Roth IRA for Beginners: How It Works and Why People Use One

I can still remember the first time a financially savvy mentor told me I needed to “open a Roth IRA immediately.” I nodded politely, but internally, my mind went blank. I honestly thought “Roth” was the name of a specific financial advisor at a local bank who was going to handle my money.

When you first decide to take control of your financial future, navigating a Roth IRA for beginners feels like reading a foreign language. The Wall Street jargon is intentionally intimidating. It feels like everyone else was handed a secret instruction manual that you missed out on.

Here is the operational truth: investing does not require a finance degree, you do not need to watch stock tickers scroll across your TV screen, and you do not need to be rich to start. If you are looking to build long-term, generational wealth, the single most powerful tool available to the American middle class is the Roth Individual Retirement Account.

This is the definitive, operational guide to the Roth IRA for beginners. We are going to strip away the complex jargon, run the hard mathematical comparisons, explain exactly how this account legally shields your money from the IRS, and give you the exact step-by-step playbook to open one today.

The Basket Metaphor: Explaining a Roth IRA for Beginners

The single biggest mistake anyone researching a Roth IRA for beginners makes is assuming the account itself is an investment. Beginners will frequently ask, “I put $1,000 into a Roth IRA, what is my interest rate going to be?”

A Roth IRA is not an investment. It is simply a special type of account.

Think of a Roth IRA like a woven shopping basket. When you walk into a grocery store, the basket itself does not feed you; it is just the container that holds your food. A Roth IRA is simply a “tax-advantaged basket.” Once you open the account (get the basket), you still have to walk down the aisles and pick out the actual investments (like index funds, stocks, or bonds) to put inside of it.

What makes this particular basket so special? It acts as an impenetrable, legal shield against the Internal Revenue Service.

Why Starting Early Matters More Than Investing More

One of the biggest misconceptions about retirement investing is that you need a high income before opening a Roth IRA. In reality, the most valuable asset in your investment portfolio is not your salary—it’s time.

Imagine two investors. Sarah starts contributing $250 per month at age 25 and continues until she turns 35, investing for just 10 years before stopping completely. James waits until age 35 to begin but contributes the same $250 per month every month until he retires at age 65.

Although James invests for three decades, Sarah’s money has an additional ten years to compound. Depending on investment returns, she may finish with a retirement balance that rivals—or even exceeds—James’s, despite contributing far less money overall.

This is the power of compound growth. Your investments don’t simply earn returns; those returns begin generating returns of their own year after year. Over several decades, this compounding effect becomes far more important than trying to perfectly time the market or waiting until you can afford larger contributions.

The lesson for beginners is simple: don’t wait until you feel financially “ready.” Starting with even modest, consistent contributions today often produces better long-term results than delaying your investments while trying to save larger amounts in the future.

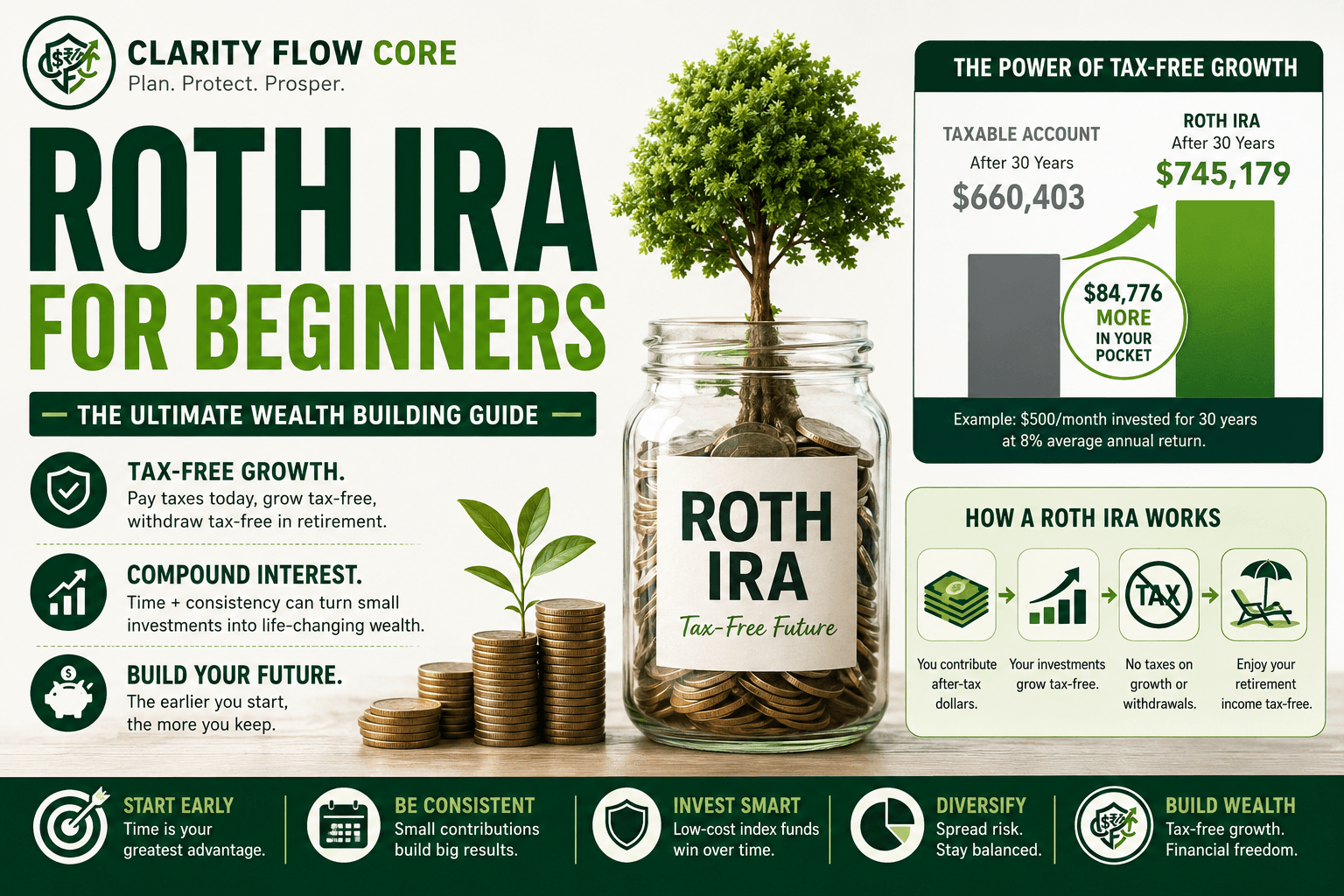

The Math: Why a Roth IRA for Beginners is So Powerful

To truly grasp the leverage of a Roth IRA for beginners, you have to look at the math of how standard investing works versus tax-advantaged investing.

When you open a normal, taxable brokerage account and invest your money, the government taxes your profits. If you buy a stock for $10,000 and it grows to $100,000, you have a massive $90,000 profit. But when you sell that stock to use the money in retirement, the government steps in and demands “Capital Gains” taxes on that $90,000. You could easily lose 15% to 20% of your wealth to the IRS in a single day.

A Roth IRA completely reverses the math.

When you put money into a Roth IRA, you are using “after-tax” money (meaning the income taxes were already taken out of your paycheck by your employer). Because you already paid taxes on the seed, the government legally cannot tax the harvest.

Let’s look at the operational math of investing $500 a month for 30 years at an 8% average annual return:

| Metric | Standard Taxable Brokerage | The Roth IRA |

| Total Money Invested | $180,000 | $180,000 |

| Total Future Value | $745,179 | $745,179 |

| Total Profit (Capital Gains) | $565,179 | $565,179 |

| Taxes Owed at Retirement | -$84,776 (Assuming 15% rate) | $0 |

| Your Actual Take-Home | $660,403 | $745,179 |

For anyone executing a Roth IRA for beginners strategy, this tax loophole is mathematically worth tens of thousands of dollars. You get to withdraw every single penny of that compound interest completely tax-free. No audits. No capital gains. It is all yours. (Want to ensure you are maximizing your current tax strategies today as well? Read our guide on Standard Deduction vs. Itemizing: Which Option Saves More?).

Traditional vs. Roth: What is the Difference?

A common point of confusion in any Roth IRA for beginners guide is the difference between a “Traditional” IRA and a “Roth” IRA.

- Traditional IRA: You get a tax break today. The money you contribute lowers your taxable income this year, but when you retire, you have to pay income taxes on every dollar you withdraw (both the contributions and the massive growth).

- Roth IRA: You get no tax break today. However, your money grows tax-free, and your qualified withdrawals in retirement are 100% tax-free.

For many younger workers and those currently in lower tax brackets, a Roth IRA can be an attractive option because qualified withdrawals are tax-free.

Who Is a Roth IRA Best For?

A Roth IRA is often a good fit for:

- Young professionals early in their careers.

- Workers expecting higher future income.

- Investors seeking tax-free retirement withdrawals.

- Individuals who want flexibility to access contributions if necessary.

A Roth IRA may be less attractive for:

- High earners who exceed contribution limits.

- Investors seeking immediate tax deductions.

- Individuals nearing retirement who expect lower future tax rates.

The Rules: Contribution and Income Limits

Because this tax advantage is so massive, the IRS strictly limits how much money you can put into the basket each year. Navigating a Roth IRA for beginners means understanding these IRS rules so you do not accidentally trigger a financial penalty.

The Contribution Limits

You cannot dump your entire salary into this account. Roth IRA contribution limits are updated periodically by the IRS. Always verify the current annual contribution limits before funding your account. (The IRS generally provides a standard maximum for individuals under 50, and a higher “catch-up” limit for those 50 and older).

The Income Limits (MAGI)

The Roth IRA was designed specifically to help the middle class. If you are a high-earning executive, the IRS restricts your ability to use it directly.

Roth IRA eligibility phases out at higher income levels. Check the latest IRS income limits before making contributions, as these thresholds are adjusted periodically for inflation depending on your filing status (Single vs. Married Filing Jointly).

(Note: If you make more than the phase-out limit, you are legally barred from contributing directly. However, wealthy investors bypass this using a highly complex loophole called a “Backdoor Roth IRA”).

Execution: The 3-Step Setup Guide

Reading the theory of a Roth IRA for beginners is one thing; executing it is another. You do not need to drive to a physical bank or wear a suit to open an account. Here is the exact order of operations to get your money working for you today from your laptop.

Step 1: Choose a Brokerage

You need an institution to hold your basket. The top three most trusted, low-cost brokerages in the US are Fidelity, Vanguard, and Charles Schwab. All three are fantastic, but Fidelity and Schwab generally have the most user-friendly digital apps for absolute beginners. Go to their website, click “Open an Account,” and select “Roth IRA.”

Step 2: Fund the Account

Once the account is open, you need to connect your primary checking account and transfer the money over.

The most critical operational step of a Roth IRA for beginners is funding it consistently. You do not have to hit the annual maximum limit all at once! If you are following The 50/30/20 Budget Rule Explained Simply, simply set up an automated transfer of $100 or $140 a week. Consistency is much more important than a massive initial lump sum.

Step 3: Buy the Investments (Do Not Miss This)

This is where millions of people fail. When you transfer $1,000 from your bank into your new Roth IRA, that money sits in a “Settlement Fund.” A settlement fund is basically a digital waiting room. If you leave it there, it is not invested in the stock market; it is just gathering dust. You must physically click “Trade” and buy an investment.

A core lesson in this Roth IRA for beginners playbook is what to actually buy. The smartest, safest route for someone who doesn’t want to research individual companies is an index fund. (If you aren’t sure how these work, read Index Funds vs. Mutual Funds: What Beginners Should Know).

- The S&P 500 Index Fund: This automatically buys you a tiny slice of the 500 largest, most successful companies in America. You aren’t betting on one horse; you are betting on the entire US economy.

- The Target Date Fund: This is the ultimate “set it and forget it” option. You pick the year you want to retire (e.g., “Target Date 2060”), and a computer algorithm automatically balances your investments for you, making them highly aggressive while you are young, and safer as you approach retirement.

When a Roth IRA for Beginners Backfires

Retirement accounts are highly regulated. If you treat this account like a Las Vegas casino or a checking account, you will get burned. Here is exactly when these accounts backfire on retail investors:

1. The Settlement Fund Trap

As mentioned above, the most devastating trap in a Roth IRA for beginners strategy is the uninvested cash error. I have spoken to people who dutifully contributed $500 a month for five years, only to log in and realize their account balance was exactly what they put in. They never actually bought a stock or a fund. They lost out on five years of the greatest bull market in history because they left the cash in the settlement fund.

2. The Over-Contribution Penalty

If you accidentally automate your savings too well and exceed the annual limit, the IRS will penalize you. They charge a strict 6% excise tax penalty on the excess amount for every single year that the extra money remains in the account. You must track your total deposits carefully.

3. Day Trading Inside the Account

A Roth IRA is designed for long-term, buy-and-hold investing. If you use your Roth IRA to day-trade volatile cryptocurrency, meme stocks, or highly leveraged options, and you lose $5,000, that money is gone forever. You cannot claim that $5,000 as a “capital loss” on your taxes to offset your income, and you cannot magically put an extra $5,000 back into the account to replace it because of the annual contribution limits. Never gamble inside a tax-advantaged retirement account.

The Secret Backup Plan: The Withdrawal Rule

A major reason people are terrified to invest is the fear of locking their money in a federal vault until they are 59 ½ years old. What if life goes wrong, you lose your job, and you desperately need that cash?

The psychological safety net of a Roth IRA for beginners is the principal withdrawal rule.

You can withdraw your contributions at any time, for any reason, without taxes or penalties. If you contribute $5,000 this year, and the stock market grows that money to $6,000, the $1,000 of profit is strictly locked away for retirement. But that initial $5,000 seed you planted? You can pull it out tomorrow if you absolutely have to.

While you should always rely on a dedicated cash buffer for immediate disasters—read up on Emergency Fund Basics: How Much Cash Should You Keep?—knowing that your original contributions are legally accessible provides incredible peace of mind for nervous investors.

Frequently Asked Questions (FAQs)

Can I lose money in a Roth IRA?

Yes. The account itself does not guarantee returns. Performance depends entirely on the investments you choose to buy inside the account.

Can I have both a Roth IRA and a 401(k)?

Yes. Many investors contribute to both to maximize their tax-advantaged retirement savings.

How much money do I need to start?

Many modern brokerages allow you to begin with small contributions, sometimes as little as $1 to open the account.

What happens if I exceed the contribution limit?

You may owe a 6% excise tax penalty every year the excess amount remains in the account unless the excess contribution is corrected before the tax deadline.

Is a Roth IRA better than a savings account?

They serve completely different purposes. Savings accounts are designed to protect short-term cash, while Roth IRAs are intended for long-term, tax-free investing and wealth building.

References & Trusted Sources

A Roth IRA is governed by IRS contribution rules, withdrawal regulations, and income eligibility requirements. Before opening or funding an account, it’s a good idea to review the latest guidance from these trusted government agencies and investor education organizations.

- Internal Revenue Service (IRS) – Learn how Roth IRAs work, including eligibility requirements, contribution rules, withdrawal guidelines, and tax treatment.

- IRS Publication 590-A – Official guidance covering IRA contributions, annual limits, income eligibility, and contribution rules.

- IRS Publication 590-B – Understand qualified withdrawals, Roth IRA distributions, conversions, and inherited IRA rules.

- Investor.gov (U.S. Securities and Exchange Commission) – Educational resources covering compound interest, diversification, long-term investing, and retirement planning fundamentals.

- U.S. Securities and Exchange Commission (SEC) – Saving and Investing – Learn the basics of investing, managing investment risk, and building wealth over time.

- FINRA Investor Education Foundation – Practical guidance on choosing investments, understanding risk, and becoming a more informed long-term investor.

The Bottom Line

Opening a retirement account feels like a massive adult milestone, but the mechanics are remarkably simple. A Roth IRA for beginners doesn’t require a Wall Street degree or thousands of dollars in startup capital.

Choose a broker, open the “basket,” set up an automatic weekly transfer, buy an index fund, and close the app. The most important variable in investing is not how much money you make; it is how much time you give your money to compound. Ensure your daily finances are structured properly by understanding How Much Should You Keep in Checking vs Savings? and leveraging an HYSA vs Money Market Account, then stop leaving tax-free money on the table and start building your financial fortress today.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.