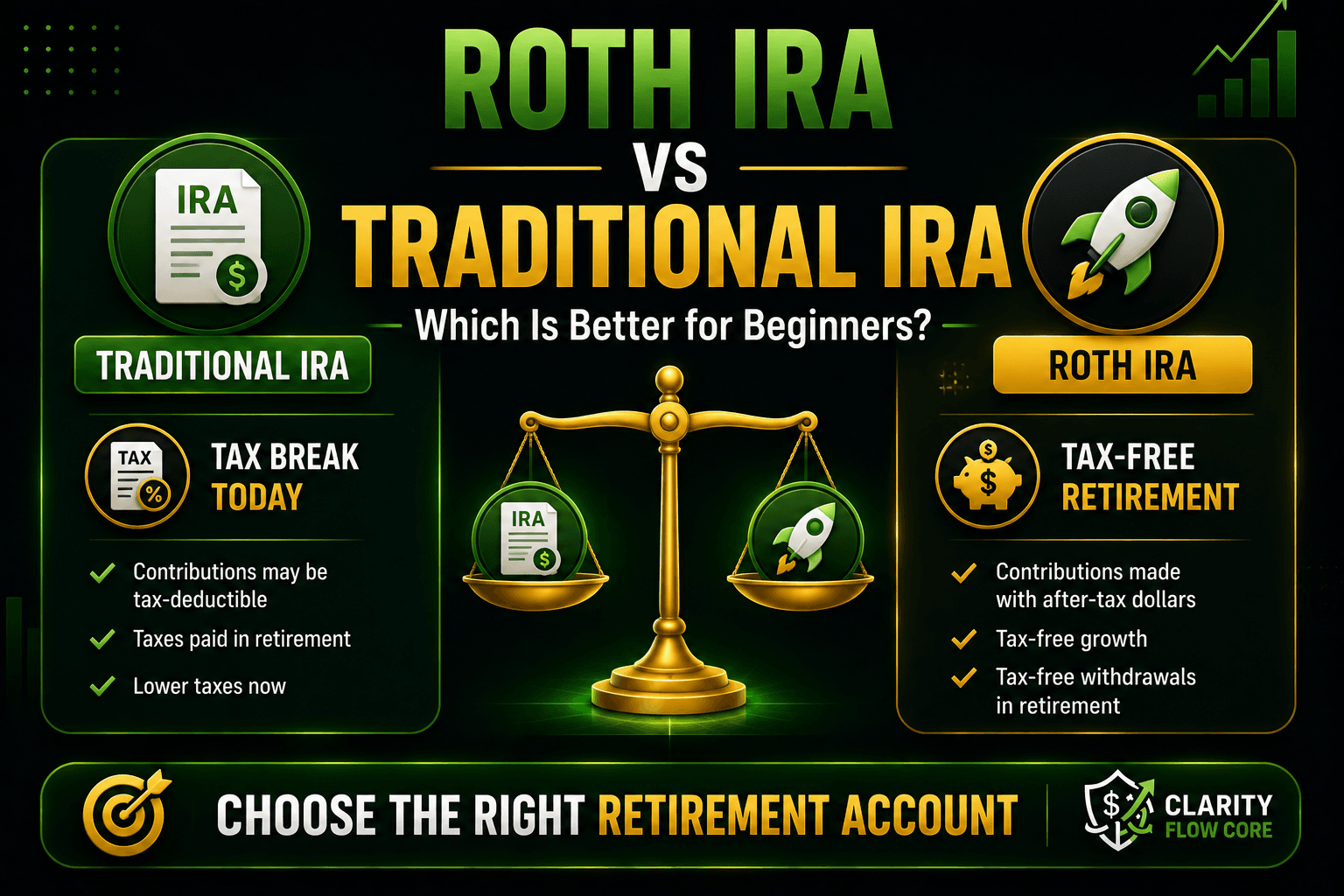

Traditional IRA vs Roth IRA: Which Is Better for Beginners?

When comparing a Traditional IRA vs Roth IRA, the right choice completely changes how much you pay the IRS.

⚡ Quick Answer

For most beginners, a Roth IRA is usually the better choice because your investments grow tax-free, and your withdrawals in retirement are 100% tax-free. Traditional IRAs generally make more sense for higher-income earners who need an immediate tax deduction today and expect to be in a lower tax bracket during retirement.

When you finally decide it is time to start investing for your future, you are immediately hit with a wall of confusing financial jargon. You just want to set up a basic retirement account, but right out of the gate, you are forced to make a choice: Traditional IRA or Roth IRA?

If you pick the wrong one, will you lose all your money? Will the IRS penalize you?

Take a deep breath. You are not going to lose your money, and simply opening an account is already a massive step in the right direction. Both of these accounts are designed to do the exact same thing: help you legally avoid paying taxes on the money you save for retirement. The only difference is when you get the tax break.

Do you want to save money on your taxes today? Or do you want to pay zero taxes when you pull the money out in thirty years?

In this guide, we are going to break down exactly how both IRAs work, compare them side-by-side without using confusing Wall Street terminology, and give you a simple framework to decide which account makes the most sense for your current financial situation.

What is an IRA? (The Absolute Basics)

Before we compare the Traditional and the Roth, we need to clarify what an IRA actually is.

IRA stands for Individual Retirement Arrangement (though most people call it an Individual Retirement Account). The biggest mistake beginners make is thinking that an IRA is an investment itself. It is not.

Think of an IRA as a special, tax-protected shopping basket. When you open the account and put money into it, that money is just sitting in the basket doing nothing. To actually grow your wealth, you have to look inside the basket and use that cash to buy investments—like stocks, bonds, or index funds.

If you are not sure what to actually put in your basket once it is open, we highly recommend reading our guide on Index Funds vs. Mutual Funds: What Beginners Should Know.

Because the government wants you to save for your own retirement, they give this specific “shopping basket” special tax superpowers. But because the government also loves rules, they force you to choose how you want your tax break applied: the Traditional way or the Roth way.

2026 IRA Contribution Limits

Before deciding which account is best for you, it is crucial to know exactly how much money the IRS legally allows you to put into these baskets each year. The government regularly adjusts these limits for inflation to keep up with the economy.

For 2026, the IRS has set the following contribution limits across all your IRAs combined:

| Age Bracket | Annual Contribution Limit (2026) |

| Under 50 | $7,500 |

| 50 and Older (Catch-Up) | $8,600 |

Note: You cannot put $7,500 into a Traditional IRA and another $7,500 into a Roth IRA in the same year. This limit is the absolute total you can contribute across all of your individual retirement accounts.

The Traditional IRA: Pay Taxes Later

The Traditional IRA is the classic retirement account. The entire strategy behind a Traditional IRA is to get a tax break right now, while you are working, and worry about the taxes later when you are retired.

How It Works

When you put money into a Traditional IRA, you get to deduct that amount from your income taxes for the year.

If you make $60,000 this year and you put $5,000 into a Traditional IRA, the IRS acts as if you only made $55,000. You pay income taxes on a smaller number, which means you either get a bigger tax refund in April or you owe the government less money.

Once the money is in the account, it grows completely tax-free. You can buy and sell investments inside the basket without paying capital gains taxes.

However, the IRS always gets their cut eventually. When you turn 59 ½ and start pulling the money out to pay for your retirement expenses, every dollar you withdraw is treated as regular income. You will pay ordinary income tax on it based on whatever tax bracket you fall into during retirement.

Who Should Pick a Traditional IRA?

A Traditional IRA makes the most mathematical sense if you are currently in a high tax bracket but expect to be in a much lower tax bracket when you retire.

Real-World Example: Let’s say David is 50 years old and at the peak of his career. He is making $150,000 a year and is sitting in a high tax bracket. Every dollar he earns is taxed heavily.

David contributes to a Traditional IRA because he wants the tax deduction today to lower his painful tax bill. When David retires at 65, he will stop working. His income will drop significantly because he will only be living off his investments and Social Security. When he pulls money out of his Traditional IRA in retirement, he will be in a much lower tax bracket, meaning he pays fewer taxes overall.

Traditional IRA May Be Better If:

✅ You have a high current income.

✅ You need immediate tax deductions today to lower your tax bill.

✅ You expect to be in a significantly lower tax bracket during retirement.

The Roth IRA: Pay Taxes Now, Never Again

The Roth IRA is the younger, incredibly popular sibling of the Traditional IRA. The strategy here is the exact opposite: you pay your taxes upfront today, so you never have to pay the IRS another dime for the rest of your life.

How It Works

When you contribute to a Roth IRA, you do not get a tax deduction for the year. You fund the account with “after-tax” dollars—meaning the money hitting your Roth IRA is the cash left over in your paycheck after taxes have already been taken out.

But here is the massive superpower of the Roth IRA: because you already paid taxes on the money going in, all the growth and all the withdrawals are 100% tax-free.

If you put $5,000 into a Roth IRA and over thirty years it grows to $50,000, you get to pull out the entire $50,000 in retirement without giving the IRS a single penny. It is completely legally shielded from future taxes.

If you want a deeper dive into why this specific account is a favorite among financial planners, check out our dedicated guide: Roth IRA for Beginners: How It Works and Why People Use One.

Who Should Pick a Roth IRA?

The Roth IRA is almost always the best choice for beginners, young professionals, and anyone currently in a lower tax bracket.

If you are in your 20s or 30s, you are likely making the lowest salary you will ever make in your career. That means you are currently in a low tax bracket. It makes perfect sense to pay taxes on your money right now while your rate is low, lock the money away, and let it grow tax-free for decades.

Real-World Example: Sarah is 24, just graduated college, and makes $45,000 a year at her first job. She is in a very low tax bracket. Sarah does not need a tax deduction today because she barely pays any income tax to begin with.

She puts $4,000 into her Roth IRA. By the time Sarah is 65, that $4,000 has compounded and grown into $60,000. Because she used a Roth, Sarah pays zero taxes on that massive pile of growth.

Roth IRA Is Usually Best If:

✅ You are under 40 or early in your career.

✅ You are currently in a lower tax bracket.

✅ You want 100% tax-free income in retirement.

✅ You want the flexibility to withdraw your contributions early without a penalty.

Traditional IRA vs Roth IRA: The Ultimate Side-by-Side Comparison

To make the decision as clear as possible, here is exactly how the two accounts stack up against each other.

| Feature | Traditional IRA | Roth IRA |

| Tax Break | Tax deduction today. | Tax-free withdrawals in retirement. |

| Funding Source | Pre-tax dollars. | After-tax dollars. |

| Taxes on Growth | Tax-deferred (you pay later). | Tax-free (you never pay). |

| Early Withdrawal Rules | 10% penalty + taxes if withdrawn before age 59 ½ (some exceptions apply). | You can withdraw your contributions (but not earnings) at any time, penalty-free and tax-free. |

| Required Minimum Distributions (RMDs) | Yes. At age 73, the IRS forces you to start pulling money out and paying taxes. | No. You can leave the money in the account until you die and pass it to your heirs tax-free. |

| Income Limits to Contribute | Anyone with earned income can contribute, but high earners might not get the tax deduction. | High earners are legally restricted from contributing directly. |

Understanding 2026 Roth Income Limits (Phase-Outs)

The government loves the Roth IRA, but they restrict the extremely wealthy from utilizing it natively. Because of this, the IRS enforces strict income limits. If you make above a certain threshold, your ability to contribute to a Roth IRA phases out and eventually drops to zero.

Here are the official 2026 Roth IRA Income Limits (based on your Modified Adjusted Gross Income, or MAGI):

- Single / Head of Household: Your ability to contribute begins phasing out at $153,000 and is entirely eliminated if you make $168,000 or more.

- Married Filing Jointly: Your ability to contribute phases out starting at $242,000 and is eliminated if you make $252,000 or more.

If you earn above these limits, you cannot legally contribute directly to a Roth IRA. However, a common workaround for high-income earners is the “Backdoor Roth IRA” strategy, which involves putting money into a Traditional IRA and immediately converting it to a Roth to bypass the income ceiling.

How to Choose Which IRA is Right for You

If you are still on the fence, ask yourself these three simple questions:

1. Do you think you will make more money in the future than you do today?

If the answer is yes—which it is for almost all beginners—go with the Roth IRA. Pay the taxes now while your income is low. If you are currently in your peak earning years and plan to retire soon, a Traditional IRA likely makes more sense.

2. Do you want flexibility in case of an absolute disaster?

The Roth IRA has a unique feature: because you already paid taxes on the money you put in, the IRS allows you to pull your contributions out at any time, for any reason, without a penalty. (You just cannot pull out the growth) .

While you should never treat your retirement account like a savings account, this flexibility makes the Roth IRA slightly safer for beginners who are terrified of locking their money away forever.

(Note: We always suggest having a separate, fully-funded cash safety net before investing. Run your numbers through our Advanced Emergency Fund Analyzer to see how much cash you need to keep out of the stock market.)

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings Target3. Are you a high earner?

The IRS places income limits on the Roth IRA. If you hit this limit, a Traditional IRA becomes your primary option. You can take advantage of the upfront tax deduction and avoid the hassle of backdoor conversion strategies if you prefer a simpler approach.

Common Mistakes Beginners Make With IRAs

No matter which account you choose, you need to avoid these massive financial traps.

Mistake 1: Opening the account but leaving the money in cash

As mentioned earlier, an IRA is just a basket. If you transfer $5,000 from your checking account into a Roth IRA and close your laptop, that money will just sit there in cash. It will not grow. You have to log into your brokerage account and actively use that $5,000 to purchase index funds, ETFs, or stocks.

Mistake 2: Investing while drowning in high-interest debt

There is no point in trying to earn an 8% return in your Roth IRA if you are currently paying 25% interest on a maxed-out credit card. The math will always work against you. If you are carrying high balances, pause your investing. Use our Free Credit Utilization Calculator & Recovery System to build a strategy to wipe out your credit card debt first. Once the bad debt is gone, funnel those monthly payments directly into your IRA.

Is High Credit Utilization Dragging Down Your Score?

Credit utilization accounts for 30% of your total credit score. Calculate your exact ratio across all your cards and generate a mathematical payoff plan to hit the safe zone and boost your score fast.

Calculate My UtilizationMistake 3: Treating the account like a piggy bank

Yes, the Roth IRA allows you to pull contributions out without a penalty. But every time you pull money out of your retirement account, you are robbing your future self of decades of compound interest. Only use this feature in an absolute, worst-case scenario emergency.

Your Step-by-Step Action Plan

Ready to start building wealth? Follow this exact checklist to get your retirement plan up and running this week.

- Fund Your Baseline Emergency Savings: Before you lock money away for age 60, make sure you have 3 to 6 months of living expenses sitting in a High-Yield Savings Account.

- Pick Your Account: If you are a beginner or a young professional, choose the Roth IRA. If you are a high earner looking for immediate tax relief, pick the Traditional IRA.

- Open the Account: Go to a reputable, low-cost brokerage firm like Fidelity, Vanguard, or Charles Schwab. Opening an IRA online takes less than ten minutes.

- Automate Your Contributions: Set up an automatic transfer from your checking account to your new IRA every time you get paid. If you aren’t sure how much you can afford to contribute, structure your budget using The 50/30/20 Budget Rule Explained Simply.

- Invest the Cash: Log in and buy broadly diversified, low-cost index funds or a Target Date Retirement Fund.

- Project Your Future: Want to see exactly what age you can retire based on your new IRA contributions? Plug your numbers into our Financial Freedom Planner to map out your long-term wealth trajectory.

Map Out Your Path to Financial Freedom

Stop winging your financial future. Use our free planner to set concrete goals, optimize your monthly savings rate, and calculate exactly when you will achieve total financial independence.

Build My Freedom PlanFrequently Asked Questions (FAQ)

Can I have both a Traditional and a Roth IRA?

Yes. You can open and contribute to both types of IRAs in the same year. However, the total amount you contribute across both accounts cannot exceed the annual IRS limit (which is $7,500 for people under 50 in 2026). You cannot put $7,500 in a Traditional and another $7,500 in a Roth in the same year.

Do I need an IRA if I already have a 401(k) at work?

Ideally, yes. A 401(k) is tied to your employer, while an IRA is controlled entirely by you. Most financial experts recommend contributing enough to your 401(k) to get the employer match (free money), and then funding a Roth IRA because IRAs typically offer better, lower-cost investment options than workplace 401(k) plans.

Can I withdraw my money before age 59 ½?

If you have a Traditional IRA, pulling money out early triggers a 10% IRS penalty plus you will owe income taxes on the withdrawal. If you have a Roth IRA, you can withdraw your contributions anytime without penalty, but pulling out the earnings early will trigger penalties and taxes. There are a few exceptions (like buying your first home or paying for qualified education expenses), but generally, you should leave the money alone.

What if I am a freelancer or have a side hustle?

If you are self-employed, you can still use Traditional and Roth IRAs. However, you also have access to special small-business retirement accounts that allow you to save vastly more money. Read our guide on SEP IRA vs Solo 401(k) for Freelancers to see if you qualify.

How do I report my IRA on my taxes?

If you use a Traditional IRA, you will enter your contributions on your tax return to claim your deduction. Your brokerage will send you a Form 5498. If you use a Roth IRA, you generally do not need to report your regular contributions on your tax return because you do not get a deduction for them.

Can my child open a Roth IRA?

Yes. If your child has earned income (like from a summer job, tutoring, or babysitting), you can open a Custodial Roth IRA for them. It operates with the same rules and benefits, allowing them to take advantage of compound interest from an incredibly young age. Just remember, they can only contribute up to the actual amount of money they earned that year.

Conclusion

Choosing between a Traditional and a Roth IRA does not need to paralyze you. If you are just starting out, the Roth IRA is almost always the clear winner. By paying your taxes today while your income is relatively low, you are setting yourself up for decades of tax-free growth and a massive, tax-free payday in retirement.

The most important step isn’t picking the perfect account—it is simply getting started. Open the account, set up a small automatic monthly transfer, buy a low-cost index fund, and let compound interest do the heavy lifting for the rest of your career. Your future self will thank you.

References

- Internal Revenue Service (IRS): Official guidelines on IRA contribution limits, deduction rules, and Roth phase-out limits.

- Consumer Financial Protection Bureau (CFPB): Educational resources on planning for retirement and understanding different types of investment accounts.

- Federal Deposit Insurance Corporation (FDIC): Recommendations on establishing baseline savings habits before entering the stock market.

- Investor.gov (U.S. Securities and Exchange Commission): Free tools and information regarding asset allocation, index funds, and compound interest.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.