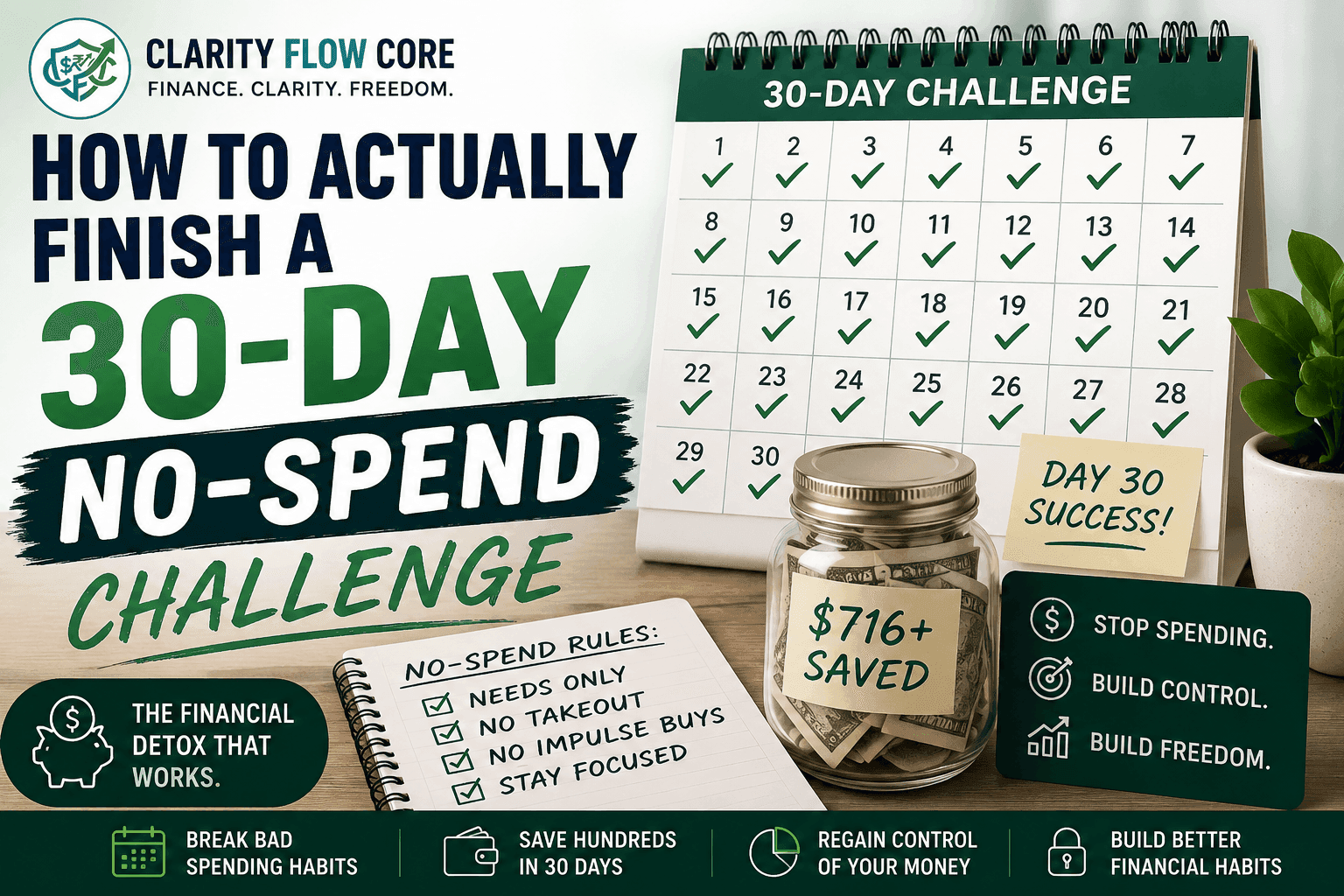

How to Actually Finish a 30-Day No-Spend Challenge

If your bank account is a bucket with a giant hole in the bottom, you cannot fix it by slowly pouring more water in. You have to plug the leak.

There are instances when the slow and steady approach to budgeting just doesn’t work. If you are in a cycle of ordering takeout four times a week, subscribing to apps you never use, and impulsively buying things off social media late at night, a slight budget adjustment won’t help.

You need a hard financial detox. You need a 30-day no-spend challenge.

It is not a permanent lifestyle shift. It is a quick, aggressive reset on your finances that breaks your poor spending habits, forces you to be creative with what you already have, and frees up a massive chunk of cash in exactly one month.

Here is the operational math behind why this works, the strict rules of the game, and a realistic guide to actually completing a 30-day no-spend challenge without quitting in week two.

⚡ Quick Answer

A 30-day no-spend challenge is a short-term financial reset where you eliminate all non-essential spending for 30 days. Essential expenses like rent, groceries, utilities, insurance, and transportation remain allowed, while discretionary purchases are paused to help save money and break spending habits.

What is a 30-Day No-Spend Challenge?

The premise is exactly what you think it is. For 30 days, you agree to spend a grand total of zero dollars on everything outside of fundamental survival needs.

This is the financial equivalent of a fasting protocol. The idea is not to punish yourself forever. The goal is to hit the pause button on consumerism so you can clearly see where your cash has been quietly draining. By removing the steady buzz of daily micro-transactions, you will suddenly discover exactly how much money you blow simply out of boredom or convenience.

Benefits of a 30-Day No-Spend Challenge

Why put yourself through a month of financial fasting? A successful no-spend challenge can help:

- Break emotional spending habits

- Reveal hidden subscription costs

- Increase emergency savings faster

- Reduce credit card debt

- Improve budgeting awareness

- Build healthier long-term financial habits

Many people are surprised by how little they miss certain purchases after the first two weeks. The challenge often reveals that convenience spending—not necessity—is what quietly drains monthly cash flow. Even if you never repeat the challenge, many participants report spending significantly less money for months after it ends because they become hyper-intentional with their future purchases.

The Rules: Needs vs Wants

To thrive in a 30-day no-spend challenge, you have to set incredibly strict guidelines on day one. If you leave things in a gray area, your brain will absolutely deceive you into justifying a “little treat.”

Here is the definitive breakdown of what you can and cannot buy:

| Category | The “Green Light” List (Allowed) | The “Red Light” List (Banned) |

| Housing & Utilities | Rent, mortgage, electricity, water, internet, cell phone. | Smart home upgrades, new decor, premium cable packages. |

| Food & Drink | Basic groceries to cook at home (rice, beans, chicken, vegetables). | Restaurants, drive-thrus, UberEats, $6 lattes, alcohol, convenience store snacks. |

| Transportation | Gas to get to work, public transit passes, basic repairs. | Car washes (use a hose), road trip gas, premium detailing. |

| Health & Personal | Vital prescriptions, basic toiletries (toothpaste, soap), toilet paper. | Haircuts, manicures, new makeup, skincare hauls. |

| Entertainment | Free local parks, library books, walking, existing subscriptions. | Movie tickets, concerts, bar tabs, buying new video games, late-night Amazon browsing. |

| Financial | Minimum debt payments, taxes, insurance premiums. | Investing extra money (save it in cash until the month is over to avoid cash flow traps). |

(Once you master these grocery and utility rules, you can easily integrate them into your permanent lifestyle by learning 7 Everyday Saving Habits That Can Make a Real Difference).

The Math: How Much Money Does This Actually Free Up?

A lot of people dismiss the 30-day no-spend challenge because they think cutting out coffee won’t make them rich. They are right—coffee won’t make you rich. But the aggregate total of all your impulsive spending over 30 days is staggering.

According to Consumer Expenditure Survey data from the Bureau of Labor Statistics, food away from home, entertainment, and discretionary shopping remain among the most common categories where households overspend.

Let’s look at a highly realistic scenario of a moderate spender over a typical month:

| Impulse Expense | Frequency | Cost Per Instance | Total Monthly Drain |

| DoorDash / Takeout | 2x per week | $35 | $280 |

| Coffee Shop Runs | 4x per week | $6 | $96 |

| Amazon Impulse Buys | 3x per month | $40 | $120 |

| Happy Hour / Drinks | 2x per month | $50 | $100 |

| Random Target/Store Runs | 2x per month | $60 | $120 |

| Total Cash Saved | $716 |

By simply existing and refusing to swipe your card for 30 days, you instantly manufacture over $700 in free cash flow. That is enough to wipe out a small credit card balance or fully fund a tier-one emergency fund in a single month.

Create Your Personal No-Spend Rules Before Day One

One of the biggest reasons people fail a 30-day no-spend challenge is that they start without defining their own rules. Every time an unexpected situation comes up, they end up negotiating with themselves. Those small exceptions eventually snowball until the challenge quietly disappears.

Before your challenge begins, spend fifteen minutes creating a simple set of personal rules. Write them down in a notebook or the notes app on your phone so you don’t have to make emotional decisions later.

For example, decide exactly how you will handle situations like:

- A friend invites you out for dinner.

- Your coworkers order lunch together.

- An online retailer sends you a “Today Only” discount.

- You discover a product you’ve wanted for months suddenly goes on sale.

- A family member asks you to split the cost of a gift.

Having predetermined answers removes almost all of the internal debate.

It also helps to create a small “approved alternatives” list before the challenge starts. Instead of going out for entertainment, plan free activities such as visiting a local park, borrowing books from the library, watching movies you already own, hiking, cooking new recipes with pantry ingredients, or inviting friends over for a game night instead of meeting at a restaurant.

Another useful strategy is to keep a simple spending journal throughout the month. Whenever you feel the urge to buy something, write down what you wanted to purchase, roughly how much it cost, and what triggered the impulse. After 30 days, you’ll often discover clear patterns. Maybe stress after work leads to food delivery orders, boredom results in online shopping, or social media browsing creates unnecessary purchases.

Those insights are often more valuable than the money you save because they reveal the habits that quietly drain your finances throughout the year. Once you identify those triggers, you can build permanent systems to reduce unnecessary spending long after the challenge ends.

Most importantly, the challenge teaches intentional spending—a habit that continues creating financial benefits long after the thirty days have ended.

The Pre-Game: How to Prepare

If you wake up on the first of the month and blindly decide to stop spending money, you will fail by day four. A successful 30-day no-spend challenge requires militant preparation.

1. Perform a Pantry Inventory

Check your kitchen before the challenge begins. Most of us have half-empty boxes of pasta, frozen vegetables, and canned foods sitting in the back of the pantry. Your goal for this month is to eat your inventory. Base your grocery list only on the missing ingredients needed to turn those random items into actual meals.

2. Unsubscribe & Delete

Your phone is a digital mall designed to extract your money. Opt out of promotional emails from your favorite clothing brands. Delete the Amazon, DoorDash, and UberEats apps from your home screen. You cannot buy what you do not see. (If you are a freelancer with highly variable income, eliminating these recurring digital temptations is critical. Read How to Budget as a Freelancer When Income Changes Every Month to stabilize your cash flow).

3. Manage Social Friction

The number one reason individuals fail a 30-day no-spend challenge is peer pressure. You have to tell your friends and family exactly what you are doing. If they invite you to a $40 brunch, you have to be comfortable saying, “I’m doing a strict financial detox this month, but come over later and I’ll make coffee.” If your no-spend challenge is the result of an unexpected layoff rather than a personal goal, I Lost My Job: A 30-Day Financial Survival Plan provides a step-by-step strategy for prioritizing bills, protecting your emergency fund, and managing the first month of unemployment.

The 4-Week Reality (A Survival Guide)

If you have never done this before, the psychological phases of the month are highly predictable. Here is exactly what to expect.

Week 1: The Honeymoon Phase

Starting a 30-day no-spend challenge feels exciting. You are motivated. You meal-prep on Sunday, you bring your lunch to work, and you feel entirely in control of your life. Week one is easy.

Week 2: The Deprivation Dip

This is where 80% of people quit. The novelty has worn off. You are tired of eating the meals you prepped. Your friends are going out on Friday night, and you are sitting at home watching TV. The impulse to spend money just to feel a dopamine hit is intense. Understanding exactly why emotional spending happens during periods of deprivation is key to surviving this week.

Operational Fix: Implement the 48-Hour List. When the desperate urge to buy something hits, write it down on a piece of paper. Tell yourself you can buy it on day 31. This satisfies the brain’s need to acknowledge the item without actually spending the cash.

Week 3: The Routine Shift

If you survive week two, week three gets easier. You have naturally begun to implement everyday saving habits. You stop habitually opening shopping apps. You realize that you can actually survive a stressful Tuesday at work without immediately buying takeout on the way home.

Week 4: The Finish Line

You are staring at your bank account, and the balance is higher than it has been in months. The motivation returns because you can clearly see the mathematical results of your discipline. You coast to the finish line.

When This Backfires

A 30-day no-spend challenge is a highly effective tool, but it has sharp edges. If you fall into these common traps, the strategy completely collapses:

- The Day 31 Binge: This is the most common point of failure. You successfully complete the month, save $800, and feel so deprived that on day 31, you go to the mall and blow $600 on clothes and a fancy dinner to “reward” yourself. You just erased a month of hard work in three hours.

- The Hoarding Loophole: Some people “prepare” for a no-spend month by spending $500 at Costco on the 31st of the previous month so they don’t have to buy anything during the challenge. That isn’t a no-spend challenge; that is just shifting your billing cycle.

- Ignoring Actual Maintenance: The point of a 30-day no-spend challenge is to stop wasting money on garbage, not to ignore your responsibilities. If your car dashboard throws a check engine light, or you get a toothache, pay for it. Delaying vital maintenance will always cost you significantly more money down the road.

Frequently Asked Questions (FAQs)

Can I buy groceries during a no-spend challenge?

Yes. Basic groceries and essential household items are generally allowed.

Can I pay bills during a no-spend challenge?

Absolutely. Rent, utilities, insurance, debt payments, and other obligations continue as normal.

What if I have an emergency?

Emergencies are exceptions. The goal is to eliminate unnecessary spending, not ignore important health or safety needs.

How much money can I save during a no-spend month?

The amount varies, but many people save hundreds of dollars by eliminating discretionary purchases.

Is a no-spend challenge worth it?

A no-spend challenge can be worthwhile for people who feel stuck in a cycle of impulse spending, subscription creep, or lifestyle inflation. While it is not a permanent budgeting solution, it can help reset spending habits and increase awareness of where money is going.

Can couples do a no-spend challenge together?

Yes. Many people find that accountability from a spouse or partner makes the challenge much easier to complete.

What to Do With Your Savings

At the conclusion of the 30 days, you are going to log into your checking account and see hundreds of dollars just sitting there. Do not let it sit in your checking account. Idle cash gets spent.

Before the month is even over, you need a plan for those funds.

If you do not have a cash reserve, you need to route that money immediately into safety. Read Emergency Fund Basics: How Much Cash Should You Keep? to set your target, and then review HYSA vs. Money Market Account: What’s the Difference? to find a secure place that actually pays you interest on that money.

If you are dealing with toxic, 24% credit card debt, use that lump sum to execute a massive payment against your principal. If you are unsure which card to pay off first, read up on Debt Avalanche vs. Debt Snowball: Which Debt Payoff Method Works Better? to form your attack plan.

Once you deploy the cash, you need to establish a sustainable baseline. You cannot live on a 30-day no-spend challenge forever, but you can take the discipline you just built and transition it into The 50/30/20 Budget Rule Explained Simply.

You have successfully plugged the leak. Now, you can actually start filling the bucket.

Budgeting & Spending Resources

A successful no-spend challenge is built on understanding your spending habits—not simply avoiding purchases for 30 days. The following resources offer practical guidance on budgeting, consumer spending, financial wellness, and building sustainable money habits.

- Consumer Financial Protection Bureau (CFPB) – Explore tools and educational resources for budgeting, managing everyday expenses, and improving your overall financial well-being.

- Bureau of Labor Statistics (BLS) – Consumer Expenditure Surveys – National data showing how U.S. households spend money across categories such as food, transportation, housing, and entertainment.

- MyMoney.gov – U.S. government financial education covering budgeting, saving, goal setting, and responsible money management.

- Federal Deposit Insurance Corporation (FDIC) – Money Smart – Free financial education on budgeting, spending decisions, emergency savings, and long-term financial planning.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit budgeting assistance, financial counseling, and debt management resources if overspending has led to financial hardship.

- Consumer.gov – Consumer education on budgeting, spending wisely, avoiding scams, and managing money effectively.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. Financial situations, spending habits, and budgeting needs vary from person to person. Before making major financial decisions, consider consulting a qualified financial professional or advisor. Any products, services, or financial strategies mentioned may vary based on individual eligibility, lender terms, or personal circumstances.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.