W-4 Form Explained: How Tax Withholding Actually Works

If you want to understand why having the W-4 form explained is the single most important thing you can do for your paycheck, you just have to look at the month of April. Every spring, millions of Americans sit down to file their taxes, and they experience one of two extremes.

Half of them jump for joy because they are getting a massive $4,000 refund. The other half stare at their computer screens in absolute horror because they suddenly owe the IRS $2,500 that they do not have.

Neither of these situations is a surprise, and neither of them is luck. Your tax refund (or your tax bill) is entirely determined by a single piece of paper you filled out on your very first day of work: the IRS Form W-4.

If you are tired of owing the government money, or if you are tired of living paycheck-to-paycheck while waiting for a massive refund to save you, you have the operational power to fix it today. Here is the ultimate guide to getting the W-4 form explained, adjusting your withholdings, and taking permanent control of your cash flow.

⚡ Quick Answer

- The W-4 form tells your employer how much federal income tax to withhold from each paycheck.

- Completing it accurately helps reduce the chances of receiving an unexpectedly large tax refund or owing a significant tax bill when you file your return.

What Actually is the W-4 Form?

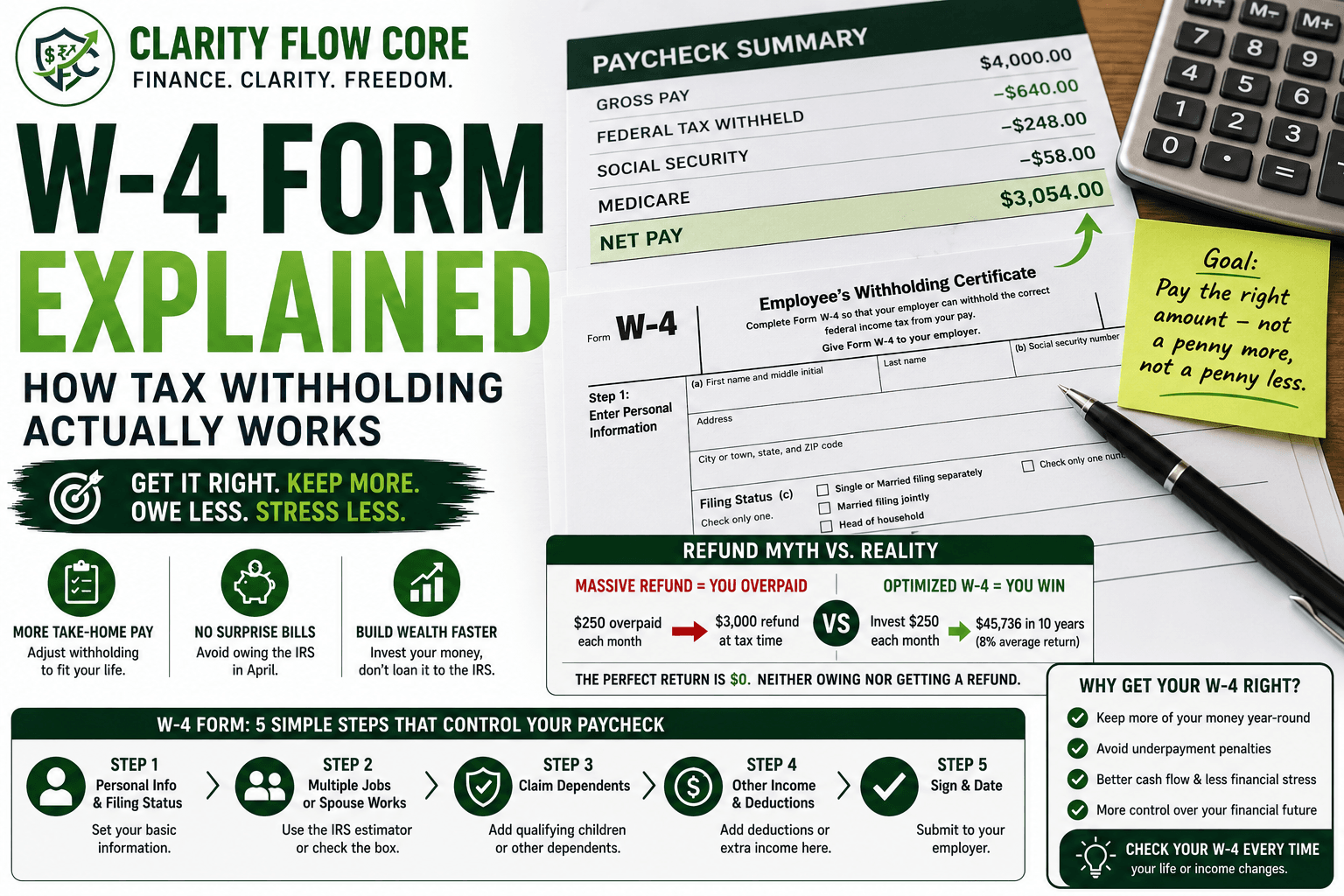

When you get hired for a new job, Human Resources hands you a massive stack of onboarding paperwork. Tucked inside that packet is the Employee’s Withholding Certificate.

This form does one very specific, highly critical job: it tells your employer’s payroll department exactly how much money to hold back from your paycheck each week to send to the IRS for your federal income taxes.

The United States tax system is “pay-as-you-go.” You cannot simply wait until Tax Day to write a check for your entire tax bill for the year. The IRS demands a cut of every single paycheck you earn as you earn it. Your W-4 dictates exactly how big that cut is. If you want the W-4 form explained simply: it is the dial that controls the volume of your take-home pay.

The Math: The Myth of the “Good” Tax Refund

Before we get the individual steps of the W-4 form explained, we need to completely rewire how you think about tax refunds.

Most people view a $3,000 tax refund as a wonderful gift from the government or a forced savings account. It is not a gift. It is a mathematical failure.

If you get a $3,000 refund, it means you overpaid your taxes by $250 every single month last year. The government took your money, held onto it for a year, used it to fund their own operations, paid you exactly 0% interest on it, and then finally handed your own money back to you twelve months later.

Look at the operational math of what happens when you keep that money instead of loaning it to the IRS. If you properly adjust your W-4 to put that $250 back into your monthly paycheck, and you route it into an investment:

| Strategy | Monthly Cash | Annual Result | Hypothetical 10-Year Investment Growth |

| Bad W-4 (Massive Refund) | $0 extra per month | You get a $3,000 check. | $30,000 (No compound growth). |

| Optimized W-4 (Invested) | $250 extra per month | You invest $3,000. | $45,736 (Massive compound growth). |

By failing to get the W-4 form explained to you, you are actively losing thousands of dollars in compound interest.

The Goal is Zero: Your goal when filling out a W-4 is not to get a massive refund, and it is not to owe a massive bill. From a cash-flow perspective, many people aim for a refund or balance due that is as close to zero as possible. You want to pay the IRS exactly what you owe them—not a penny more, and not a penny less.

Step-by-Step: The W-4 Form Explained

A few years ago, the IRS completely redesigned the W-4. They removed the confusing “allowances” system (where you had to claim a “1” or a “0”) and replaced it with a straightforward, five-step worksheet. Here is exactly how to navigate it.

Step 1: Personal Information and Filing Status

This step is mandatory. You will fill out your name, address, and Social Security number.

The most critical part of having this step of the W-4 form explained is selecting your Filing Status (Single, Married Filing Jointly, or Head of Household). Your employer’s payroll software uses this exact status to determine your Standard Deduction.

If you select “Single,” the software assumes you get the standard individual deduction and calculates your taxes based on that baseline.

(Warning: If you are married but you both work, blindly checking “Married Filing Jointly” in Step 1 can actually cause you to under-withhold if you ignore Step 2).

Step 2: Multiple Jobs or Spouse Works

This is where 90% of the agonizing mistakes happen. If you work two jobs, or if you are married and both you and your spouse work, you must complete Step 2.

If you skip this step, Job A will assume it is your only income, and Job B will assume it is your only income. They will both give you the full Standard Deduction, resulting in neither job taking out enough taxes. Come April, you will owe the IRS thousands of dollars.

To get this section of the W-4 form explained correctly, you have three options to fix the dual-income trap:

- Option A: Use the IRS Tax Withholding Estimator online (more on this below).

- Option B: Use the Multiple Jobs Worksheet on page 3 of the W-4.

- Option C (The Operational Hack): If you and your spouse make roughly the exact same amount of money, you can both simply check the box in Step 2(c) on your respective W-4s. This tells both employers to cut your standard deduction in half, ensuring enough taxes are withheld to cover your combined household income.

Step 3: Claiming Dependents

Do you have children under the age of 17? This is where you claim the Child Tax Credit.

You generally multiply the number of qualifying children by $2,000. If you have two kids, you put $4,000 on line 3.

Here is the best part of having the W-4 form explained: this number is an annual total. Your employer will take that $4,000, divide it by the number of pay periods in the year, and reduce your tax withholding by that exact amount each paycheck. This puts more money in your pocket today instead of making you wait for a refund.

Step 4: Other Adjustments (The Secret Weapon)

Step 4 is optional, but it is the ultimate tool for fine-tuning your paycheck. This is where advanced tax planning happens.

- Step 4(a) Other Income: If you have income outside of a regular job that isn’t taxed (like dividends from investments or rental property cash flow), put the annual total here so your W-2 employer can withhold taxes for it automatically.

- Step 4(b) Deductions: If you plan on Itemizing your deductions instead of taking the Standard Deduction, use the worksheet to enter that larger amount here.

- Step 4(c) Extra Withholding (The Panic Button): If you owed the IRS $1,200 last year and you are terrified of it happening again, simply take $1,200, divide it by your 24 paychecks, and put $50 on line 4(c). Your employer will automatically pull an extra $50 out of every single check and send it to the IRS. You will never have a surprise tax bill again.

(Note: Many side-hustlers use Step 4(c) to avoid making quarterly estimated payments. If you have a freelance video editing business, you can use your W-2 job’s W-4 to withhold extra cash to cover your side hustle taxes!)

Step 5: Sign and Date

Sign the form and hand it back to your HR department or upload it to your payroll portal. You are done.

When Your W-4 Strategy Backfires

No W-4 form explained guide is complete without looking at the worst-case scenarios. If you treat this form casually, it will backfire aggressively. Here is exactly when the system burns you:

1. The Underpayment Penalty

The IRS does not just get mad if you owe them money in April; they literally fine you for it. If you fill out your W-4 incorrectly, underpayment penalties depend on several factors, including how much tax was owed, how much was withheld, and whether safe-harbor rules were met. You will have to pay the taxes you owe, plus a percentage-based fine for failing to withhold enough throughout the year.

2. “Life Event” Blindness

Your W-4 is not a legally binding contract that you are locked into forever. A major reason people need the W-4 form explained is that they filled it out at age 22 and never looked at it again.

You must ask your HR department for a new W-4 immediately if any of these “Life Events” occur:

- You get married or divorced (Your filing status changes).

- You have a baby (You get a new Child Tax Credit).

- Your spouse gets a new job or loses a job (Your household income bracket shifts drastically).

- You start a profitable side hustle (You will owe 1099 taxes and need to adjust your W-2 withholding to cover the difference).

The Ultimate Hack: The IRS Withholding Estimator

If you are terrified of doing the manual math wrong, the government actually built a highly effective digital tool to do it for you.

Grab your most recent pay stub, grab your spouse’s pay stub, and go to the Tax Withholding Estimator on the official IRS.gov website. The calculator will ask you a series of simple questions about your salary, your 401(k) contributions, and your dependents.

At the end of the questionnaire, it will tell you exactly whether you are currently on track for a refund or a massive bill. Best of all, it will literally generate a pre-filled W-4 document for you based on the math. All you have to do is print it, sign it, and hand it to your boss. This automates the entire W-4 form explained process.

Frequently Asked Questions (FAQs)

When should I update my W-4?

You should consider updating your W-4 whenever you experience a major life event such as marriage, divorce, a new child, a second job, or significant changes in income.

Can I submit a new W-4 at any time?

Yes. Employees can generally update their W-4 whenever they want through their employer’s payroll system.

What happens if I claim too little withholding?

You may owe additional taxes when filing your return and could potentially face underpayment penalties.

What happens if I claim too much withholding?

You may receive a larger refund, but your take-home pay throughout the year will be lower.

Does the W-4 affect state taxes?

The W-4 only affects federal income tax withholding. Many states have separate withholding forms.

References & Trusted Sources

To ensure your withholding is accurate and compliant, always refer to the official documentation and tools provided by the Internal Revenue Service:

- IRS Form W-4 (Employee’s Withholding Certificate)

- IRS Tax Withholding Estimator

- IRS Publication 505 (Tax Withholding and Estimated Tax)

- IRS FAQs on Withholding

The Bottom Line

Understanding exactly how your paycheck is calculated is the ultimate adult superpower. By getting the W-4 form explained to you and actively adjusting your withholdings, you stop giving the government interest-free loans and you stop living in absolute terror of April 15th.

If you are trying to optimize your entire financial life, fixing your tax withholdings is step one. Once your paycheck is accurate, you can route that extra monthly cash into The 50/30/20 Budget Rule Explained Simply or use it to accelerate your Debt Avalanche vs. Debt Snowball payoff plan.

Check your pay stubs this Friday. If you are withholding too much, run your numbers through the IRS estimator, hand a new W-4 to your HR department, and take permanent control of your hard-earned money.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.