Financial Freedom Planner

Are you tired of guessing when you will finally be out of debt? The journey to wealth building doesn’t start with picking the perfect stock—it starts with understanding your current financial foundation.

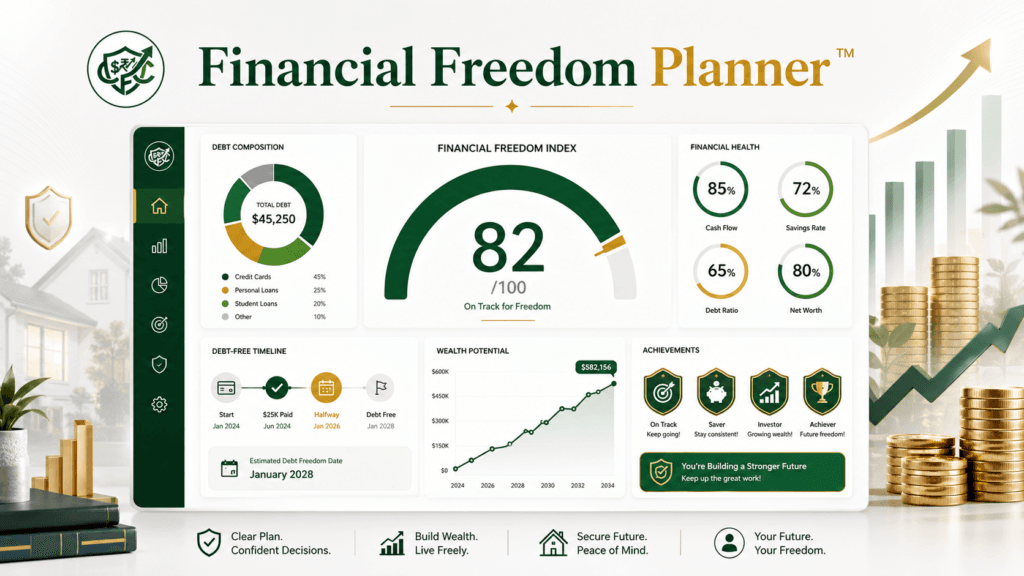

The Clarity Flow Core Financial Freedom Planner™ is more than just a standard debt payoff calculator. It is a complete financial diagnostic tool designed to give you a clear roadmap to financial independence. By analyzing your income, expenses, debt-to-income (DTI) ratio, and emergency fund, this dashboard will generate your personalized Financial Freedom Index™, calculate your exact debt-free date, and show you exactly what to prioritize next.

Enter your details below to unlock your custom financial dashboard. (Note: Your data is processed locally in your browser and is never stored or shared).

Already know your monthly debt obligations? Use our Debt-to-Income (DTI) Analyzer & Loan Readiness Planner to measure your borrowing capacity, or try the Advanced Emergency Fund Analyzer to determine how much cash you should keep in reserve before focusing on debt payoff.

What is the Financial Freedom Index™?

Your Financial Freedom Index™ is a comprehensive score from 0 to 100 that measures your overall financial health. Unlike a credit score, which only looks at how well you borrow money, your Freedom Index evaluates how well you manage your wealth.

The score is calculated using four vital metrics:

- Debt Health: Evaluates your Debt-to-Income (DTI) ratio to ensure monthly payments aren’t consuming your lifestyle.

- Savings Health: Measures your emergency fund against your essential living expenses.

- Cash Flow: Looks at the gap between what you earn and what you owe.

- Investment Readiness: Determines if your foundation is secure enough to begin allocating capital toward wealth-building vehicles like index funds or a Roth IRA.

Not sure how these financial metrics work together? Explore our guides on:

- Emergency Fund vs Paying Off Debt: Which Should You Do First?

- How Much Emergency Fund Do You Really Need?

- How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide

- The 50/30/20 Budget Rule Explained Simply

The 5 Stages of the Financial Roadmap

Personal finance is a step-by-step process. Skipping steps—like investing in the stock market while carrying high-interest credit card debt—can actually cost you money in the long run. Our planner automatically places you into one of five stages based on your current inputs:

- Financial Survival: You are living paycheck-to-paycheck with less than one month of living expenses saved. Top Priority: Build a starter emergency fund immediately to stop relying on credit cards for unexpected expenses.

- Debt Elimination: You have a small safety net, but consumer debt is draining your cash flow. Top Priority: Attack your high-interest balances using the Debt Avalanche or Debt Snowball method. If you’re trying to decide which payoff strategy is best, read:

- Financial Stability: You are free of high-interest consumer debt! Top Priority: Expand your emergency fund to cover 3 to 6 months of essential living expenses.

- Wealth Building: Your defensive financial foundation is fully built. Top Priority: Start making your money work for you by consistently investing in retirement accounts and the broader market.

- Financial Security: Your investments are compounding, and your passive income potential is growing. You are officially on the path to total financial independence.

Why Your Debt-Free Timeline Matters

One of the biggest hurdles to paying off debt is a lack of motivation. When you owe tens of thousands of dollars across credit cards, auto loans, and student loans, the finish line feels impossible to reach.

The Debt Freedom Timeline™ breaks your journey down into manageable milestones (25%, 50%, and 75% paid off). More importantly, the Recovery Simulator allows you to see exactly what happens if you add an extra $100 or $250 to your monthly payments. You won’t just see how many months you save—you will see the exact dollar amount of interest you keep in your pocket instead of handing it to the bank.

The Opportunity Cost of Debt (Wealth Potential Simulator)

What could you achieve if you didn’t have a monthly car payment or credit card bill?

Our Wealth Potential Simulator takes your current total monthly debt payments and projects what would happen if you invested that exact same amount into the market (assuming a historical 7% annual return) after becoming debt-free. Seeing your future wealth grow into hundreds of thousands of dollars is often the ultimate motivation needed to crush your current debt. Many people are surprised to discover that eliminating debt often creates a larger long-term financial impact than finding a slightly better investment. The combination of reduced interest costs and increased investing capacity can dramatically accelerate wealth building.

Build Your Financial Freedom Plan: Recommended Next Steps

The Financial Freedom Planner is designed to show where you are today, but the real value comes from taking action on the areas that need improvement. Use these guides to strengthen your financial foundation and accelerate your progress.

Budgeting & Cash Flow

- The 50/30/20 Budget Rule Explained Simply

- Best Beginner Budgeting Method for Irregular Income

- How to Budget as a Freelancer When Income Changes Every Month

- How Much Should You Keep in Checking vs Savings?

Emergency Funds & Savings

- Emergency Fund vs Paying Off Debt: Which Should You Do First?

- How Much Emergency Fund Do You Really Need?

- How to Build a $10,000 Emergency Fund Step-by-Step

- High-Yield Savings Account vs Traditional Savings Account

- High-Yield Savings Account vs CD: Which Is Better in 2026?

- Money Market Account vs High-Yield Savings Account

Debt Reduction & Credit Improvement

- Debt Avalanche vs Debt Snowball

- What Happens After You Pay Off All Your Debt?

- How Much Debt Is Too Much?

- Credit Utilization vs Payment History

- 10 Credit Score Mistakes That Can Cost You 100+ Points

Investing & Long-Term Wealth Building

- Roth IRA vs Traditional IRA: Which Is Better for Beginners?

- SEP IRA vs Solo 401(k): Which Retirement Plan Is Better?

- Real Estate Investing vs Index Funds

- How Much Should You Have Saved by Age 30, 40, and 50?

Related Financial Planning Tools

- Credit Utilization Recovery System

- Credit Score Simulator & Improvement Planner

- Debt-to-Income (DTI) Analyzer & Loan Readiness Planner

- Advanced Emergency Fund Analyzer

- Mortgage Affordability Calculator & Home Buying Planner

Frequently Asked Questions (FAQ)

What is a healthy Debt-to-Income (DTI) ratio? Lenders generally prefer a DTI ratio below 36%, with no more than 28% of that debt going toward a mortgage or rent. If your DTI climbs above 43%, you are considered in the “high risk” category for financial stress, making it difficult to qualify for new loans or handle financial emergencies.

Should I pay off debt or build an emergency fund first? This is a classic personal finance debate. The best approach is usually a hybrid one: save a “starter” emergency fund of 1 month of essential living expenses first. This prevents you from going further into debt if a car breaks down. Once that starter fund is secure, divert all extra cash flow toward eliminating your high-interest credit card debt.

Are student loans and mortgages considered “bad” debt? Not necessarily. Bad debt typically refers to high-interest consumer debt, like credit cards or personal loans used for depreciating assets. Mortgages and reasonable student loans are often considered “good” or “neutral” debt because they are tied to assets that generally appreciate in value or increase your earning potential. However, eliminating them still increases your monthly cash flow and ultimate financial freedom.

The Bottom Line

Financial freedom is rarely achieved through a single decision. It is built through hundreds of small choices made consistently over time: spending less than you earn, eliminating high-interest debt, building emergency savings, investing regularly, and protecting your financial foundation.

The Financial Freedom Planner helps bring all of those pieces together into a single roadmap. Instead of guessing what to do next, you can identify your biggest opportunities for improvement and focus on the actions that will have the greatest impact on your long-term financial future.

Use the planner above to calculate your Financial Freedom Index™, track your progress, and create a realistic plan that moves you closer to financial independence one step at a time.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.