Best Credit Cards for Beginners: What Actually Matters

If you open YouTube or Reddit and search for the best credit cards for beginners, you will immediately be hit with a massive wall of financial noise.

One influencer tells you to chase premium travel rewards so you can fly first class to Dubai. Another recommends complex, multi-card setups with massive annual fees. You see flashy metal cards, rotating point categories, and complex redemption portals.

For someone who just wants to build a financial foundation, this advice is completely toxic.

The truth is that the best credit cards for beginners are rarely the ones with the biggest rewards or the most aggressive marketing campaigns. For most first-time users, the operational goal is incredibly simple: build your credit history safely, avoid expensive consumer debt, and learn exactly how the banking system works without making a $5,000 mistake early in your career.

In the beginning, your objective is not to maximize cashback. Your objective is to build a pristine FICO score so that when you eventually want to execute the How to House Hack: The FHA Loan Strategy Explained playbook, the bank actually approves your mortgage.

A good starter card should make that process mathematically easier, not more confusing. Here is the operational truth behind the best credit cards for beginners, the exact math of how to use them, and the hidden traps that ruin millions of young credit profiles every year.

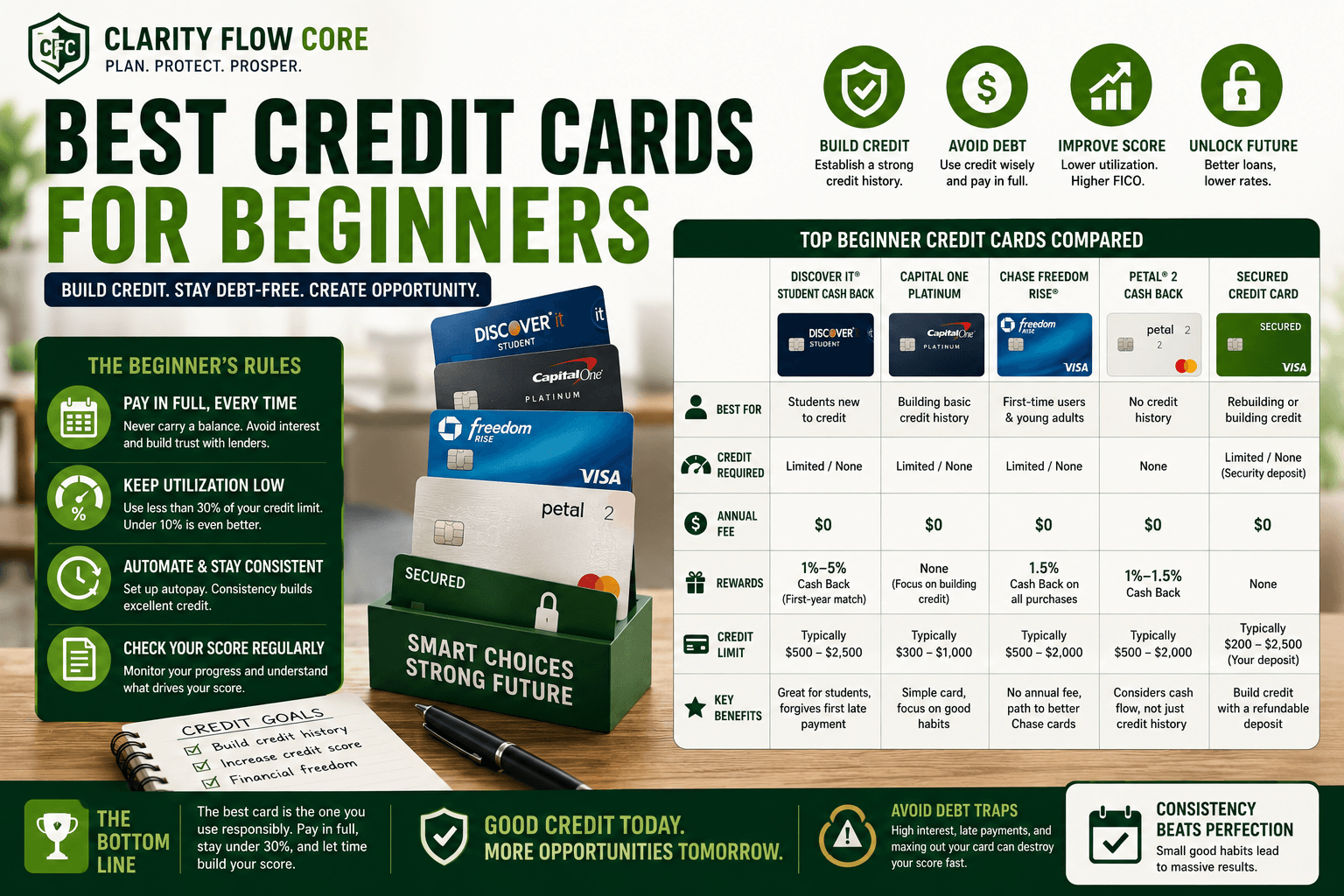

What Actually Makes the Best Credit Cards for Beginners?

A massive mistake first-time applicants make is focusing entirely on cashback percentages. A 2% cashback rate is mathematically irrelevant if you carry a balance and pay 28% in interest charges.

When evaluating the best credit cards for beginners, you should completely ignore the rewards program and look for these specific operational features:

- $0 Annual Fee: You should never pay a bank for the privilege of building your credit. Your first credit card is an account you need to keep open for decades to anchor the “Age of Credit” metric on your report. If it has an annual fee, you will eventually want to cancel it.

- Reasonable Approval Odds: If you have zero credit history, applying for a premium travel card will result in an automatic denial and a hard inquiry that damages your blank report. You need cards specifically underwritten for “thin files.”

- Free FICO Score Tracking: You need to monitor the algorithmic output of your behavior. (If you aren’t sure how these scores work, read FICO vs. VantageScore: Why Credit Scores Differ Between Apps.

- Simplicity: The best credit cards for beginners do not require you to activate rotating categories every quarter or track complex point valuations.

The smartest move you can make is choosing a card that helps you build consistent, automated habits over time. Here is the definitive list of the best credit cards for beginners and exactly why they work.

1. Discover it® Student Cash Back

Best for: College Students Who Want Operational Simplicity

Discover has dominated the student market for a reason. Their underwriting algorithms are highly sympathetic to young adults with zero credit history. They look at your university enrollment and potential future income rather than demanding a ten-year payment history.

One reason the Discover it® Student is frequently ranked among the best credit cards for beginners is that it actively encourages credit education instead of aggressively pushing you into debt.

The Operational Benefits:

- $0 Annual Fee.

- First-Year Cashback Match: They automatically match all the cashback you earn at the end of your first year, which is a nice windfall, but it is simple to understand.

- Forgiveness: They automatically waive your first late payment fee (though you should never be late) and do not hit you with a penalty APR if you make a mistake early on.

The Downside:

Discover relies on its own payment network, not Visa or Mastercard. While acceptance in the US is near 99%, it is frequently rejected internationally. If you are studying abroad, this is not the card for you.

2. Capital One Platinum

Best for: Building Militant, Basic Credit Habits

This is one of the most brutally simple starter cards available on the market, which is exactly why it is one of the best credit cards for beginners.

The Capital One Platinum offers absolutely zero rewards. No points. No cashback. No travel miles. For a beginner, this is actually a massive psychological advantage.

A major trap first-time cardholders fall into is swiping their card for things they do not need, simply to “earn points.” They overspend to chase a 1.5% return, and end up paying 29.99% in interest when they cannot afford the bill. By completely removing the rewards incentive, the Capital One Platinum forces you to focus strictly on building consistency.

The Operational Benefits:

- $0 Annual Fee.

- Automatic Credit Line Reviews: Capital One will automatically review your account after 6 months of on-time payments and often proactively increase your credit limit, which rapidly improves your credit score.

- Highly Accessible Approval: They are known for approving “thin” or “fair” credit profiles.

3. Chase Freedom Rise®

Best for: Entering the Chase Ecosystem Early

Chase is the undisputed king of premium credit cards. However, historically, they have demanded at least one year of established credit history before approving anyone for their entry-level cards. This completely locked beginners out.

The Chase Freedom Rise® changed the landscape, making it one of the most strategic best credit cards for beginners. Chase designed this card specifically for people with zero credit history, with a massive operational caveat: your approval odds skyrocket if you have a checking account with Chase that holds at least $250.

The Operational Benefits:

- $0 Annual Fee.

- Flat 1.5% Cashback: Simple, easy-to-understand rewards on every purchase.

- The 5/24 Rule Advantage: Chase has an unwritten rule: if you have opened 5 or more credit cards across any bank in the last 24 months, they will automatically deny you. By starting your journey with the Freedom Rise, you build a relationship with Chase early, ensuring you have access to their premium cards later in life.

4. Petal® 2 Visa® (Cash Flow Underwriting)

Best for: Freelancers and Non-Traditional Income

If you run a side hustle, as discussed in 1099 Taxes Explained for Freelancers and Side Hustlers, traditional banks might reject your credit card application because your income is irregular and you lack a FICO score.

Cards like the Petal® 2 Visa® bypass the traditional FICO system entirely using “Cash Flow Underwriting.” When you apply, you securely link your primary checking account. The bank’s algorithm scans your bank history to see how much money you make, how much you save, and how reliably you pay your rent and utility bills.

For young professionals earning online income or inconsistent gig money, this alternative approval model makes it one of the absolute best credit cards for beginners.

The Operational Benefits:

- $0 Annual Fee.

- Alternative Approval: You can get approved based on your actual banking habits, not an arbitrary 3-digit score.

- No Fees: They charge no late fees, no international fees, and no bounced check fees.

5. The Secured Credit Card (The Ultimate Backup)

Best for: Rebuilding Credit or Guaranteed Approvals

If you have aggressively damaged your credit in the past, or if you simply cannot get approved for any of the unsecured options listed above, you must use a Secured Credit Card. This is the safety net of the best credit cards for beginners.

How the Math Works:

You provide the bank with a refundable cash security deposit upfront. If you put down a $300 deposit, the bank hands you a credit card with exactly a $300 limit.

At first, a secured card feels incredibly frustrating because it requires your own cash. However, it is an operational tool. You use the card to buy $20 in gas every month, and you pay it off immediately. The bank reports that on-time payment to the credit bureaus. After 6 to 8 months of flawless behavior, the bank will automatically “graduate” your account. They will mail your $300 deposit back to you and convert the card into a standard, unsecured credit line.

If a secured card is your best option, Best Secured Credit Cards for Beginners in 2026 compares the top beginner-friendly secured cards, including their deposit requirements, fees, graduation policies, and approval odds.

The Operational Math: Credit Utilization

The single biggest reason people researching the best credit cards for beginners ruin their score in the first six months is that they do not understand the math of “Credit Utilization.”

Your Credit Utilization Ratio is how much money you currently owe compared to your total credit limit. This single metric accounts for a massive 30% of your entire FICO score.

If you’re unfamiliar with this concept, What Is Credit Utilization — And Why Does It Matter? explains exactly how credit utilization is calculated, why lenders watch it so closely, and how it influences your credit score.

When you get your first credit card, the bank will likely give you a very small limit, perhaps $500. If you buy a $400 television on that card, you are utilizing 80% of your available credit.

| Credit Limit | Current Balance | Utilization Ratio | Algorithmic Impact on FICO Score |

| $500 | $400 | 80% | Massive Drop (High Risk) |

| $500 | $250 | 50% | Moderate Drop (Medium Risk) |

| $500 | $40 | 8% | Massive Increase (Excellent) |

The algorithm views anyone utilizing more than 30% of their limit as a high-risk borrower desperate for cash. If you max out your small beginner card, your credit score will immediately plummet 40 to 60 points, even if you make your minimum payments on time.

The Rule: To maximize the best credit cards for beginners, you must keep your reported balance under 10% of your total limit. If your limit is $500, never let the statement close with a balance higher than $50.

📈 Check Your Credit Utilization Risk

Credit utilization is one of the most influential credit score factors. Use our Credit Utilization Calculator & Recovery System to see where you stand and discover ways to improve your utilization ratio.

When This Backfires: The Operational Traps

A credit card is a financial chainsaw. If used correctly, it clears the path to building wealth. If used recklessly, it will amputate your cash flow. Even if you choose from the list of the best credit cards for beginners, you must avoid these fatal traps:

1. The “Paying Interest Builds Credit” Myth

This is the most destructive lie in personal finance. Millions of beginners believe that they must carry a balance and pay the bank a little bit of interest every month to “prove” they are good borrowers and build their score.

This is 100% mathematically false. Paying interest does absolutely nothing for your credit score. If you pay your statement balance in full, exactly on time, every single month, you will build a pristine credit score while paying exactly $0.00 in interest. Utilize the “grace period.”

2. Treating Credit Like an Emergency Fund

A credit card is a method of payment; it is not a safety net. If your car transmission blows up and you put a $3,000 repair on a beginner credit card at 28% interest, that debt will compound rapidly and destroy your monthly budget. You must build a liquid cash moat first. (Read Emergency Fund Basics: How Much Cash Should You Keep? before you apply for any credit cards).

3. The “Shotgun” Application Mistake

When beginners get rejected for their first card, they panic. They instantly apply for four other cards from different banks in the span of 48 hours.

Every single application triggers a “Hard Inquiry” on your credit report. The algorithm views a sudden burst of inquiries as a sign of extreme financial distress. Applying for multiple cards rapidly will drop your score significantly and ensure automatic denials across the board. Apply for one card. If denied, wait at least three months before applying for another.

The Bottom Line

The best credit cards for beginners are not the ones with the sleekest metal designs or the highest signup bonuses. The perfect starter card is simply a tool that fits your current financial reality and helps you build responsible habits consistently.

Treat your new credit card exactly like a debit card. If you do not have the physical cash sitting in your checking account today, do not swipe the credit card.

Put your card on autopay the exact day you activate it. Buy one small tank of gas or a Spotify subscription on it every month, pay the balance in full, and keep your utilization under 10%. Credit building is not about hacking the system; it is about militant, boring consistency. Choose a no-fee card, set up your systems, and let time do the heavy lifting for your financial reputation.

References & Trusted Resources

- Consumer Financial Protection Bureau (CFPB) – Credit Cards and Credit Scores

- Federal Trade Commission (FTC) – Understanding Credit Reports and Scores

- FICO – Credit Score Education

- Experian – Credit Utilization and Credit Scores

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

3 Comments

Comments are closed.