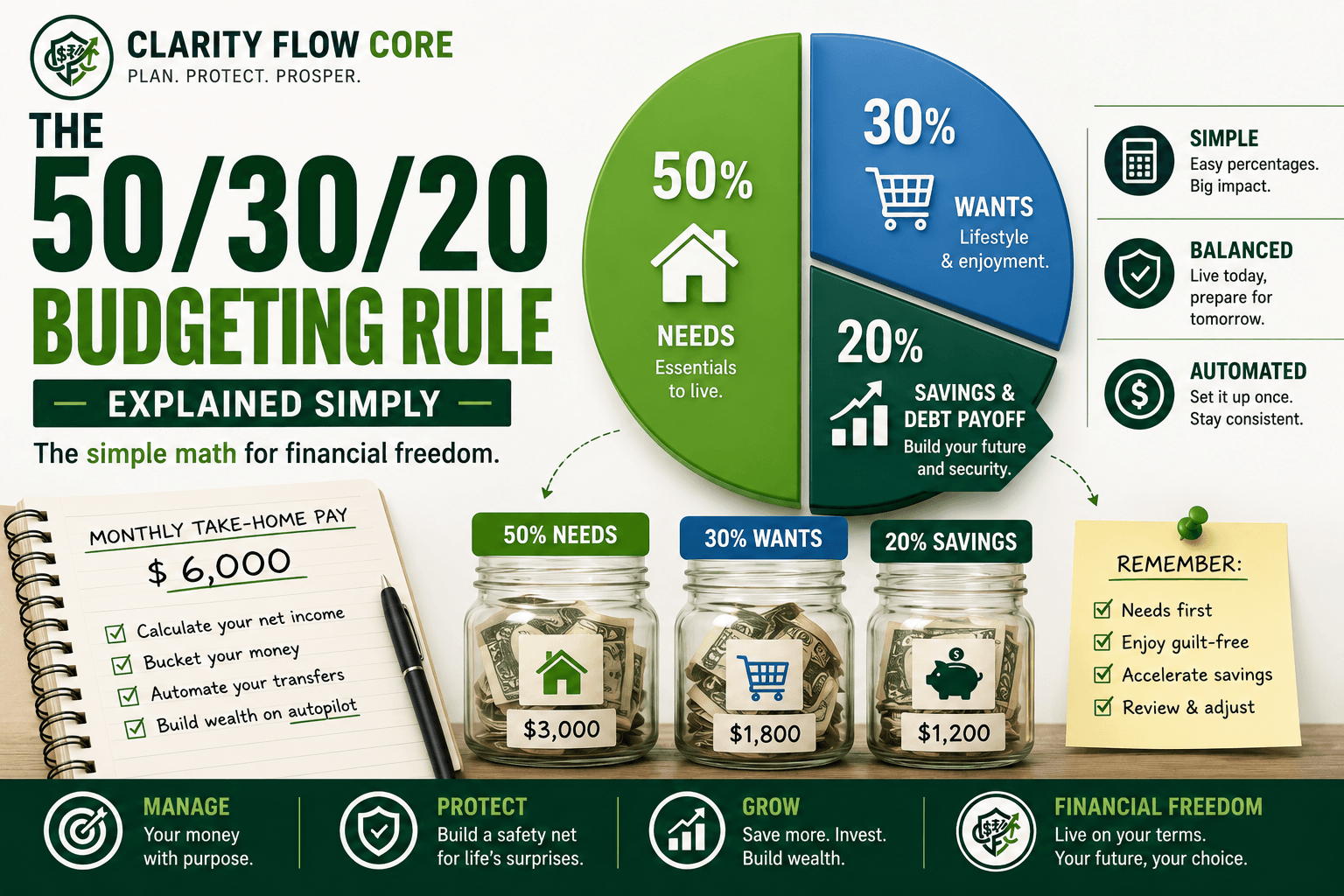

The 50/30/20 Budget Rule Explained Simply

I used to think budgeting was synonymous with self-punishment. For years, I attempted to manage my money by downloading ridiculously sophisticated, 14-tab spreadsheets. I recorded every single $4 coffee I bought, agonizing over pennies, and feeling intense guilt every time I spent money on something remotely fun.

Predictably, the strategy was short-lived. It usually lasted exactly three weeks before I burned out. It was a financial crash diet, and much like severely restricting calories, restricting your spending too aggressively always ends in a massive binge.

I desperately wanted to be able to pay my bills, destroy my debt, and invest for the future, but I also wanted to enjoy my actual life without feeling like a mathematical failure.

Enter the 50/30/20 budgeting rule.

This simple financial framework, initially popularized by Senator Elizabeth Warren in her book All Your Worth, completely strips away the confusing, restrictive micro-calculations of traditional budgeting. It is the absolute best operational framework for anyone looking to build a massive financial core while remaining sane.

Here is exactly how the 50/30/20 budgeting rule works, the behavioral psychology of why it is so effective, how to calculate your true numbers, and how to automate the entire system starting today.

What is the 50/30/20 Budgeting Rule?

The sheer genius of the 50/30/20 budgeting rule rests entirely in its simplicity. Instead of breaking your spending into 50 exhausting micro-categories (like “Entertainment,” “Pet Supplies,” “Gas,” or “Home Maintenance”), you dump your income into just three massive buckets:

- 50% for Needs (Survival Level)

- 30% for Wants (Guilt-Free Spending)

- 20% for Savings & Debt Payoff (Your Future)

By focusing on these macro-percentages, you are free to spend your money in absolutely any way you want, as long as you stay within the three guardrails. It forcefully shifts your daily mindset from “scarcity” to “management.”

Step 1: Calculate Your True “After-Tax” Income

Before you can execute the 50/30/20 budgeting rule, you need to know exactly how much water is actually in the well. The 50/30/20 budgeting rule is based exclusively on your net income, not your gross income.

Your gross income is your massive salary before the government takes their cut. Your net income, or after-tax income, is the actual, spendable cash that hits your checking account on payday.

If you are a standard W-2 employee, this calculation is easy: look at your bank deposits. However, if your employer automatically deducts money from your paycheck for a 401(k) retirement plan or health insurance premiums, you must logically add those amounts back into your take-home pay for the purposes of this equation.

Why? Because 401(k) contributions technically count toward your 20% savings bucket, and health insurance technically counts toward your 50% needs bucket!

If you are a freelancer or a 1099 contractor (like a freelance video editor or graphic designer), calculating your net income is much more dangerous. You must manually subtract your estimated self-employment taxes and business expenses before applying the 50/30/20 budgeting rule.

| Income Type | The Operational Math | Your “Net Income” for the Rule |

| W-2 Employee | Bank Deposits + 401(k) Contributions + Payroll Health Insurance | Total Net Income |

| 1099 Freelancer | Gross Client Invoices – 30% Tax Reserve – Business Expenses | Total Net Income |

(Note: If you run a side hustle and need help separating your taxes, review our Freelance Video Editor Tax Guide: Deductions & Write-Offs before attempting to budget).

The 50% Bucket: Your “Needs” (The Survival Number)

Exactly half of your take-home pay should be spent on the bare, non-negotiable requirements of keeping yourself alive and employed. These are the bills that you absolutely must pay to put a roof over your head, food in your stomach, and keep your life running.

If you were to lose your job tomorrow, these are the expenditures you would still be legally or physically required to pay.

If you’re planning to move out for the first time, understanding these essential expenses is critical before signing a lease. Read How Much Should You Save Before Moving Out on Your Own? to estimate the upfront costs and monthly budget you’ll need for a smooth transition.

What Actually Counts as a Need?

- Mortgage payments or rent.

- Basic groceries (Food required to live, not $100 steak dinners).

- Basic utilities (Electricity, water, trash, and internet for work).

- Health insurance premiums and required daily medications.

- Commute costs (Auto loan, gas, bus pass, basic car maintenance).

- Minimum debt payments (The absolute minimums on credit cards or student loans to avoid default).

The Reality Check on Needs

If your basic needs are currently swallowing 70% or 80% of your money, you have a fundamental cash-flow crisis. You cannot mathematically execute the 50/30/20 budgeting rule if your rent is too expensive.

To get your expenses back down to 50%, you cannot rely on skipping lattes. You must make sweeping, aggressive operational moves: downsize your apartment, get a roommate, aggressively shop your rates using How to Save on Insurance Without Cutting Coverage, or trade in a heavily financed car for a cheaper commuter vehicle.

The 30% Bucket: Your “Wants” (Guilt-Free Spending)

This is the psychological safety valve. This is the exact bucket that makes the 50/30/20 budgeting rule genuinely sustainable over a 30-year period. You are a human being; you must enjoy the money you work so hard to obtain, or you will eventually rebel against your own financial system.

What Actually Counts as a Want?

- Eating out, hitting the drive-thru, and ordering UberEats.

- Concerts, sporting events, and weekend vacations.

- Streaming subscriptions (Netflix, Spotify, Hulu).

- Video games, gym memberships, and expensive hobbies.

- Upgrading to the newest smartphone when your old one works fine.

- That iced coffee on a Tuesday afternoon.

The absolute greatest thing about this specific bucket is that it completely removes the shame and guilt from money. As long as your fun spending is at or below 30% of your take-home earnings, you never have to feel bad about buying a cappuccino or booking a flight again. The mathematical heavy lifting is already done. Your bills are paid, and your future is funded.

The 20% Bucket: Saving & Debt Payoff (Your Future)

This final bucket is how you actually build wealth, achieve financial security, and permanently escape the paycheck-to-paycheck cycle. Exactly one-fifth of your income must be totally committed to ensuring your financial future is protected.

What Goes Into the 20% Bucket?

- Building a fully funded cash reserve.

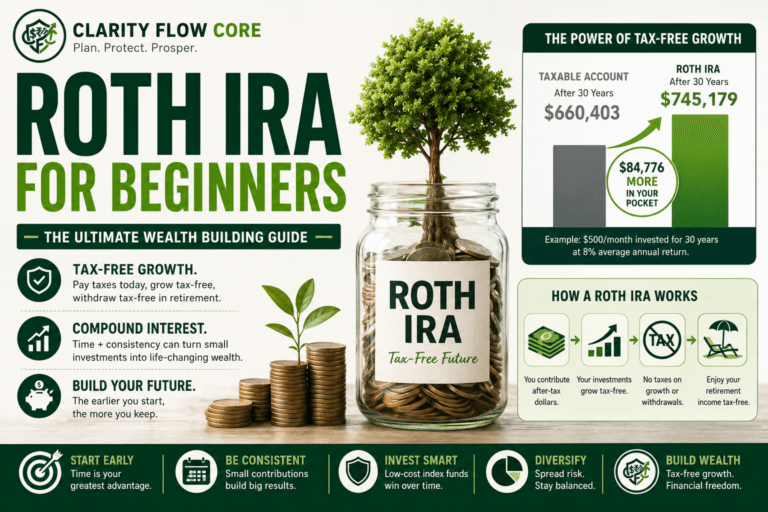

- Putting money into a tax-advantaged retirement account (like a Roth IRA for Beginners or a 401k).

- Making aggressive, additional principal payments on high-interest debt.

- Saving for long-term capital goals, like a down payment on a house.

The 20% Order of Operations

A fatal flaw people make when starting the 50/30/20 budgeting rule is trying to do everything simultaneously. If you try to invest in the stock market, save for a house, and pay down massive credit card debt all at once, your 20% bucket will be stretched too thin to make any mathematical progress. You must follow a strict order:

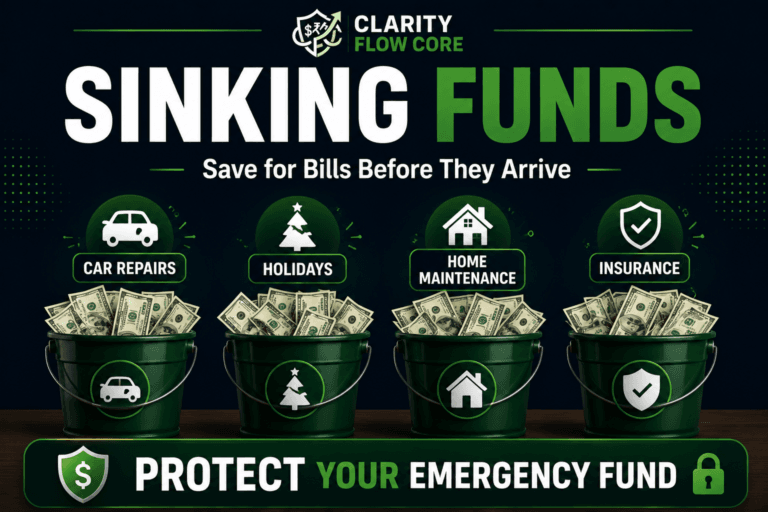

- The Starter Shield: Route your entire 20% bucket into a High-Yield Savings Account until you hit $1,000. (See Emergency Fund Basics: How Much Cash Should You Keep? for the math on this). If you’re opening your first HYSA, How to Choose Your First High-Yield Savings Account explains how to compare APYs, FDIC insurance, account fees, and other important features before choosing a bank.

- Smash the Toxic Debt: Once you have a basic safety net, turn the 20% firehose totally on your high-interest credit cards using the Debt Avalanche vs. Debt Snowball method. Do not invest a single dollar until 24% interest debt is eradicated.

- The Full Moat: After the toxic debt is gone, route that 20% back into your savings account until you have a full 3 to 6 months of living expenses saved.

- Invest & Build Wealth: Zero consumer debt. Massive safety net. Now, you aggressively route that 20% into index funds, a Roth IRA, or saving for real estate.

🗺️ What Will Your 20% Bucket Actually Build?

Knowing how to allocate your money is only half the battle. Now it’s time to see the timeline. Plug your current debt, savings, and 20% monthly contribution into our free Financial Freedom Planner to calculate your exact debt-free date and map your custom route to independence.

Real-World Math: The 50/30/20 Budgeting Rule in Action

Let’s look at the raw operational math for an average individual to see how the 50/30/20 budgeting rule functions in reality. Assume David’s true after-tax take-home pay is $5,000 a month.

| The 50% Needs ($2,500) | The 30% Wants ($1,500) | The 20% Future ($1,000) |

| Rent: $1,400 | Restaurants/Bars: $400 | Credit Card Overpayment: $500 |

| Groceries: $400 | Concerts/Events: $300 | Emergency Fund: $250 |

| Utilities/Internet: $200 | Clothing/Shopping: $400 | Roth IRA Contribution: $250 |

| Car Payment/Insurance: $350 | Subscriptions: $100 | |

| Minimum Debt Payments: $150 | Vacation Sinking Fund: $300 | |

| Total: $2,500 (Exact) | Total: $1,500 (Guilt-Free) | Total: $1,000 (Wealth Building) |

David gets to spend $1,500 a month purely on having fun, without a single ounce of anxiety, because his entire financial life is mathematically protected.

How to Adjust the 50/30/20 Rule as Your Income Changes

One of the biggest advantages of the 50/30/20 budget rule is that it isn’t tied to a specific income level. Whether you receive a raise, change jobs, or experience a temporary drop in income, the framework can be adjusted without completely rebuilding your budget.

For example, if your salary increases, it can be tempting to let your spending grow at the same pace—a habit known as lifestyle inflation. Instead of immediately upgrading your car, moving into a more expensive apartment, or increasing discretionary spending, consider directing a portion of your additional income toward savings or debt repayment. Even increasing your savings rate from 20% to 25% can significantly accelerate your progress toward an emergency fund, home down payment, or retirement goals.

The same principle applies during more challenging financial periods. If your income temporarily decreases, focus on protecting essential expenses first. You may need to reduce spending in the “wants” category while maintaining minimum debt payments and continuing to save something—even if it’s only a small amount. Maintaining the habit of saving is often more important than the dollar amount during difficult months.

If your income drops because you’ve been laid off, I Lost My Job: A 30-Day Financial Survival Plan provides a step-by-step roadmap for prioritizing bills, stretching your emergency fund, and managing your finances during the first month of unemployment.

Remember that the 50/30/20 rule is a guideline, not a strict law. Some households in high-cost cities may spend more than 50% on necessities, while others with lower housing costs may comfortably save well above 20%. The goal isn’t to force your finances into exact percentages but to create a balanced spending plan that supports both your current lifestyle and your long-term financial security. Reviewing your budget every few months helps ensure it continues to reflect your changing income, priorities, and financial goals.

When the 50/30/20 Budgeting Rule Backfires

The 50/30/20 budgeting rule is an incredible framework, but it is not completely bulletproof. If you execute it poorly, it will actively work against you. Here is exactly when and why the system backfires:

1. The High Cost of Living Trap

With severe inflation and soaring housing costs in massive metropolitan areas (like New York or San Francisco), many Americans simply cannot squeeze their living costs into 50% of their income.

If you discover that your rent and basic food are taking up 65% of your salary, do not panic, and do not abandon the framework. You simply need to tweak your ratios temporarily to reflect reality. Replace the model with a 65/15/20 rule.

You recognize that you have unavoidable massive needs (65%), which means you must ruthlessly cut back on your fun spending (slashing wants to 15%). However, you absolutely never compromise on paying your future self (maintaining the savings bucket at a strict 20%). Over time, as your income increases or you pay off a car, your ratios will naturally drift back toward the 50/30/20 baseline.

2. The Lifestyle Creep Failure

This is how people making $150,000 a year still live paycheck-to-paycheck. When you get a $1,000 monthly raise at work, human nature dictates that you put all $1,000 directly into your “Wants” bucket to buy a nicer car or take better vacations.

You must strictly apply the 50/30/20 budgeting rule to all new income. If you get a $1,000 raise, you only get to add $300 to your Wants bucket. You must logically assign $500 to cover inflating Needs, and strictly route an additional $200 directly into your investment accounts.

3. Mixing Needs and Wants (The Luxury Justification)

Be brutally honest with yourself. Basic sustenance is a need. A $100 steak dinner is a want. A reliable 10-year-old Toyota Camry to commute to work is a need. A brand-new, $60,000 luxury SUV is a want. If you start categorizing luxury upgrades in your 50% “Needs” bucket, you are lying to yourself, and the math will collapse.

Automating the System: The Final Hack

The ultimate secret to long-term success with the 50/30/20 budgeting rule is to entirely eliminate human error. If you rely on your own willpower to manually move money around on the 31st of the month, you will eventually fail.

Furthermore, keeping all your money mixed together in a single checking account is a recipe for disaster. You will inevitably look at your balance and accidentally spend your 20% savings money on a 30% want.

The Automated Banking Setup:

You must physically separate the money.

- Use your primary checking account exclusively for your 50% Needs and your 30% Wants.

- Open a completely separate High-Yield Savings Account (HYSA) at a different, online-only bank.

Read our operational guide on How to Automate Savings Using Split Direct Deposit. When your paycheck is generated, have your employer’s payroll software instantly route your exact 20% chunk directly to your external savings account before the money ever hits your primary bank.

If you do not see that 20% when you log into your daily banking app, you will not be tempted to spend it. Your Needs and Wants remain in your checking account, providing the reassuring certainty that your future is already fully funded in the background.

FAQ

Is the 50/30/20 budget rule realistic?

Yes. Many people use it as a starting framework, though the percentages can be adjusted based on local costs and personal circumstances.

Does the 50/30/20 rule work for low incomes?

It can, but people in high-cost areas or with lower incomes may need to temporarily modify the percentages.

Should retirement contributions count toward the 20%?

Generally yes. Retirement savings are part of your future-focused financial goals.

What if my needs exceed 50%?

Reduce discretionary spending where possible and gradually work toward bringing needs closer to the target range.

Is the 50/30/20 rule better than zero-based budgeting?

Neither is universally better. The 50/30/20 rule prioritizes simplicity, while zero-based budgeting offers more detailed control.

The Bottom Line

You do not need a finance degree, a complex mobile app, or a color-coded spreadsheet to master your cash flow. Budgeting should not be a stressful, part-time job.

The 50/30/20 budgeting rule gives you a highly actionable, mathematical blueprint to pay your essential bills, systematically destroy your debt, and still live a vibrant, enjoyable life. Calculate your three macro-percentages this weekend, automate your savings transfers on Monday morning, and permanently chase away your financial anxiety.

References & Trusted Sources

- Consumer Financial Protection Bureau (CFPB) – Budgeting, saving, and money management resources

- Consumer.gov (Federal Trade Commission) – Making and following a budget

- U.S. Department of Labor – Retirement savings and 401(k) information

- Internal Revenue Service (IRS) – Retirement Topics: 401(k) Plans

- Internal Revenue Service (IRS) – Individual Retirement Arrangements (IRAs)

- Federal Deposit Insurance Corporation (FDIC) – Money Smart Financial Education Program

- MyMoney.gov (U.S. Financial Literacy and Education Commission) – Budgeting and financial planning resources

- Federal Reserve – Report on the Economic Well-Being of U.S. Households (latest available edition)

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

8 Comments

Comments are closed.