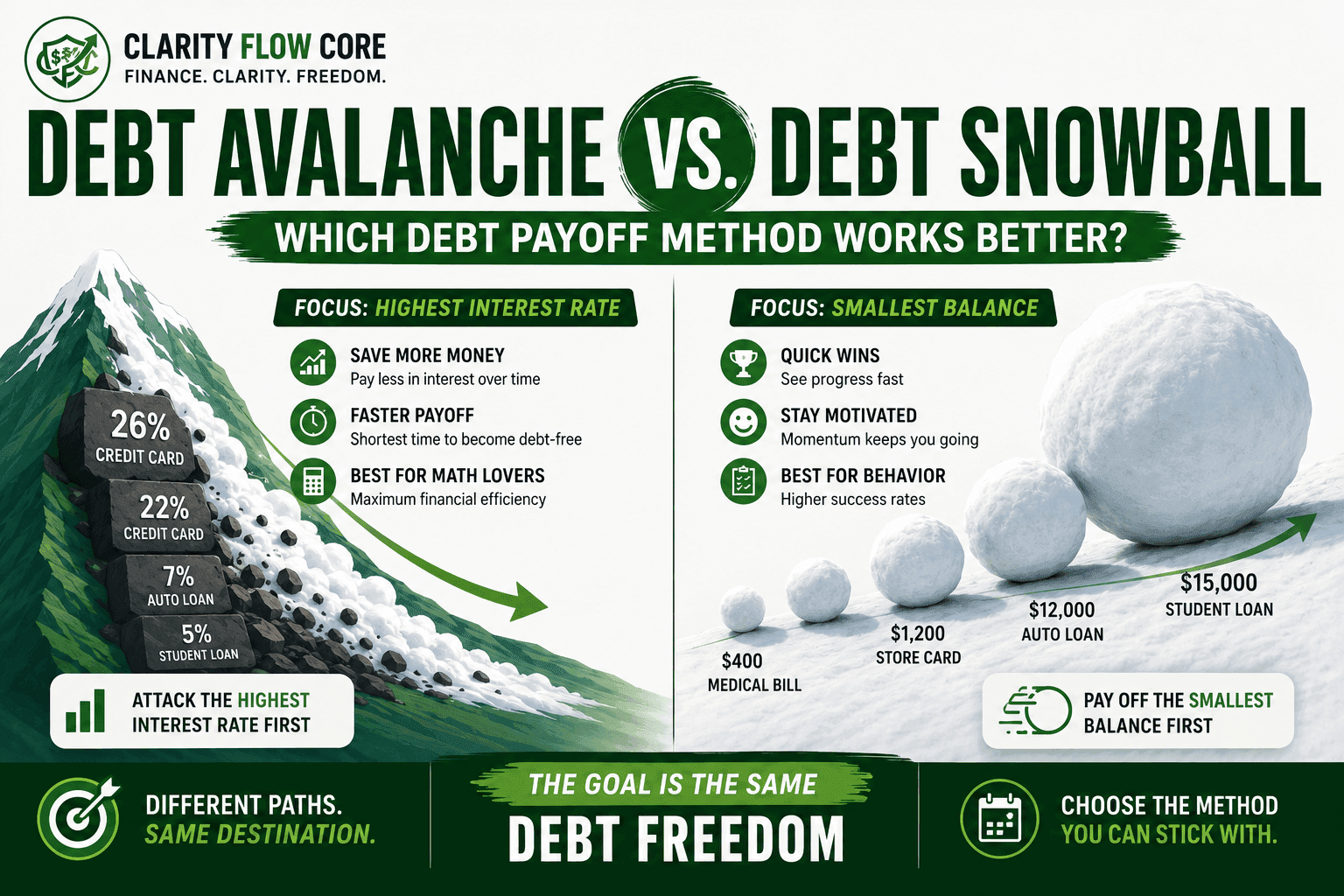

Debt Avalanche vs. Debt Snowball: Which Debt Payoff Method Works Better?

When deciding how to finally crush your credit card balances, the choice almost always comes down to the debt avalanche vs debt snowball method.

I vividly remember sitting at my kitchen table, staring at a stack of bills. I had four different balances across four different cards. Every time payday rolled around, I would try to spread my extra cash evenly across all the accounts, hoping to see the balances drop.

It felt like trying to empty a swimming pool with a teaspoon. Months went by, and the balances barely moved. If you are trying to dig your way out of consumer debt, you already know that “just paying a little extra” does not work. You need a targeted, ruthless strategy.

⚡ Quick Answer

- Debt Snowball pays off debts from the smallest balance to the largest, creating quick psychological wins.

- Debt Avalanche pays off debts from the highest interest rate to the lowest, minimizing total interest costs.

- The Verdict: The best method is the one you can consistently follow until all debt is eliminated.

Debt Snowball vs. Debt Avalanche: A Direct Comparison

| Feature | Debt Snowball | Debt Avalanche |

| Priority | Smallest Balance | Highest Interest Rate |

| Main Benefit | Motivation | Saves More Money |

| Fastest Psychological Wins | ✅ | ❌ |

| Lowest Interest Cost | ❌ | ✅ |

| Best For | People needing momentum | Highly disciplined savers |

When deciding how to attack your accounts, the debate almost always comes down to the debt avalanche vs debt snowball. Both strategies work, but they approach the problem from two completely different angles. One uses pure mathematics, and the other relies on behavioral psychology.

Here is exactly how both methods operate, the real-world math behind them, and how to choose the strategy that will actually get you to a zero balance.

The Foundation: What Both Methods Have in Common

Before we compare the debt avalanche vs debt snowball, you must understand the golden rule that makes both of them function.

No matter which method you choose, the baseline operational strategy is identical:

- You pay the absolute minimum payment on every single debt you owe, except for one.

- You take every extra dollar you can find in your budget and aggressively attack that single “target” debt.

- Once that target debt hits zero, you take the money you were throwing at it and roll it into the next target.

The only difference between the debt avalanche vs debt snowball is how you choose that target.

The Debt Snowball Method (The Psychological Win)

Popularized by financial experts who study human behavior, the Debt Snowball strategy ignores interest rates entirely. Instead, it focuses on giving you quick psychological victories to keep you motivated.

How it works:

You list all your debts from the smallest balance to the largest balance, regardless of the interest rate. You throw every spare dollar at the smallest balance until it hits zero, and then roll that payment into the next smallest.

Traditional finance professors hate this method because it isn’t mathematically perfect. But behavioral economics tells us a different story: human beings are not perfectly rational calculators. If we were rational, we wouldn’t be sitting in credit card debt in the first place.

Many financial experts argue that behavior plays a larger role in debt payoff success than mathematical optimization alone. The Debt Snowball is highly effective because it hacks your brain’s dopamine system. By attacking the smallest balance first, you might be able to completely eliminate a debt in just three or four weeks. When you see a balance hit zero, you get a massive psychological high.

The Snowball Math:

Let’s say you have $500 extra a month to put toward your debt. Here is your target order:

| Target Order | Debt Type | Balance | Minimum Payment | Your Action |

| Target 1 | Medical Bill | $400 | $25 | Pay $500 (Done in 1 month) |

| Target 2 | Store Credit Card | $1,200 | $35 | Minimum + previous $500 |

| Target 3 | Auto Loan | $8,000 | $300 | Minimum only (for now) |

| Target 4 | Student Loan | $22,000 | $250 | Minimum only (for now) |

In a single month, you physically cross an account off your list. That momentum keeps you fired up to attack Target 2.

The Debt Avalanche Method (The Mathematical Win)

The Debt Avalanche method is for the numbers nerds. It completely ignores how big or small your balances are. Instead, it targets the toxic interest rates that are bleeding your bank account dry.

How it works:

You list all your debts from the highest interest rate (APR) to the lowest interest rate, regardless of the balance size.

Mathematically, the Debt Avalanche is the superior strategy. Credit card companies make their money by charging you compound interest. By attacking the highest interest rate first, you are stopping the bleeding at the most severe wound.

This method will absolutely save you the most money in interest charges over the long haul, and it will technically get you out of debt a few months faster than the Snowball method.

The Avalanche Math:

Using that same $500 in extra monthly cash, here is your target order:

| Target Order | Debt Type | Balance | Interest Rate (APR) | Your Action |

| Target 1 | Store Credit Card | $4,000 | 26% | Pay $500/month here |

| Target 2 | Major Credit Card | $8,000 | 22% | Minimum only |

| Target 3 | Auto Loan | $12,000 | 7% | Minimum only |

| Target 4 | Student Loan | $15,000 | 5% | Minimum only |

Head-to-Head: Debt Avalanche vs Debt Snowball

Still not sure which route to take? Let’s look at the operational scorecard for the debt avalanche vs debt snowball.

The Debt Snowball

- Pros: Incredibly motivating. You will literally have fewer bills to manage each month very quickly. It has the highest proven success rate for people who struggle with financial discipline.

- Cons: Costs you more money over time. Because you ignore interest rates, high-APR accounts will continue to compound in the background.

The Debt Avalanche

- Pros: Saves you the absolute maximum amount of money on interest. It is the fastest mathematical route to zero debt.

- Cons: Requires immense, emotionless discipline. It can feel like a grueling grind.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyHow to Choose the Right Method for Your Personality

Choosing between the debt avalanche vs debt snowball isn’t really about mathematics—it’s about understanding your own behavior. The strategy that works best on paper isn’t always the one you’ll continue following six months from now. The goal isn’t to pick the method that looks smartest in a spreadsheet; it’s to choose the one that keeps you making consistent progress until every balance is gone.

The Debt Snowball is often the better choice if you’ve struggled to stick with budgets or debt repayment plans in the past. Paying off a smaller balance quickly creates an immediate sense of accomplishment. Every account you eliminate means one less payment to worry about each month, making your financial life feel simpler. Those early victories can create the motivation needed to tackle much larger debts that once seemed impossible.

The Debt Avalanche is generally the better option if you’re naturally analytical and motivated by efficiency. If watching interest charges accumulate bothers you more than waiting for quick wins, prioritizing the highest APR first allows more of every payment to reduce your principal instead of paying interest. Although progress may feel slower in the beginning, you’ll usually eliminate your debt while paying less interest overall.

Your personality isn’t the only factor to consider. Your debt profile matters too. If your smallest debt is only a few hundred dollars, eliminating it quickly may free up extra monthly cash flow that can then be redirected toward higher-interest accounts. On the other hand, if one credit card is charging an extremely high penalty APR while your remaining debts carry relatively low interest rates, delaying that account could become unnecessarily expensive.

If you’re choosing a repayment strategy because you’ve recently lost your job, I Lost My Job: A 30-Day Financial Survival Plan explains how to prioritize essential bills, preserve cash, and manage debt payments while your income is temporarily interrupted.

A practical compromise is the Hybrid Method. Start by eliminating one or two very small balances that can be paid off within a month or two. These quick victories reduce the number of accounts you manage and build confidence. Once those smaller debts disappear, reorganize your remaining balances by interest rate and switch to the Debt Avalanche. This combines the motivational benefits of the Snowball with the long-term savings of the Avalanche.

Whichever strategy you choose, avoid constantly switching between methods. Every time you change your payoff order, you interrupt your momentum and create unnecessary decision fatigue. Instead, commit to one plan for at least three to six months before reevaluating your progress. During that time, focus on finding additional money to accelerate your payoff—whether that’s cutting discretionary spending, using tax refunds, applying work bonuses, or directing unexpected windfalls toward your target debt.

Remember that neither strategy can compensate for continuing to accumulate new debt. The fastest payoff plan in the world won’t work if new credit card balances are added every month. Continue making purchases only when you can pay the statement balance in full, avoid unnecessary financing offers, and build an emergency fund as your debt decreases so unexpected expenses don’t force you back into borrowing.

Ultimately, the debate over debt avalanche vs debt snowball has a surprisingly simple answer. The winner isn’t determined by a calculator—it’s determined by consistency. The method that keeps you motivated, prevents you from giving up, and helps you reach a zero balance is the method that works best for you.

One final point is worth remembering: your repayment strategy is not permanent. As your financial situation improves, your priorities may change as well. A salary increase, a lower interest rate through refinancing, or the payoff of a major loan can completely reshape the order that makes the most sense. Revisit your debt repayment plan every few months, celebrate meaningful milestones along the way, and adjust your strategy when circumstances genuinely change—not simply because progress feels slow. Staying flexible while remaining committed is often the key to becoming completely debt-free.

When This Backfires

Both strategies are highly effective, but they have distinct breaking points. If you understand the pitfalls of the debt avalanche vs debt snowball, you can prevent yourself from failing halfway through.

When the Avalanche Backfires:

The Avalanche fails when you face a “motivation desert.” Suppose your highest interest rate debt is also your largest balance—like a $15,000 credit card at 25%. Even throwing $500 extra at it every month, you will be paying on that single card for over two years before the account is closed. Because you don’t get the “quick wins” of crossing off smaller accounts, the fatigue sets in. You get tired, you lose focus, and you revert back to making minimum payments.

When the Snowball Backfires:

The Snowball fails when you have a toxic, predatory interest rate lurking in the background. Suppose you are spending three months paying off a $1,500 medical bill that charges 0% interest, just because it is your smallest balance. Meanwhile, you have a $10,000 credit card balance sitting at a 29.99% penalty APR. While you are feeling good about the medical bill, that credit card is generating $250 in new interest charges every single month. The math will completely overwrite your psychological win.

The Secret “Hybrid” Approach

What if you want the psychological wins of the Snowball but the financial savings of the Avalanche? You don’t have to strictly choose one side of the debt avalanche vs debt snowball debate. You can build a hybrid model.

- Step 1: The Micro-Snowball. If you have a couple of tiny, annoying debts (like a $150 forgotten utility bill or a $300 doctor’s bill), aggressively pay those off in the first month. Get them out of your life. Get the dopamine hit.

- Step 2: The Major Avalanche. Once the annoying micro-debts are cleared, re-order your major credit cards and loans strictly by interest rate. Attack the highest APR with ruthless intensity so you stop bleeding cash.

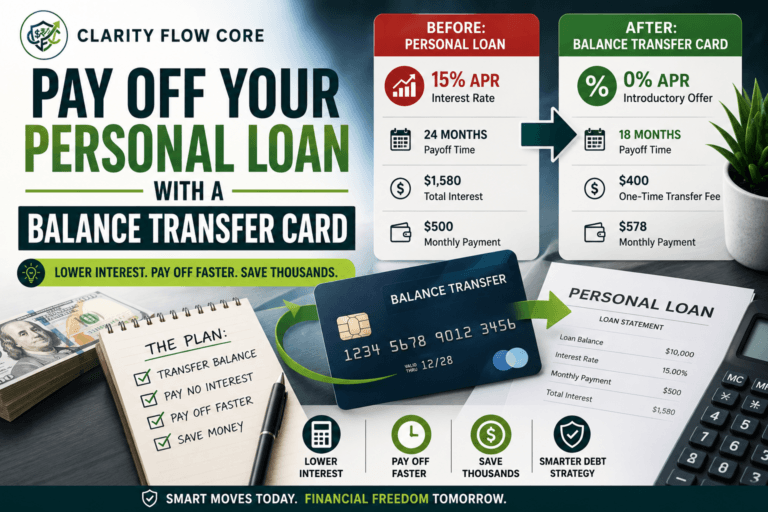

- Step 3: Pause the Interest. If you have a decent credit score, look into transferring your highest interest debt onto a promotional card. As outlined in How 0% APR Balance Transfers Work — And When They’re Worth It, this effectively drops the interest rate to zero for 12 to 18 months, allowing you to attack the principal balance without the math fighting against you.

Frequently Asked Questions (FAQs)

Which method pays off debt faster?

Debt Avalanche typically eliminates debt faster because it minimizes interest costs.

Which method saves the most money?

Debt Avalanche generally results in lower total interest paid.

Which method is best for beginners?

Many beginners find Debt Snowball easier because the quick wins provide motivation.

Can I switch methods later?

Yes. Many people start with a Snowball approach and later transition into an Avalanche strategy once they build payoff momentum.

Does either method improve credit scores faster?

Neither directly improves scores faster. Consistent on-time payments and lower balances are what matter most.

The Bottom Line

The debate of debt avalanche vs debt snowball is incredibly popular online, but the truth is beautifully simple.

The “best” method is not the one that looks prettiest on a spreadsheet. The best method is the one you will actually stick to for the next 18 months. If you are deeply analytical, motivated by saving money, and hate paying a single cent to the bank, choose the Avalanche. If you get overwhelmed easily and need to see visual progress to stay focused, choose the Snowball.

Pick your strategy, point your extra cash at the target, and take your cash flow back. Once your debt is cleared, protect your progress by understanding What Is Credit Utilization and Why Does It Matter? and reading up on FICO vs VantageScore: Why Credit Scores Differ Between Apps.

Debt Repayment & Credit Resources

Paying off debt is about more than choosing a strategy. Understanding how interest rates, credit reports, and repayment habits affect your finances can help you stay motivated and make smarter financial decisions over the long term.

- Consumer Financial Protection Bureau (CFPB) – Explore practical resources on managing debt, budgeting, communicating with creditors, and improving your overall financial health.

- Federal Reserve – Review consumer credit data and educational resources to better understand household debt trends, borrowing, and lending in the United States.

- myFICO® – Learn how payment history, credit utilization, and debt balances influence your FICO® Score, along with practical strategies for strengthening your credit profile.

- Experian – Educational articles covering debt repayment strategies, balance management, credit utilization, and responsible credit use.

- Equifax – Consumer education on credit reports, debt management, borrowing, and building long-term financial health.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit credit counseling, Debt Management Plans (DMPs), budgeting assistance, and personalized financial guidance.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

9 Comments

Comments are closed.