How Buying Bank-Repossessed Cars Actually Works

Let’s be brutally honest for a moment. Walking into a regular car dealership lot right now is a financial horror show.

Between the inflated list prices, the mandatory $800 “dealership documentation” fees, and used auto loans carrying 8% to 12% interest rates, financing a standard commuter car can easily wreck your monthly cash flow. You will spend five years paying off an asset that is actively plummeting in value.

If you are exhausted by the traditional dealership games and want to learn exactly how to buy bank repossessed cars, you are already ahead of the curve.

When someone defaults on their auto loan, the bank sends a tow truck to take the asset back. But banks do not want to be in the used car business. They are lenders. Every day that a vehicle sits in an impound lot, the bank loses money on storage fees and depreciation. They want that metal off their books immediately, which means they send them to auction to be liquidated for pennies on the dollar.

Here is the operational math behind the system, the strict rules of the auction lot, and exactly how to buy bank repossessed cars without accidentally buying a broken nightmare.

⚡ Quick Answer

Buying a bank-repossessed car usually involves purchasing a vehicle through an auction, credit union sale, or lender liquidation event. Because banks want to recover loan balances quickly, repossessed vehicles often sell below retail value. However, buyers typically purchase them “as-is” and should strictly budget for inspections, repairs, fees, and title processing delays.

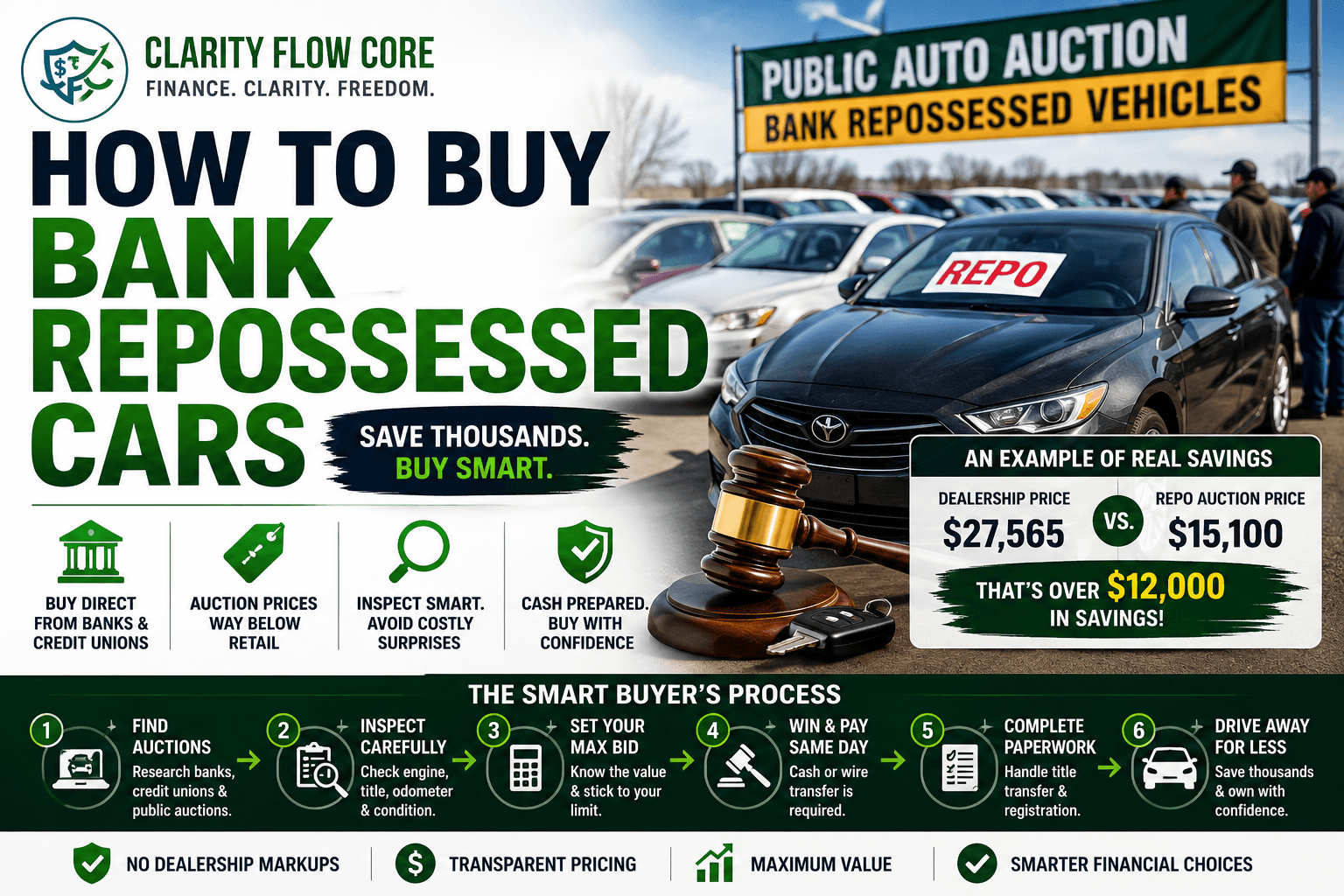

The Math: Dealerships vs. Repo Auctions

To understand how to buy bank repossessed cars effectively, you have to look at the raw numbers.

When a dealership takes in a trade-in, they have to recondition it, detail it, market it, pay the salesperson a commission, and build in a massive profit margin. When a bank sends a repo to auction, they simply want to recover the remaining balance of the defaulted loan.

Let’s look at a realistic scenario of a 5-year-old Honda Accord:

| Expense Category | Traditional Dealership | Bank Repo Auction |

| Vehicle Base Price | $22,000 | $14,500 (Winning Bid) |

| Dealership Doc Fees | $800 | $0 |

| Auction Buyer’s Premium | $0 | $600 |

| Financing (5 Years @ 8%) | $4,765 in interest | $0 (Paid in Cash) |

| Total Out-of-Pocket Cost | $27,565 | $15,100 |

The foundational rule of how to buy bank repossessed cars is that you are cutting out the middleman. By taking on the risk of buying the car exactly as it sits, you can save over $12,000 on a standard commuter vehicle.

Pros and Cons of Buying a Repossessed Car

Before executing this strategy, you must weigh the operational reality.

Pros:

- Potentially lower purchase price.

- Zero dealership markup or documentation fees.

- Opportunity to pay cash and avoid interest entirely.

- Wide variety of inventory across multiple brands.

Cons:

- Severely limited inspection opportunities.

- No warranty (sold strictly “As-Is”).

- Potential repair and maintenance costs.

- Auction buyer premiums and hidden fees.

- Title processing delays preventing immediate legal registration.

Step 1: Where the Inventory Actually Hides

A common hurdle when researching how to buy bank repossessed cars is simply finding the inventory. Not all vehicle auctions are open to the general public; many require a specialized dealer’s license to enter.

If you are a regular consumer, you have to target specific institutions:

- Local Credit Unions: This is the absolute best place for beginners to start. Smaller regional credit unions often do not have the volume to justify sending cars to massive auction houses. Instead, they will run a “sealed bid” auction right on their website or in their parking lot. You inspect the car, slide a piece of paper with your bid into a box, and the highest bidder wins.

- Public Auto Auctions: Facilities like GovPlanet, local police impound lots, and county fleet auctions are usually open to the public. You register online, pay a small refundable deposit to get a bidder paddle, and show up on a Saturday morning.

- Direct Bank Sales: Some major banks have online portals where they list their repossessed inventory directly to consumers before resorting to the auction block.

Step 2: The Financial Setup (Cash is King)

Before you can master how to buy bank repossessed cars, you must master your own liquidity. You cannot walk into an auction house and ask to speak to their finance manager. They do not have one.

Many repo auctions require immediate payment through cash, wire transfer, certified funds, or pre-arranged financing. When the gavel drops and you win the bid, you are usually expected to pay in full by the end of the business day.

If you have been practicing the 7 Everyday Saving Habits That Can Make a Real Difference, you might already have the cash sitting in a High-Yield Savings Account. If you do not have $15,000 in liquid cash, you must secure your funding before you even step onto the lot. Start building that reserve effortlessly today by learning How to Automate Savings Using Split Direct Deposit.

Some credit unions will pre-approve you for a specific “auction auto loan.” They will hand you a blank check with a hard spending limit (e.g., “Not to exceed $12,000”). You take that check to the auction. If you win a car for $10,000, you write the check for $10,000, and the credit union formalizes the loan the next day. (To guarantee you secure the best possible rate on this pre-approval, you must understand your algorithmic profile. Read FICO vs. VantageScore: Why Credit Scores Differ Between Apps before applying).

Step 3: The “Eyes-Only” Inspection

The most critical step in how to buy bank repossessed cars involves the inspection limitation.

At a dealership, you get to test drive the vehicle. You can take it on the highway and listen for weird suspension noises. At a repo auction, you get none of that. In most cases, the cars are lined up in a dirt lot. You are not allowed to drive them. You are rarely allowed to put the key in the ignition. You are buying a highly complex machine based almost entirely on an “eyes-only” assessment.

To survive this, you have to bring the right tools and know exactly what to look for.

| What to Check | How to Check It | What a Failure Looks Like (Walk Away) |

| Engine Oil | Pull the dipstick and wipe it on a white paper towel. | If the oil looks like a milky, brown milkshake, the head gasket is blown. The engine is dead. |

| Transmission Fluid | Pull the transmission dipstick. | If it smells burnt like campfire wood, the transmission is slipping and needs replacing. |

| Vehicle History | Write down the VIN from the windshield. | Run a CARFAX report on your phone. If it shows “Salvage Title” or “Flood Damage,” leave immediately. |

| Undercarriage | Bring a flashlight and look under the engine block. | Fresh puddles of red or black fluid mean active, expensive leaks. |

| The “Sniff Test” | Open the door and smell the interior. | A heavy mildew smell means water leaked into the cabin, which destroys the electrical system. |

Not every repossessed vehicle is a hidden bargain. Some were maintained meticulously by owners who simply experienced financial hardship, while others may have suffered years of deferred maintenance. The key is evaluating the individual vehicle objectively rather than assuming every repo is automatically a great deal.

Step 4: The Hidden Costs of the Auction Block

A common misconception about how to buy bank repossessed cars is that your winning bid is your final price. It never is. You must calculate the operational logistics of getting the car off the lot.

- The Buyer’s Premium: Auction houses do not work for free. They usually charge the buyer a premium on top of the winning bid. This can be a flat fee (like $400) or a percentage of the purchase price (usually 3% to 5%).

- The Key Problem: The reality of how to buy bank repossessed cars is that the previous owner rarely hands over the keys nicely when the tow truck arrives. Many repo cars are sold without keys. You will need to hire a mobile automotive locksmith to come to the lot, laser-cut a new key, and program the transponder chip. That usually costs $250 to $400.

- The Towing Logistics: Because you don’t know if the car is legally registered, insured, or mechanically safe to drive on the highway at high speeds, many smart buyers choose to tow auction purchases directly to an independent mechanic for a full inspection before driving them extensively. You need to factor in roughly $150 for a flatbed delivery.

When This Backfires: The Reality Check

Anyone teaching you how to buy bank repossessed cars will tell you that it carries massive risk. These are not certified pre-owned vehicles. You are buying the financial fallout of someone else’s life.

Here is exactly when and why the strategy backfires:

1. The “As-Is” Legal Trap

The biggest risk in how to buy bank repossessed cars is the legal paperwork. These vehicles are sold strictly “As-Is.” There is no cooling-off period. There is no Lemon Law protection. If you win the bid on a truck, tow it to your mechanic, and find out the engine block is cracked in half, you cannot return it to the bank. You own a very heavy, very expensive piece of scrap metal.

Because of this danger, you should never drain your bank account to win a bid. You must keep a robust cash buffer in your Emergency Fund Basics: How Much Cash Should You Keep? specifically dedicated to immediate post-auction repairs.

2. The Maintenance Sabotage

When discussing how to buy bank repossessed cars, we must address human psychology. If someone is struggling so badly financially that they cannot afford their $400 monthly car payment, they definitely stopped paying for $80 oil changes and $600 brake jobs a year ago.

Repossessed cars are almost universally neglected. Furthermore, if the previous owner knew the repo man was coming, they might have actively sabotaged the car out of spite. They might have poured bleach in the gas tank or stripped out the expensive touchscreen radio. You have to assume every repo car needs all of its fluids flushed, new brakes, and new tires on day one.

3. Title Delays

Another trap when learning how to buy bank repossessed cars is the title processing. You usually do not get the physical title handed to you on auction day. The auction house has to process the paperwork with the bank and the DMV, which can take 30 to 60 days. You cannot legally register or insure the car to drive it until that title arrives in your mailbox.

Frequently Asked Questions (FAQs)

Are bank-repossessed cars cheaper?

Often, yes. Repossessed vehicles can sell below retail market prices because lenders are focused strictly on recovering remaining loan balances rather than maximizing profit.

Can you finance a repossessed car?

Sometimes. Some banks, credit unions, and specialized auction lenders offer financing, but many public auctions require payment in full within a very short timeframe.

Are repossessed cars reliable?

It varies wildly. Some are well maintained, while others may have severe deferred maintenance or mechanical problems. A thorough visual inspection is absolutely critical.

Do repossessed cars come with warranties?

Generally no. Almost all auction and repo vehicles are sold strictly “as-is,” meaning you assume all mechanical and financial risks once you win the bid.

Is buying a repossessed car risky?

Yes. Lower prices often come with significantly greater uncertainty regarding the vehicle’s maintenance history, electrical health, and structural condition.

Step 5: Bidding Strategy and Mastering Your Ego

The psychological side of how to buy bank repossessed cars requires intense discipline. Auction fever is a real, hazardous psychological trap designed to separate you from your money.

If the auctioneer is talking fast, the adrenaline is pumping, and you are in a bidding war against a guy in a trucker hat across the aisle, your ego will try to take over. You will stop bidding on the value of the car and start bidding just to “beat” the other guy.

Before the bidding begins, determine your absolute maximum price. Take the Kelley Blue Book “Fair Condition” value, subtract the 5% buyer’s premium, subtract $300 for keys, and subtract $1,500 for a mechanical safety buffer.

Whatever number you are left with is your hard cap. If the bidding goes even one single dollar over your limit, put your hands in your pockets and walk away. There is always another auction next week.

The Bottom Line

The ultimate goal of how to buy bank repossessed cars is to save yourself from a decade of high-interest consumer debt.

If you blindly bid on the shiniest car on the lot without doing the mechanical checks, you will lose thousands of dollars. But if you execute how to buy bank repossessed cars correctly—by bringing a flashlight, sticking to a ruthless maximum bid, and keeping a cash reserve for repairs—you can bypass the dealership entirely.

If you successfully purchase your vehicle outright without a loan, you must understand the immediate algorithmic consequences by reading Why Your Credit Score Dropped After Paying Off Your Car Loan.

Get your cash ready, learn the warning signs, and go buy a reliable daily driver for a fraction of the retail price.

References & Trusted Sources

To verify the legal protections, values, and risks associated with purchasing used or repossessed vehicles, consult these official industry resources:

- Consumer Financial Protection Bureau (CFPB) – Auto Loans

- Federal Trade Commission (FTC) – Buying a Used Car Rule

- NADA Vehicle Values (J.D. Power)

- Kelley Blue Book (KBB)

- National Auto Auction Association (NAAA)

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.