What Happens If You Only Pay the Minimum on a Credit Card?

Quick Answer:

If you only pay the minimum on a credit card, your account technically stays in “good standing,” meaning you avoid late fees and protect your payment history. However, you trigger a massive compounding interest trap. The bank completely revokes your interest-free grace period, charging you an average of 20% to 24% interest compounded daily on your remaining balance. This leaves your principal virtually untouched and stretches a minor balance into a decades-long debt cycle.

You open your monthly credit card statement, and there it is: a total balance of $2,500. Right next to it, highlighted in a clean, non-threatening box, is your Minimum Payment Due: just $50.

Psychologically, the bank has designed this to feel like a massive win. Your brain rationalizes, “I can keep $2,450 in my checking account this month, hand the bank a crisp $50 bill, and keep my financial life moving without missing a beat.”

This is the most profitable trap in the entire banking sector.

When you only pay the minimum on a credit card, you are not actually paying off your debt. You are simply paying the bank a monthly subscription fee to keep them from reporting you to the credit bureaus.

Early in my financial journey, I utilized this exact method during a tight month after an expensive car repair. I figured I would just pay the $35 minimum and handle the rest later. It took me six months of making those tiny payments to realize my total balance hadn’t dropped by more than a couple of double cheeseburgers. I was running on a financial treadmill, and the bank was controlling the speed.

If you are currently carrying a balance and relying on minimum payments, you must look at the cold operational math. Here is the definitive editorial breakdown of what happens when you slice your bill down to the bare minimum, how the algorithm calculates your debt, and the exact playbook to break the cycle.

The Illusion of Safety: What a Minimum Payment Actually Does

To understand why this system is so dangerously sticky, we have to look at what the minimum payment legally achieves. It does exactly two things:

- It satisfies your contractual agreement for the month, completely preventing late fees.

- It marks your account as “current” on your credit report, safeguarding your 35% FICO payment history metric.

Because of this, many consumers assume they are perfectly safe. They treat their credit card like a standard installment loan—similar to a car payment or a student loan—where making the required monthly payment steadily kills the balance.

But a credit card is revolving debt, and the structural math is entirely different.

The Brutal Math: How the Minimum Due is Calculated

The bank does not pull your minimum payment out of thin air. It is calculated using a highly calculated corporate formula designed to do one specific thing: keep you in debt for as long as humanly possible while preventing you from legally defaulting.

Most major credit card issuers calculate your minimum payment using the “Percent + Interest” method. Your monthly minimum is typically the greater of $25–$35, OR:

Minimum Payment = (1% to 2% of Total Principal Balance) + New Interest Charges + Late Fees

Look closely at that formula. The bank is only requiring you to pay down a microscopic 1% to 2% of the actual cash you borrowed (the principal). The rest of that minimum payment is simply covering the interest you accumulated during the previous 30 days.

Want to see how this plays out with real numbers? Use our Credit Card Interest Calculator to estimate your payoff timeline, total interest paid, and how even small extra payments can dramatically reduce debt.

The Immediate Elimination of the Grace Period

The absolute second you pay anything less than the full Statement Balance, you kill your Interest-Free Grace Period.

Normally, if you pay your bill in full every month, the bank charges you 0% interest on your purchases. The moment you carry even $1 of debt past the due date, that grace period vanishes into thin air. Not only does your remaining balance immediately begin accruing interest, but every single new purchase you make moving forward starts racking up interest the exact day you swipe the card.

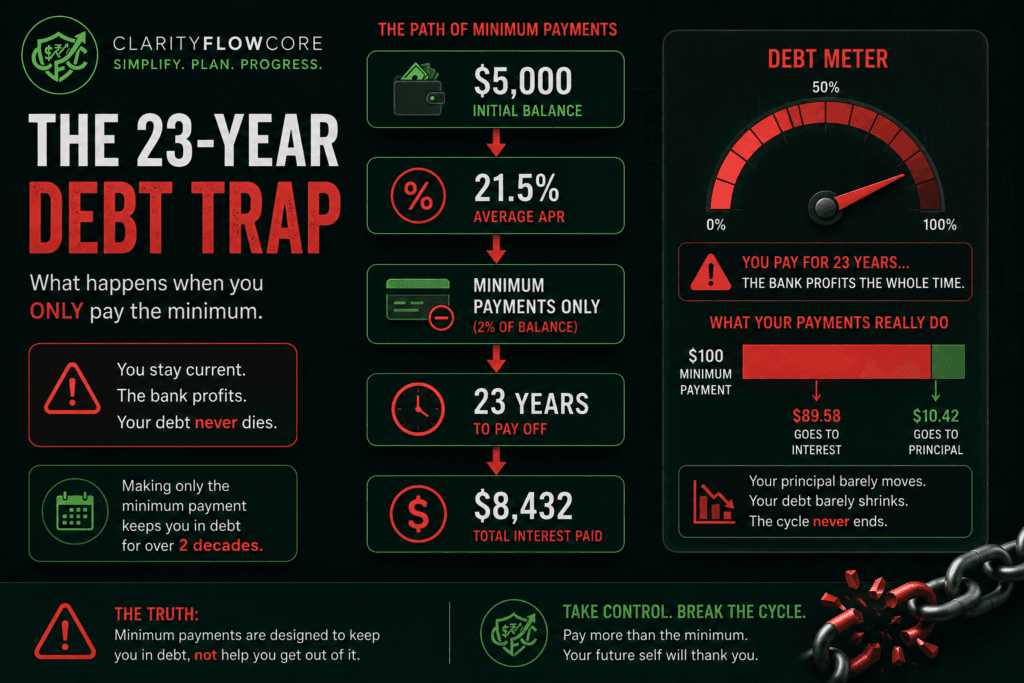

The Case Study: The 30-Year $5,000 Trap

Let’s look at a raw, real-world numerical example to see how this operational layout functions over a long timeline.

Suppose you have a $5,000 balance on a rewards credit card. Because inflation and market shifts have pushed rates up, your card currently has an average Annual Percentage Rate (APR) of 21.5%. Your bank calculates your minimum payment as 2% of the total balance or $30, whichever is higher.

If you stop spending on the card entirely and only pay the minimum on a credit card every month, here is the exact trajectory of your money:

| Financial Metric | The Minimum Payment Reality |

| Initial Debt Balance | $5,000 |

| Credit Card APR | 21.5% |

| Initial Minimum Payment Due | $100 |

| Time Required to Hit a $0 Balance | 23 Years (276 Months) |

| Total Principal Repaid | $5,000 |

| Total Interest Paid to the Bank | $8,432 |

| True Cost of Your Original Purchases | $13,432 |

Think about this editorial reality: if you used that card to buy a couch, a computer, and a weekend vacation, you will still be sending a check to the bank for those items long after the couch has rotted in a landfill and the computer has become obsolete tech. You paid a premium of $8,432 in pure interest to a multibillion-dollar institution for the luxury of making slow payments.

The Collateral Damage: Why Your Credit Score Will Take a Hit

Many consumers are shocked to discover that their credit score is actively dropping month after month, even though they have an unblemished record of on-time minimum payments. They call the customer service line, furious because they think the algorithm has a glitch.

It doesn’t. Your score is dropping because of your Credit Utilization Ratio.

As we established in our foundational guide, your credit utilization represents exactly 30% of your total FICO score. It measures your current balances against your total credit limits.

When you only pay the minimum on a credit card, your principal balance decreases at a painful, glacial pace. If your card has a $5,500 limit and you owe $5,000, your utilization is locked in at a dangerous 90.9%.

The algorithm views anyone sitting above a 30% utilization rate as a major risk factor. It assumes you are drowning financially and using your credit cards to artificially sustain your lifestyle. By leaving your balance virtually untouched month after month, you lock your credit score into an anchor. You will never qualify for prime interest rates on a home mortgage or a car loan as long as that utilization remains choked.

📈 Check Your Credit Utilization Risk

Credit utilization is one of the most influential credit score factors. Use our Credit Utilization Calculator & Recovery System to see where you stand and discover ways to improve your utilization ratio.

When This Backfires: The Operational Traps

Relying on the minimum payment safety net is like walking through a minefield. The moment your life experiences a slight cash flow disruption, the strategy backfires aggressively:

1. The “Minimum Payment Increase” Shock

Many people do not realize that minimum payments are dynamic. If you have a $5,000 balance and you suddenly have to swipe the card for a $1,500 emergency medical expense, your balance jumps to $6,500.

Because your balance went up, your interest charges for the month also jumped significantly. Your next minimum payment won’t just go up by a few dollars—it could instantly double to cover the massive influx of new interest. If your budget is already stretched to the limit, this sudden payment shock can cause you to default entirely.

If missed payments eventually cause your account to be sent to collections, don’t ignore the situation or agree to the first offer you receive. How To Handle Debt Collectors Without Making Things Worse explains how to verify the debt, understand your rights, and negotiate effectively.

2. The Rewards Delusion

“But I’m earning 2% cash back on my purchases!”

This is the classic justification used by consumers who carry a balance on a premium rewards card. They willingly pay a 22% interest rate to chase a 2% rewards rate.

Let the math sink in: you are actively giving the bank $22 in interest charges just so they can hand you a $2 statement credit. You are operating at a net loss of 20%. If you carry a balance, your rewards are completely meaningless. The interest charges erase the perks within the first 48 hours of the billing cycle.

3. The Balance Freeze

If you carry a high utilization balance for too long while making only minimum payments, the bank’s internal risk software will flag your account. To protect themselves from a potential bankruptcy, the bank may execute an operational move called “Balance Chasing.” Every time you pay your principal down by $20, the bank will immediately lower your total credit limit by $20. They freeze your available credit so you can never swipe the card again, leaving you trapped with a maxed-out card and zero financial flexibility.

The Operational Deficit: Running the Numbers

To visualize the sheer speed at which your money is being redirected away from your actual net worth, let’s look at how the bank splits a single $100 minimum payment during month one of your debt cycle:

Your $100 Payment

├── $89.58 ──> Bank's Pure Profit (Interest Charges)

└── $10.42 ──> Actual Debt Reduction (Principal)

Out of your hard-earned hundred-dollar bill, only $10.42 went toward actually lowering what you owe. The remaining $89.58 vanished completely into corporate interest margins. That is not a wealth-building strategy; it is an absolute financial drain.

How to Escape the Minimum Payment Treadmill

If you are currently trapped in this cycle, you must shift your strategy from a passive consumer to an aggressive asset manager. Here is the operational playbook to wipe out the balance fast.

Step 1: Execute a Mid-Cycle Emergency Payment

Do not wait for your statement due date to pay your bill. Credit card interest is calculated using your Average Daily Balance. If you get paid bi-weekly, send $50 or $100 to your credit card the exact day your paycheck hits your checking account. By lowering your balance early in the month, you reduce the average daily figure the bank uses to calculate your interest, mathematically shrinking your next monthly bill.

Step 2: Leverage the Balance Transfer Loophole

If your credit score is still floating in the good tier (above 690), you have a massive window of opportunity. You can apply for a 0% APR Balance Transfer Card.

These specialized cards allow you to move your high-interest $5,000 balance over to a new bank in exchange for a small upfront fee (usually 3% to 5%). In return, the new bank pauses your interest charges completely for 15 to 21 months.

The Operational Power Move:

Without a 21.5% interest rate eating your money every month, 100% of your monthly payment goes directly toward crushing your principal debt. A $200 monthly payment that would have barely moved the needle on your old card will now completely wipe out your debt in under two years.

Step 3: Implement the Debt Avalanche

If you have multiple cards, stop trying to pay a little bit extra on all of them. Line your cards up from the highest interest rate down to the lowest interest rate.

Set every single card to Autopay for the absolute Minimum Balance to protect your credit score and avoid late fees. Then, take every single spare dollar from your monthly budget and throw it entirely at the card with the highest interest rate. Once that card hits a $0 balance, take its entire payment capacity and roll it into the next highest card. This is the fastest, most mathematically efficient way to dismantle revolving debt.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyFrequently Asked Questions (FAQs)

1. Does paying only the minimum payment protect my credit history?

Yes. Making your minimum payment on time satisfies your monthly credit agreement. Your bank will report the account as “Current” to the credit bureaus, keeping your payment history metric completely green. However, it will severely hurt your score via your credit utilization ratio if the balance remains high.

2. Can I use my credit card rewards to pay the minimum balance?

Yes, most credit card issuers allow you to redeem your accrued points or cash back as a statement credit. If your minimum payment is $35 and you have $35 worth of rewards points, you can use them to cover the minimum due. However, remember that carrying a balance means the interest charges have already wiped out the true value of those rewards.

3. What is the difference between the Minimum Amount Due and the Statement Balance?

The Statement Balance is the total amount of money you charged to the card during the 30-day billing cycle. Paying this number in full completely protects your interest-free grace period. The Minimum Amount Due is simply the smallest amount you can pay to avoid default and penalties.

4. Why did my minimum payment suddenly go up if I didn’t buy anything new?

If your credit card has a Variable APR (which almost all modern credit cards do), your interest rate is directly tied to the Federal Reserve’s prime rate. If the Federal Reserve raises interest rates to combat inflation, your card’s APR automatically increases. This means your monthly interest charges go up, forcing your minimum payment higher even if your balance stayed the same.

5. Is it ever okay to only pay the minimum due?

Yes, as a temporary triage strategy during an absolute financial emergency. If you lose your job or face a massive medical expense, paying the minimum due allows you to hoard your liquid cash in a high-yield savings account while keeping your credit score from tanking. However, this should only be used for 1 to 2 months max while you re-stabilize your budget.

The Bottom Line

The credit card minimum payment is a brilliant piece of behavioral psychology. It makes an unmanageable debt look completely affordable by packaging it into a tiny, bite-sized monthly fee.

Stop playing the bank’s game on their terms. If you only pay the minimum on a credit card, you are signing a multi-decade contract to hand your wealth over to corporate shareholders. Treat your balances as an emergency that requires immediate, aggressive intervention. Automate your minimums to keep your record clean, cut out unnecessary spending, deploy the debt avalanche, and reclaim control of your monthly cash flow.

Once you’ve broken free from the minimum-payment cycle and are rebuilding your credit, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you establish healthier credit habits and strengthen your credit profile over time.

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Credit Cards – Learn how credit card interest, minimum payments, grace periods, and billing cycles work, along with your rights as a cardholder.

- FICO® – What’s in Your FICO® Score? – Understand how payment history and credit utilization influence your credit score, and why carrying high balances can affect future borrowing.

- Federal Trade Commission (FTC) – Credit, Loans, and Debt – Official consumer guidance on managing credit card debt, avoiding costly borrowing mistakes, and improving your financial health.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit credit counseling, debt management plans (DMPs), and educational resources for paying off credit card debt.

- AnnualCreditReport.com – Request your free credit reports from Equifax, Experian, and TransUnion to monitor your accounts, balances, and payment history.

- Experian – Ask Experian – Educational articles explaining minimum payments, credit utilization, interest charges, balance transfers, and strategies for improving your credit profile.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.