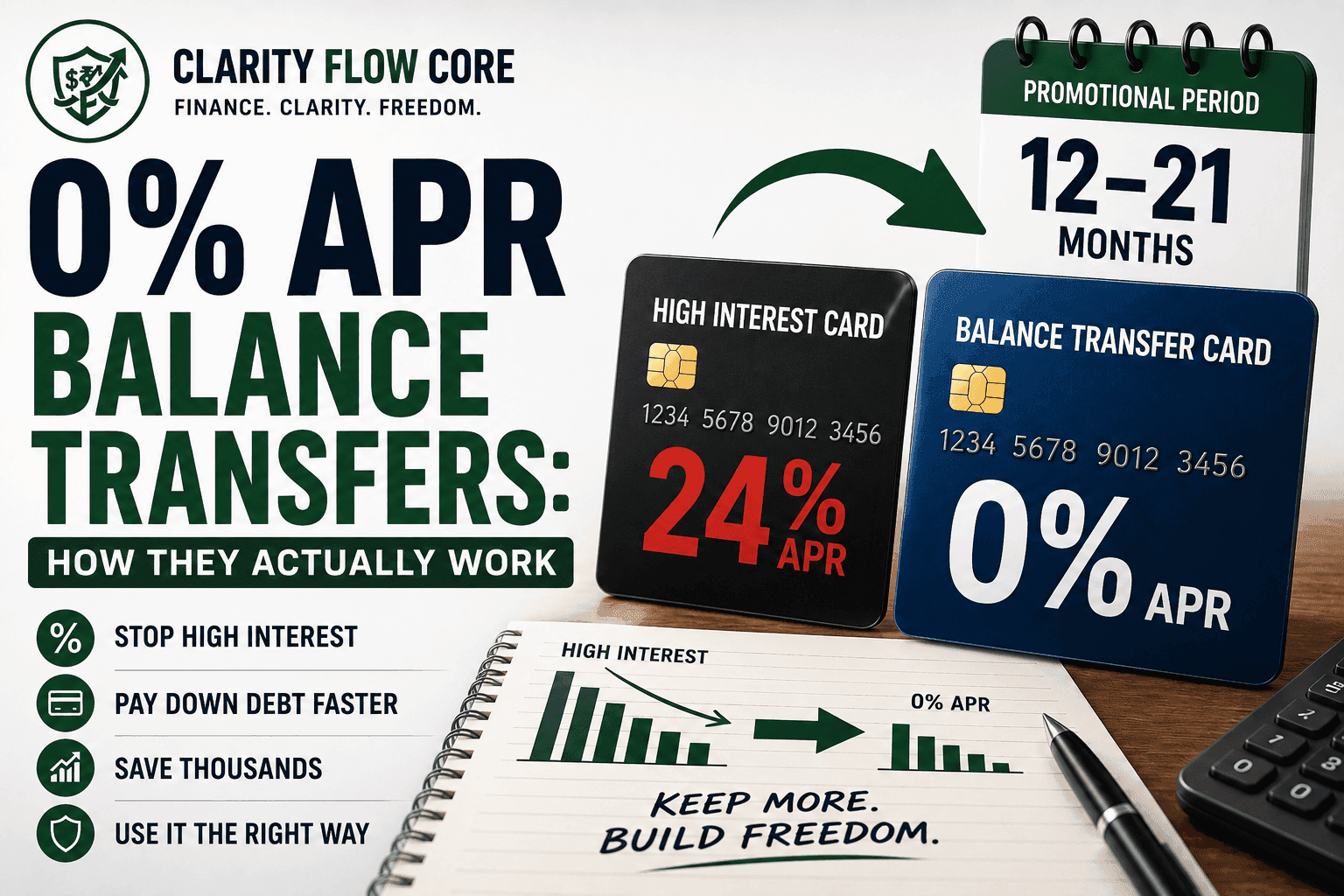

0% APR Balance Transfers: How They Actually Work

If you are carrying a credit card balance at a 24% interest rate, your minimum payment is no longer paying off debt—it is simply paying for the privilege of keeping the account open. When 20% to 30% of your monthly payment is immediately vaporized by interest charges, fighting your way to a zero balance without a 0% APR balance transfer feels mathematically impossible.

A 0% APR balance transfer is not a magic eraser, and it does not forgive your debt. What it does is pause the compounding math. By moving your high-interest debt to a specialized promotional card, you stop the bleeding. For a set period—usually 12 to 21 months—every single dollar you send to the bank goes directly toward destroying the principal.

⚡ Quick Answer

A 0% APR balance transfer allows you to move existing high-interest credit card debt to a new card offering a temporary 0% interest promotion. You typically pay a one-time transfer fee, but every payment during the promotional period goes directly toward reducing the principal balance.

Here is the actual math behind how these transfers work, how to execute the move without damaging your credit, and the common traps that cause this strategy to backfire.

The Math: Why the Transfer Makes Sense

To understand why a balance transfer is such a critical tool, you have to look at the raw numbers. Credit card companies rely on daily compounding interest.

Let’s say you have a $10,000 balance on a card with a 24% APR. You can afford to pay $250 a month.

If you leave the debt where it is, it will take you over five and a half years to pay it off, and you will hand the bank nearly $9,000 in interest.

Now, let’s look at the 0% APR balance transfer route. You open a new card offering 0% APR for 18 months. The bank charges a standard 3% transfer fee upfront to move the money. That fee ($300) gets added to your principal, meaning your new starting balance is $10,300.

Here is how those two scenarios compare:

| Strategy | Starting Debt | Monthly Payment | Time to Payoff | Total Cost (Interest + Fees) |

| Do Nothing (24% APR) | $10,000 | $250 | 68 Months | $8,895 in interest |

| 0% APR Transfer (3% Fee) | $10,300 | $572 (Aggressive) | 18 Months | $300 transfer fee |

By paying a one-time $300 fee, you avoid nearly $9,000 in future interest. To make this work optimally, you ignore the $250 payment and aggressively increase it to $572 a month. In exactly 18 months, you are completely debt-free.

How to Execute a 0% APR Balance Transfer

You have to execute a balance transfer carefully. If you skip a step or misunderstand the bank’s rules, you can accidentally void the promotional rate.

Step 1: The Cross-Bank Rule

You generally cannot transfer a balance between two cards from the same bank. If you have $5,000 of debt on a Chase card, Chase will not let you execute a 0% APR balance transfer to a new Chase promotional card. You must find a product from a competitor, like Citi, Discover, or Wells Fargo.

Step 2: Check Your Credit Profile

To qualify for the longest promotional periods (15 to 21 months), you need a strong credit history. Generally, borrowers with good to excellent credit profiles are more likely to qualify for the longest promotional periods and highest credit limits. If your score is lower, you may still get approved, but for a shorter 0% window (like 6 to 9 months) and a lower credit limit.

Step 3: Calculate the Breakeven Point

Always do the math before applying for a 0% APR balance transfer. If you only owe $1,000 and plan to pay it off in two months, the interest on your current card might only be $40. A 5% transfer fee on $1,000 is $50. In that scenario, paying the fee actually costs you more than staying put. Only transfer debt that will take you more than a few months to clear. (Not sure how much damage a minimum payment does? Read What Happens If You Only Pay the Minimum on a Credit Card?).

Step 4: Keep Paying the Old Card

This is a critical operational detail. When you initiate the transfer on your new bank’s dashboard, the payment is not instantaneous. It can take three days to three weeks for the new bank to electronically send the funds to your old bank. Do not stop paying your old card. Keep making the minimum payments until you physically see the balance hit $0.00 on your old statement.

When This Backfires

A 0% APR balance transfer is highly effective, but the financial institutions offering them are banking on the fact that a large percentage of customers will mess up. If you make these mistakes, the strategy collapses:

- Missing a Single Payment: The 0% APR is a conditional contract. Depending on the card agreement, missing a payment may cause you to lose promotional terms and incur higher interest charges. Put your minimum payment on autopay the day you activate the card.

- The Phantom Debt Trap: You successfully execute a 0% APR balance transfer and move your $10,000 debt to the new card. Your old credit card now has a zero balance and a $10,000 limit of free space. It is incredibly tempting to start putting groceries, gas, or dinners on that old card again. If you haven’t fixed the spending habits that caused the debt in the first place, you will end up with maxed-out balances on both cards. (Learn how to break this cycle by reading How the Debt Snowball Method Works for Credit Card Debt).

- Mixing New Purchases with Transferred Debt: Do not use your new 0% APR balance transfer card to buy things. Often, the 0% promotion applies strictly to the transferred debt, not new purchases. If you buy a $500 TV on the new card, that specific purchase may start accruing 24% interest immediately. Treat the balance transfer card like a quarantine zone for old debt, not a tool for new spending.

- The “Deferred Interest” Mirage: Be certain you are applying for a true 0% APR credit card and not a “deferred interest” store card (common at furniture and electronics retailers). With a true 0% APR card, if you have $100 left over when the promotion ends, you only pay interest on that remaining $100 moving forward. With a deferred interest card, if you leave even $1 unpaid, the bank back-charges you all the interest that would have accrued from day one.

When Is a Balance Transfer NOT Worth It?

Balance transfers are powerful, but they aren’t the right solution for every financial scenario. You should likely avoid a balance transfer if:

- You have small balances that can easily be repaid in a few months (the transfer fee will outweigh the interest saved).

- You have poor credit that won’t qualify for promotional offers or a high enough limit to absorb the debt.

- Your debt is caused by ongoing overspending that you haven’t reigned in yet. Opening a new line of credit will only worsen the issue.

- Situations where monthly payoff goals exceed your budget, meaning you will barely make a dent in the principal before the 0% promotion expires.

Adding the Debt Snowball Synergy

A balance transfer is a multiplier for your overall debt payoff strategy.

If you are using the Debt Snowball Method (where you focus all your extra cash on paying off your smallest debt first for psychological momentum), a 0% APR balance transfer is the perfect place to park your largest, most intimidating balance. (Want to compare the math vs. the psychology? Read Debt Avalanche vs Debt Snowball: Which Strategy Saves More Money?).

While you aggressively attack your smaller credit cards, personal loans, or medical bills, your massive credit card balance sits safely frozen at 0%. It isn’t growing. The compound interest is neutralized. Once the smaller debts are cleared, you can pivot your entire financial arsenal toward the balance transfer card, rapidly destroying the principal before the promotional clock runs out.

Frequently Asked Questions (FAQs)

Does a balance transfer hurt your credit score?

Applying for a new card may cause a temporary dip due to a hard inquiry, but lower utilization can improve your score over time.

What happens when the 0% period ends?

Any remaining balance begins accruing interest at the card’s standard APR.

Can I transfer multiple credit cards to one balance transfer card?

Often yes, if the new card’s credit limit is high enough to accommodate the combined balances and the transfer fees.

How long do balance transfer offers last?

Promotional periods commonly range from 12 to 21 months, though terms vary by issuer.

Is a balance transfer better than a personal loan?

It depends on the interest rate, fees, and payoff timeline. Balance transfers are often best for short-term aggressive payoff plans, while fixed-rate personal loans are better for debts that will take several years to clear.

References & Trusted Sources

To verify current federal regulations regarding credit card fees, interest rates, and promotional terms, consult these official resources:

- Consumer Financial Protection Bureau (CFPB) – Credit Card Balance Transfers

- Federal Trade Commission (FTC) – Credit Card Terms and Fees

- CFPB – Credit Card Interest and APRs

- Federal Reserve – Consumer Credit Reports

The Bottom Line

A 0% APR balance transfer does not eliminate debt, but it can dramatically improve the math working against you. By replacing high-interest compounding with a temporary 0% promotional period, you gain time to focus on reducing principal rather than feeding interest charges.

The strategy works best when paired with disciplined budgeting, automatic payments, and a clear payoff plan. Used correctly, a balance transfer can save thousands of dollars and accelerate your path to becoming debt-free. Once the balance is cleared, protect your financial profile moving forward by understanding What Is Credit Utilization and Why Does It Matter? and reading our breakdown on FICO vs VantageScore: Why Credit Scores Differ Between Apps.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

5 Comments

Comments are closed.