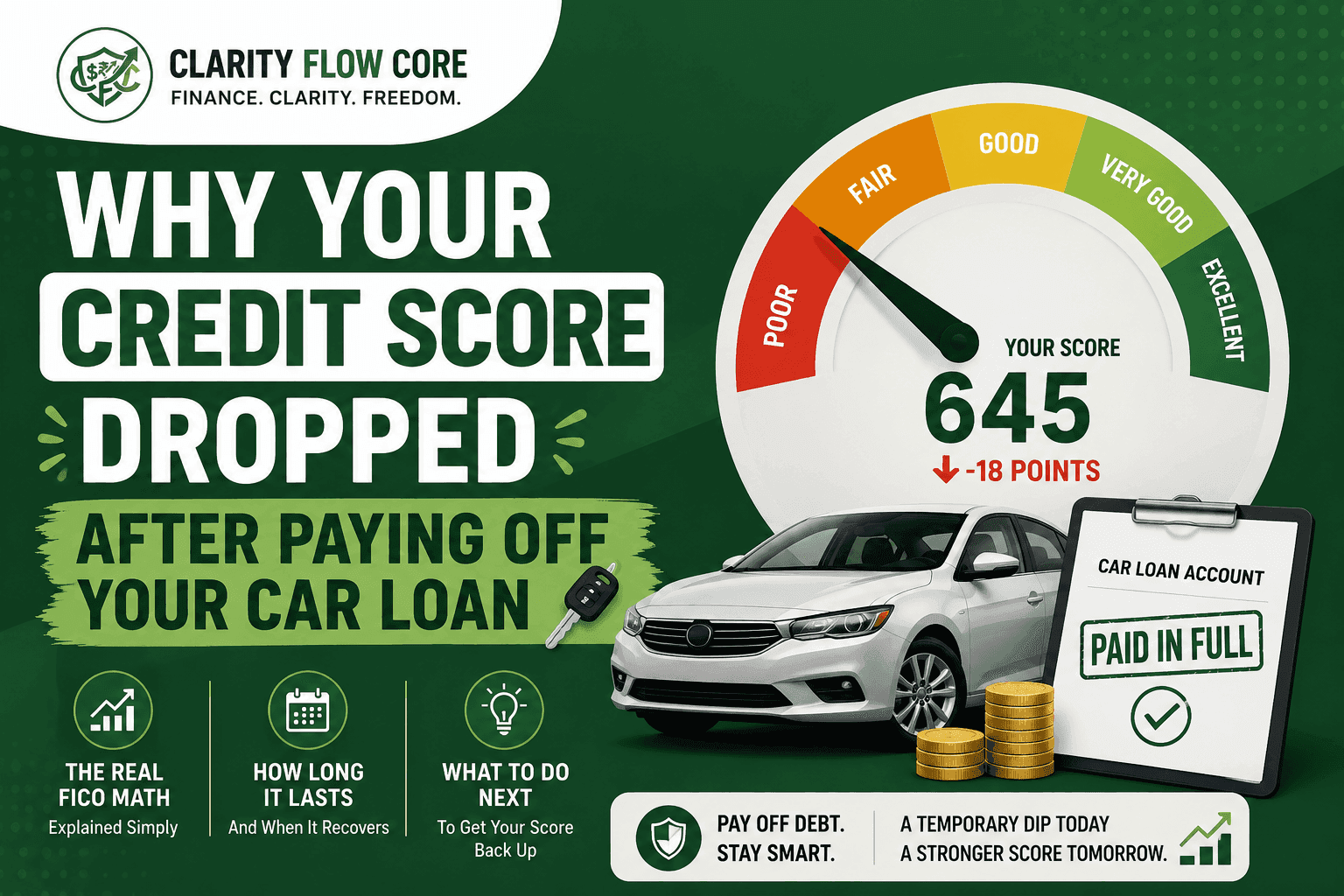

Why Your Credit Score Dropped After Paying Off Your Car Loan

You did everything right. You made every $400 monthly payment on time for five years. You sent the final check to the bank, you received the title in the mail, and you finally own your vehicle free and clear.

Then, a few weeks later, you open your banking app and get a bad surprise. Your FICO score just tanked by 15 points.

One of the most infuriating things in personal finance is seeing a credit score drop after paying off car loan debt. It feels like the credit bureaus are actively punishing you for being financially responsible and eliminating your debt.

The reality is that your credit score is not a measurement of your overall financial health or your net worth. It is simply an algorithm that measures how you interact with active debt. When you close an account, you alter the mathematical formula that makes up your profile.

If you are staring at a credit score drop after paying off car loan balances, here is exactly why the algorithm penalized you, how the math works, and what you need to do next to get your score moving back up.

⚡ Quick Answer

- A credit score can temporarily drop after paying off a car loan because the loan closes, which may affect your credit mix and how scoring models evaluate your active credit profile.

- The drop is usually temporary and does not mean paying off the loan was a financial mistake.

The Math Behind a Credit Score Drop After Paying Off Car Loan

To understand why your score fell, you have to look at the raw data. Your FICO credit score is made up of five specific components.

When you pay off a vehicle, two of these areas take an immediate hit.

| Credit Score Component | Percentage of FICO Score | Impact When Car is Paid Off |

| Payment History | 35% | Neutral (Positive history remains for up to 10 years) |

| Amounts Owed (Utilization) | 30% | Neutral (Installment loans don’t boost utilization) |

| Length of Credit History | 15% | Negative (Active profile shifts) |

| Credit Mix | 10% | Negative (You lose an installment loan) |

| New Credit | 10% | Neutral |

Let’s break down exactly why those two negative impacts happen and drive the credit score drop after paying off car loan accounts.

1. You Lost Your “Credit Mix” (10% of Your Score)

The credit bureaus want to see that you can handle several different types of debt simultaneously. This is known as your “Credit Mix.”

There are two primary categories of debt:

- Revolving Credit: Credit cards and lines of credit where the balance fluctuates.

- Installment Loans: Mortgages, student loans, and car loans where you pay a fixed amount over a set term.

If your auto loan was your only open installment loan, paying it off completely removes that category from your active profile. To the algorithm, your credit file suddenly looks less diverse. This loss of diversity is a primary driver of a credit score drop after paying off car loan obligations.

2. Your Active Credit Profile Shifted (15% of Your Score)

Lenders love long, proven track records. A portion of your score is calculated by averaging the age of all your accounts.

When you make your final car payment, that specific loan account is officially marked as “Closed.” While the paid-off loan remains on your credit report and continues contributing to your overall credit history for years, the closure can still affect how certain scoring models evaluate your active credit profile. This mathematical shift almost always results in a credit score drop after paying off car loan debt.

The Scenario: Why Utilization Didn’t Save You

Many people are shocked by a credit score drop after paying off car loan balances because they assume their “Credit Utilization” improved.

Credit utilization measures how much debt you owe compared to your total available credit limits. It makes up 30% of your score. (To master this critical metric, read our complete guide on What Is Credit Utilization and Why Does It Matter?).

However, credit utilization is almost exclusively tied to revolving credit (credit cards). Installment loans are calculated differently. If you pay off a $15,000 auto loan, it does not instantly free up $15,000 of “available credit” the way paying off a maxed-out credit card does.

Because paying off an installment loan provides zero boost to your revolving credit utilization, there is no positive mathematical bump to offset the loss of your credit mix.

How Long Does a Credit Score Drop After Paying Off Car Loan Last?

Breathe deep. The good news about a credit score drop after paying off car loan debt is that the penalty is fleeting.

Because the drop was triggered by a routine account closure—and not a negative event like a missed payment or a collection—your score will likely rebound.

Here is the typical recovery timeline:

- Days 1 – 30: The loan is reported as “Closed” to the bureaus. Score typically drops.

- Days 30 – 60: Score stabilizes. The algorithm adjusts to your new credit mix.

- Days 60 – 90+: Many consumers see their scores stabilize or recover over time, provided they continue making on-time payments and maintain healthy credit habits.

If you are checking different apps and seeing wildly different numbers during this recovery period, do not panic. Read up on FICO vs. VantageScore: Why Credit Scores Differ Between Apps to understand which algorithm your bank is actually looking at.

When This Backfires: The Panic Responses

Panicking over a credit score drop after paying off car loan balances often leads people to make terrible financial decisions. The algorithm wants you to stay in debt, but you must resist the urge to play its game.

Here is exactly when the recovery process backfires:

- Taking Out a New Loan: The absolute worst thing you can do is run out and finance a jet ski, a new car, or take out a personal loan just to “fix your credit mix.” You are intentionally losing money to interest charges just to buy FICO points. Never pay money to artificially inflate a credit score.

- Closing Old Credit Cards: Some people pay off their car and decide they want to be completely debt-free, so they immediately cancel their oldest credit cards. This is a massive mistake. Closing your oldest credit cards will destroy your credit utilization and further reduce your active account age, causing your score to plummet drastically.

- Disputing the Closed Account: A closed account in good standing is a positive mark on your report for up to a decade. Do not file a dispute with the credit bureaus trying to get the car loan removed from your history just because your score dipped.

Frequently Asked Questions (FAQs)

How many points can a credit score drop after paying off a car loan?

The impact varies by credit profile, but temporary changes are common, usually ranging between 10 to 30 points.

Is it bad to pay off a car loan early?

Not necessarily. Eliminating debt often improves overall financial health and saves you money on interest, even if your score fluctuates temporarily.

Will my score recover?

Many consumers see their scores stabilize or improve over time as they continue building positive credit history with their remaining open accounts.

Should I keep a loan open just for my credit score?

Generally, paying interest solely to maintain a credit score is not considered a sound financial strategy.

Does paying off a car loan remove it from my credit report?

No. Positive closed accounts can typically remain on your credit report for up to 10 years, serving as proof of your reliability to future lenders.

Why Paying Off the Loan Is Still a Win

A temporary score fluctuation does not change the fact that paying off a car loan eliminates interest costs and improves monthly cash flow.

Benefits of a paid-off car often include:

- Lower monthly obligations

- Improved debt-to-income (DTI) ratio

- Increased savings capacity

- Reduced financial stress

- More flexibility to invest or pay down other debts

Remember: a credit score is a tool, not the goal.

What You Should Actually Do Next

To recover from a credit score drop after paying off car loan accounts, your operational strategy should be incredibly boring. Focus on the basics of your remaining open accounts.

First, keep your credit card balances exceptionally low. Keep your utilization under 10%, and make every single payment on time.

Second, redirect your cash flow. If you were paying $400 a month for your car, route that exact amount into a High-Yield Savings Account or your basic emergency fund. If you understand How Sinking Funds Protect Your Emergency Savings, you know that setting this cash aside now will pay for your next car in cash, allowing you to bypass the dealership financing games entirely.

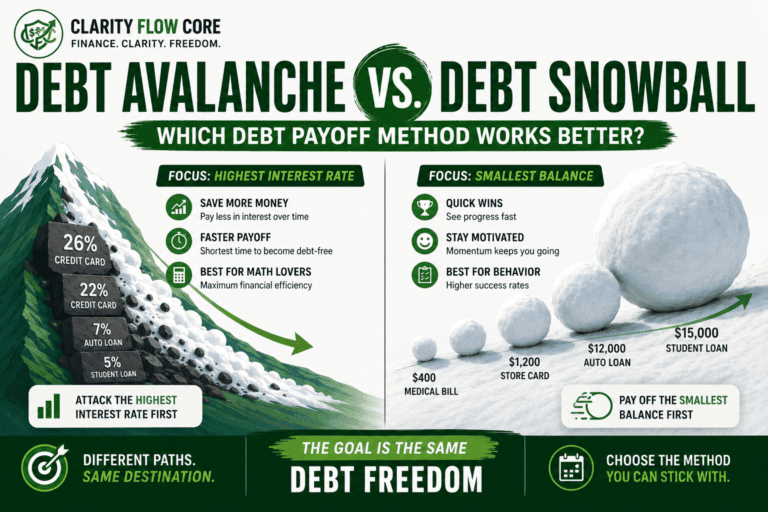

If you still have other consumer debt, use the newly freed-up $400 to accelerate your payoff timeline. (If you are unsure how to deploy the cash, our guide on Debt Avalanche vs. Debt Snowball: Which Debt Payoff Method Works Better? will give you the exact math).

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyFinally, if your credit score drop after paying off car loan debt exceeds 40 points, or if it hasn’t rebounded after three to four months, there may be a deeper administrative error on your file. To find out exactly what the bureaus are seeing, read our guide on How to Read and Fix Errors on Your Credit Report.

Do not let a temporary credit score drop after paying off car loan debt ruin your celebration. Getting rid of a depreciating asset’s monthly payment is a massive financial victory. Enjoy the extra cash flow in your monthly budget, ignore the FICO app for a few months, and let the algorithm work itself out.

References & Trusted Sources

To better understand how closed installment loans affect your credit algorithms, rely on these authorized consumer resources:

- myFICO Credit Education

- Experian Credit Education

- Equifax Credit Education Center

- Consumer Financial Protection Bureau (CFPB)

- AnnualCreditReport.com (The Authorized Federal Portal)

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.