Standard Deduction vs. Itemizing: Which Option Saves More?

For the first five years of my professional career, I kept a beat-up shoebox tucked in the back of my closet. Throughout the year, I obsessively tossed receipts into that box—a $15 receipt for office pens, a slip for donating old clothes to Goodwill, a receipt for a $40 medical co-pay. I was absolutely certain that when tax season arrived, I would “itemize” my deductions, uncover secret tax loopholes, and get massive revenge on the IRS.

When April finally arrived, I spent three agonizing hours doing the arithmetic. The total sum of every single receipt I had meticulously saved for 12 months was roughly $4,200.

Then, I looked at the IRS Standard Deduction for that year. It was over $12,000.

I had spent hours of my life counting pennies and organizing crumpled paper, only to realize the government was offering me a massive, flat deduction entirely for free. I tossed the shoebox into the recycling bin and never looked back.

You are not the only one completely confused by the standard deduction vs itemizing debate. The U.S. tax code can feel complex, yet the math behind this specific choice is actually brutally simple. Here is the operational framework to determine exactly which choice will leave more money in your bank account this April.

The Foundation: What Actually is a Tax Deduction?

Before we declare a winner in the standard deduction vs itemizing showdown, we must clear up a massive societal misunderstanding regarding write-offs.

A tax deduction does not mean the government hands you cash. If you buy a $1,000 laptop for work and “deduct” it, the government does not send you a check for $1,000.

A deduction simply lowers your Taxable Income. If you make $60,000 this year and claim a $10,000 deduction, the IRS pretends you only earned $50,000. They only charge you taxes on that smaller amount. During tax season, your only goal is to legally reduce your taxable income as low as legally possible.

When navigating standard deduction vs itemizing, there are two distinct operational paths to achieve that lower number. You are legally barred from doing both on the same form. You must choose one.

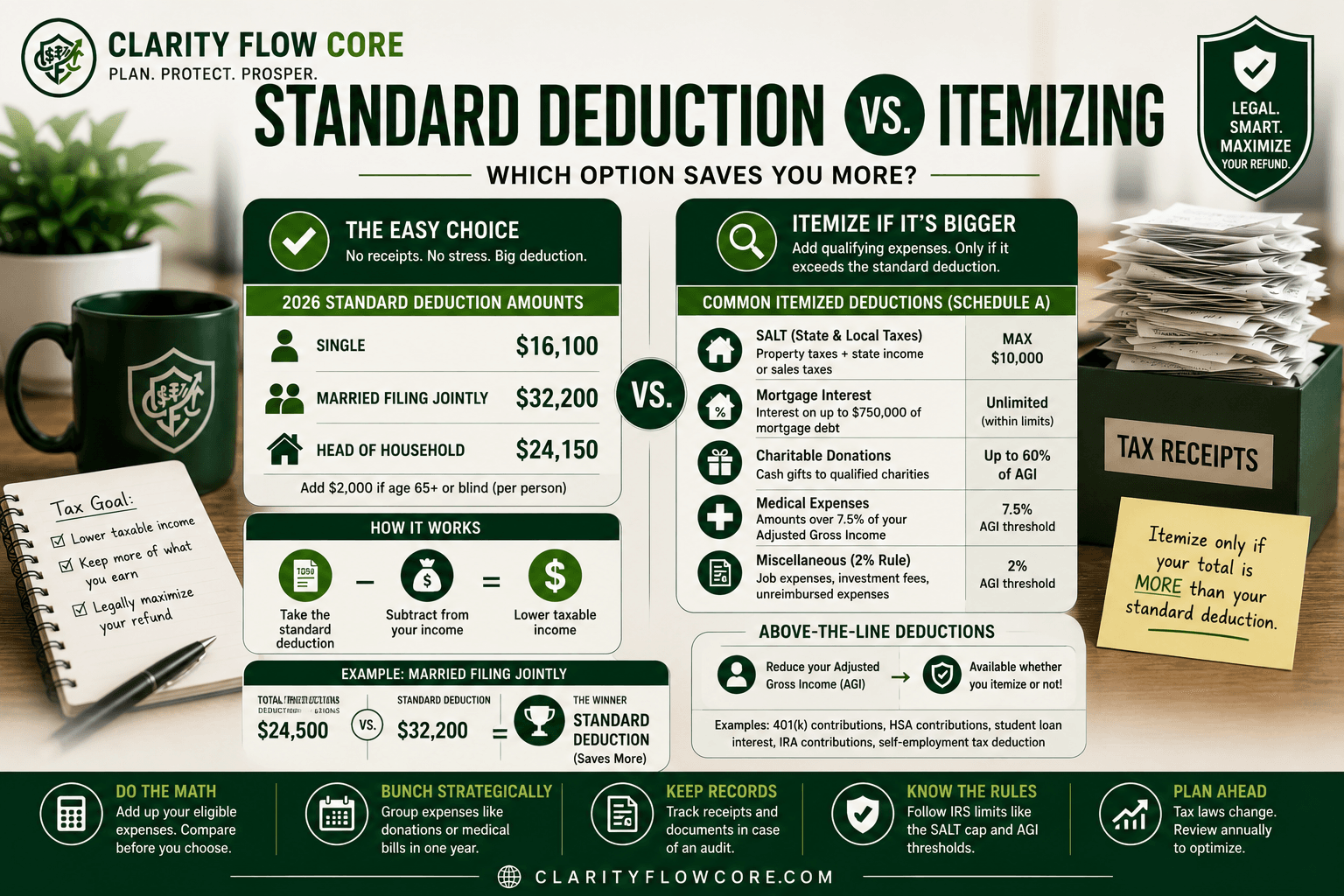

Path A: The Standard Deduction

The Standard Deduction is the ultimate “easy button” provided by the federal government. You are allowed to subtract a massive, flat amount of money from your income without answering any questions. You generally do not need receipts to claim the standard deduction itself. However, you should still retain records related to income, tax credits, business expenses, and other items reported on your tax return. You simply check a box on your tax return.

Due to aggressive inflation adjustments, the standard deduction has reached record-breaking highs. Standard deduction amounts are adjusted periodically for inflation. Verify current figures on IRS.gov before filing.

2025/2026 Standard Deduction Baselines:

| Filing Status | Base Deduction Amount |

| Single / Married Filing Separately | $15,750 |

| Married Filing Jointly | $31,500 |

| Head of Household | $23,625 |

(Note: If you are over age 65 or legally blind, the IRS grants an additional bump to these numbers, usually around $1,600 to $2,000 per qualifying person depending on filing status).

For roughly 88% of all American taxpayers, this flat number is vastly higher than all of their individual expenses combined. It is designed to completely simplify the tax system for the middle class.

Path B: Itemizing Your Deductions

The alternative path is to itemize. Instead of taking the government’s flat deduction, you manually sum up specific, IRS-approved expenses you incurred during the year and list them on a form called Schedule A.

The operational rule is simple: You should only itemize if your total qualified expenses exceed your standard deduction. If you are Married Filing Jointly, you need to locate more than $31,500 in qualified costs for itemizing to be mathematically worth your effort. That is a massive hurdle. So, what actually counts toward that total?

1. The SALT Cap (State and Local Taxes)

You are allowed to deduct the property taxes you pay on your house, alongside either your state income taxes or state sales taxes. However, there is a brutal legislative limit. The IRS caps this specific deduction at $10,000, regardless of how much you actually pay in local taxes. If you own a home in a high-tax state like California, New Jersey, or Illinois, you will hit this $10,000 cap instantly and lose the ability to deduct the remainder.

2. The Mortgage Interest Deduction

This is the single biggest reason why most Americans still itemize. You can write off the interest you pay on the first $750,000 of your mortgage debt. Because 30-year mortgage rates have hovered between 6% and 7% recently, new homeowners are paying a staggering amount of interest in the first few years of their loan. If you paid your lender $18,000 in pure interest this year, that entire amount goes directly into your itemized bucket.

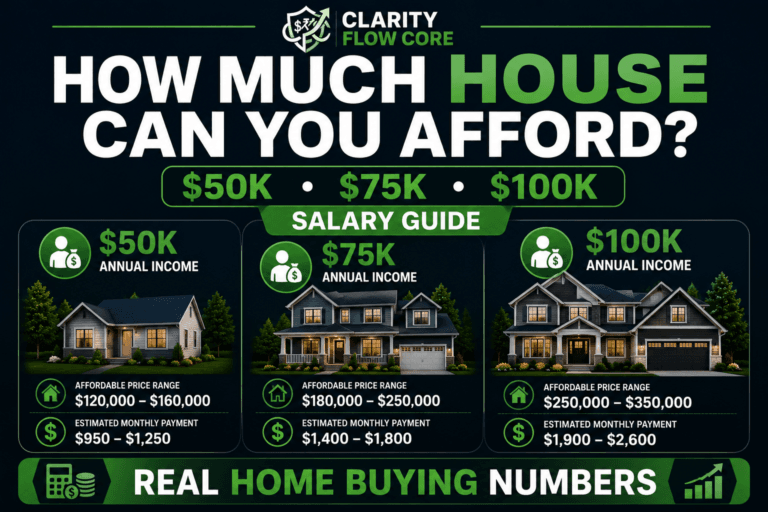

(Want to see if you are ready to take on a mortgage? Check out our First-Time Homebuyer Guide: How Much House Can You Really Afford? to see where you stand.)

3. Charitable Donations

Cash donations to registered 501(c)(3) nonprofits, tithes to your church, or the fair market value of items given to Goodwill all count. The catch? You need a receipt or a bank statement for every single dollar. Tossing $20 cash into a collection bucket does not count if you lack the paper trail. The IRS requires documentation for charitable contributions. Larger donations may require written acknowledgments from the organization.

4. Extreme Medical Costs

This is the hardest hurdle to clear. You can only deduct out-of-pocket medical costs that exceed 7.5% of your Adjusted Gross Income (AGI). If your household makes $100,000, you get zero tax breaks on your first $7,500 in medical expenditures. You can only deduct the money you spent after hitting that massive threshold. Qualified medical expenses are defined by IRS rules and not all healthcare-related spending is deductible.

The Math: Finding the Break-Even Point

Let’s look at the raw operational math of standard deduction vs itemizing for a hypothetical couple, Sarah and John. They are married, file jointly, and own a nice property in Texas. They must clear the $31,500 hurdle to make itemizing worth it.

| Itemized Category | Amount Paid | Allowable Deduction |

| State & Property Taxes | $12,000 | $10,000 (Due to SALT Cap) |

| Mortgage Interest Paid | $14,000 | $14,000 |

| Charitable Donations | $3,000 | $3,000 |

| Medical Expenses | $4,000 | $0 (Did not hit 7.5% of AGI) |

| Total Itemized Deductions | — | $27,000 |

Despite owning a home, paying massive property taxes, and giving heavily to charity, Sarah and John’s itemized total of $27,000 falls drastically short of their $31,500 standard deduction. In the standard deduction vs itemizing battle, they should claim the standard deduction rather than itemize. Important records should still be retained according to IRS recordkeeping guidelines.

The Secret Middle Ground: “Above-The-Line” Deductions

When debating standard deduction vs itemizing, readers constantly ask: “What if I want to claim the massive standard deduction, but I also want to write off my student loan interest?”

You can.

The IRS offers a highly specific category called Adjustments to Income, commonly referred to as “Above-the-Line” deductions. You are legally allowed to claim these specific write-offs in addition to claiming your massive standard deduction. Do not miss these three:

- Student Loan Interest: If you meet the income requirements, you can deduct up to $2,500 of the interest you paid on your federal or private student loans this year.

- Traditional IRA Contributions: If you put money into a Traditional IRA, you can usually deduct up to $7,000 (or $8,000 if you are 50 or older) directly from your taxable income. Review our comparison on Roth IRA for Beginners: How It Works and Why People Use One to maximize your retirement strategy.

- Health Savings Account (HSA) Contributions: If you have a High-Deductible Health Plan and fund an HSA, you can deduct every single dollar you contribute, up to the annual limit.

This loophole ensures you get rewarded for paying off debt and saving for retirement, even if you never itemize. (If you run a side hustle, your deductions are completely separate. Review our guides on 1099 Taxes Explained for Freelancers and Side Hustlers and Freelancer Tax Deductions: Common Expenses You May Be Able to Claim.)

The Advanced Playbook: “Bunching”

If you run the math and realize you are hovering right on the borderline of itemizing every single year, you should execute a strategy called “Bunching”.

Let’s assume you predictably donate $5,000 to charity every December. If you do that, you never clear the itemizing hurdle.

Instead of donating in December 2026, you hold the cash and donate $10,000 in January 2027. By aggressively “bunching” two years’ worth of charitable donations into a single tax year, you artificially spike your itemized deductions enough to clear the threshold for that specific year. You itemize in year one, and revert to the standard deduction in year two, maximizing your overall tax shield.

5 Common Mistakes That Sabotage Tax Returns

When attempting to maximize tax refunds, everyday taxpayers often fall into these costly traps:

- Misunderstanding How Deductions Work: Believing a $500 deduction results in a $500 larger refund. It only lowers your taxable income by $500, which might save you $110 depending on your tax bracket.

- Itemizing Without Proof: Guessing how much you donated to Goodwill and taking an itemized deduction without bank statements or receipts. This can create documentation problems if the IRS requests support for the deduction.

- Missing Above-The-Line Deductions: Forgetting to claim student loan interest or HSA contributions because you assumed you “couldn’t” since you took the standard deduction. If paying debt is overwhelming, utilize our Debt-to-Income Ratio Guide to restructure your finances.

- Mixing Business and Personal Expenses: Trying to write off a personal vehicle or home office on Schedule A. Freelancers must use Schedule C for business expenses, keeping them totally separate from the standard deduction discussion.

- Draining Emergency Savings to Maximize Deductions: Emptying your bank account into an IRA right before Tax Day just to lower your tax bill. Ensure you always check your baseline cash reserves using the Advanced Emergency Fund Analyzer before locking up your cash.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetYour Tax Preparation Action Plan

Ready to stop guessing? Follow these exact steps to ensure you leave no money on the table this April.

- Step 1: Know Your Standard Baseline. Identify your filing status and memorize your standard deduction (e.g., $15,750 for single filers). That is your target to beat.

- Step 2: Tally Your Big Four. Add up your state/local taxes (capped at $10,000), your mortgage interest, your charitable giving, and any massive medical bills.

- Step 3: Compare and Decide. If your “Big Four” total is less than your standard deduction, stop worrying about receipts. Claim the standard deduction rather than itemize.

- Step 4: Claim Your Above-The-Line Wins. Regardless of what you chose in Step 3, submit your 1098-E for student loan interest and your HSA contribution forms to lower your AGI even further.

- Step 5: Map Your Wealth. Tax savings shouldn’t just sit in a checking account. Use the Financial Freedom Planner to direct your refund toward your long-term retirement and investment goals.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanFrequently Asked Questions (FAQs)

Can I switch between the standard deduction and itemizing every year? Yes. You are not locked in. You can take the standard deduction in 2025, itemize in 2026, and switch back to the standard deduction in 2027 based on whichever option gives you the bigger tax break each year.

Do I need to keep receipts if I take the standard deduction? No. The beauty of the standard deduction is that the IRS does not require you to prove any expenses to claim it. However, you still need receipts if you are claiming business expenses for a side hustle or claiming specific tax credits.

Can I deduct my credit card interest? No. Personal credit card interest is not tax-deductible under any circumstances. If high interest is destroying your budget, stop looking for tax loopholes and utilize the Credit Utilization Calculator & Recovery System to build a rapid payoff plan.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationCan I deduct my rent? On your federal tax return, no. Rent payments for your personal residence are never deductible. (Note: A few specific states offer small renter’s credits on state income taxes, but this does not apply to federal returns).

Does a better credit score get me a better tax rate? No. Your credit score has absolutely no bearing on your IRS tax obligations. However, if you are looking to buy a house (which does offer tax benefits via mortgage interest), use the Credit Score Simulator & Improvement Planner to prep your profile for the lowest possible interest rates.

Simulate Your Future Credit Score

Wondering how a new credit card, a missed payment, or paying off a loan will impact your score? Stop guessing. Run real-life financial scenarios instantly through our free simulator.

Launch Credit SimulatorShould homeowners always itemize deductions?

No. Homeowners should compare their mortgage interest, property taxes, charitable contributions, and other eligible deductions against the standard deduction each year.

What is Schedule A?

Schedule A is the IRS form used to report itemized deductions instead of claiming the standard deduction.

Can married couples choose different deduction methods?

No. Married couples filing jointly must use the same deduction method on the return.

References & Trusted Sources

To ensure you are fully prepared for tax season, review the official IRS guidelines referenced in this article:

- IRS Publication 17 (Your Federal Income Tax)

- IRS Schedule A Instructions (Itemized Deductions)

- IRS Topic No. 551 (Standard Deduction)

- IRS Medical and Dental Expenses Guidelines

- IRS Charitable Contributions Requirements

- IRS Student Loan Interest Deduction Rules

Conclusion

Unless you recently purchased an incredibly expensive home with a high interest rate, suffered a catastrophic medical emergency, or donated a massive sum to charity, you are highly likely to take the Standard Deduction.

They should claim the standard deduction rather than itemize. Important records should still be retained according to IRS recordkeeping guidelines. However, the ultimate rule of the standard deduction vs itemizing debate is to never guess. Always run the math both ways inside your tax software before hitting submit. The modern tax code is uniquely designed so that, for the vast majority of Americans, the easiest path is mathematically the most profitable.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.