How to Budget as a Freelancer When Income Changes Every Month

When your income fluctuates wildly from month to month, standard budgeting advice falls apart. You cannot rigidly save 20% of your income if you don’t know exactly what 100% of your income will be. If you are waiting on a client to finally approve a heavy video project so you can send the final invoice, but your rent and software subscriptions are due tomorrow, that cash flow gap creates massive anxiety. (If you are just getting started in this specific space, read How to Start a Video Editing Side Hustle (Even as a Beginner)).

If you want to learn how to budget as a freelancer, you have to stop budgeting based on what you hope to make, and start budgeting based on your Baseline.

⚡ Quick Answer

To budget as a freelancer when income changes every month, calculate your minimum monthly expenses (your baseline), pay yourself a consistent salary from your business account, and build a cash buffer that covers at least three to six months of expenses. This separates your personal finances from your business income and smooths out irregular client payments.

The Reality of the “Slow Month”

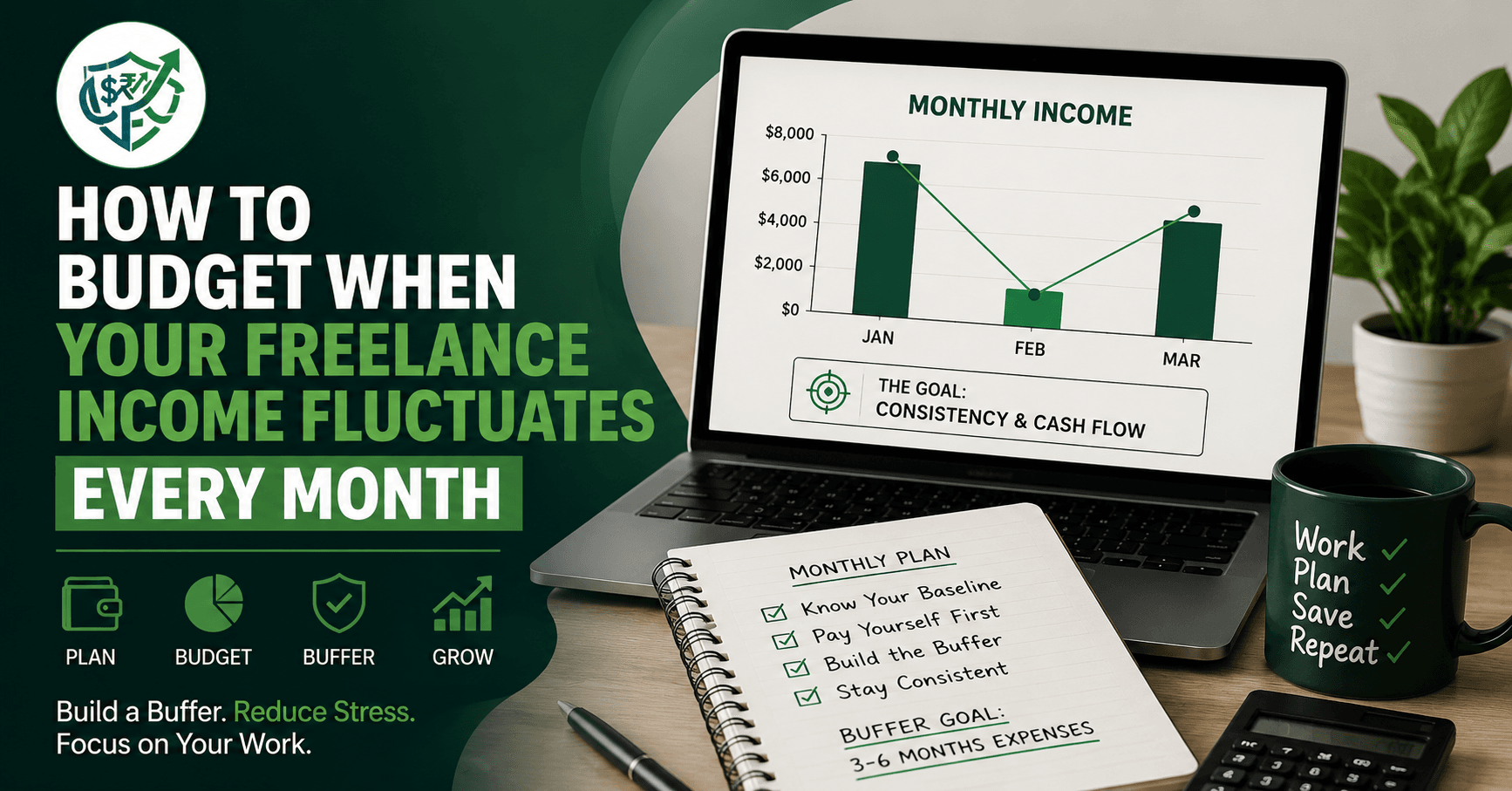

Let’s look at a realistic first quarter for a freelance video editor. It rarely looks like a steady, predictable salary.

- January: $7,000 (Landed a big corporate gig)

- February: $2,400 (Client delayed the next project; only routine retainer work)

- March: $5,500 (Corporate gig wrapped; picked up two smaller projects)

Total Q1 Income: $14,900.

Average Monthly Income: $4,966.

On paper, making almost $5,000 a month is a healthy freelance business. But in reality, if this editor doesn’t have a buffer system, February is an absolute nightmare. They will likely be scrambling to pay basic bills, taking on bad clients out of desperation, or putting expenses on a credit card just to survive. The quarterly income is fine, but the monthly cash flow is broken.

Common Mistakes When You Budget as a Freelancer

Before building a financial system that actually works, you have to stop doing the things that guarantee stress. The “feast or famine” cycle is usually caused by these four operational blunders:

- Relying on future invoices: Counting money that a client “promises” to pay next week as money you have today is a recipe for disaster. Net-30 payment terms often turn into Net-45 or Net-60. Until the cash clears your bank, it does not exist.

- Mixing business and personal money: Buying groceries on the exact same debit card you use to pay for your Adobe Creative Cloud subscription. This makes it mathematically impossible to know if your business is actually profitable.

- Forgetting the IRS: Seeing a $3,000 deposit and thinking you have $3,000 to spend. Freelancers are on the hook for both standard income tax and the self-employment tax.

- Upgrading lifestyle too fast: Having one $8,000 month and immediately financing a new car or moving into a more expensive apartment, assuming that $8k is your permanent new normal.

Step 1: Calculate Your Bare-Bones Baseline

Your baseline is the absolute minimum amount of money you need to keep the lights on, your internet running, and your business operational. It strips away dining out, new gear purchases, and vacations. It is your survival number.

To find it, you need to pull your last three months of bank statements. Highlight only the non-negotiable expenses.

Real Example: Freelancer Baseline Budget

| Expense | Monthly Cost |

| Rent | $1,200 |

| Utilities | $150 |

| Groceries | $400 |

| Transportation | $200 |

| Insurance | $250 |

| Phone & Internet | $100 |

| Total Baseline | $2,300 |

If your personal baseline is $2,300, that is the only number you should care about when planning your month. You do not need to make $5,000 a month to survive; you need to make $2,300. Everything above that is fuel for your business growth and your buffer.

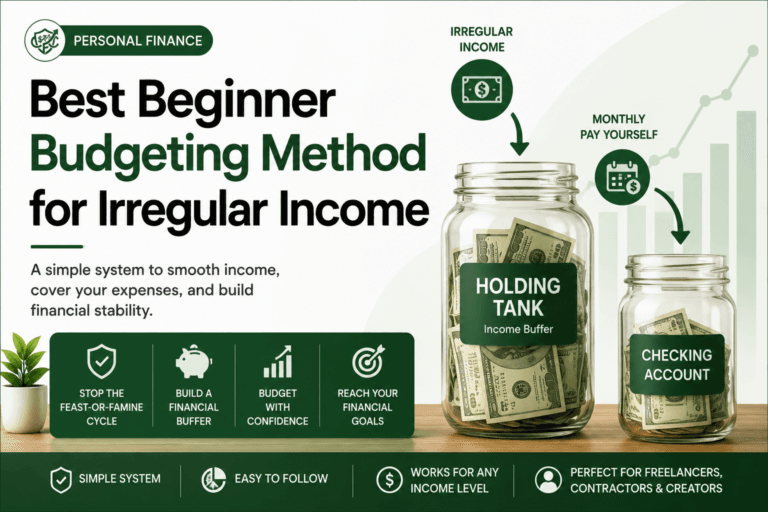

Step 2: Build the One-Month Buffer

Instead of paying bills with the money you earned this month, your goal is to pay this month’s bills with last month’s money. You achieve this by strictly separating your accounts.

| Account Type | What Goes In | What It Pays For | Target Balance |

| Business Checking | All client payments and platform payouts. | Software subscriptions, hosting, contractors. | 1.5x monthly business expenses |

| Personal Checking | A fixed “salary” you transfer to yourself from Business Checking on the 1st of the month. | Rent, groceries, utilities, personal insurance. | 1x monthly personal baseline |

| The Buffer (Savings) | Any profit left over after paying your salary, taxes, and business expenses. | Nothing. It sits here to cover slow months (like February). | 3 to 6 months of your baseline |

When you land a massive contract, your personal “salary” transfer to your checking account remains exactly the same. The extra cash stays in the business to fund your buffer and pay your quarterly estimated taxes.

To find the best place to park your buffer cash so it actually earns interest, review our breakdown on HYSA vs. Money Market Account: What’s the Difference?

How Much Should Freelancers Save for Taxes?

When you operate as an employee, taxes are invisible. When you are a freelancer, taxes are your biggest line-item expense.

Freelancers are responsible for federal income tax, state income tax, and the 15.3% Self-Employment Tax (which covers Medicare and Social Security). Because no one is withholding this for you, you must build the holdback into your operational system.

A universal benchmark for freelancers is to save 25% to 30% of every single dollar that enters your business checking account.

Do not wait until the end of the month to move this money. The second an invoice clears, transfer 30% into a separate tax savings account. (You can streamline this exact process by reading How to Automate Savings Using Split Direct Deposit). By ruthlessly holding back 30%, you guarantee that you will always have the cash on hand to make your quarterly estimated tax payments to the IRS. For a deep dive into the specific mechanics of 1099 filings and self-employment taxes, read our complete guide on 1099 Taxes Explained for Freelancers and Side Hustlers and explore industry-specific write-offs in the Freelance Video Editor Tax Guide: Deductions & Write-Offs.

What If You Have a Very Bad Month?

This is the scenario that keeps freelancers awake at 3:00 AM. What happens when a major client ghosts you, your pipeline dries up, and you only bring in $800 for the entire month?

If you have built your system correctly, a bad month is an annoyance, not a catastrophe.

- Deploy the Buffer First: This is exactly what the buffer is for. Do not panic. Transfer your standard $2,300 salary from your business savings buffer to your personal checking account. Your personal life remains completely unaffected by the business slowdown.

- Reduce Discretionary Spending: While your baseline covers your survival, a bad month means you pause all unnecessary business spending. Cancel any software subscriptions you aren’t actively using this month and pause any paid advertising.

- Do Not Use Credit Cards: Do not finance your lifestyle on a credit card charging 24% interest just to pretend you are having a good month. Rely on your cash reserves. (If you are unsure how big that reserve should ultimately be, consult Emergency Fund Basics: How Much Cash Should You Keep?).

- Focus 100% on Client Acquisition: If you have zero client work to fulfill, you now have 40 free hours a week to prospect. Send cold emails, edit spec work for potential clients, and aggressively rebuild your pipeline.

What Happens After the Buffer Is Built?

Eventually, your business buffer account will hit that 3 to 6-month goal. When your business savings are fully funded, you no longer need to hoard cash. That excess revenue is finally ready to be put to work.

Once the buffer is full, your extra revenue should be routed to:

- Equipment Upgrades: Buying that new ultra-wide monitor, more RAM, or a better camera setup in cash, rather than financing it.

- Retirement Investing: Funding a Solo 401(k) or a Roth IRA to build long-term wealth outside of your freelance business.

- Healthcare Planning: Fully funding an HSA (Health Savings Account) to cover high deductibles and routine medical expenses.

When This Strategy Backfires

This buffer system is powerful, but it has two major traps. If you lack discipline, you will break the mechanics of the budget.

Trap 1: Starving Your Growth

If you become too obsessed with hoarding cash in your buffer, you might hesitate to invest in things that actually make your life easier. Refusing to pay $20 a month for an audio-syncing plugin that saves you three hours of editing a week is bad business. Your time is your most valuable asset. If a tool clearly generates a positive return on investment, buy it.

Trap 2: The “Slush Fund” Mentality

If you are constantly dipping into the business buffer to pay for personal weekend trips, spontaneous concert tickets, or emergency vet bills, the system collapses. The buffer is strictly there to protect your business from fluctuating client payments. It is not a slush fund to finance personal overspending. Keep your business money and personal money entirely separated.

Frequently Asked Questions (FAQs)

How many months of expenses should freelancers save? Most freelancers should aim for a baseline buffer of 3 to 6 months of combined personal and business expenses to safely absorb late client payments and dry spells.

Should freelancers pay themselves a salary? Yes. The most successful freelancers pay themselves a consistent, fixed monthly amount from their business checking account rather than spending wildly directly from client payments.

What percentage of freelance income should go to taxes? A common and safe guideline is to hold back 25% to 30% of your gross business income to cover federal, state, and self-employment taxes.

Can freelancers use the 50/30/20 budget? Yes, but it is often much more effective to implement the 50/30/20 rule on your personal salary only after creating a stable income buffer inside your business accounts.

What is the biggest budgeting mistake freelancers make? The most common mistake is spending money from large invoices immediately before accounting for taxes, future operating expenses, and inevitable slow months.

The Bottom Line

The biggest shift when you budget as a freelancer is realizing that your income is not your paycheck. Your income is the average of what your business produces over time. By building a buffer, paying yourself consistently, and establishing a firewall between your business and personal finances, you remove the emotional roller coaster from freelancing.

The goal is not to predict every single month perfectly. The goal is to build a mathematical system that keeps working even when clients pay late, projects disappear, or business slows down temporarily. Once that system is in place, freelancing becomes significantly less stressful and far more sustainable.

References & Trusted Sources

To ensure you are properly managing your freelance taxes, structuring your business accounts, and avoiding severe IRS penalties, consult these official small business resources:

- Consumer Financial Protection Bureau (CFPB) – Small Business Resources

- IRS Self-Employment Tax Center

- U.S. Small Business Administration (SBA) – Cash Flow Management

- SCORE – Small Business Budgeting Templates

- Federal Reserve – Small Business Resources

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.