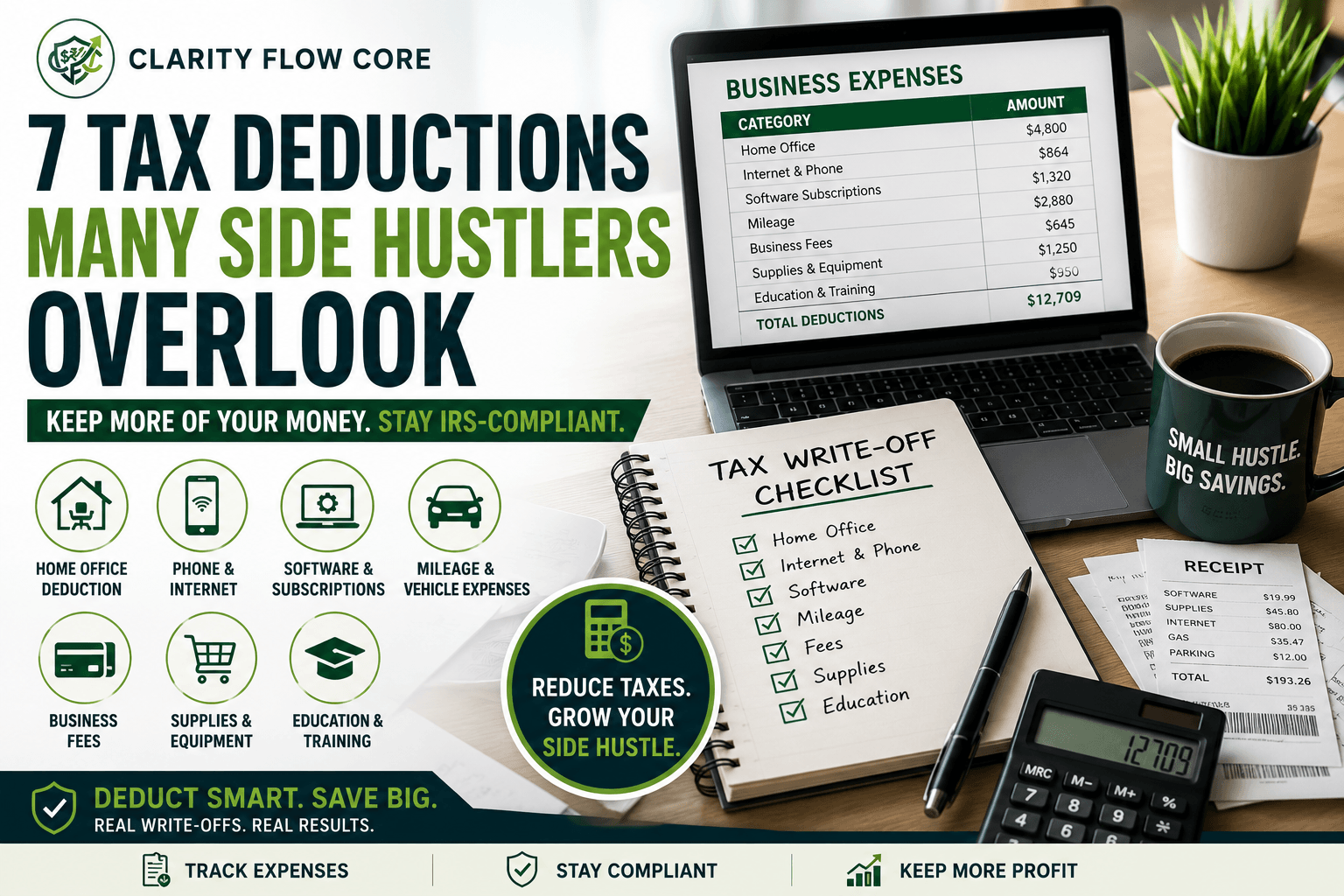

7 Tax Deductions Many Side Hustlers Overlook

You finally started making money outside of your regular 9-to-5. You landed a few clients, the invoices cleared, and your bank account is growing. But before you take that cash and upgrade your lifestyle, you need to uncover the most effective tax deductions for your side hustle.

(If you’re new to self-employment, start with 1099 Taxes Explained for Freelancers and Side Hustlers to understand how self-employment taxes work before focusing entirely on deductions).

Uncle Sam always wants his cut.

When you work a traditional W-2 job, your employer pays half of your Medicare and Social Security taxes. When you are a freelancer, you are hit with the Self-Employment Tax, meaning you pay the full 15.3% yourself, plus your standard income tax brackets.

Navigating this reality as a new freelancer can be genuinely terrifying. However, the absolute worst thing you can do is overpay the IRS simply because you didn’t know the rules. You do not need to be a massive corporation to take advantage of the U.S. tax code. The government actually incentivizes small business owners to reinvest in their operations.

If you want to keep your hard-earned money, you need to know exactly which business write-offs are 100% legal, surprisingly easy to claim, and heavily overlooked by beginners. Here is the operational math behind the most powerful side hustle tax deductions available to you this year.

⚡ Quick Answer

Freelancers and side hustlers can drastically lower their tax bill by tracking ordinary and necessary business expenses. The most effective 1099 tax deductions include the home office deduction, partial cell phone and internet bills, software subscriptions, payment processing fees, and business mileage.

To survive an audit, you must strictly separate personal and business finances and keep meticulous records of your deductible business expenses.

The IRS “Golden Rule” of Write-Offs

Before we look at the specific tax deductions for your side hustle, you must understand the foundational rule of the IRS.

A business expense is legally deductible if it is both “ordinary” and “necessary.”

- Ordinary: An expense that is common and accepted in your specific trade or business.

- Necessary: An expense that is helpful and appropriate for your trade or business. (It does not have to be absolutely indispensable to be considered necessary).

You cannot write off a brand-new jet ski if you are a freelance graphic designer. But a new MacBook Pro? Absolutely.

Here is how the “Ordinary and Necessary” rule applies in the real world:

| Expense | Freelance Video Editor | Uber Driver | Is it Deductible? |

| Adobe Creative Cloud | Necessary software to edit videos. | Irrelevant to driving. | Yes for Editor / No for Driver |

| Car Washes & Detailing | Irrelevant to editing at home. | Necessary to maintain a clean ride for passengers. | No for Editor / Yes for Driver |

| $400 Rolex Watch | Not necessary. Your phone tells time. | Not necessary. Your dashboard tells time. | NO (Audit Trap) |

With that framework established, here are the seven most lucrative tax deductions for your side hustle that you should be tracking immediately.

1. The Home Office Deduction

If you edit videos, write articles, or code software from a spare bedroom, the Home Office Deduction is mathematically the most powerful tool in your arsenal of self-employed tax deductions.

To qualify, you must use a specific area of your home regularly and exclusively for your business. You cannot write off your dining room table if you also eat dinner there.

There are two ways to calculate this deduction:

- The Simplified Method: The IRS allows you to deduct $5 per square foot of your home office, up to a maximum of 300 square feet. If your spare bedroom is 150 square feet, your deduction is a flat $750. It requires zero math and zero receipts.

- The Actual Expenses Method: If you rent an expensive apartment or have a large mortgage, this method is often far more lucrative. You calculate the square footage of your office as a percentage of your entire home, and you deduct that percentage of your total housing costs (including utilities, insurance, and HOA fees).

- Apartment Size: 1,000 sq ft.

- Office Size: 200 sq ft. (20% of your home).

- Total Rent & Utilities Paid for the Year: $24,000.

- Your Write-Off: 20% of $24,000 = $4,800.

Lowering your taxable income by $4,800 is one of the most effective tax deductions for your side hustle, saving you hundreds of dollars in actual cash. (If you’re unsure how to manage irregular freelance income alongside these deductions, see How to Budget as a Freelancer When Income Changes Every Month).

2. A Portion of Your Cell Phone & Internet Bill

You need the internet to deliver client work, and you need a cell phone to take client calls and manage your business social media accounts.

You cannot write off your entire family’s unlimited data plan. However, you can safely deduct the percentage you realistically use for work. If you use your personal cell phone for business roughly 40% of the time, you can legally write off 40% of the annual bill.

If your phone bill is $100 a month ($1,200 a year), and your home internet is $80 a month ($960 a year), a 40% business-use claim gives you an $864 deduction.

3. Software and SaaS Subscriptions

In the digital economy, software is your storefront. Think about the tools you need to run your daily operations. Because these are direct operating expenses, they are 100% deductible.

If you are a content creator or digital freelancer, your software stack likely looks like this:

- Adobe Premiere Pro or Photoshop ($55/mo)

- Canva Pro ($15/mo)

- Squarespace Website Hosting ($20/mo)

- Google Workspace / Custom Email ($6/mo)

- QuickBooks Self-Employed or Bookkeeping Software ($15/mo)

That equals roughly $1,332 a year. When calculating the best freelancer deductions, never ignore the small, recurring $15 charges. They compound heavily over 12 months. (Freelance creatives can also review our Freelance Video Editor Tax Guide: Deductions, Write-Offs & Basics for industry-specific examples).

4. Payment Processing & Bank Fees

This is one of the most frequently missed 1099 tax deductions for side hustlers.

Are you getting paid through PayPal, Stripe, Square, or Upwork? Those platforms take a hefty 2.9% to 3% fee (sometimes up to 10% on Upwork) out of every single transaction.

Let’s say a client pays you $2,000 via Stripe. Stripe takes a $60 fee, and $1,940 actually hits your bank account.

At the end of the year, Stripe will send a 1099-K form to the IRS stating that your gross volume was $2,000. If you do not claim that $60 fee as a business expense on your Schedule C, you will literally pay income taxes on money that Stripe kept. Always deduct merchant fees, wire transfer costs, and business bank account maintenance fees.

5. Self-Education and Courses

The government actually incentivizes you to improve your skills, making education one of the smartest tax deductions for your side hustle.

If you buy an online course on advanced color grading, attend a digital marketing workshop, or purchase a book directly related to improving your current freelance service, keep that receipt.

The Catch: The education must maintain or improve the skills required in your current business. You cannot write off a $15,000 real estate license course if your current side hustle is freelance writing. It must apply to the business you are actively running.

For example, a video editor learning advanced editing techniques would generally fall within the scope of business education expenses. See How to Start a Video Editing Side Hustle (Even as a Beginner) for more on how to scale those specific skills.

6. Advertising, Marketing, and Lead Gen

Any money you spend trying to get your brand in front of new clients is a valid, 100% deductible business expense.

This includes:

- Paying $50 to boost a post on Facebook or Instagram.

- Printing physical business cards or flyers.

- Buying “Connects” on Upwork to apply for jobs.

- Paying a networking group’s annual membership fee.

- Hiring a logo designer on Fiverr.

Marketing is the lifeblood of client acquisition, and the IRS fully supports you spending money to grow your revenue.

7. Business Mileage and Travel

If you have to drive to meet a local client, pick up hard drives, or shoot a wedding, those miles count.

You cannot deduct your standard, daily commute to your regular W-2 day job. But driving specifically for your freelance gig is a prime write-off. Tracking your miles is arguably one of the most profitable tax deductions for your side hustle because of the generous IRS Standard Mileage Rate (which is updated periodically, but usually hovers around 65 to 67 cents per mile).

If you drive 3,000 miles this year specifically for freelance video shoots and client meetings, you get a direct $2,010 deduction. If you deliver food, drive for rideshare apps, or meet clients in person, mileage often becomes one of the largest deductions available.

Do not try to guess this number in April. Download a mileage tracker app like MileIQ or Everlance on January 1st, which uses GPS to automatically log your drives in the background.

5 Most Commonly Missed Side Hustle Deductions

Even experienced freelancers forget to track certain overhead costs. Because many of these services are set to “auto-pay,” they become invisible to the business owner. Do not forget to claim these deductible business expenses:

- Business Domain Names & Website Hosting: Buying a URL from Namecheap or GoDaddy is a 100% deductible advertising and operations expense.

- Professional Memberships: Dues paid to professional organizations, local chambers of commerce, or trade associations.

- Business Insurance: If you carry General Liability Insurance, Errors & Omissions (E&O) insurance, or specific equipment insurance to protect your camera gear, the premiums are deductible.

- Cloud Storage: Upgrading your Google Drive, Dropbox, or Apple iCloud storage specifically to house heavy client files is an ordinary and necessary expense.

- Accounting Software & Professional Fees: The $15/month you pay for QuickBooks, or the $400 you pay a CPA to file your Schedule C, are entirely deductible costs of doing business.

What Records Should You Keep?

In the event of an IRS audit, the burden of proof rests entirely on you. You cannot just claim a $5,000 deduction for electronics and expect the government to take your word for it. To safely claim business write-offs, you must maintain a pristine paper trail.

You need to keep the following documents securely filed (digitally or physically) for at least three to seven years:

- Business Bank Statements: Showing clear separation of income and expenses.

- Itemized Receipts: A credit card statement showing a charge to “Best Buy” isn’t enough; you need the actual receipt showing you bought a business laptop, not a video game console.

- Mileage Logs: A contemporaneous log detailing the date, distance, and business purpose of every drive.

- Software Invoices: Download the PDF invoices from your SaaS providers monthly.

- Phone and Internet Bills: Highlighting the total cost to back up your business-use percentage claims.

- 1099 Forms: All 1099-NEC and 1099-K forms sent to you by clients and payment processors.

When Deductions Backfire: The Audit Traps

Understanding the list of tax deductions for your side hustle is only half the battle. Knowing how to stay out of trouble with the IRS is just as important. If you treat the tax code like a cheat code to fund your personal life, it will backfire aggressively.

Here are the operational traps that trigger audits:

1. Commingling Your Funds

If you buy your groceries, your dog food, and your Adobe subscription all on the exact same personal credit card, you are begging for an audit. If the IRS audits your tax deductions for your side hustle and sees commingled funds, they can instantly disallow all of your deductions due to poor record-keeping. You will be forced to pay back-taxes and severe financial penalties. You must open a dedicated Business Checking Account.

A separate business checking account also makes quarterly tax payments much easier to track. See Quarterly Estimated Taxes Explained for Freelancers and Side Hustlers.

2. The “Section 179” Gear Trap

The IRS has a rule (Section 179) that allows you to deduct the entire purchase price of heavy equipment in a single year. Beginners hear this and immediately finance a $4,000 camera and a $3,000 computer, thinking the “write-off” makes it free.

A write-off does not make an item free. It just means you don’t pay taxes on the money used to buy it. If you spend $7,000 on gear to save $1,500 in taxes, you are still out $5,500 in actual cash. Never buy gear just to get a tax deduction.

3. The Hobby Loss Rule

If your side hustle loses money for three out of five consecutive years, the IRS will reclassify your business as a “hobby.” Once you are classified as a hobby, you are legally barred from claiming any tax deductions for your side hustle, but you still have to report the income. You must operate with a legitimate profit motive.

Choosing the right business structure can also help demonstrate legitimate business intent. See Sole Proprietor vs LLC: Which Is Best for a Side Hustle?.

Frequently Asked Questions (FAQs)

Can I deduct a laptop used for both work and personal use?

Yes, but you can only deduct the percentage of the cost that corresponds to its business use. If you use it 70% for your freelance work and 30% for personal browsing, you can only write off 70% of the cost.

Can I deduct meals with clients?

Generally, yes. You can deduct 50% of the cost of qualifying business meals provided the meal has a clear business purpose and you or an employee is present.

Do I need receipts for every deduction?

Yes. While bank statements prove a transaction occurred, itemized receipts are required to prove what was actually purchased and that it qualifies as an ordinary and necessary business expense.

Can I deduct a home office if I rent?

Absolutely. The home office deduction applies to both renters and homeowners, provided the space is used regularly and exclusively for business. Renters can deduct a percentage of their monthly rent and utility payments.

What happens if I forget to claim a deduction?

If you forget to claim a legitimate business expense on your original tax return, you can generally file an amended return (Form 1040-X) within three years of the original filing date to claim the missed deduction and secure a refund.

Your Next Steps

The key to successfully claiming all these tax deductions for your side hustle is ruthless, simple organization. You do not need to hire a $300/hour Wall Street accountant right away. You simply need to implement a financial system.

Treat your side hustle like a real, operational business, track your expenses meticulously, and stop giving the IRS more money than they are legally entitled to.

Before tax season arrives, review these essential guides to guarantee your business finances are fully optimized:

- 1099 Taxes Explained for Freelancers and Side Hustlers

- Quarterly Estimated Taxes Explained for Freelancers

- Freelancer Tax Deductions: Common Expenses You May Be Able to Claim

- Sole Proprietor vs LLC: Which Is Best for a Side Hustle?

References & Trusted Sources

To ensure your write-offs remain compliant and mathematically accurate, always refer to the official documentation provided by the Internal Revenue Service:

- IRS Publication 535 (Business Expenses)

- IRS Home Office Deduction Guidance

- IRS Schedule C Instructions

- IRS Section 179 Information

- IRS Qualified Business Income Deduction Guidance

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.