CD Laddering Explained: A Simple Way to Manage Savings Rates

In a fluctuating economic environment, finding a safe place to grow your cash—while understanding How Much Should You Keep in Checking vs Savings?—and maintaining access to it can feel impossible. You want the high yields of long-term investments, but you do not want to lock up all your money for years behind a penalty wall.

For over a decade, it seemed like a joke to store your money in a traditional bank account. Big national banks were paying an insulting 0.01% APY on savings. If you kept $10,000 in the bank for a year, it barely generated enough interest to buy a single cup of coffee.

Then, the Federal Reserve aggressively shifted interest rates to battle inflation, and the entire banking landscape turned upside down. Suddenly, high-yield accounts and Certificates of Deposit (CDs) were yielding 4%, 5%, and sometimes even more.

When rates spike, the immediate impulse is to shift your entire cash reserve into a high-rate CD to guarantee that return. But that creates a massive operational problem. What if you put all your money away for a year, and your car’s transmission blows apart next month? What if you lock in a 4.5% rate today, but the bank offers 5.5% next week?

This exact conflict between yield and liquidity is why CD laddering is making a massive resurgence. CD laddering is an old-school banking approach that mathematically solves the problem. Here is the operational math behind the strategy, exactly how to build one, and the hidden banking traps that ruin it.

What Actually is a Certificate of Deposit (CD)?

Before you can master CD laddering, you have to understand the underlying asset. Banks and credit unions provide a highly specific type of savings vehicle called a Certificate of Deposit.

When you open a CD, you agree to leave a specific amount of money with the bank for a strict, predetermined amount of time, known as the “term.” In exchange for locking your money up, the bank guarantees you a set interest rate for the entire duration of that term.

The Math: If you open a 1-year CD with $10,000 at a 5.00% APY, you will make exactly $500 in interest. Your 5.00% is locked in by a legally binding contract. It does not matter if the stock market crashes tomorrow, or if the Federal Reserve slashes interest rates back to zero next month. The bank owes you that 5.00%.

The Catch (Early Withdrawal Penalties): The bank pays you a premium rate because they need to know exactly how long they can use your capital to fund other loans. If you break the contract and withdraw your money before the term is up, the bank will hit you with an Early Withdrawal Penalty (EWP).

These penalties are brutal. A standard penalty on a 1-year CD is often “90 days of simple interest.”

If your $10,000 CD earns $41.66 a month in interest, breaking the contract early will cost you roughly $125. If you break the contract in the very first month, the penalty will actually eat into your initial $10,000 principal. You will walk away with less money than you started with. (To prevent this, ensure your baseline cash reserves are fully funded first. Review Emergency Fund Basics: How Much Cash Should You Keep?).

The Danger of the Single CD Strategy

Let’s assume you have a fully funded $20,000 cash reserve. Putting 100% of it into a single 2-year CD is a massive liquidity risk.

If you lose your job or face a medical emergency in six months, your entire safety net is trapped behind that penalty wall. Furthermore, you are taking a massive interest rate risk. If inflation forces rates higher next year, your $20,000 is stuck earning the old, lower rate. You miss out on the new profits.

The Solution: How CD Laddering Works

CD laddering fixes the liquidity trap by breaking up your massive cash pile into smaller, equal pieces and spreading them out over multiple, staggered expiration dates.

Instead of making one massive, rigid wager, CD laddering creates a revolving door of cash.

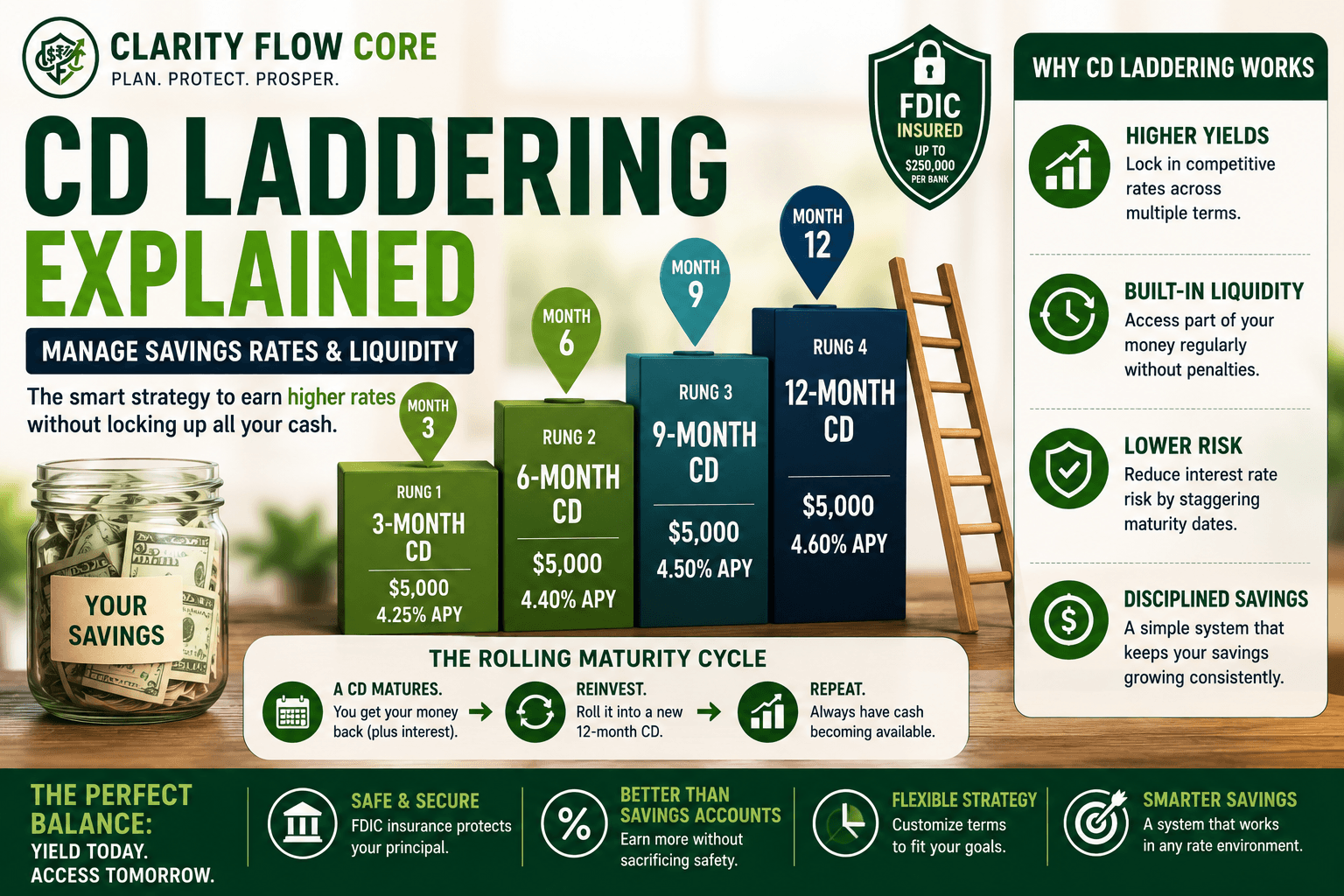

Let’s use that same $20,000 to build a highly liquid, short-term system. You divide the cash into four equal $5,000 chunks. You walk into the bank (or log into your online brokerage) and buy four distinct CDs on the exact same day.

The 1-Year CD Laddering Execution

| Rung | Term Length | Amount Invested | Hypothetical APY |

| CD 1 | 3-Month Term | $5,000 | 4.25% |

| CD 2 | 6-Month Term | $5,000 | 4.40% |

| CD 3 | 9-Month Term | $5,000 | 4.50% |

| CD 4 | 12-Month Term | $5,000 | 4.60% |

The Rolling Maturity Magic

Here is where the operational brilliance of CD laddering shines.

- Month 3: Your very first CD comes due. You now have $5,000 in liquid cash sitting in your checking account, plus the interest it earned. If you had an emergency, you take the cash and use it. Zero penalties. If you don’t need the money, you take that $5,000 and immediately buy a brand-new 12-month CD.

- Month 6: Your second CD comes due. You have access to cash once more. Again, if you do not need it to survive, you buy another 12-month CD.

By the end of the first year, you will have successfully transformed your portfolio. You now own four 12-month CDs, maximizing your interest rate. However, because you staggered the start dates, one of those 12-month CDs will mature and become liquid cash every three months.

You have successfully locked in the higher interest rates of long-term investments, but your CD laddering system guarantees you can access a chunk of your money four times a year without ever paying a bank fee.

The 5-Year Wealth Builder Ladder

If you have a larger cash pile that you absolutely know you will not need for daily emergencies (like a down payment fund for a house you plan to buy in a few years), you can stretch the CD laddering strategy to maximize yield.

Instead of months, you use years. You take $50,000 and divide it into five $10,000 rungs:

- $10,000 in a 1-Year CD

- $10,000 in a 2-Year CD

- $10,000 in a 3-Year CD

- $10,000 in a 4-Year CD

- $10,000 in a 5-Year CD

Long-term CDs almost always pay higher interest than short-term CDs. When year one ends, you take the maturing funds and buy a new 5-Year CD. After five years of executing this CD laddering cycle, you will own five separate 5-Year CDs, earning the absolute maximum premium rates, yet one of them will mature every single year.

Who Should Consider CD Laddering?

CD laddering works best for people who have specific savings goals but still want periodic access to their money.

You may benefit from a CD ladder if:

- You already have a fully funded emergency fund.

- You are saving for a home down payment in 1–5 years.

- You want predictable returns without stock market risk.

- You dislike seeing savings rates constantly change.

- You have cash sitting in a checking account earning almost nothing.

CD laddering may not be ideal if:

- You need immediate access to all of your cash at any given moment.

- You have high-interest credit card debt.

- You are investing for retirement decades away.

- You have not yet built a basic emergency fund.

For many households, the best approach is combining multiple savings tools. Start with an emergency fund, then consider a ladder for longer-term cash reserves.

Why CD Laddering Dominates a Fluctuating Market

Interest rates are inherently unpredictable. Wall Street analysts spend thousands of hours debating whether the Federal Reserve will hike rates, cut rates, or pause.

The beauty of CD laddering is that it completely removes the need to predict the future. It is a mathematically balanced hedge against market volatility.

- If rates drop next year: You win. You already locked in today’s high rates for the next 12 to 60 months on your longer-term rungs.

- If rates rise next year: You still win. Because of your staggered CD laddering setup, one of your short-term rungs will expire soon. You simply take that mature cash and reinvest it at the new, higher market rate.

When This Backfires: The Operational Traps

A CD laddering system is incredibly safe, but banks are businesses designed to make a profit. If you “set it and forget it” without understanding the rules of engagement, this strategy will backfire and trap your money.

1. The Auto-Renewal Trap

This is the single biggest danger in CD laddering. When a CD matures, the bank does not automatically wire the money back to your checking account. They place the funds into a “Grace Period” (usually 7 to 10 days).

If you do not log in and explicitly tell the bank to transfer the funds or buy a specific new CD within that 10-day window, the bank will automatically renew your CD for the exact same term length.

Here is the catch: they will renew it at their current standard rate, which is often a terrible, rock-bottom APY. If you ignore the maturity date email, your high-yield 5% CD might auto-renew into a 0.5% CD, and your money is locked up for another year. You must track your maturity dates on a calendar.

2. The Inflation Reality Check

While CD laddering protects your cash from stock market crashes, it does not always protect you from inflation. If you lock your money into a 3% CD, but the cost of groceries and housing goes up by 5% that year, your money is mathematically losing purchasing power. CDs are for wealth preservation and cash flow management, not massive wealth creation. (If you want to outpace inflation long-term, read our guide on Index Funds vs. Mutual Funds: What Beginners Should Know).

3. The Callable CD Trap

If you buy CDs through a brokerage account (like Vanguard or Schwab) instead of a direct retail bank, you might accidentally buy a “Callable CD.” These offer slightly higher rates, but the bank retains the right to “call” (cancel) the CD early if interest rates drop. They give you your principal and interest back, but they strip away your ability to ride out the high rate. Always ensure you are buying “Non-Callable” CDs for your ladder.

CD Laddering vs. High-Yield Savings Accounts (HYSA)

A common question is: Why not just put everything in a High-Yield Savings Account?

HYSAs are fantastic vehicles, but they carry a distinct flaw: variable rates. Your HYSA rate goes down on Wednesday if the Federal Reserve cuts rates on Tuesday. There is zero rate protection.

The ultimate operational strategy uses both. Learn the nuances by reading How to Choose Your First High-Yield Savings Account and comparing the data in HYSA vs. Money Market Account: What’s the Difference?.

- Keep your immediate 30-day to 60-day survival fund in a fully liquid HYSA.

- Keep the remaining balance of your 6-month emergency reserve inside a CD laddering system. This ensures that a massive portion of your safety net is protected from sudden rate cuts, while the HYSA provides immediate liquidity for a 2:00 AM plumbing emergency.

Your Action Plan: How to Build Your Ladder Today

You do not need to wear a suit and drive to a physical bank branch to execute this. In fact, traditional brick-and-mortar banks usually offer the worst CD rates on the market.

To build a profitable CD laddering system, look to online-only banks like Ally, Marcus by Goldman Sachs, Discover Bank, or Capital One 360. Because they do not pay for physical real estate, they pass the profits back to you via higher APYs.

Start small. Learn How to Automate Savings Using Split Direct Deposit to funnel cash seamlessly into your new accounts. You do not need $20,000 to begin. Many online banks have completely eliminated minimum deposit requirements for their certificates. You could build a functional CD laddering system with just $400, placing $100 on each rung.

The mathematical principles are exactly the same. Map out your timeline, log into your banking app, lock in your rates, and let the rolling maturities guarantee your liquidity.

Frequently Asked Questions (FAQs)

Is CD laddering safe?

Yes. CDs from FDIC-insured banks are protected up to applicable limits (typically $250,000 per depositor, per institution).

How much money do I need to start a CD ladder?

Many banks allow you to start with a few hundred dollars. Some online banks have completely eliminated minimum deposit requirements.

What happens when a CD matures?

You can withdraw the funds to your checking account, spend them, or reinvest them into a new CD at the current market rate.

Can I lose money with a CD?

Generally not if held to maturity, as your principal and interest are guaranteed. However, inflation may reduce your overall purchasing power, and early withdrawal penalties can eat into your principal.

Is CD laddering better than a savings account?

Not necessarily. Many people use both together. Savings accounts offer immediate liquidity, while CD ladders lock in guaranteed, often higher interest rates for money you won’t need right away.

References & Trusted Sources

For further research on current banking regulations, deposit insurance, and interest rate trends, consult these official resources:

- FDIC – Certificates of Deposit (CDs) Tips

- Consumer Financial Protection Bureau (CFPB) – Savings Accounts and CDs

- Federal Reserve – Interest Rate Policy Overview

- NCUA – Share Certificates at Credit Unions

The Bottom Line

CD laddering isn’t just a savings account; it is a strategic cash flow system. By taking an hour to spread your cash across staggered maturities, you successfully lock in premium interest rates without trapping yourself behind early withdrawal penalties. Check the rates at your preferred online bank today, buy your first three rungs, and put your money to work securely.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

3 Comments

Comments are closed.