7 Everyday Saving Habits That Can Make a Real Difference

When the cost of rent and groceries is constantly creeping up, clipping 50-cent coupons isn’t going to fix your cash flow. If you want to stop bleeding cash, you need to master proven everyday saving habits right now.

A few years ago, I reviewed my bank statements and realized dozens of small recurring expenses were quietly draining hundreds of dollars each month. None of them seemed significant individually, but together they were costing me more than my rent increase. I was losing money entirely by accident.

Most people genuinely want to save money, but they rely entirely on the wrong tool to do it: willpower. Willpower is a finite resource. If you have to actively make the decision to not buy a coffee, not order takeout, and not upgrade your phone every single day, you will eventually cave.

The secret to keeping your bank account growing isn’t about denying yourself every pleasure in life. It is about building automated systems, focusing on the massive expenses that actually move the needle, and establishing everyday saving habits that run effortlessly in the background.

Here is the operational breakdown of the most effective everyday saving habits to implement immediately, how the math actually plays out, and where frugality usually backfires.

⚡ Quick Answer

The most effective everyday saving habits rely on automation and minimizing friction, rather than daily willpower. By implementing the 24-hour rule for online shopping, unlinking saved credit cards, automating a “pay yourself first” split direct deposit, and aggressively negotiating the “Big Three” expenses (Housing, Food, and Transportation), you can systematically redirect hundreds of dollars back into your bank account each month.

The Psychology Behind Everyday Saving Habits

Before we look at spreadsheets, we have to fix the psychological leaks in your spending. Retailers and tech companies spend billions of dollars engineering their apps to make you part with your money as frictionlessly as possible. One-click checkout is the enemy of strong everyday saving habits.

To fight back, you have to intentionally introduce friction into your own life.

1. The 24-Hour Rule

This is the single most effective psychological boundary you can set. Whenever you are scrolling online and you see a non-essential item that you suddenly “must have,” you are not allowed to buy it right then.

Put it in your digital shopping cart and close the app. Force yourself to wait exactly 24 hours.

The sudden dopamine spike of seeing a shiny new object wears off. Your logical brain takes over from your emotional brain. Nine times out of ten, when you open that cart the next day, you will realize you don’t actually need the item, and you will delete it. You just saved yourself $100 by simply waiting.

2. Unlinking Your Credit Cards

If your credit card information is saved in your web browser, Amazon, Apple Pay, and DoorDash, you are making it too easy to spend money. Go into your browser settings and delete your saved cards.

Force yourself to physically stand up, walk to your wallet, pull out the card, and manually type in the 16-digit number every single time you want to buy something online. That tiny bit of physical friction is often the cornerstone of good everyday saving habits, making you pause and say, “Never mind, it isn’t worth the effort.”

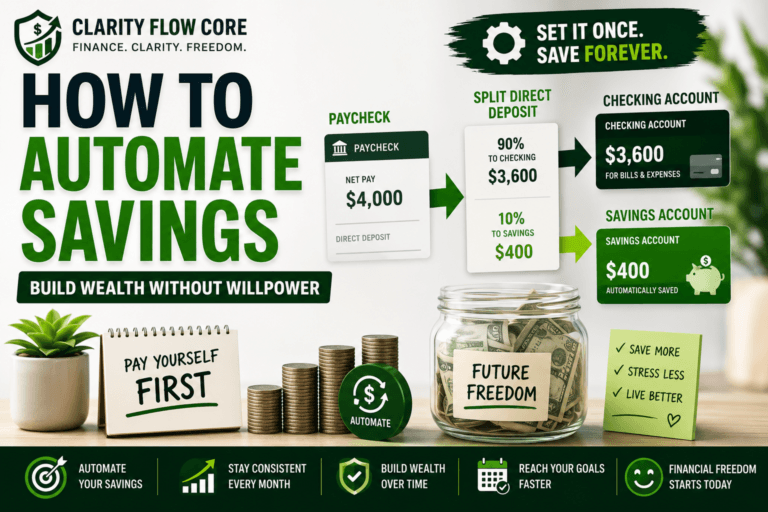

Automating Your Wealth: The “Pay Yourself First” Method

If you wait until the end of the month to save whatever cash happens to be left over, you will almost always save zero. Human nature dictates that we will expand our lifestyle to consume whatever resources are readily available in our checking account.

To build wealth, you must invert the formula. The foundation of reliable everyday saving habits is paying yourself first.

- Step 1: Separate Your Accounts. You cannot keep your savings in the exact same bank as your everyday checking account. If you log in to check your balance before buying groceries and see your $5,000 savings sitting right there, your brain subconsciously registers that you have plenty of money to spend. Open a high-yield account at a separate, online-only bank. (Not sure which account is best? Read HYSA vs. Money Market Account: What’s the Difference?). Do not download their app onto your phone. Make the money slightly annoying to access.

- Step 2: The Direct Deposit Hack. Go to your employer’s HR portal. Set up a split direct deposit. Route 10% to 20% of your gross income directly into that new HYSA, and let the remaining 80% go to your normal checking account to pay your bills. If you never see that 20% hit your primary account, you will never miss it.

Attacking the “Big Three” Expenses

Most personal finance advice yells at you for buying a $5 latte. But skipping your latte isn’t life-changing. Scaling your everyday saving habits means attacking the Big Three: Housing, Food, and Transportation.

According to Bureau of Labor Statistics (BLS) consumer spending data, housing, transportation, and food consistently represent the largest household spending categories for most Americans.

Here is exactly what happens to your cash flow when you optimize these three areas:

| Expense Category | Traditional Approach | Optimized Approach | Monthly Savings |

| Food (Delivery) | DoorDash 3x a week ($30/meal) | Cooking generic brands at home ($8/meal) | $264 saved |

| Transportation | Financing a brand new SUV | Buying a reliable 5-year-old sedan | $350 saved |

| Housing | Renewing lease with 8% hike | Negotiating rent or House Hacking | $150+ saved |

| Total Impact | — | — | $764+ per month |

3. Slashing Your Housing Costs

Housing is your biggest expense, which means it offers the biggest opportunity for savings.

- Negotiate Your Rent: Landlords do not want to lose good tenants. When your lease is up, research comparable apartments. Ask for a rent reduction or a free month to sign a new lease.

- House Hacking: Consider buying a duplex or a house with a rentable basement. The rent from your tenant can cover a massive portion of your mortgage. (Dive into the math in House Hacking Explained: Using an FHA Loan to Lower Housing Costs).

4. Hacking Your Food Budget

Food is the easiest category to accidentally overspend in because you make food choices three times a day.

- Kill the Delivery Apps: Delete UberEats and DoorDash. A $15 meal easily turns into $28 after service fees and tips.

- The “Cook Once, Eat Twice” Rule: Meal prepping on Sundays is exhausting. Instead, just double the recipe of whatever you are cooking for dinner. You immediately have lunch for the next day.

5. Rethinking Transportation

We have been conditioned to believe that we always need a massive car payment. We don’t.

- Buy Used: A brand-new car loses 20% of its value the second you drive it off the lot. Buy a reliable, 5-year-old Toyota or Honda. (And if you are worried about what happens after you finally pay a vehicle off, read Why Your Credit Score Dropped After Paying Off Your Car Loan).

- Shop Your Insurance: Car insurance companies slowly raise your rates every year. Spend 30 minutes getting quotes from three different competitors every six months.

Plugging the Micro-Leaks

Once the Big Three are under control, it is time to audit the slow drips. Ignoring micro-leaks destroys good everyday saving habits.

- 6. The Ruthless Subscription Audit: The subscription model is a brilliant business strategy, but it is toxic for your wallet. Print out your last two months of credit card statements. Take a red pen and circle every single recurring charge. If you have not used that service in the last 14 days, cancel it immediately.

- 7. Negotiate Your Bills: Internet and cell phone providers heavily overcharge their loyal, existing customers. Call your internet provider’s retention department. Tell them nicely that you are looking at a competitor offering a cheaper rate and ask if they can match it to keep your business.

The Biggest Saving Mistakes People Make

As you build your new habits, be careful not to fall into the common traps that derail beginners. Avoid these major saving mistakes:

- Saving Without a Budget: You cannot save money if you don’t know where it is going. You need a baseline framework like The 50/30/20 Budget Rule Explained Simply.

- Relying on Credit Cards for Emergencies: Savings should protect you from debt, not the other way around.

- Keeping Savings in a Checking Account: Your checking account earns zero interest. Unused cash needs to be moved to an HYSA.

- Trying to Cut Every Expense at Once: If you try to change 15 habits overnight, you will burn out.

- Ignoring Inflation: Leaving cash under your mattress guarantees you lose purchasing power over time.

When Everyday Saving Habits Backfire

Frugality is a highly effective tool, but it has sharp edges. If you push your everyday saving habits too far, the entire system breaks down. Here is exactly when this strategy backfires:

- Frugality Fatigue: If you cut out every single subscription, never eat at a restaurant, and refuse to buy a $4 coffee, you will eventually burn out. You will snap, walk into a mall, and blow $400 on clothes you don’t need just to feel something. Sustainable everyday saving habits allow for a small, guilt-free “fun money” budget.

- Tripping Over Dollars to Pick Up Pennies: Some people will spend two hours driving across town to three different grocery stores just to save $4 on chicken. Your time is valuable. If the operational effort to save the money vastly outweighs the actual dollar amount saved, you are doing it wrong.

- Ignoring Vital Maintenance: Skipping your bi-annual dental cleaning to save $150 will cost you $2,000 in root canals later. Delaying an oil change to save $60 will destroy a $4,000 engine. True everyday saving habits require you to spend money on preventative maintenance.

Where Should Your Savings Actually Go?

Now that you have freed up hundreds of dollars a month, what do you actually do with it? Leaving it in a checking account where it earns 0.01% interest means you are actively losing money to inflation. The end goal of everyday saving habits is to put your money to work.

If you’re ready to move your savings into an HYSA, How to Choose Your First High-Yield Savings Account explains what to look for before opening an account.

- Build the Emergency Fund: Your very first goal is to save 3 to 6 months of basic living expenses. This is your financial armor against a blown car transmission. (Calculate your exact number using Emergency Fund Basics: How Much Cash Should You Keep?).

- Crush High-Interest Debt: If you have credit card debt charging you 24% interest, attack it aggressively. Use the Debt Avalanche vs. Debt Snowball framework to pick your mathematical target.

- Invest the Rest: Once you are debt-free with a full emergency fund, your savings need to shift into investments. (Start with the basics by reading Index Funds vs. Mutual Funds: What Beginners Should Know).

Frequently Asked Questions (FAQs)

How much should I save each month?

A common starting goal is 10%–20% of your gross income, but any consistent amount is far better than saving nothing.

What is the easiest saving habit to start?

Automating your savings through a split direct deposit is often the simplest and most effective strategy because it requires zero ongoing willpower.

Should I save money or pay off debt first?

High-interest consumer debt (like credit cards) generally deserves priority because the interest rates will mathematically outpace any savings yield, though maintaining a small $1,000 baseline emergency fund is also critically important.

Is keeping money in a checking account a bad idea?

Checking accounts are highly useful for paying your monthly bills, but long-term savings typically grow faster and are safer from impulse purchases when held in high-yield savings accounts.

Your First Move Today

You do not need to overhaul your entire life by 5:00 PM today. Trying to implement twenty everyday saving habits at once is a guaranteed recipe for failure.

Start small. Tonight, log into your banking portal and set up an automatic transfer of just $50 to a separate savings account for every payday. Tomorrow, cancel just one streaming service. Scaling your everyday saving habits starts with one move.

Want to supercharge your progress and completely reset your baseline? Jump into our guide on How to Actually Finish a 30-Day No-Spend Challenge to detox your finances this month.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. Saving strategies, budgeting methods, and financial outcomes vary depending on personal income, expenses, debt obligations, and individual financial goals. Before making major financial decisions, consider consulting a qualified financial professional or advisor. Any financial products, services, or strategies mentioned may have different terms, risks, or eligibility requirements based on your personal circumstances.

Sources & References

This article was reviewed using publicly available information from consumer finance institutions, budgeting research, and behavioral finance resources.

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve Consumer Spending & Household Reports

- Bureau of Labor Statistics Consumer Expenditure Surveys

- Experian Personal Finance Education Center

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

4 Comments

Comments are closed.