How Sinking Funds Protect Your Emergency Savings

The problem with most emergency funds is that we use them for things that aren’t actual emergencies. Instead of using sinking funds for predictable bills, we aggressively drain our safety nets and then wonder why we always feel broke.

If you own a car, needing new tires isn’t an emergency. It’s a statistical guarantee. You should definitely understand your Emergency Fund Basics: How Much Cash Should You Keep?, but that money is for catastrophic, unpredictable events like a sudden job loss or a massive medical crisis—not routine maintenance.

When that $800 tire bill hits, you probably pull it from your main savings account. You spend the next three months aggressively building that balance back up. Then you get hit with a $1,200 annual insurance premium. Your balance drops again.

This cycle of saving and draining is exhausting. It makes you feel like you are bad at managing money.

The fix isn’t to restrict your spending further or force yourself to Actually Finish a 30-Day No-Spend Challenge every time a bill arrives. The fix is to separate your “unknown risk” money from your “known upcoming expenses.” That is exactly what a sinking fund does.

⚡ Quick Answer

A sinking fund is money set aside for predictable future expenses like car repairs, insurance premiums, holiday spending, or home maintenance. Unlike an emergency fund, which protects you from unexpected financial disasters, a sinking fund helps you prepare for expenses you know are coming. Using sinking funds prevents routine bills from draining your emergency savings.

Sinking Funds vs. Emergency Funds

A sinking fund is money you set aside each month for a specific, predictable expense that doesn’t happen monthly. Instead of getting blindsided by a massive bill in December, you save for it in small increments all year long.

Here is how the two types of savings differ in practice:

| Feature | Emergency Fund | Sinking Fund |

| Purpose | Unknown events (job loss, medical) | Irregular expenses (holidays, property taxes) |

| Target Balance | 3 to 6 months of living expenses | Exact amount of the upcoming bill |

| Psychology | You hope you never have to use it | You are actively planning to spend it |

Life Without Sinking Funds vs. Life With Sinking Funds

To truly understand the power of this system, let’s look at a practical example of how irregular expenses destroy a standard budget.

Without Sinking Funds (The Reactionary Approach):

- October: The $1,200 annual auto insurance bill arrives. You don’t have it in checking, so it goes on a credit card at 24% interest.

- December: You need $1,000 for holiday gifts and travel. You drain your emergency fund to pay for it.

- January: Your car needs $600 in repairs. Your emergency fund is empty. You are forced into panic mode and high levels of stress.

With Sinking Funds (The Proactive Approach):

- October: The insurance bill arrives. The $1,200 is already sitting in a dedicated savings account because you saved $100 a month for the last year. You pay it in cash.

- December: The $1,000 for holiday gifts is fully funded. You buy the gifts without touching a credit card.

- January: The car needs repairs. The auto-maintenance fund covers it easily. Your emergency fund remains completely untouched. Cash flow remains stable.

Common Sinking Funds Worth Creating

You do not need to create a fund for every possible life scenario, but you should target the bills that routinely blow up your checking account. Here are the most common irregular expenses that require sinking funds:

| Category | Typical Annual Cost |

| Car Repairs & Maintenance | $500–$2,000 |

| Car Insurance Premiums | $600–$2,000 |

| Holiday Gifts & Travel | $500–$2,500 |

| Annual Property Taxes | Variable based on location |

| Home Maintenance | 1–3% of home value annually |

| Pet Expenses (Vet visits) | $300–$1,000 |

| Technology Replacement | $500–$2,000 |

(Note: If you are trying to free up cash flow to fund these accounts, ensure you are not overpaying on your current premiums by reading How to Save on Insurance Without Cutting Your Coverage).

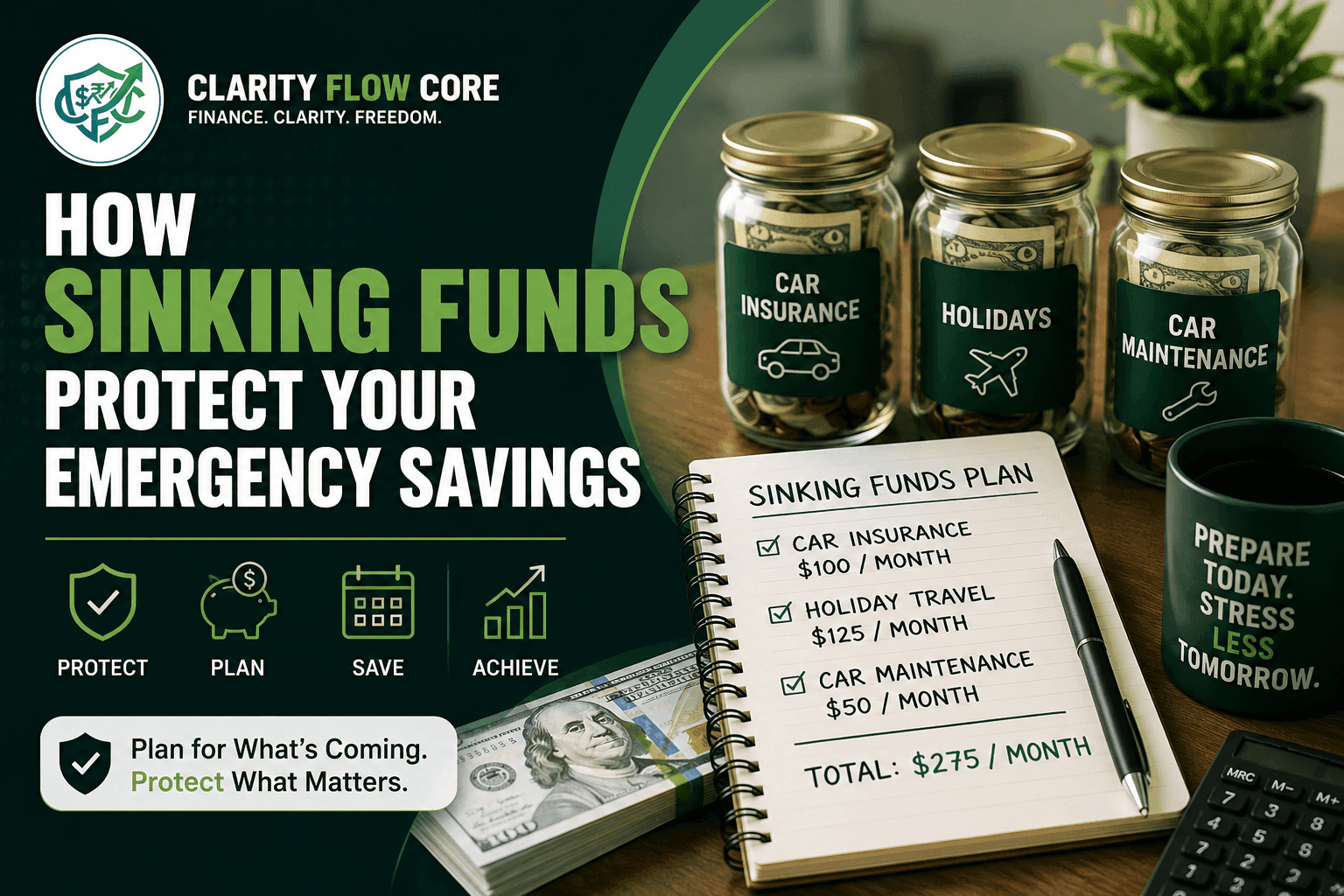

The Math: Breaking Down the Sinking Fund

Let’s look at a realistic scenario. Suppose you have three major non-monthly expenses coming up this year.

If you try to cash-flow these out of your regular monthly checking account, a month like October (when insurance is due) will completely break your budget—even if you strictly follow The 50/30/20 Budget Rule Explained Simply.

Instead, calculate the monthly sinking fund contribution by dividing the total need by 12 months:

| Expense | Annual Cost | Monthly Savings Goal |

| Car Insurance | $1,200 | $100 |

| Holiday Travel & Gifts | $1,500 | $125 |

| Routine Car Maintenance | $600 | $50 |

| Total | $3,300 | $275 |

Once you know the math, you must separate the cash. Route that $275 every month directly into a separate account. When October arrives, that $1,200 insurance bill is already sitting there waiting to be paid. Your main checking account doesn’t feel it, and your emergency fund remains untouched.

You can use the calculator below to quickly break down your own irregular expenses into manageable monthly goals.

How Many Sinking Funds Should You Have?

This is a common question that trips up beginners. While the math above is clean, how do you actually structure the accounts?

- Start with 3–5: Focus entirely on your largest, most painful annual expenses first (like property taxes, auto insurance, and holidays).

- Consolidate Smaller Categories: Do not open a separate bank account for a $150 annual software subscription. Roll smaller items into a general “Annual Subscriptions” fund.

Where Should You Keep Sinking Funds?

If you leave your sinking fund money in your primary checking account, you will accidentally spend it on groceries or takeout. The money must leave your main account.

Because you know exactly when you will need this money, it does not need to be locked away in a rigid investment account. The smartest place to park sinking funds is in a high-yield account that pays you interest while the money waits. Consider reading HYSA vs. Money Market Account: What’s the Difference? to find a secure vehicle that earns a strong yield.

Once the account is open, automate the process. Check out our guide on How to Automate Savings Using Split Direct Deposit so the money routes to your sinking fund invisibly, before you can ever spend it.

When This Backfires

Sinking funds are the most effective way to smooth out a jagged cash flow. But the strategy can quickly fall apart if you make these common mistakes:

- Account Clutter: Some people get overly excited and create 15 different sinking funds. One for clothes, one for haircuts, one for coffee. Managing that many accounts becomes a part-time job. Keep it to 3 to 5 major categories.

- Borrowing from Peter to Pay Paul: You fully funded your “Holiday” sinking fund, but suddenly you want a new laptop. You transfer the money out, promising yourself you’ll refill it before December. You won’t. If you cross-contaminate the funds, the system breaks.

- Ignoring Preventative Habits: Having a car maintenance fund does not mean you should stop changing your oil. Implementing 7 Everyday Saving Habits That Can Make a Real Difference protects these accounts from draining prematurely.

Frequently Asked Questions (FAQs)

Are sinking funds the same as emergency funds? No. Emergency funds cover unexpected financial emergencies (job loss, major medical events), while sinking funds cover highly predictable future expenses (insurance, holidays, taxes).

How many sinking funds should I have? Most people only need 3 to 5 major sinking funds covering their largest irregular expenses. Too many funds become overly complicated to manage.

Should sinking funds earn interest? Yes. High-yield savings accounts and money market accounts are often great places to keep sinking fund money so it grows while waiting to be spent.

Can I use one account for multiple sinking funds? Yes. Many people track their separate sinking fund categories using a spreadsheet or budgeting app while actually keeping all the physical money pooled in a single high-yield savings account.

What is the best sinking fund to start first? Car repairs, annual insurance premiums, and holiday spending are often the most useful starting categories because they cause the most frequent budget disruptions.

The Bottom Line

The purpose of a sinking fund is not necessarily to save more money. It is to make the money you already have far more organized.

When you stop using your emergency fund for predictable expenses, your finances become significantly less stressful. Large annual bills no longer feel like emergencies because you mathematically planned for them months in advance.

A simple system of sinking funds allows you to protect your true emergency savings, smooth out your monthly cash flow, and gain absolute control over your financial life.

References & Trusted Sources

To ensure your savings strategies align with standard banking practices and consumer protection guidelines, consult these official resources:

- Consumer Financial Protection Bureau (CFPB) – Budgeting Resources

- FDIC – Savings Resources

- Federal Reserve – Household Financial Well-Being Studies

- Consumer Reports – Vehicle Ownership Costs

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.