Mortgage Affordability Calculator & Home Buying Planner

Buying a home is one of the largest financial decisions most people will make. Before you begin house hunting or applying for a mortgage, you need to know exactly what the math looks like.

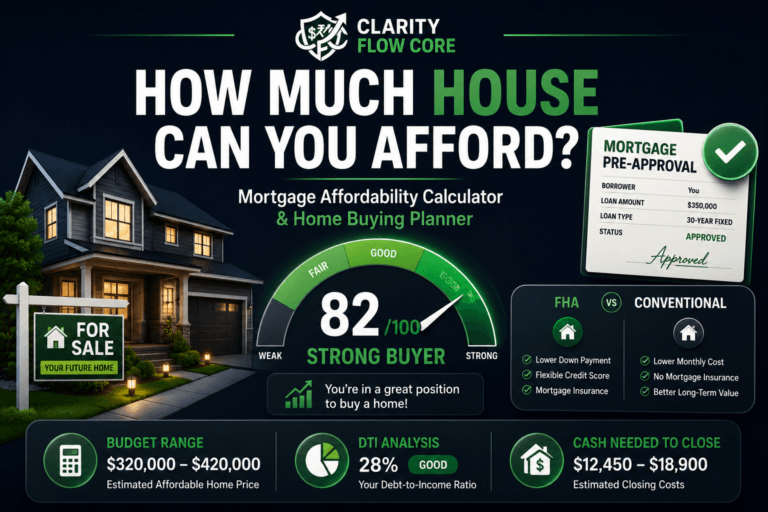

Wondering how much house you can realistically afford in today’s market? Use our Mortgage Affordability Calculator to estimate your true home buying budget, projected monthly mortgage payment, debt-to-income ratio (DTI), loan readiness, and the actual cash you will need to close the deal. Simply enter your income, current debts, savings, and down payment information to receive a personalized affordability report and an actionable financial plan.

Use the interactive calculator below to get started.

Our mortgage affordability calculator is designed to help first-time buyers and experienced homeowners evaluate affordability before applying for a mortgage.

What This Mortgage Affordability Calculator Helps You Discover Before Buying a Home

Many buyers focus only on whether they can qualify for a mortgage. The more important question is whether the home remains affordable after accounting for taxes, insurance, maintenance, debt obligations, and emergency savings.

This calculator helps you estimate a realistic home buying budget, evaluate your debt-to-income ratio, compare loan readiness scenarios, estimate cash needed to close, and identify potential financial risks before you begin shopping for a home.

Understanding Your Mortgage Affordability Calculator Results

Once you enter your numbers, our calculator provides a comprehensive breakdown of your home buying readiness. Here is what your personalized metrics mean:

Home Buying Readiness Score Your readiness score provides an immediate snapshot of how prepared you are to purchase a home. It calculates your overall financial health based on factors such as your gross income, existing debt levels, available savings, down payment size, projected housing costs, and your post-purchase financial reserves.

Approval Outlook The approval outlook estimates how competitive your financial profile may be when applying for a mortgage. While not a guarantee of approval, it can help you understand whether you may be a strong candidate based on common lending factors or if additional financial preparation may be beneficial before you approach a lender.

Debt-to-Income Ratio (DTI) Your DTI compares your total monthly debt obligations (including your new estimated mortgage) to your gross monthly income. Many lenders consider this ratio an important factor when evaluating your borrowing capacity. Lower DTI ratios generally provide more flexibility. If your DTI is hovering near the danger zone, use our Debt-to-Income Analyzer & Loan Readiness Planner to map out a strategy to lower it.

FHA vs Conventional Loans Your report includes a side-by-side comparison of FHA and Conventional mortgage readiness. FHA loans often offer more flexible qualification requirements and lower credit score minimums, while Conventional loans may provide long-term savings for borrowers with stronger financial profiles. If you are unsure which path to take, read our guide on FHA vs Conventional Loans: Which Mortgage is Better for You?.

Cash Needed to Close Buying a home requires vastly more cash than just a down payment. Your report estimates your hidden additional costs, such as closing expenses and lender fees, moving costs, and required cash buffers so you can better prepare for the full financial commitment of homeownership while maintaining an appropriate financial cushion after closing.

Common Home Buying Mistakes

Many first-time buyers focus entirely on the maximum amount a lender is willing to approve. Unfortunately, loan approval and affordability are not the same thing.

One of the most common mistakes is purchasing a home that leaves little room for emergencies, maintenance costs, or future financial goals. Homeownership often includes expenses that renters do not face, such as repairs, property taxes, insurance increases, and replacement of major systems.

Another common mistake is using nearly all available savings for a down payment. While a larger down payment can reduce monthly payments, it should not come at the expense of maintaining an adequate emergency fund after closing.

The strongest financial position is one where you can comfortably afford your home while still maintaining savings, investing for the future, and handling unexpected expenses without relying on debt.

How Lenders Determine Mortgage Affordability

Many first-time buyers assume mortgage approval is based solely on their income. In reality, lenders evaluate several financial factors simultaneously when determining how much house you can afford.

The first factor is your debt-to-income ratio (DTI). This compares your monthly debt obligations to your gross monthly income. A lower DTI generally signals that you have sufficient cash flow available to handle a mortgage payment comfortably.

Credit history is another major consideration. Borrowers with stronger credit profiles often qualify for lower interest rates, which can significantly reduce monthly payments and increase purchasing power. Even a small difference in mortgage rates can translate into thousands of dollars in savings over the life of a loan.

Lenders also review your available cash reserves. Having money left after closing demonstrates financial stability and helps reassure lenders that you can continue making payments if unexpected expenses arise. This is one reason many financial experts recommend maintaining a fully funded emergency fund before purchasing a home.

Employment stability also plays a role. Consistent income and a reliable work history generally strengthen a mortgage application. Self-employed borrowers and individuals with variable income may face additional documentation requirements during underwriting.

Finally, lenders evaluate the overall risk of the loan, including the size of your down payment, the type of property being purchased, and the loan program being used. Understanding these factors before applying can help you identify potential weaknesses and improve your approval odds.

The goal is not simply to qualify for the largest mortgage possible. The goal is to purchase a home that supports your long-term financial health while leaving room for savings, investing, and unexpected expenses.

Before choosing a price range, it’s worth understanding how much of your monthly income should realistically be dedicated to housing. Read How Much of Your Income Should Go Toward Housing Costs? to learn how financial professionals determine a sustainable housing budget.

Tips to Improve Your Home Buying Budget

If your calculator results show room for improvement, do not get discouraged. The math simply shows you what to focus on next. Consider taking these specific steps:

- Reduce Existing Debt: High minimum payments on credit cards or auto loans severely limit the size of the mortgage you can qualify for. Eliminating a $300/month car payment can drastically increase your home buying power.

- Increase Your Down Payment: Saving a larger down payment reduces your total loan amount, lowers your monthly payment, and can potentially eliminate the need for costly Private Mortgage Insurance (PMI).

- Build Dedicated Emergency Reserves: Lenders want to see that you have cash left over after closing day. Ensure your personal safety net is fully funded by running your numbers through our Advanced Emergency Fund Analyzer.

- Improve Your Credit Profile: A higher credit score unlocks lower interest rates, saving you tens of thousands of dollars over a 30-year loan. See how different financial actions impact your score using our Credit Score Simulator & Improvement Planner.

- Shop Around for Rates: Do not accept the first mortgage offer you receive. Comparing multiple lenders can help you find highly competitive loan terms that lower your monthly burden.

Why Every Home Buyer Should Use a Mortgage Affordability Calculator

Many homebuyers focus only on the monthly mortgage payment, but true affordability includes property taxes, homeowners’ insurance, mortgage insurance, closing costs, and existing debt obligations. A mortgage affordability calculator helps you evaluate the complete financial picture before making one of the largest purchases of your life.

Understanding your affordability range early can help you set realistic expectations, compare loan options, and avoid financial strain after closing.

Prepare for Homeownership: Recommended Next Steps

Buying a home is about much more than qualifying for a mortgage. The strongest homebuyers prepare their credit profile, reduce unnecessary debt, build emergency reserves, and fully understand the costs of ownership before making an offer.

Use the guides below to strengthen your financial position and improve your long-term affordability.

Credit & Mortgage Readiness

- What Credit Score Do You Need to Buy a House in 2026?

- Minimum Credit Score Needed to Buy a House in 2026

- FHA Loan Requirements 2026: Everything You Need to Know

- FHA Loan vs USDA Loan vs Conventional Loan

- PMI Explained: When Mortgage Insurance Is Required

- What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline

Home Buying Costs

- How Much Down Payment Do You Really Need to Buy a House?

- Closing Costs Explained: What Home Buyers Actually Pay

- Property Taxes Explained for First-Time Home Buyers

- Rent vs Buy: Which Option Makes More Financial Sense?

Financial Planning Before Buying

- How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide

- Emergency Fund vs Paying Off Debt: Which Should You Do First?

- How Much Emergency Fund Do You Really Need?

- Financial Freedom Planner

- Credit Utilization vs Payment History: Which Matters More?

Related Financial Tools

- Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner

- Free Credit Score Simulator & Improvement Planner

- Free Credit Utilization Calculator & Recovery System

- Advanced Emergency Fund Analyzer

- Financial Freedom Planner

How Accurate Is This Mortgage Affordability Calculator?

This mortgage affordability calculator is designed to provide realistic estimates based on the financial information you enter. While no mortgage affordability calculator can guarantee lender approval, it can help you understand how income, debt, savings, down payments, and housing costs interact when determining your home buying budget. Using a mortgage affordability calculator early in the process can help prevent costly mistakes and improve financial preparedness.

Home Buying Planner FAQ

How much house can I actually afford? True affordability goes beyond simply getting approved for a loan. It depends on your income, monthly debts, available savings, down payment amount, interest rates, property taxes, and homeowners insurance costs. This calculator provides a realistic estimate so you do not accidentally become “house poor.”

What is a good debt-to-income ratio for a mortgage? While absolute maximums vary, most traditional lenders prefer your total debt-to-income ratio (including your new housing payment) to stay below 36% to 43%. A lower DTI ratio generally improves your affordability, lowers your risk, and provides significantly more financial flexibility in your monthly budget.

Is a 20% down payment required to buy a house? No. This is a common myth. Many first-time buyers purchase homes with 3% to 5% down using conventional loans, or 3.5% down using FHA programs. However, keep in mind that putting down less than 20% usually requires you to pay for mortgage insurance every month.

Does this calculator guarantee mortgage approval? No. The results generated here are estimates intended for educational and financial planning purposes only. Actual approval decisions depend heavily on strict lender guidelines, the official underwriting process, and a deep manual review of your complete financial profile.

Where can I learn more about the mortgage process?

- Understanding mortgage qualification requirements, affordability calculations, debt-to-income ratios, down payment options, and closing costs can help you make more informed home buying decisions. The guides linked throughout this page provide a strong foundation for first-time and repeat homebuyers alike.

- Consumer Financial Protection Bureau (CFPB)

- U.S. Department of Housing and Urban Development (HUD)

Disclaimer This calculator and the accompanying information are provided for educational and informational purposes only. Results are strictly estimates based on the unverified information you enter and should not be considered financial, legal, tax, or official lending advice. Mortgage approval, final loan terms, and eligibility requirements vary significantly by lender and individual circumstances. Always consult with qualified financial professionals and licensed mortgage lenders before making major financial decisions.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.