Roth IRA Contribution Limits and Rules for 2026: A Complete Guide

If you are looking for a way to build serious, long-term wealth, the Roth IRA is one of the most powerful tools at your disposal. The premise is incredibly simple: you put money into the account after you have paid your taxes on it today, and then every dollar of growth—and every dollar you withdraw in retirement—is 100% tax-free.

But because the tax benefits are so massive, the government does not let you put an unlimited amount of money into a Roth IRA. The Internal Revenue Service (IRS) sets strict annual limits on exactly how much you can contribute, and they also enforce strict income limits that restrict high earners from using the account directly.

Every year, the IRS adjusts these rules to account for inflation. If you accidentally put too much money into your account, or if you contribute when your income is too high, you could get hit with a nasty 6% tax penalty every single year until you fix the mistake.

In this guide, we are going to break down the exact 2026 Roth IRA contribution limits, explain the income phase-out ranges without using confusing accounting jargon, and show you exactly how to maximize your tax-free retirement savings this year.

⚡ 2026 Roth IRA Quick Reference

| Rule | 2026 Number |

| Contribution Limit | $7,500 |

| Catch-Up Limit (50+) | $8,600 |

| Single Phase-Out Starts | $153,000 |

| Single Cutoff | $168,000 |

| Married Phase-Out Starts | $242,000 |

| Married Cutoff | $252,000 |

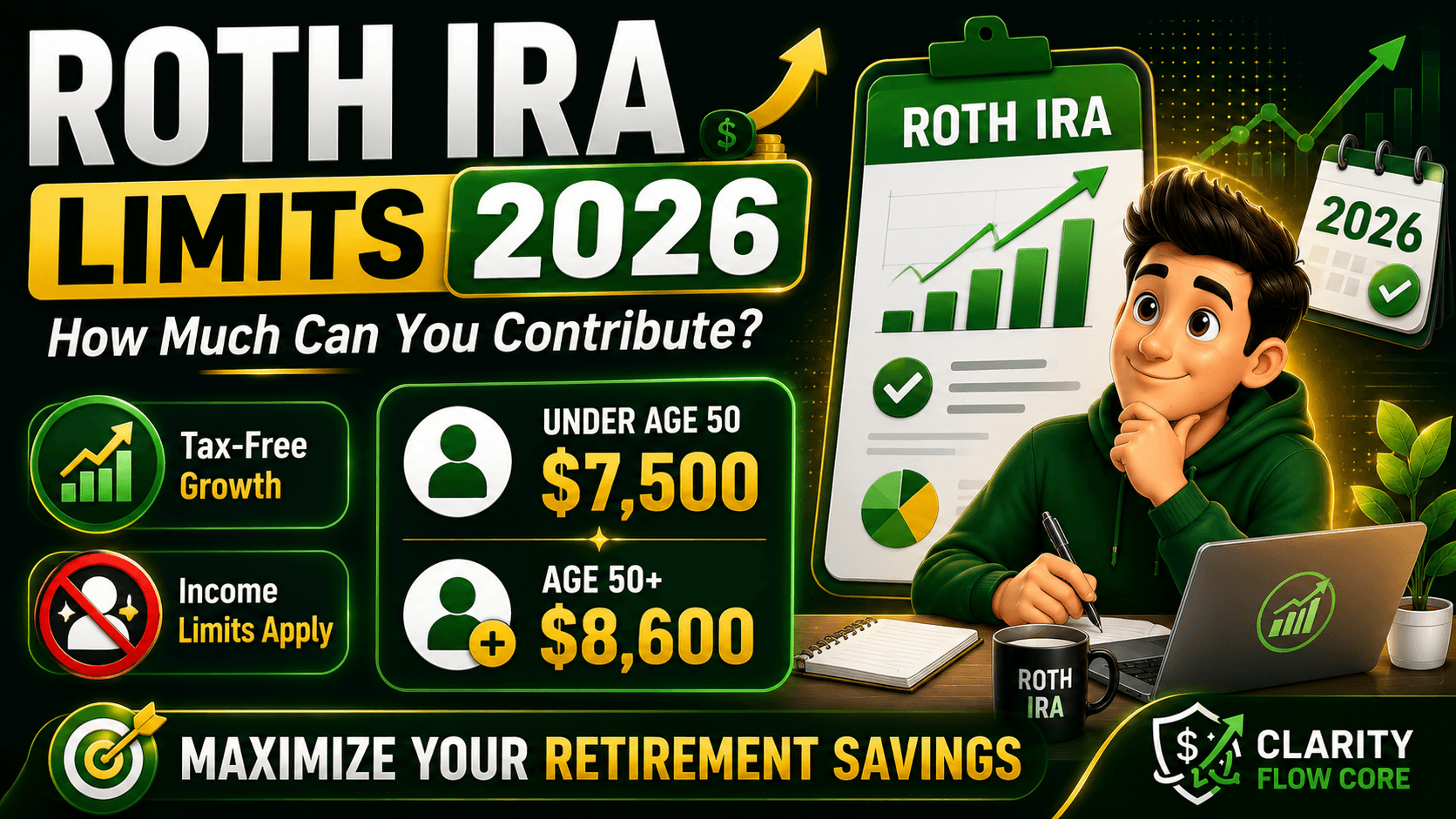

2026 Roth IRA Contribution Limits

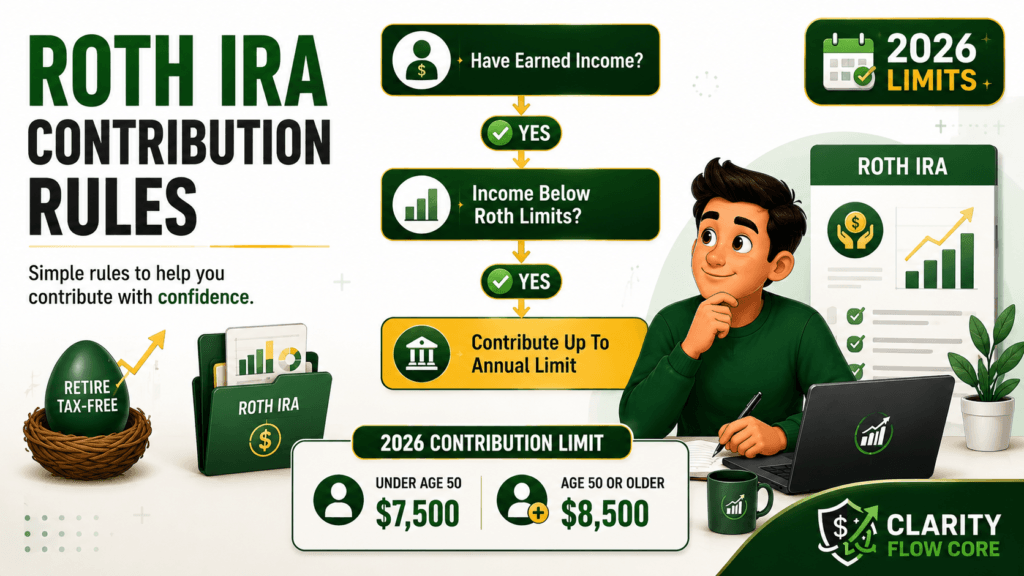

The first rule of a Roth IRA is the annual contribution limit. This is the absolute maximum amount of cash the IRS allows you to physically transfer into your IRA over the course of the year. For 2026, the IRS has officially set the standard contribution limits based on your age.

If You Are Under Age 50

If you are under the age of 50, your maximum Roth IRA contribution limit for 2026 is $7,500.

You do not have to contribute the full $7,500. You can put in $50 a month, or $1,000 a year—whatever fits comfortably into your budget. But once you hit that $7,500 ceiling, you legally cannot add another penny to your Roth IRA for the rest of the year.

If You Are Age 50 or Older (Catch-Up Contributions)

If you turn 50 years old at any point during the 2026 calendar year, the government gives you a bonus. Because you are getting closer to retirement age, the IRS allows you to make an additional “catch-up” contribution of $1,100.

This brings your total maximum contribution limit for 2026 to $8,600.

(Note: These limits apply to all of your IRAs combined. You cannot put $7,500 into a Traditional IRA and another $7,500 into a Roth IRA in the same year. The $7,500 limit is the maximum you can spread across both accounts.)

2026 Roth IRA Income Limits (The Phase-Out Rules)

The second massive rule you need to understand is the income limit. The government created the Roth IRA specifically to help working-class and middle-class Americans save for retirement. To keep the ultra-wealthy from hoarding tax-free money, the IRS restricts who can legally use the account based on their income.

To figure out if you are allowed to contribute, you have to look at your Modified Adjusted Gross Income (MAGI). Think of MAGI as your total yearly income minus a few specific tax deductions.

If your MAGI crosses a certain threshold, the amount you are allowed to contribute starts to shrink—this is called the “phase-out” range. If your income goes even higher, your ability to contribute drops to $0.

Here are the official 2026 Roth IRA income limits based on how you file your taxes:

Single / Head of Household

- Full Contribution: If your MAGI is less than $153,000, you can contribute the full $7,500 (or $8,600 if 50+).

- Partial Contribution (Phase-Out): If your MAGI is between $153,000 and $167,999, the amount you can contribute is reduced. If your income falls inside the phase-out range, the IRS reduces your contribution limit using a specific formula. You can still put some money in, but not the maximum amount.

- No Contribution Allowed: If your MAGI is $168,000 or more, you are completely restricted from contributing directly to a Roth IRA.

Married Filing Jointly

- Full Contribution: If you and your spouse have a combined MAGI of less than $242,000, you can each contribute the maximum limit to your individual Roth IRAs.

- Partial Contribution (Phase-Out): If your combined MAGI is between $242,000 and $251,999, your contribution limits are reduced using the IRS formula.

- No Contribution Allowed: If your combined MAGI is $252,000 or more, neither of you can directly contribute to a Roth IRA.

Married Filing Separately

The IRS heavily penalizes married couples who choose to file their taxes separately while still living together.

- If you lived with your spouse at any point during the year and you file separately, your phase-out range begins at $0 and ends at $10,000.

- If you make $10,000 or more, you cannot contribute to a Roth IRA.

What Happens If You Earn Too Much?

If you get a massive promotion this year and suddenly find that your income exceeds the $168,000 limit (for single filers) or the $252,000 limit (for married couples), you are not entirely locked out of tax-free growth.

High-income earners often use a completely legal strategy known as the “Backdoor Roth IRA”.

Because there are no income limits to contribute to a Traditional IRA, you can put your money into a Traditional IRA first. Then, you immediately execute a “Roth Conversion,” transferring that money from the Traditional basket into the Roth basket. You will have to pay income taxes on the money during the conversion, but once it is in the Roth, it grows tax-free forever.

If you are a high earner or a freelancer who wants to shelter even more money from taxes, we highly recommend reading our guide on SEP IRA vs Solo 401(k) for Freelancers to explore higher-limit alternatives.

The Earned Income Rule and Spousal IRAs

There is a golden rule in the retirement world: you cannot contribute to an IRA unless you have “earned income”. Earned income means money you made from actually working—like a salary from a W-2 job, hourly wages, or profits from a side hustle or small business.

Passive income—like unemployment benefits, child support, rental income, or interest from a savings account—does not count. If you only made $4,000 from working your part-time job this year, the absolute maximum you can put into your Roth IRA is $4,000. You cannot exceed your actual earned income for the year.

The Spousal IRA Exception

If you are married and filing jointly, the IRS offers a fantastic exception for stay-at-home parents or non-working spouses. As long as one spouse works and earns enough income to cover the contributions for both people, the non-working spouse can open and fund their own Roth IRA.

For example, if a working spouse makes $100,000 a year and the other spouse stays home to raise children (earning $0), the working spouse can fund their own Roth IRA with $7,500, and they can also put $7,500 into a separate Spousal Roth IRA for their partner.

When Should You Contribute to Your Roth IRA?

One question many first-time investors ask is whether they should contribute their entire annual limit at once or spread their contributions throughout the year.

There isn’t a single “correct” answer. If you have enough cash available early in the year, contributing a lump sum allows your investments to spend more time in the market, giving compound growth more time to work in your favor. Historically, investing earlier has often produced better long-term results because your money has a longer opportunity to grow.

However, for most people, making automatic monthly contributions is the more practical strategy. Contributing $625 each month allows you to reach the full 2026 limit of $7,500 without placing unnecessary strain on your budget. It also follows a disciplined investing approach known as dollar-cost averaging, where you invest consistently regardless of whether the market is rising or falling.

The most important factor isn’t whether you contribute monthly or annually—it’s contributing consistently. Even smaller, automatic deposits made year after year can build substantial tax-free wealth over several decades thanks to the power of compounding.

Common Mistakes Beginners Make With Roth IRAs

Now that you know the limits, you need to ensure you do not make a mistake that triggers a penalty or stalls your financial growth. Avoid these massive traps.

Mistake 1: Overcontributing by Accident

If you accidentally put $8,000 into your Roth IRA when the limit is only $7,500, the IRS will hit you with a 6% penalty on the excess $500. What is worse, they will charge you that 6% penalty every single year until you remove the extra cash from the account. If you realize you made a mistake, contact your brokerage immediately before Tax Day to withdraw the excess funds and avoid the ongoing tax nightmare. Excess contributions typically need to be corrected before your tax filing deadline to avoid ongoing penalties.

Mistake 2: Funding the Account and Leaving it in Cash

Putting $7,500 into a Roth IRA does not mean you have invested $7,500. A Roth IRA is just a protective tax basket. If you transfer the money from your bank and never log in to buy actual investments (like low-cost index funds or ETFs), your money will sit there in cash, earning practically nothing. To build wealth, you must actively purchase assets inside the account.

Mistake 3: Skipping an Emergency Fund

Because Roth IRAs have a unique rule that allows you to withdraw your contributions (but not your growth) without a penalty at any time, many beginners treat their Roth IRA like a standard savings account. This is a disaster. Every time you pull money out, you reset your compound interest and rob your future self.

Before you start aggressively funding your retirement, use our Advanced Emergency Fund Analyzer to calculate exactly how much cash you need to hold in a separate, accessible High-Yield Savings Account. For a deeper dive into how to build this cushion, read our Emergency Fund Basics Guide.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetYour Step-by-Step Action Plan

Ready to maximize your Roth IRA in 2026? Follow this precise timeline.

- Check Your Eligibility: Look at your expected salary for the year. If you are single and expect to make less than $153,000, you are clear to proceed.

- Determine Your Goal: You do not have to hit the $7,500 limit. Decide how much you can comfortably afford to save each month without going into debt. Use our Financial Freedom Planner to map out how different monthly contributions will impact your retirement age.

- Automate Your Deposits: Break your annual goal into monthly chunks. To hit the $7,500 limit, you need to contribute $625 per month. Set up an automatic transfer from your checking account to your brokerage account on the day you get paid.

- Invest the Cash: Ensure your automated deposits are actually being used to purchase index funds or target-date retirement funds inside the IRA.

- Watch the Deadline: You actually have until Tax Day (usually April 15) of the following year to make contributions for the current year. You can make 2026 contributions all the way up until April 2027.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanFrequently Asked Questions (FAQ)

Can I contribute to both a 401(k) and a Roth IRA? Yes. Your 401(k) limits and your IRA limits are completely separate. In 2026, you can max out your workplace 401(k) and still put $7,500 into a personal Roth IRA (assuming you meet the income requirements).

What happens if I turn 50 halfway through the year? If your 50th birthday falls at any time during the calendar year (even December 31st), you are eligible to make the full $8,600 catch-up contribution for that entire tax year.

Do I have to take Required Minimum Distributions (RMDs) from my Roth IRA? No. One of the massive advantages of a Roth IRA over a Traditional IRA is that the IRS never forces you to withdraw the money. You can leave the funds in your Roth IRA to grow tax-free for your entire life, and eventually pass the tax-free account down to your heirs.

Can my child open a Roth IRA? Yes, but only if they have actual earned income. If your teenager made $3,000 working a summer job as a lifeguard, you can open a Custodial Roth IRA for them and contribute up to $3,000.

What if I contribute to a Roth IRA and then realize I made too much money? If your income ends up being higher than you expected and you accidentally contribute past the phase-out limit, you can contact your brokerage and ask them to “recharacterize” your contribution. They will shift the money into a Traditional IRA, helping you avoid the 6% overcontribution penalty.

Does my Roth IRA limit change if I get married this year? Yes. The IRS looks at your marital status as of December 31st. If you get married on December 30th, the IRS considers you married for the entire tax year, and you will be subject to the joint income limits rather than the single limits.

Conclusion

The Roth IRA is arguably the single best wealth-building tool available to the average investor. By understanding the 2026 limits—$7,500 for those under 50, and $8,600 for those 50 and older—you can build a strategic plan to maximize your tax-free growth.

Remember, you do not have to hit the maximum limit to be successful. The most important action you can take is simply to start. Open the account, automate your monthly contributions, invest the cash in low-cost index funds, and let time and compound interest do the heavy lifting for your financial future.

Retirement Planning Resources

Roth IRA rules change periodically as the IRS adjusts contribution and income limits for inflation. The following resources can help you verify current limits, understand retirement account rules, and make informed long-term investing decisions.

- Internal Revenue Service (IRS) – Review the official Roth IRA contribution limits, income eligibility rules, catch-up contributions, and retirement account regulations.

- IRS Publication 590-A – Official guidance covering IRA contribution rules, eligibility requirements, and annual contribution limits.

- IRS Publication 590-B – Learn about Roth IRA withdrawals, distributions, conversions, and inherited IRA rules.

- Investor.gov (U.S. Securities and Exchange Commission) – Educational resources explaining long-term investing, diversification, compound growth, and retirement planning fundamentals.

- FINRA Investor Education Foundation – Explore retirement investing concepts, investment risks, and practical guidance for building long-term wealth.

- Consumer Financial Protection Bureau (CFPB) – Access educational resources on retirement planning, budgeting, and developing healthy long-term financial habits.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.