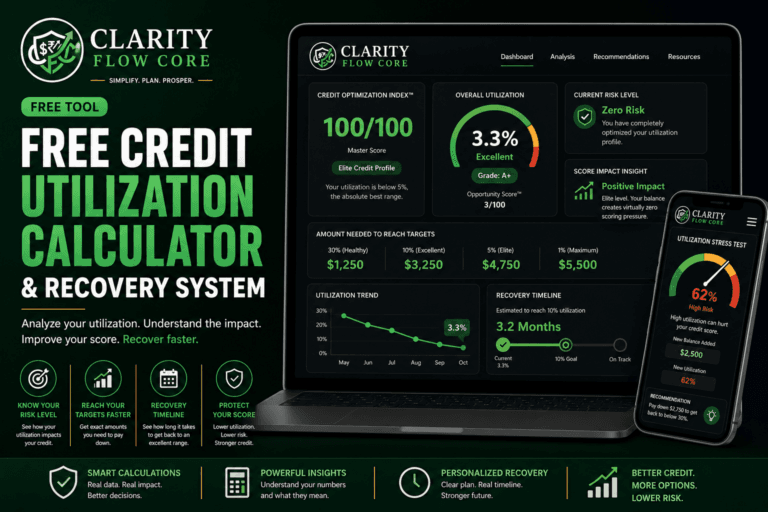

Credit Utilization Planner & Recovery System

Is your credit score dropping because of high balances? Stop guessing and start strategizing.

Use our free diagnostic tool below fix high credit utilization and simulate how future payments will impact your profile, and build a month-by-month recovery timeline to get your FICO score back into the elite tier.

What This Credit Utilization Recovery System Helps You Discover

Your credit utilization ratio is one of the fastest-changing parts of your credit score. A single large purchase can temporarily increase utilization and lower your score, while a strategic payment can often recover lost points within a single reporting cycle.

This calculator helps you:

- Calculate your current utilization ratio

- Identify how many points may be at risk

- Estimate target balances for optimal scoring

- Create a realistic payoff strategy

- Build a month-by-month utilization recovery plan

Whether you’re preparing for a mortgage, applying for a new credit card, or simply trying to improve your financial profile, understanding utilization is one of the fastest ways to improve your credit health.

Who Should Use This Credit Utilization Planner & Recovery System?

This tool is designed for anyone who wants to improve their credit profile, qualify for better loan terms, or understand why their credit score recently changed.

It can be especially useful if you:

- Recently noticed a sudden drop in your credit score

- Are preparing to apply for a mortgage or auto loan

- Want to improve your approval odds for a new credit card

- Carry balances across multiple credit cards

- Are actively rebuilding your credit after past mistakes

- Want to understand how utilization affects your FICO score

Even small changes in utilization can have a significant impact on credit scoring models, making this one of the fastest areas to improve.

How to Fix High Credit Utilization (The Complete Guide)

If you have ever logged into your banking app, checked your credit score, and felt your stomach drop because it suddenly plummeted 30 or 40 points—even though you have never missed a payment—you are not alone.

For most young adults and beginners, this is a terrifying moment. You immediately assume your identity was stolen or a bill went to collections. But in 99% of cases, it is actually a silent metric called credit utilization.

The good news? Unlike a missed payment or a bankruptcy, a credit utilization penalty is completely temporary. Your credit score doesn’t have a long-term memory for this. Once you understand how the algorithm works, you can recover those lost points in as little as 30 days.

Here is the honest, stress-free guide to understanding credit utilization, why the system penalizes you, and exactly how to fix high credit utilization to get your FICO score back on track.

The Real Problem: What Is Credit Utilization?

At its core, credit utilization is a very simple math equation: it is the percentage of your total available credit that you are currently using.

If you have a credit card with a $1,000 limit, and your current balance is $400, your credit utilization is 40%.

To the credit bureaus (Experian, Equifax, and TransUnion), this number is a measure of desperation. If you are only using 5% of your available credit, you look like a responsible borrower who doesn’t need the bank’s money. If you are using 85% of your available credit, the algorithm assumes you are in a financial crisis and relying on debt just to survive. To protect themselves, the banks instantly drop your score.

In fact, credit utilization makes up 30% of your total FICO score. It is the second most important factor behind your payment history.

Not sure how credit utilization compares to other credit score factors? Read our guide: Credit Utilization vs Payment History: Which Matters More?

You can also learn exactly how much utilization affects your score in: How Much Does Credit Utilization Affect Credit Score?

Why It Happens (Even When You Pay in Full)

This is the biggest source of frustration for beginners: you can get penalized for high credit utilization even if you pay your card off in full every single month.

How is that possible? It comes down to a timing loophole.

Credit card companies only report your balance to the credit bureaus once a month. This usually happens on your Statement Closing Date, which is typically three weeks before your actual bill is due.

Imagine you have a $2,000 credit limit. You buy a $1,500 laptop on the 10th of the month. On the 15th, your bank takes a snapshot of your account and reports a $1,500 balance to the credit bureaus. Your utilization is now reported at 75%. Your credit score tanks. A week later, you get paid and pay off the entire $1,500 balance so you don’t owe any interest.

You did the right thing financially, but because of when the bank took the snapshot, the algorithm thinks you are maxed out.

Common Utilization Mistakes That Tank Your Score

Beyond the timing loophole, here are three incredibly common mistakes people make that accidentally spike their utilization.

Mistake 1: Maxing Out One Single Card

The credit algorithm looks at two things: your overall utilization (all your balances divided by all your limits) and your per-card utilization.

If you have three credit cards with zero balances, but one card is completely maxed out, your score will still drop. Lenders view a single maxed-out card as a massive red flag. You cannot hide a maxed-out card behind your other healthy accounts.

Mistake 2: Closing an Old Starter Card

Let’s say you finally upgraded to a premium travel rewards card, so you decide to close the basic $1,000 limit starter card you got in college because you never use it anymore.

When you close that old account, that $1,000 limit vanishes from your credit profile. Your total available credit shrinks, which means your overall utilization percentage instantly spikes—even if your actual spending hasn’t changed. Always keep old, no-annual-fee cards open. Just put a small $5 subscription on them and set them to autopay.

Mistake 3: Believing the “30% Rule” is the Finish Line

Every financial blog on the internet repeats the same advice: “Keep your credit utilization below 30%.”

While 30% is a great safety boundary to prevent your score from dropping, it is not the goal. 30% is just “average.” If you want to achieve an elite credit score (750+), you need to push your utilization below 10%, and ideally between 1% and 5%.

Many people are surprised to learn that the popular “30% utilization rule” is often misunderstood. Learn more in: The 30% Credit Utilization Myth: What Actually Matters?

Practical Solutions: How to Fix High Credit Utilization

If your score is currently suffering because of high balances, here is your practical, step-by-step action plan to fix it.

1. The Mid-Cycle Payoff Hack

If you are someone who pays their balance in full every month but still suffers from high reported utilization, you just need to beat the snapshot.

Find out exactly what day your Statement Closing Date is (you can find this on your PDF statement or in your banking app). Then, log in and pay your current balance down to almost zero two days before that date. When the bank takes their snapshot, they will report a tiny balance, your utilization will register at 1%, and your score will instantly benefit.

2. Request a Credit Limit Increase (CLI)

If you can’t lower the balance (the top number in the math equation), you can lower your utilization by increasing your total limit (the bottom number).

Log into your credit card app and look for an option to “Request a Credit Limit Increase.” Many banks allow you to request this via a “soft pull,” meaning it won’t hurt your credit score to ask. If they bump your limit from $2,000 to $4,000, your utilization percentage instantly gets cut in half, without you paying a single dime.

If you’re considering this strategy, make sure you understand how credit limit increases affect your overall credit profile and approval odds.

(Warning: If you are currently struggling with overspending, do not do this. More credit can be a dangerous trap if you rely on credit cards to cover gaps in your income).

3. Deploy the Debt Avalanche

If you are carrying balances across multiple cards and paying expensive interest, you need a mathematical approach. Focus all of your extra cash on the card that is closest to being maxed out, or the one with the highest interest rate. Pay the minimums on everything else. Once that highest card is brought down to a healthy level, roll those payments into the next one.

If you’re comparing payoff strategies, you may also want to review the differences between the Debt Avalanche and Debt Snowball methods before creating your repayment plan.

Improve Your Credit Utilization: Recommended Next Steps

High credit utilization is one of the fastest ways to lose credit score points, but it is also one of the easiest factors to improve. If you’re actively working on rebuilding your score, these guides can help.

Understand How Credit Utilization Works

- The 30% Credit Utilization Myth: What Actually Matters?

- How Much Does Credit Utilization Affect Credit Score?

- Credit Utilization vs Payment History: Which Matters More?

Improve Your Credit Score

- 10 Credit Score Mistakes That Can Cost You 100+ Points

- How to Build a Strong Credit Profile Without Paying a Dime in Interest

- How to Increase Your Credit Limit Without Hurting Your Credit Score

- What Credit Score Is Needed for Each Type of Credit Card?

Managing Credit Card Debt

- What Happens If You Missed a Credit Card Payment?

- What Happens If You Only Pay the Minimum on a Credit Card?

- Debt Consolidation vs Debt Settlement: Which Actually Saves More Money?

- I Can Only Afford the Minimum Payments — Now What?

Related Financial Tools

Use these tools together for a complete view of your financial health:

- Free Credit Score Simulator & Improvement Planner

- Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner

- Financial Freedom Planner

- Advanced Emergency Fund Analyzer

- Mortgage Affordability Calculator & Home Buying Planner

Many lenders evaluate credit score, debt-to-income ratio, savings reserves, and overall financial stability together. Using these tools as a complete financial planning system can help identify weaknesses before applying for major loans.

Frequently Asked Questions

Does credit utilization have a memory? Under the most common scoring models (like FICO 8), credit utilization has absolutely zero memory. If your utilization was at 90% last month and your score dropped 50 points, but you pay it down to 5% this month, your score will rebound almost immediately as soon as the new balance is reported. You are not permanently penalized for past high utilization.

Should I just carry a small balance to build my credit? Absolutely not. You do not need to pay the bank interest to build your credit. To optimize your score, you want your statement to show a small balance (to prove you use the card), but you should always pay that statement balance in full by the due date to avoid interest charges.

Will applying for a new credit card fix my utilization? Technically, yes. Opening a new card adds a new credit limit to your profile, which lowers your overall utilization percentage. However, applying for a new card triggers a “hard inquiry,” which will temporarily drop your score by a few points. Furthermore, if you are already struggling with high balances, adding a new card introduces the temptation to spend more, which can make the original problem much worse.

The Bottom Line

Credit utilization is one of the most misunderstood parts of credit scoring. Many borrowers assume they are doing everything right because they never miss a payment, only to discover that high reported balances are quietly damaging their score.

The good news is that utilization is highly responsive. Unlike late payments or collections, utilization can improve dramatically within a single reporting cycle. By lowering balances, timing payments strategically, and keeping utilization as low as possible, you can often recover lost points much faster than expected.

Use the Credit Utilization Recovery System above to identify problem areas, calculate your target utilization levels, and build a realistic recovery plan that helps move your credit score in the right direction.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.