice that the math feels entirely disproportionate.

When the bank runs their annual analysis and realizes property taxes or insurance spiked, they find two distinct problems they have to fix simultaneously:

- The Deficit (The Past): Because the bank was collecting the old, lower amount all year, but had to pay the new, higher tax bill in December, your escrow account went into the negative. You owe them money to refill the hole you already dug.

- The New Baseline (The Future): Now that the bank knows the taxes are permanently higher, they must collect the new, higher amount moving forward for next year’s bill.

This creates the “Double Whammy.” You are forced to pay for the past mistake while simultaneously funding the more expensive future.

The Brutal Escrow Math

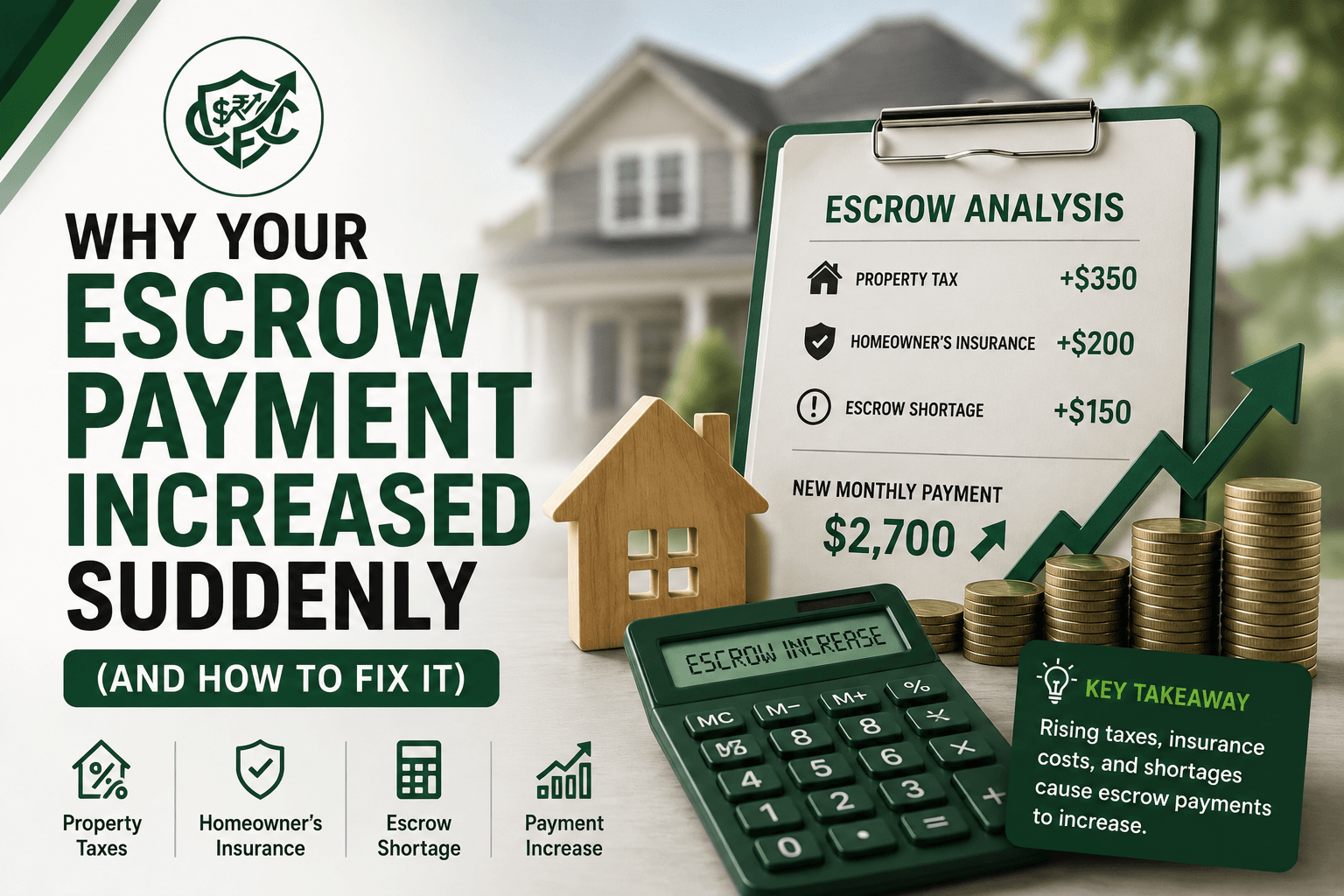

Here is a real-world breakdown of exactly how a $2,200 mortgage can skyrocket to $2,700 overnight:

| Stage | Amount |

| Initial Mortgage | $2,200 |

| Property Tax Increase (Funding the Future) | +$350 |

| Escrow Shortage Recovery (Paying for the Past) | +$150 |

| New Payment | $2,700 |

The RESPA Cushion

To make matters slightly worse, federal law (RESPA) allows banks to require a two-month “cushion” in your escrow account at all times to prevent future shortages. If your taxes went up, the required baseline for that two-month cushion also went up. The bank will add a few extra dollars to your monthly increase simply to pad the emergency reserve.

When This Backfires: The Operational Traps

When people receive an escrow shortage notice, panic often causes them to make irrational, emotional financial decisions. If you react incorrectly, you will accelerate the damage. Here is exactly when your reaction backfires:

1. Ignoring the Shortage Letter

Some homeowners see the massive lump-sum shortage amount on the letter and simply throw the paper in the trash, hoping the bank will forget. They won’t. If you ignore the letter, the bank will automatically enact the default option: they will aggressively increase your monthly mortgage payment to recover the shortage over 12 months. If you do not track this in a Smart Budget Planner & Cash Flow Analyzer and your checking account runs dry, your automatic mortgage payment will bounce, triggering severe late fees and destroying your credit score.

2. Under-Insuring to Save Cash

When faced with skyrocketing insurance premiums, some homeowners try to lower their escrow payment by cutting their insurance coverage to the absolute minimum. They raise their deductible to $10,000 or drop their dwelling coverage below the replacement cost of the home.

⚠ Warning: Lowering insurance coverage to reduce escrow payments can expose homeowners to catastrophic financial losses after disasters or major damage claims. You are saving $50 a month but risking a $200,000 total loss if a fire destroys the property. Learn Practical Ways to Lower Insurance Costs Without Cutting Coverage instead of compromising your core protection.

3. Assuming the Bank Made a Math Error

Homeowners frequently waste hours screaming at bank customer service representatives, accusing them of stealing money. The bank did not make a mistake. The bank does not determine your taxes, and they do not set your insurance rates. They simply pay the invoices mailed to them by the city and the insurance carrier. If you want to be angry, you must direct that anger at the county tax assessor or the insurance underwriter.

The Operational Fix: Your Action Plan

If your escrow payment increased suddenly, you have a specific, operational action plan you must execute to stabilize your cash flow.

Step 1: Choose Your Shortage Payment Method

The bank will give you two options to cure the negative deficit in your escrow account.

- Option A (The Lump Sum): You can write a single check today for the exact amount of the shortage from your savings. If you do this, your monthly payment will still go up slightly to cover the new baseline, but you avoid the painful “double whammy” shortage recovery fee. This is why reading How Much Emergency Fund Do You Really Need? is critical before buying a house.

- Option B (The Spread): If you do not have the liquid cash, do nothing. The bank will automatically divide the shortage by 12 and add it to your monthly payment for the next year. It requires zero upfront cash, but it squeezes your monthly budget tightly. (Pro Tip: If spreading the cost makes your monthly budget unaffordable, you may need to free up cash elsewhere. Re-evaluating a heavy auto loan via our Leasing vs. Buying Used Cars: Which Actually Costs Less? guide is often the fastest way to absorb a new $500 housing expense).

Step 2: Aggressively Shop Your Insurance

Because you cannot easily change your property taxes, you must attack the insurance premium.

Do not accept a 30% rate hike from your current insurance carrier without a fight. Call an independent insurance broker in your city. An independent broker can instantly shop your policy across 15 different carriers to find the exact same coverage for a cheaper price. If you find a cheaper policy, sign the paperwork, and the new insurance company will automatically notify your bank to update the escrow baseline.

Step 3: File Your Homestead Exemption

If you bought the house last year, verify immediately with your county tax assessor’s website that your Homestead Exemption is actively filed and approved. If you missed the deadline, file it immediately so your tax burden drops for the next calendar year.

Step 4: Protest Your Property Taxes

If the county tax assessor claims your house is worth $500,000, but you just bought it for $420,000, you are being over-taxed.

Every county has a specific window (usually in the spring) where you can legally protest your property valuation. You file an appeal with the county, provide your recent appraisal or purchase contract as evidence, and demand they lower the assessed value. If you win the appeal, the city will issue a revised, lower tax bill, which will eventually force the bank to lower your escrow requirement.

Frequently Asked Questions (FAQs)

1. Can I cancel my escrow account and pay the bills myself?

Sometimes, but it depends on your loan. If you have an FHA loan or a VA loan, escrow accounts are strictly mandated by federal law; you cannot cancel them. If you have a Conventional Loan and have built up at least 20% equity in the property, you can often submit a written request to the bank to “waive escrow.” If approved, your monthly payment will drop to just principal and interest, but you are now 100% responsible for saving cash and paying the massive tax and insurance bills yourself.

2. Did my actual mortgage interest rate go up?

If you have a Fixed-Rate Mortgage, absolutely not. Your interest rate and principal payment are locked for the life of the loan. The only components of your payment that increased were the taxes and insurance. (Note: If you have an Adjustable-Rate Mortgage or ARM, your interest rate can increase, which is a separate issue entirely).

3. Will my escrow payment ever go back down?

Yes. The “Double Whammy” of recovering a shortage only lasts for 12 months. Once the 12-month recovery period is over, the shortage is paid off. The following year, your monthly payment will mathematically drop back down to the new baseline (assuming your taxes and insurance do not spike again).

4. What is an escrow cushion?

Federal law (RESPA) allows banks to keep an emergency reserve in your escrow account—typically equal to two months of escrow payments. This cushion ensures that if your tax bill goes up slightly, the bank has enough cash on hand to pay the city without instantly triggering a severe shortage.

5. Who do I call if my escrow analysis looks completely wrong?

First, check the math. Compare the tax and insurance amounts on the bank’s analysis letter against the actual bills mailed to you by the city and your insurance carrier. If the bank accidentally paid the wrong house’s tax bill (which happens rarely), you must call your mortgage servicer’s “Escrow Department” immediately to launch an investigation.

The Bottom Line

Opening a letter to find that your escrow payment increased suddenly is one of the most frustrating rites of passage for a homeowner. It feels deeply unfair, but it is entirely predictable if you understand the mechanics of local taxation and the insurance market.

Stop assuming the bank is stealing from you, and start executing your operational defense. Understand the “double whammy” math, decide whether to pay the lump sum or spread the shortage, and aggressively shop your homeowner’s insurance policy. By proactively managing your home’s operational costs, you ensure that your property remains a wealth-building asset, rather than a monthly financial crisis.

Homeowner Resources

Unexpected escrow increases are usually tied to changes in property taxes or homeowners insurance—not your mortgage interest rate. These trusted resources can help you understand escrow accounts, property taxes, and your rights as a homeowner.

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Learn how escrow accounts work, what mortgage servicers are responsible for, and how changes in taxes or insurance affect your monthly payment.

- Consumer Financial Protection Bureau (CFPB) – Mortgage Servicing Rules – Official guidance on escrow account disclosures, annual escrow analyses, and homeowner protections under federal law.

- U.S. Department of Housing and Urban Development (HUD) – Find HUD-approved housing counselors who can help you understand mortgage payments, escrow accounts, and homeowner assistance options.

- National Association of Insurance Commissioners (NAIC) – Consumer resources on homeowners insurance, shopping for coverage, and understanding premium increases.

- Federal Housing Finance Agency (FHFA) – Educational resources for homeowners on mortgage servicing, homeownership, and housing finance.

- Fannie Mae – HomeView® – Free homeowner education covering escrow accounts, property taxes, insurance, and the ongoing costs of owning a home.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Every individual’s financial situation is unique. Always consult with a qualified financial professional or housing counselor before making major financial decisions.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.