401(k) vs IRA: Which Should You Fund First?

When deciding between a 401(k) vs IRA, making the right choice can mean the difference between retiring early and working for an extra decade.

⚡ Quick Answer

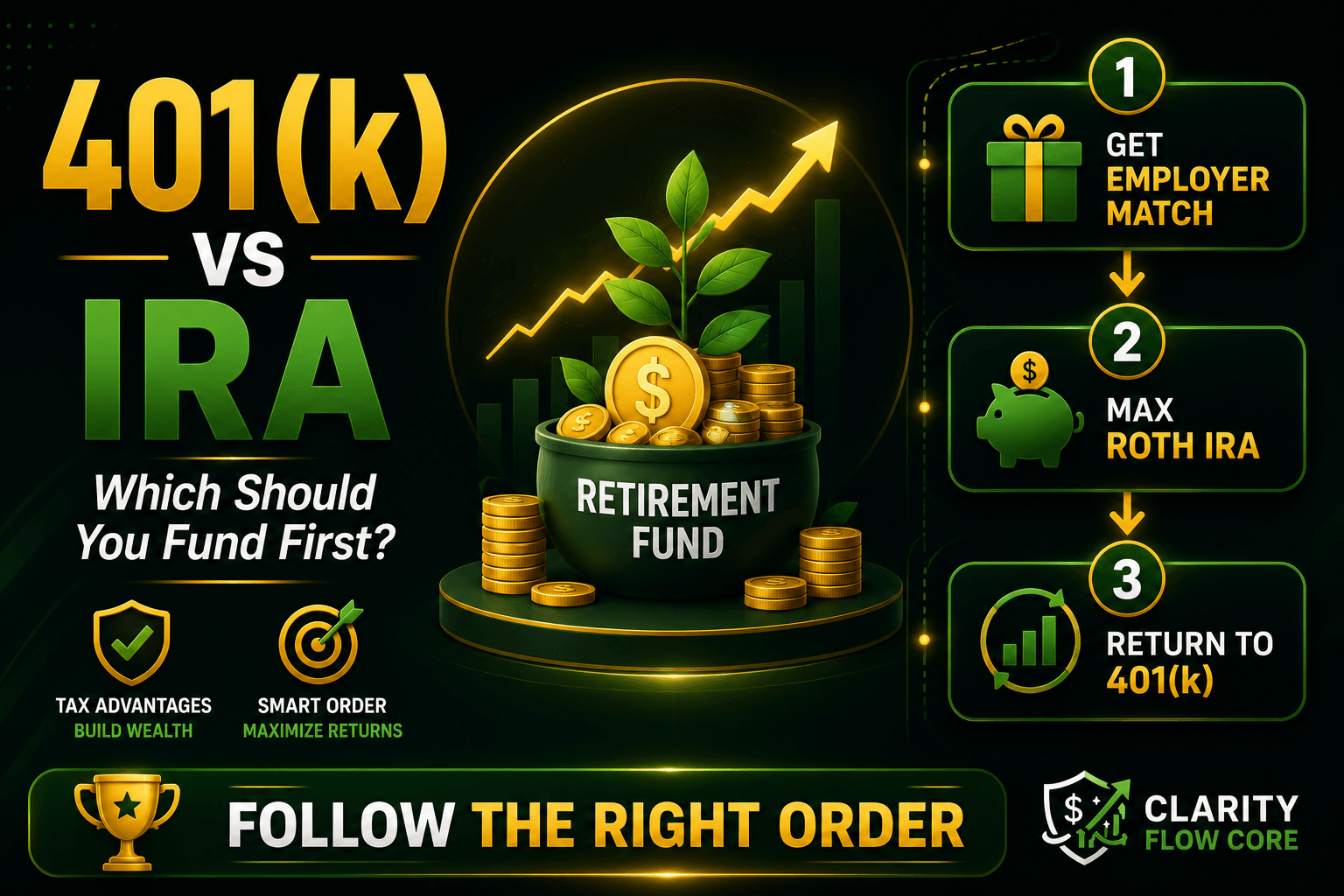

You should generally fund your accounts in this specific order: First, contribute exactly enough to your workplace 401(k) to get the full employer match (this is free money). Second, open a personal Roth IRA and max it out. Third, if you still have money left to save, go back to your 401(k) and increase your contributions.

You finally have some extra cash at the end of the month. You want to be responsible, so you decide it is time to start aggressively investing for your future. But when you sit down to allocate your budget, you hit a wall.

Should you log into your payroll portal and bump up your 401(k) contribution? Or should you go to a brokerage firm and open an Individual Retirement Account (IRA) on your own?

If you ask your coworkers, they will swear by the 401(k). If you ask independent financial advisors, they will almost always steer you toward the IRA. The truth is, they are both right. Both the 401(k) and the IRA are massive, legally protected tax shelters designed to help you build wealth.

However, they operate with different rules, different fees, and different investment options. Funding the wrong one at the wrong time will not bankrupt you, but it could cost you thousands of dollars in lost employer matches or unnecessary mutual fund fees over the next thirty years.

In this guide, we are going to break down the exact differences between a 401(k) and an IRA, compare the updated 2026 contribution limits, and give you the ultimate, step-by-step “Order of Operations” so you know exactly where to put your very first dollar—and your very last.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement plan. It gets its name from subsection 401(k) of the Internal Revenue Code. You cannot open a 401(k) on your own as an employee; your company has to offer it as part of your benefits package.

When you enroll in a 401(k), you tell your employer to automatically deduct a specific percentage of your salary from your paycheck and deposit it directly into your retirement account.

The Massive Benefit: The Employer Match

The absolute best feature of a 401(k) is the employer match. To encourage you to save, many companies will contribute their own money into your account based on how much you contribute.

For example, a company might offer a “100% match up to 5% of your salary.” If you make $80,000 a year and contribute 5% ($4,000), your employer will literally hand you another $4,000 and deposit it into your account. That is a 100% guaranteed return on your investment the second the money hits the account.

The Downside: Limited Choices and Higher Fees

Because your employer sets up the 401(k) through a specific provider (like Fidelity, Vanguard, or Empower), you are trapped inside their specific ecosystem.

You cannot buy individual stocks or choose from the thousands of mutual funds available on the open market. You are restricted to a small menu of funds chosen by your company’s HR department. Frequently, these limited options carry high administrative fees or high expense ratios, which slowly eat away at your compounding growth over time.

What is an IRA?

An IRA is an Individual Retirement Account (though the IRS technically calls it an Individual Retirement Arrangement). Unlike a 401(k), an IRA has absolutely nothing to do with your employer. You open it yourself at the brokerage firm of your choice, and you fund it by manually transferring money from your personal bank account.

The Massive Benefit: Total Control and Zero Fees

Because you open the IRA yourself, you have absolute freedom. You can open an account at a massive, low-cost broker and buy virtually any asset in the world—index funds, mutual funds, ETFs, target-date funds, or individual company stocks.

More importantly, because you are shopping on the open market, you can find highly diversified index funds with expense ratios near 0%. Over a thirty-year timeline, avoiding the 1% fees often found in a 401(k) can easily save you tens of thousands of dollars.

The Downside: No Free Money and Strict Limits

No one matches your IRA contributions. Every dollar in the account has to come out of your own pocket. Furthermore, the IRS places very strict, relatively low annual limits on how much cash you are legally allowed to put into an IRA each year.

If you are completely new to IRAs, you need to know there are two distinct types: Traditional and Roth. Before you open one, we highly recommend reading our guide on Traditional IRA vs Roth IRA: Which Is Better for Beginners?

2026 Contribution Limits: 401(k) vs IRA

Before you decide where to put your money, you must understand exactly how much the government legally allows you to save. The IRS adjusts these limits regularly for inflation.

Here are the official 2026 limits for both accounts:

| Feature | Workplace 401(k) Limit (2026) | Personal IRA Limit (2026) |

| Standard Contribution Limit | $24,500 | $7,500 |

| Age 50+ Catch-Up Limit | Additional $8,000 (Total $32,500) | Additional $1,100 (Total $8,600) |

| Age 60-63 Super Catch-Up | Additional $11,250 (Total $35,750) | Not Applicable |

| Combined Maximum (with Employer Match) | $72,000 | $7,500 (or $8,600 if 50+) |

Notice a major difference: The 401(k) limit is massive. You can shelter a huge percentage of your income inside a 401(k), while the IRA limit is capped much lower.

(Note: Under the SECURE 2.0 Act rules kicking in for 2026, if you make over $145,000 and you are 50 or older, you are legally required to make your 401(k) catch-up contributions as after-tax Roth contributions. You can no longer take a pre-tax deduction for the catch-up amount.)

The Ultimate Order of Operations

Now that you know the rules, how do you actually allocate your paycheck? Do not guess. Do not split your money 50/50. Follow this highly optimized, three-step financial strategy used by almost all professional wealth managers.

Step 1: Fund the 401(k) Just Enough to Get the Match

Your first goal is to capture 100% of the free money your employer offers.

If your company matches your contributions up to 5%, you log into your portal and set your contribution rate to exactly 5%. Do not contribute 6% yet. Do not contribute 4%. Hit the exact ceiling of the match.

Passing up an employer match is the mathematical equivalent of turning down a pay raise. If you make $60,000 a year and your employer offers a 5% match, they are offering to give you $3,000 a year for free. If you prioritize an IRA first, you permanently lose that $3,000.

Step 2: Max Out Your Personal Roth IRA

Once you have secured your match, stop contributing to the 401(k). Redirect all of your extra monthly retirement savings into a personal Roth IRA until you hit the $7,500 maximum limit for 2026.

Why pivot away from the 401(k)? Because your personal IRA gives you better options and lower fees.

Instead of being trapped in your company’s expensive mutual funds, you can use your IRA to buy a broadly diversified S&P 500 Index Fund with an expense ratio of 0.03%.

Additionally, the Roth IRA has a massive superpower: all of your investments grow completely tax-free. Because you fund the account with money that has already been taxed, the IRS allows you to pull the entire balance out in retirement without paying a single penny in taxes. Even better, if an absolute disaster strikes, you can withdraw your contributions (but not your growth) from a Roth IRA at any time without a penalty.

To fully understand the income restrictions on this account, check our breakdown of the Roth IRA Contribution Limits and Rules for 2026.

Step 3: Return to the 401(k)

What happens if you successfully capture your employer match, you max out your $7,500 Roth IRA, and you still have money left over in your budget that you want to invest?

Now, you return to your workplace 401(k). Because you have exhausted your high-quality, low-cost IRA space, the 401(k) becomes the next best place to legally shield your money from the IRS. You can continue bumping up your payroll contributions all the way until you hit the massive $24,500 limit.

If you are not sure how much you should be saving in total across both of these accounts, read our guide on How Much Should You Save for Retirement Each Month? to calculate your exact percentage.

When to Break the Rules (The Exceptions)

Personal finance is incredibly nuanced. While the “Match -> IRA -> 401(k)” sequence is perfect for 90% of beginners, there are a few specific scenarios where you should break the rules and alter your strategy.

Exception 1: You Have Zero Employer Match

If your company offers a 401(k) but refuses to match your contributions, Step 1 disappears entirely. You are getting zero free money. In this scenario, you should bypass the 401(k) completely and fund your personal IRA first. Once you max out the IRA, you can go back and start funding the unmatched 401(k) just for the tax benefits.

Exception 2: You Are a High-Income Earner Trying to Lower Your Taxes Today

If you are currently sitting in the 32% or 35% tax bracket, you are paying a fortune to the IRS every year. While a Roth IRA is fantastic for tax-free money in retirement, it does not give you a tax deduction today.

If you make a massive salary, you might want to skip the IRA entirely and aggressively max out your Traditional 401(k). By putting $24,500 into a pre-tax 401(k), you legally lower your taxable income by $24,500 this year, saving you thousands of dollars in immediate income taxes.

Exception 3: Your 401(k) Has Incredible Institutional Funds

Sometimes, large corporations offer 401(k) plans with access to “Institutional Class” mutual funds. These are exclusive funds with fees so incredibly low that regular retail investors cannot buy them in a standard IRA. If your company’s 401(k) has vastly superior, cheaper index funds than what you can buy on the open market, it makes mathematical sense to prioritize the 401(k) over the IRA.

Common Mistakes Beginners Make

Whether you choose the 401(k) or the IRA, the mechanics of investing are the same. Avoid these catastrophic wealth-destroying mistakes.

Mistake 1: Not Knowing What Your Money is Doing

A 401(k) and an IRA are not investments; they are just protective baskets. If you put money into an IRA and never log in to buy actual assets, the money will sit in cash, earning basically nothing.

With a 401(k), your company will usually automatically invest your money into a Target Date Fund based on your age. However, you still need to log in, review the fees, and verify that the money isn’t just sitting in a default money market account. You must be actively aware of what you are buying.

Mistake 2: Investing While Drowning in Bad Debt

There is absolutely no point in trying to earn an 8% return in your retirement accounts if you are carrying $15,000 on a credit card charging you 26% interest. The math will always work against you.

If your employer offers a match, get the match. But pause all other investing until the credit cards are clear. Run your balances through our Free Credit Utilization Calculator & Recovery System to build an aggressive payoff strategy, or use the Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to see exactly how much of your paycheck is being stolen by banks.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationCalculate Your True Borrowing Power

Find out exactly how lenders view your financial health. Calculate your Debt-to-Income (DTI) ratio instantly to see if you are in the safe zone before applying for a mortgage, auto loan, or new credit card.

Analyze My DTI RatioMistake 3: Treating Retirement Accounts Like Piggy Banks

If you leave a job, you will often have the option to cash out your 401(k). Never do this.

If you pull money out of a traditional 401(k) before age 59 ½, the IRS will force you to pay income tax on the entire balance, plus a massive 10% early withdrawal penalty. Worse, you rob your future self of decades of compound interest. Always “roll over” your old 401(k) directly into a personal IRA to keep the tax shelter intact.

Your Step-by-Step Action Plan

Ready to optimize your paycheck and start building wealth? Follow this precise timeline.

- Secure Your Cash Foundation: Never invest money you need to survive. Run your living expenses through our Advanced Emergency Fund Analyzer and ensure you have 3 to 6 months of cash parked in a High-Yield Savings Account.

- Locate Your Match: Ask your HR department for the exact details of your 401(k) match. Find out the percentage required to capture every cent of free money.

- Adjust Your Payroll: Log into your company’s 401(k) provider and set your contribution rate to hit the match ceiling.

- Open Your IRA: Go to a low-cost, reputable broker (like Vanguard, Schwab, or Fidelity) and open a personal Roth IRA. Set up an automatic transfer from your checking account every time you get paid.

- Invest the Cash: Verify that your automated IRA deposits are automatically purchasing low-cost index funds.

- Project Your Freedom: Plug your combined 401(k) and IRA monthly contributions into our Financial Freedom Planner to see exactly what age you will cross the million-dollar threshold.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetMap Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanFrequently Asked Questions (FAQ)

Can I have a 401(k) and an IRA at the same time?

Yes. In fact, utilizing both accounts simultaneously is the best way to rapidly accelerate your wealth. The IRS limits are completely separate. Maxing out your 401(k) does not prevent you from maxing out an IRA, provided you meet the income requirements for a Roth IRA.

Should I use a Traditional 401(k) or a Roth 401(k)?

Many employers now offer a Roth 401(k) option. A Traditional 401(k) lowers your taxes today, but you pay taxes on the withdrawals in retirement. A Roth 401(k) offers no tax break today, but withdrawals in retirement are tax-free. If you are young and in a low tax bracket, the Roth option is generally vastly superior.

Does my employer match count toward my $24,500 limit?

No. The $24,500 limit for 2026 is strictly for your personal payroll deferrals. Your employer’s matching funds do not count against this limit. The combined maximum limit for both your contributions and your employer’s contributions is $72,000 for 2026.

What happens to my 401(k) if I quit or get fired?

The money is yours. Your employer cannot take back your vested contributions. You have three choices: leave it where it is (if the plan allows), roll it over into your new employer’s 401(k), or roll it over into your personal IRA. Rolling it into an IRA is usually the best choice because it gives you control and lowers your fees.

Are IRA fees really that much lower than 401(k) fees?

Usually, yes. A 401(k) has administrative costs required to run the plan for hundreds of employees, which are often passed down to you through higher expense ratios. A personal IRA at a discount broker has zero administrative fees, meaning you only pay the microscopic expense ratios of the index funds you choose to buy.

Conclusion

The 401(k) vs IRA debate does not need to paralyze your financial progress. They are both incredible tools, and you ultimately want to utilize both of them.

The secret to building wealth efficiently is simply managing the order of operations. Grab the free money from your employer first. Then, prioritize the low fees, high flexibility, and tax-free growth of your personal Roth IRA. By following this sequence, you optimize your tax situation, lower your Wall Street fees, and put compound interest on overdrive.

Do not wait for the perfect moment. Log into your payroll portal today, secure your match, and let gravity do the rest of the work.

References

- Internal Revenue Service (IRS): Official guidelines on 2026 401(k) contribution limits, IRA deduction rules, and SECURE 2.0 catch-up mandates.

- Consumer Financial Protection Bureau (CFPB): Educational resources on planning for retirement, managing employer-sponsored plans, and understanding expense ratios.

- Investor.gov (U.S. Securities and Exchange Commission): Free tools, compound interest calculators, and information regarding asset allocation and avoiding high-fee mutual funds.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on establishing baseline savings habits and emergency funds before entering the stock market.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.