Index Funds vs. Mutual Funds: What Beginners Should Know

If you have recently taken the plunge and opened a brokerage account or a Roth IRA, congratulations. You have cleared the biggest psychological hurdle in personal finance. But if you are trying to understand the mathematical reality of index funds vs mutual funds, the choices can feel incredibly overwhelming the moment you log into your dashboard.

You transfer your hard-earned cash in, and then you are faced with a terrifying blank search bar asking for a “ticker symbol.” You are suddenly supposed to know exactly what to buy. If you search for basic investing advice, you will immediately be hit with a massive wall of financial jargon, and the two terms you will see aggressively fighting for your attention are Index Funds and Mutual Funds.

⚡ Quick Answer

- Index funds are investment funds that passively track a market index, such as the S&P 500.

- Actively managed mutual funds use professional fund managers who attempt to outperform the market.

- The Verdict: For many long-term investors, low-cost index funds are popular because of their broad diversification, significantly lower fees, and tax efficiency.

When I first started trying to build wealth, I assumed I had to spend three hours a day reading the Wall Street Journal, analyzing balance sheets, and picking individual winning stocks to be successful. That couldn’t be further from the truth. The smartest, wealthiest retail investors are using “funds”—which are basically pre-packaged baskets of stocks—to build wealth completely on autopilot.

But not all baskets are created equal. The mechanics operating behind the scenes of these funds—and more importantly, the fees they secretly siphon from your returns—are drastically different. One relies on highly paid Wall Street managers trying to predict the future, while the other simply rides the mathematical wave of the American economy.

Here is the ultimate, operational breakdown of index funds vs mutual funds, the hidden math of expense ratios, and exactly which one actually deserves your capital.

The Foundation: What is a Fund?

Before we pit index funds vs mutual funds against each other, we need to understand the structural foundation they share.

Let’s assume you have $500 to invest. You could go out and buy a couple of shares of a single company, like Apple or Tesla. But what if that specific company has a terrible year? What if their CEO resigns or a product fails? Your entire portfolio crashes. Putting all your eggs in one basket is incredibly risky.

To mitigate this risk, you need “diversification”—buying a tiny piece of hundreds of different companies so that if one sector of the economy fails, the others hold your net worth up. But you do not have enough cash to buy one individual share of 500 different companies.

Enter the “Fund.” A massive financial institution (like Vanguard or Fidelity) pools together money from hundreds of thousands of regular investors just like us. They take that massive billion-dollar pool of cash and buy a giant basket containing shares of hundreds or thousands of different stocks. Then, they sell you a “share” of that basket.

By buying just one single share of a fund, you instantly own a microscopic piece of every single company inside it.

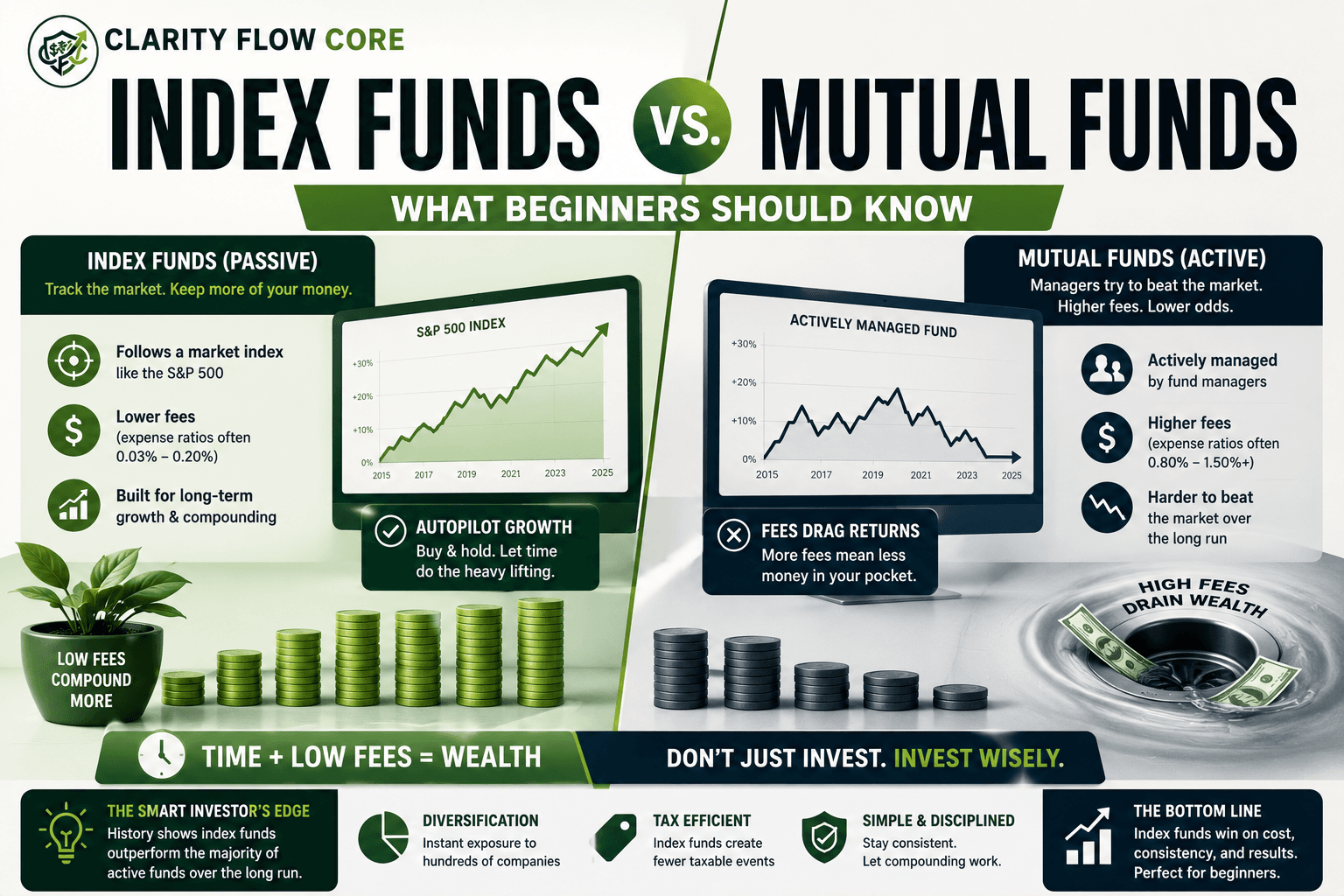

(Note: Technically, many index funds are structured as mutual funds. The real comparison in the financial world is between passively managed index funds and actively managed mutual funds).

The Heavyweight: Mutual Funds (Active Management)

When you hear your parents or grandparents talk about their retirement accounts, they are almost certainly talking about traditional, actively managed mutual funds. This has been the standard way for Americans to invest for decades.

A traditional mutual fund is actively managed. This means there is a team of highly educated, very expensive Wall Street fund managers sitting in a high-rise office. Their entire job is to analyze the stock market, read corporate earnings reports, and actively choose which stocks to buy, sell, or hold inside your basket.

Their ultimate goal? To “beat the market.” They are trying to find the hidden gems and avoid the losers so that your portfolio grows faster than the average stock market return.

It sounds amazing in theory. When comparing index funds vs mutual funds, why wouldn’t you want a financial genius actively managing your money?

The Hidden Killer: Expense Ratios

Because those managers do not work for free. To pay for their massive salaries, their research terminals, and their high-rise offices, mutual funds charge you a fee called an Expense Ratio.

A typical actively managed mutual fund’s expense ratio will often range from roughly 0.5% to 1.5% or more. That might sound like pennies, but in the investing world, it is a devastating leak in your financial boat. That fee is charged every single year on your entire balance, regardless of whether the fund made you money or lost you money.

If you leverage The 50/30/20 Budget Rule Explained Simply to build up a $100,000 portfolio in a mutual fund with a 1.5% expense ratio, you are paying them $1,500 this year. If the fund has a terrible year and loses 5% of its value, you still have to pay them $1,500.

Over a 30-year investing career, that tiny fee will literally eat hundreds of thousands of dollars of your potential compound interest.

And the absolute worst part of the index funds vs mutual funds debate? Despite their expensive degrees, the vast majority of active mutual fund managers actually fail to beat the average market return over a 10- or 20-year period. You are paying premium, luxury prices for mediocre, sub-standard performance.

The Modern Champion: Index Funds (Passive Management)

If mutual funds are driven by an expensive human pilot, index funds are driven by a free, emotionless autopilot.

An index fund is passively managed. Instead of hiring a team of humans to guess which stocks will go up, an index fund simply copies a specific, mathematical list—or “index”—of companies.

The most famous index in the world is the S&P 500, which is simply a list of the 500 largest, most profitable publicly traded companies in the United States (think Apple, Microsoft, Amazon, Google, etc.).

If you buy an S&P 500 Index Fund, the computer algorithm managing the fund automatically buys stock in those exact 500 companies. If a company has a bad year and falls out of the top 500, the computer automatically sells it. If a new company grows big enough to enter the top 500, the computer buys it.

There is no guessing. There is no crystal ball. The fund simply mirrors the health of the broader American economy.

The Magic of Near-Zero Fees

When calculating the operational math of index funds vs mutual funds, the fees are what dictate the winner. Because there are no expensive managers, analysts, or fancy offices to pay for, index funds are unbelievably cheap to run.

Instead of a 1.5% expense ratio, a standard S&P 500 Index Fund usually has an expense ratio of around 0.03% to 0.04%. Some brokerages (like Fidelity) even offer index funds with a staggering 0.00% expense ratio.

Let’s look at the math on that exact same $100,000 portfolio. With an index fund charging a 0.03% expense ratio, you are only paying $30 a year in fees.

That is $1,470 every single year that stays inside your account, compounding and aggressively growing your wealth, rather than paying for a fund manager’s summer home.

Tax Efficiency: The Unseen Advantage of Indexing

Beyond the fees, there is another massive operational reason modern investors favor one side of the index funds vs mutual funds debate, especially if you are investing in a standard, taxable brokerage account. (If taxes are your main concern right now, read Standard Deduction vs. Itemizing: Which Option Saves More?).

It all comes down to the “turnover rate” and capital gains taxes.

In an actively managed mutual fund, the manager is constantly buying and selling stocks inside the basket, desperately trying to beat the market. Under US tax law, every time they sell a stock for a profit within that fund, it triggers a capital gains tax event. At the end of the year, the mutual fund legally passes those tax bills down to you, the shareholder.

This means you could end up owing the IRS a massive tax bill on your mutual fund in April, even if you personally didn’t sell a single share of the fund yourself!

Index funds, on the other hand, have an incredibly low turnover rate. Because they just sit there and track a static list of 500 companies, they rarely buy and sell. This makes them incredibly tax-efficient, ensuring you keep the IRS entirely out of your pockets until you actually decide to sell your shares decades down the road.

When This Strategy Backfires

While the mathematical winner of the index funds vs mutual funds debate is clear, buying index funds is not a flawless, risk-free ticket to millions. The strategy requires intense behavioral discipline. Here is exactly when indexing backfires on beginners:

1. Panic Selling During a Correction

Index funds mirror the broader stock market. Historically, the stock market goes up. However, the market also crashes. In 2008, the S&P 500 lost roughly 38% of its value. If you look at your portfolio during a crash, panic, and sell your index funds to “stop the bleeding,” you permanently lock in your losses. Indexing only works if you have the emotional discipline to leave the money alone for decades, regardless of what the news cycle says.

2. The False Diversification Trap

Beginners often misunderstand diversification. They will buy an S&P 500 index fund (like VOO), a Total Stock Market index fund (like VTI), and a large-cap growth fund, thinking they are heavily diversified.

They aren’t. VTI is roughly 80% comprised of the exact same 500 companies that make up VOO. You are just buying the exact same stocks twice. You only need one core US index fund to capture the market.

3. Ignoring Asset Allocation

If you are 64 years old and planning to retire next year, you should not have 100% of your net worth in an S&P 500 index fund. If the market crashes the week before you retire, your lifestyle is ruined. As you get closer to needing the cash, you must transition a portion of your portfolio out of volatile index funds and into stable assets. (Make sure your immediate cash needs are protected by reading Emergency Fund Basics: How Much Cash Should You Keep?).

Frequently Asked Questions (FAQs)

Are index funds safer than mutual funds? Neither is risk-free, but index funds are often more diversified and generally have significantly lower fees, reducing the drag on your returns.

Can an index fund lose money? Yes. Index funds rise and fall with the broader market.

Are index funds good for beginners? Many investors consider index funds highly beginner-friendly because they offer broad diversification and require almost zero ongoing active management.

Do index funds pay dividends? Yes, many index funds distribute dividends generated by the underlying companies they hold.

Can I own both index funds and mutual funds? Yes. Many investors use a combination of both depending on their specific financial goals and risk preferences.

The Verdict: Why the Math Favors Indexing

If it sounds like I am heavily biased when comparing index funds vs mutual funds, it is because I am—and the math backs me up completely.

In 2007, legendary investor Warren Buffett famously made a $1 million bet against the hedge fund industry. He bet that a simple, low-cost S&P 500 Index Fund would outperform a hand-picked portfolio of actively managed funds over a 10-year period.

Ten years later, Buffett won the bet by a landslide. The active managers couldn’t overcome the mathematical drag of their own expensive fees. (It should always be noted that past performance does not guarantee future results).

The financial playbook is clear. Unless you are a Wall Street insider or an institutional investor, you do not need to pay a premium for active management. Your core strategy should be built on low-cost, broadly diversified index funds. It is the ultimate “set it and forget it” wealth-building machine.

Actionable Steps: How to Buy Your First Index Fund

So, how do you actually execute this? If you are staring at your brokerage account right now, here is exactly how to navigate the index funds vs mutual funds landscape.

- Ignore the Dashboard Marketing: When you log into Fidelity, Vanguard, or Charles Schwab, they will often heavily advertise their own actively managed mutual funds on the home screen because that is how they make the most money. Ignore the splashy ads.

- Check the “Expense Ratio”: Before you click buy on any fund, look for the data point labeled “Expense Ratio” or “Net Expense Ratio.” If that number is over 0.20%, you should strongly reconsider. You are actively looking for numbers like 0.03% or 0.015%.

- Look for the Classics: You don’t need to get fancy. The bedrock of most millionaire portfolios is a simple S&P 500 Index Fund or a Total Stock Market Index Fund.

- If you use Vanguard, you might look at VOO (their S&P 500 fund) or VTI (their Total Market fund).

- If you use Fidelity, you might look at FXAIX or FSKAX. (Note: These are historical examples of low-cost funds, not specific investment advice. Always verify the ticker symbol in your own brokerage).

- Automate It: The true power of index funds is consistency. Set up an automatic transfer from your checking account every month on payday, have it automatically purchase shares of your chosen index fund, and then close the app. (You can read more about the power of automation in How to Automate Savings Using Split Direct Deposit).

The Bottom Line

Investing does not have to be a full-time job. You do not need to read stock charts or predict the next big tech trend. By mastering the math of index funds vs mutual funds and choosing passive management, you keep your fees near zero, optimize your taxes, and guarantee that you will capture the long-term growth of the economy.

Ensure your daily banking is optimized alongside your investments by deciding How Much Should You Keep in Checking vs Savings? and exploring HYSA vs. Money Market Account: What’s the Difference?. Then, automate your index fund contributions and let compound interest do the heavy lifting.

References & Trusted Sources

To further verify the differences in fund structures, diversification, and fee regulations, consult these official educational resources:

- U.S. Securities and Exchange Commission (SEC) – Mutual Funds and ETFs

- Investor.gov – Diversification Basics

- FINRA – Understanding Mutual Fund Fees

- Vanguard – Index Fund Investing

- Morningstar – Fund Expense Ratios

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

3 Comments

Comments are closed.