Can a Balance Transfer Card Help Pay Off a Personal Loan?

If you took out a personal loan to consolidate debt or cover an unexpected emergency, you made a logical choice at the time. Personal loans offer fixed monthly payments and a hard payoff date.

But if you are currently staring at a personal loan with an interest rate of 12%, 15%, or even 20%+, those monthly interest charges are actively draining your bank account. The “fixed” payment feels less like a lifeline and more like an anchor.

If you are tired of losing money to compound interest—and understand the damage outlined in What Happens If You Only Pay the Minimum on a Credit Card?—you have likely looked at that stack of credit card offers in your mailbox and wondered: Can I use a 0% APR credit card to wipe out this installment loan?

The short answer is: Yes. Executing a balance transfer personal loan payoff is entirely possible, and mathematically, it is one of the most powerful moves you can make to reclaim your cash flow.

However, moving debt from an installment loan to a revolving credit card is operationally different than a standard credit-card-to-credit-card transfer. If you press the wrong button or misunderstand the bank’s terminology, you could accidentally trigger a massive cash advance fee and ruin your finances.

Here is the exact operational math behind a balance transfer personal loan strategy, the strict execution steps, the hidden fees to calculate, and exactly when this move will backfire.

⚡ Quick Answer

- A balance transfer card can sometimes be used to pay off a personal loan if the credit card issuer allows balance transfer checks or direct deposit transfers.

- The strategy may significantly reduce interest costs if the card offers a 0% introductory APR, but borrowers must accurately account for upfront transfer fees, strict promotional deadlines, and potential credit-score impacts.

The Math: Why This Strategy Works

To understand why a balance transfer personal loan maneuver is so effective, you have to look at the raw amortization math.

When you have a high-interest loan, a massive percentage of your monthly payment goes straight to the bank’s profit margin before it ever touches your principal balance. By moving that debt to a 0% APR promotional credit card, you freeze the interest. Every single dollar you pay attacks the principal directly. (For a complete breakdown on how these specific cards function, read 0% APR Balance Transfers: How They Actually Work).

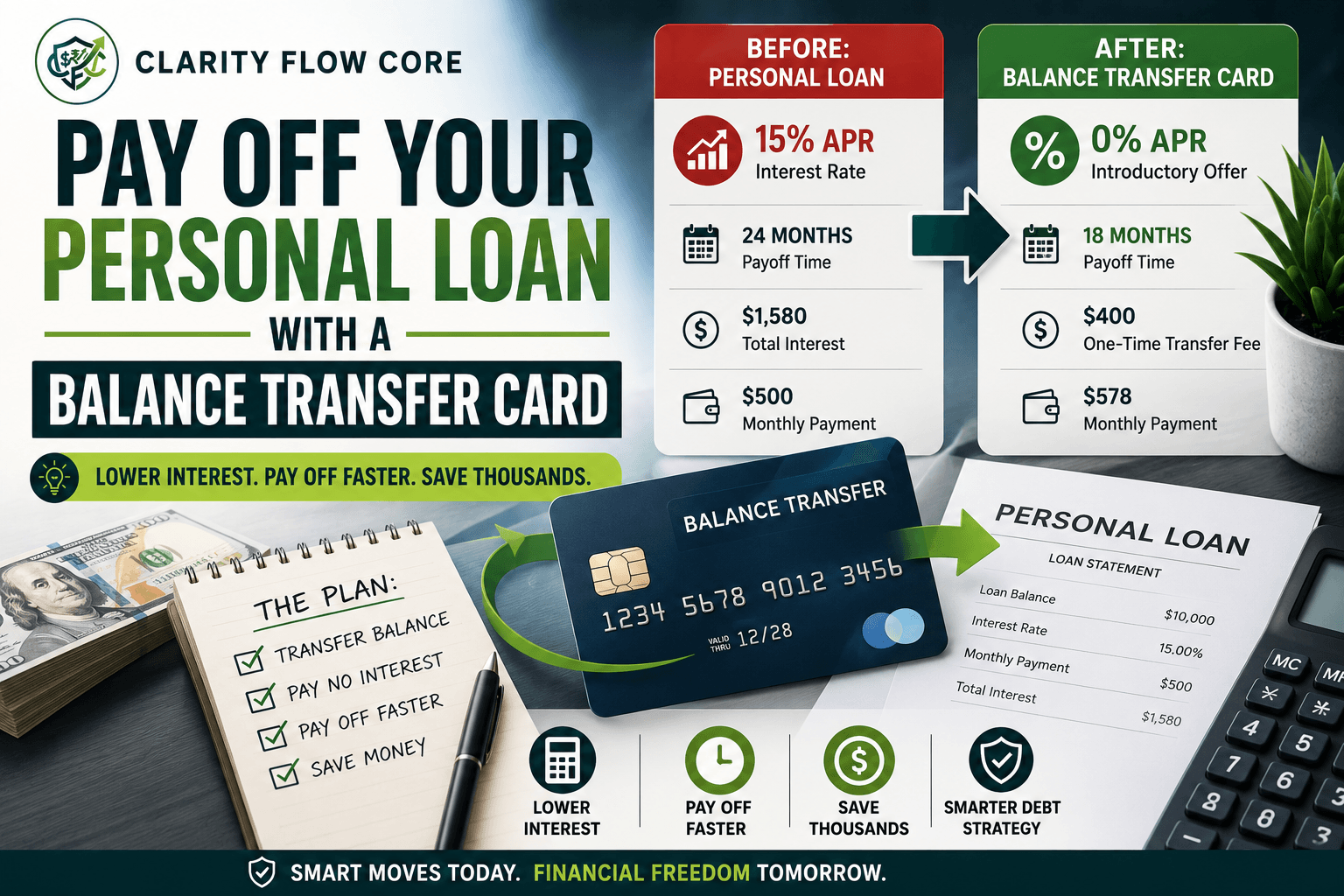

Let’s look at a highly realistic scenario. You have a $10,000 personal loan balance remaining at a 15% APR. You are currently paying $500 a month.

| Payoff Strategy | Monthly Payment | Time to Zero Debt | Total Interest / Fees Paid |

| Stay with Personal Loan (15%) | $500 | 24 Months | $1,580 |

| Balance Transfer (0% APR for 18 Months) | $578 | 18 Months | $400 (Transfer Fee) |

To execute the balance transfer personal loan strategy, you open an 18-month 0% APR card. The new bank charges a 4% transfer fee ($400) upfront. Your new starting balance is $10,400.

If you adjust your monthly payment slightly to $578, you will completely destroy that debt before the 18-month promotional clock runs out. By paying a one-time $400 fee, you save nearly $1,200 in interest and get out of debt six months faster.

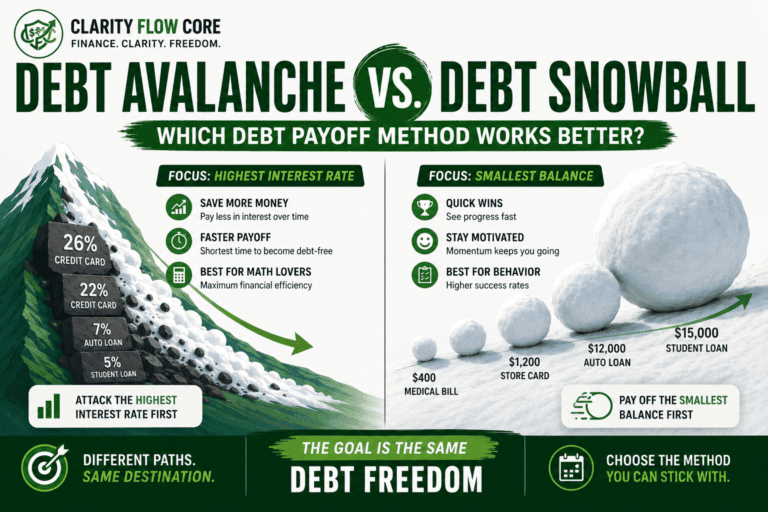

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyThe Execution: How to Actually Move the Money

Because a personal loan is classified as an installment loan (not revolving credit), you cannot simply type your personal loan account number into the online balance transfer portal of your new credit card. The systems rarely talk to each other directly.

To successfully execute a balance transfer personal loan payoff, you generally have to use one of two specific methods.

Method 1: The Convenience Check

Once you are approved for a new 0% APR credit card, the issuer will often mail your welcome packet. Tucked inside that envelope will be a set of blank checks, known as “convenience checks” or “balance transfer checks.”

You physically write this check out to your personal loan lender for the exact payoff amount. You mail it in. When the check clears, your personal loan is officially paid in full. The balance of that check is then applied to your new credit card at the 0% promotional rate.

Method 2: Direct Deposit to Checking

Today, many modern credit card issuers allow you to bypass physical checks entirely. During the balance transfer personal loan application process, the new credit card company will ask if you want the approved transfer amount deposited directly into your personal checking account.

If you select this option, the bank wires the cash (minus the transfer fee) into your standard bank account. Once the cash lands, you simply log into your personal loan portal and make a lump-sum electronic payoff.

The Ultimate Danger: The Cash Advance Trap

Warning: You must explicitly use the official balance transfer methods outlined above. Do not ever take your new credit card to an ATM, withdraw $5,000 in cash, and use it to pay off your loan.

If you do this, the bank classifies it as a “Cash Advance.” Cash advances completely ignore 0% promotional offers. You will be hit with an immediate 5% cash advance fee, and the balance will instantly start compounding at an exorbitant interest rate (often 28% or higher) from day one. It will destroy your balance transfer personal loan strategy immediately.

The Hidden Costs: Calculating the Fees

While the idea of 0% interest is incredibly appealing, moving money is rarely 100% free. Before initiating a balance transfer personal loan swap, you must calculate the friction costs.

1. The Balance Transfer Fee

Almost all 0% APR credit cards charge a one-time fee to move the debt. In the current market, the industry standard is between 3% and 5% of the total amount transferred.

If you move a $15,000 personal loan to a credit card that charges a 5% fee, the bank will immediately tack $750 onto your new balance. You must run the math to ensure the interest you save over the next year actually exceeds that $750 upfront cost. If you only have three months left on your personal loan, paying a massive transfer fee is a terrible mathematical decision.

2. The Ticking Clock

0% APR is a ticking time bomb. These promotional periods are strictly temporary, normally lasting between 12 and 21 months. If you do not pay off the entire transferred balance before the promotional period expires, the remaining debt will instantly be subjected to the card’s standard variable APR (which is almost always higher than your original personal loan rate).

The Operational Rule: Take the total amount you are transferring (including the upfront fee) and divide it by the number of months in your 0% promotional period. This is your new, mandatory monthly payment. If your budget cannot handle that specific payment, a balance transfer personal loan strategy is too risky for you.

How This Move Affects Your Credit Score

When you initiate a balance transfer personal loan payoff, you are fundamentally changing the type of debt on your credit report. This will cause your score to fluctuate. (If you aren’t familiar with how algorithms weigh different debts, review our guide on FICO vs. VantageScore: Why Credit Scores Differ Between Apps).

Here is exactly what happens behind the scenes:

- The Hard Inquiry: Applying for the new 0% APR credit card will trigger a hard inquiry on your credit report. This usually drops your score by a few points temporarily.

- The Utilization Shock: This is the biggest factor. Personal loans are installment loans; they do not heavily impact your “Credit Utilization Ratio.” Credit cards are revolving credit. If you move a $10,000 personal loan onto a new credit card that only has a $10,000 limit, that specific card is now at 100% utilization. The algorithm views a maxed-out credit card as extremely high risk.

Your credit score may temporarily fluctuate after the transfer due to the hard inquiry, new account opening, and sudden changes to your revolving credit utilization. However, as you aggressively pay down that credit card balance every month, your utilization will drop, and your score will ultimately rebound. (Master this specific metric by reading What Is Credit Utilization and Why Does It Matter?).

(Note: Because of these temporary score fluctuations, you should never execute this strategy if you are planning to buy a house or apply for a mortgage in the next six to twelve months).

When This Strategy Backfires

A balance transfer personal loan strategy is a high-level financial maneuver. If you lack discipline, it will completely blow up in your face. Here is exactly when this strategy backfires:

1. The Phantom Debt Trap

You successfully transfer your $10,000 personal loan to a 0% credit card. Your personal loan is now marked as “Paid in Full.” You feel a massive sense of relief.

Six months later, the transmission on your car dies. Because you don’t have a cash reserve (as outlined in Emergency Fund Basics: How Much Cash Should You Keep?), you are forced to take out a new personal loan to fix it. Now, you have a massive credit card balance and a new personal loan. You have doubled your debt. You must fix your underlying cash flow before moving debt around.

2. Missing a Minimum Payment

The 0% APR is a conditional contract. It requires flawless behavior. If you are even one single day late on your minimum monthly payment, the bank usually retains the right to revoke your 0% promotion instantly. Your rate will shoot up to a penalty APR, often exceeding 29.99%. You must put your minimum payment on autopay the exact day you activate the new card.

3. Mixing New Purchases

A balance transfer personal loan strategy only works if the card is used strictly as a quarantine zone for old debt. Do not use this new 0% card to buy groceries, gas, or new shoes. Often, the 0% promotion applies strictly to the transferred debt, not new purchases. If you buy something, that new purchase may start accruing high interest immediately.

When Is a Balance Transfer Worth Considering?

A balance transfer personal loan strategy is not a universal fix. It is a highly specific tool.

A balance transfer may be worth considering when:

- Your personal loan has a high interest rate.

- You qualify for a long 0% promotional period.

- The transfer fee is mathematically lower than the interest you expect to save.

- You can realistically pay off the balance before the promotional period expires.

- You are not planning to apply for a mortgage or major loan soon.

It may not be appropriate if:

- Your personal loan rate is already low.

- You cannot comfortably meet the aggressive required monthly payoff schedule.

- The upfront transfer fee exceeds your expected interest savings.

Frequently Asked Questions (FAQs)

Can you transfer a personal loan directly to a credit card?

Usually not. Most issuers require balance transfer checks or direct deposits rather than direct loan-account electronic transfers.

Does a balance transfer hurt your credit score?

It may cause a temporary fluctuation due to a hard inquiry and sudden changes in your credit utilization ratio.

What happens when the 0% APR period ends?

Any remaining balance generally begins accruing interest immediately at the card’s standard, variable APR.

Is a balance transfer cheaper than a personal loan?

Sometimes. It depends entirely on the transfer fee, the length of the promotional period, and your existing personal loan interest rate.

Can I transfer part of a personal loan balance?

In many cases, yes, provided the credit limit on the new card and the specific issuer rules allow it.

References & Trusted Sources

To verify the legal protections, fees, and rules regarding balance transfers and credit reporting, consult these official financial resources:

- Consumer Financial Protection Bureau (CFPB) – Balance Transfers

- Federal Trade Commission (FTC) – Credit Card Terms

- Federal Reserve – Consumer Credit Data

- Experian Credit Education

- myFICO Credit Education

The Bottom Line

Using a 0% APR credit card to execute a balance transfer personal loan payoff is a brilliant financial hack—but only if you treat it with militant discipline.

It stops the bleeding of high interest charges immediately and forces every dollar you pay to attack the principal balance. If you are currently using the Debt Avalanche vs. Debt Snowball method to clear your accounts, freezing the interest on your largest loan can drastically accelerate your timeline.

Run the math on the transfer fees, calculate your mandatory monthly payment, set up autopay, and use this strategy to recapture your financial freedom.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.