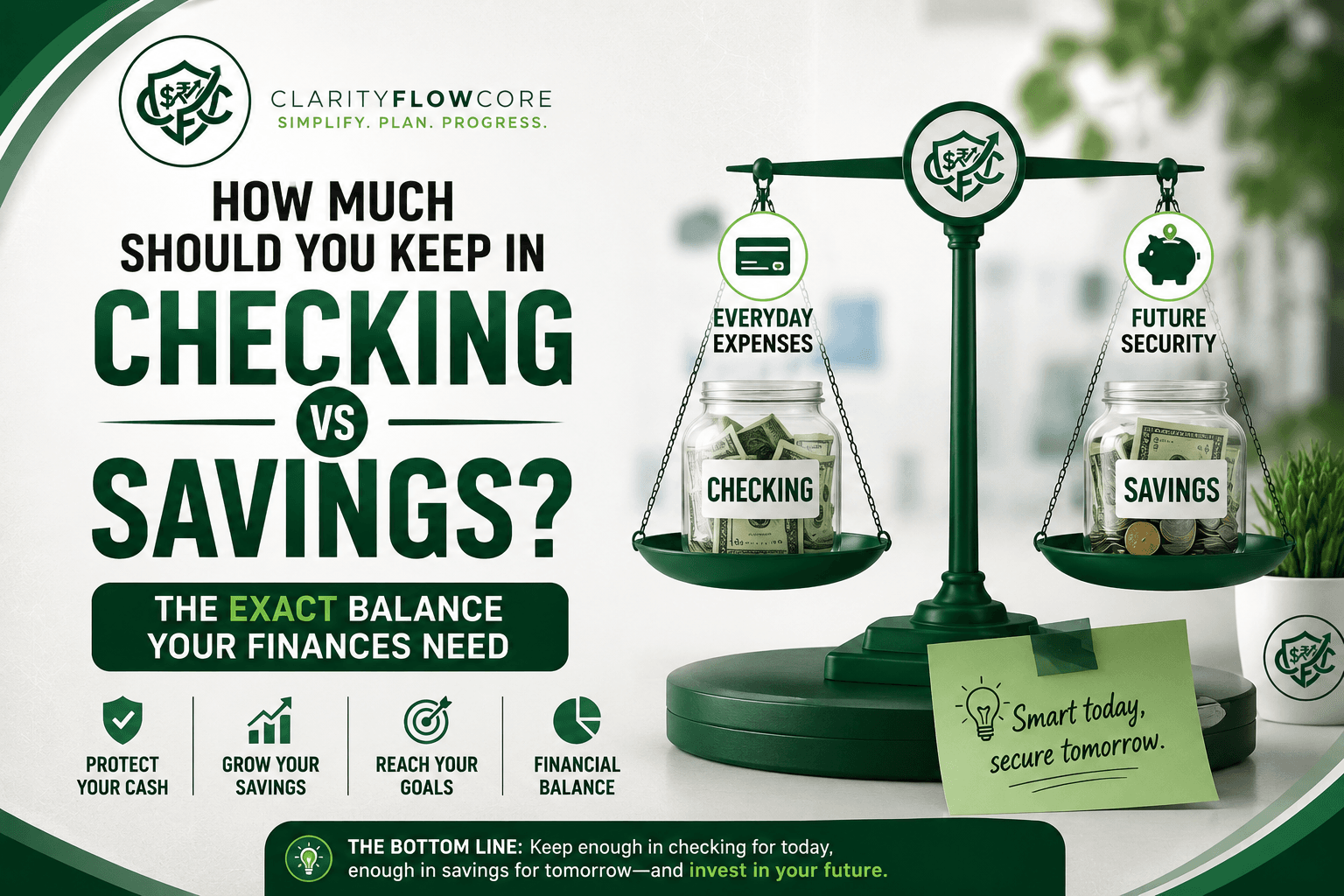

How Much Should You Keep in Checking vs Savings?

Quick Answer:

In the great checking vs savings debate, your accounts serve completely different operational purposes.

- Checking Account: Keep 1 to 1.5 months of your total living expenses here to act as a buffer against auto-pays and overdrafts.

- Savings Account (HYSA): Keep 3 to 6 months of living expenses here as your emergency fund.

- Investments: Any liquid cash you have that exceeds these two combined limits is losing value to inflation and should be routed to your brokerage or retirement accounts.

Years ago, I stood in the checkout line at the grocery store, rapidly logging into my banking app while the cashier scanned my items. I was transferring $45 from my savings account to my checking account just so my debit card wouldn’t decline.

I actually had plenty of money. I was just managing it completely wrong.

I was so obsessed with earning interest that I kept my checking account balance hovering near zero. Every time an unexpected utility bill auto-drafted a day early, I was hit with a devastating $35 overdraft fee, completely wiping out the interest I was trying to earn.

Determining exactly how much cash to keep in checking vs savings is not a guessing game. It is a highly specific, operational math problem. If you keep too little in checking, you get crushed by overdraft fees and financial anxiety. If you keep too much in checking, your cash is actively destroyed by inflation.

To optimize your cash flow and build a stress-free financial system, you must assign a strict, mathematical job to every dollar. Here is the definitive operational guide to the checking vs savings equation, the exact numbers you need in each account, and the hidden banking traps that ruin your cash flow.

The Role of the Checking Account: The Operations Center

The most dangerous misconception in the checking vs savings dynamic is treating your checking account like a wealth-building tool.

Your checking account is not a vault; it is an operations center. It is the grand central station of your financial life. Cash flows in from your employer, and it rapidly flows out to your landlord, the utility company, and your credit card issuer.

Because traditional checking accounts pay an insulting 0.01% APY (Annual Percentage Yield), holding excess money here is mathematically identical to burning it.

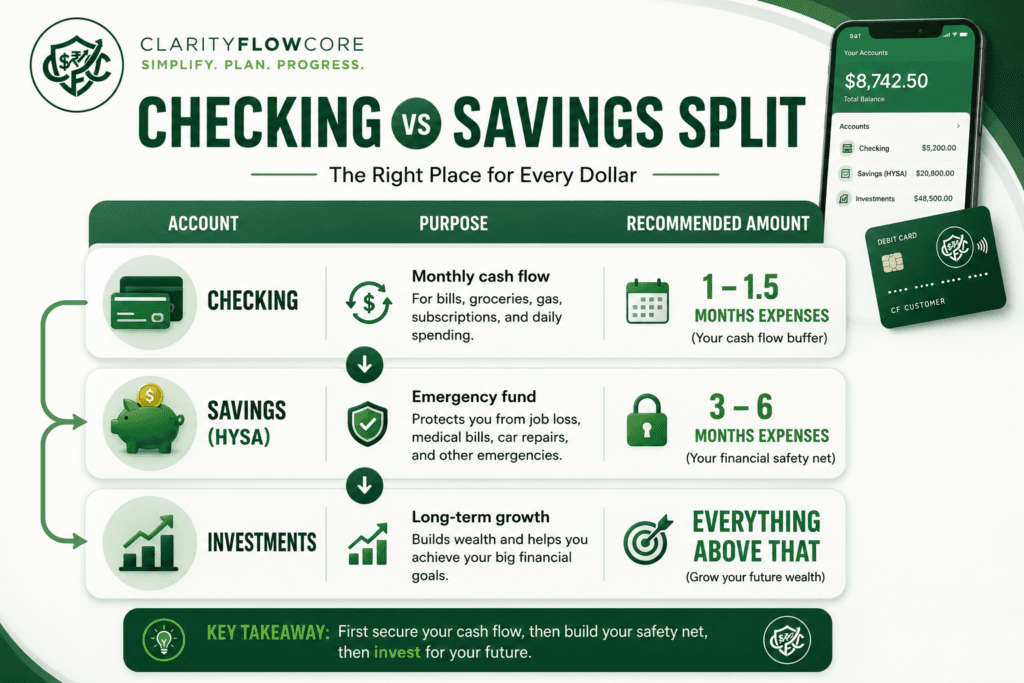

The Target Number: 1.0 to 1.5 Months of Expenses

Your checking account should hold exactly enough money to cover one to one-and-a-half months of your baseline living expenses.

Notice the wording: expenses, not income.

If your take-home pay is $6,000 a month, but your actual survival costs (rent, groceries, utilities, minimum debt payments) are $4,000, your target checking account balance should constantly hover between $4,000 and $6,000.

If you’re preparing to move into your own place, understanding these monthly living costs before signing a lease is essential. Our guide How Much Should You Save Before Moving Out on Your Own? explains how much cash you’ll likely need for upfront moving expenses and your first few months of independent living.

Why the Extra Half-Month Buffer?

That extra 0.5 month (in this case, $2,000) is the most critical component of the checking vs savings strategy. I call it the Sleep Well At Night (SWAN) Buffer.

Life does not align perfectly with your payroll schedule. Your mortgage might auto-draft on the 1st of the month, but your paycheck might not clear until the 3rd. If you keep your checking account exactly at zero, that timing mismatch will trigger a cascading series of bounced payments, late fees, and credit score strikes.

The 50% buffer absorbs all timing shocks. It ensures that no matter what day a bill hits your account, there is a deep enough pool of liquid cash to cover it instantly.

The Role of the Savings Account: The Iron Vault

If the checking account is the operations center, the savings account is your Iron Vault. This account exists for one primary reason: to protect you from the catastrophic emergencies of life.

In the modern banking ecosystem, you must strictly utilize a High-Yield Savings Account (HYSA) from an online-only bank. Traditional brick-and-mortar savings accounts pay essentially zero interest. A competitive HYSA pays between 4.00% and 5.00% APY because they lack the overhead of physical real estate.

If you’re opening your first online savings account, How to Choose Your First High-Yield Savings Account explains how to compare FDIC insurance, fees, APYs, and transfer features before choosing a bank.

The Target Number: 3 to 6 Months of Expenses

The math for your savings account is universally agreed upon by financial planners, but it scales based on your personal risk profile.

Using our previous example of $4,000 in monthly expenses:

| Your Risk Profile | Target Savings Multiplier | Required Cash in Savings |

| Highly Secure (Dual-Income, W-2 Employees) | 3 Months | $12,000 |

| Standard Risk (Single Income, Homeowner) | 6 Months | $24,000 |

| High Risk (Freelancers, 1099 Contractors) | 9 to 12 Months | $36,000+ |

This money is not for vacations. It is not for a down payment on a new car. It is the defensive shield that prevents you from going into high-interest credit card debt when your transmission explodes or your company initiates mass layoffs.

If you want to run your exact numbers through a calculator to determine your optimal split, use the interactive tool below.

How Your Life Situation Changes the Right Balance

The recommended checking and savings balances aren’t one-size-fits-all. Your ideal cash allocation depends on how predictable your income is, how stable your monthly expenses are, and how quickly you could recover from a financial emergency.

For example, if you’re a salaried employee with a stable paycheck arriving on the same day every two weeks, your cash flow is relatively predictable. Keeping about one to one-and-a-half months of expenses in checking and three to six months in a High-Yield Savings Account is usually sufficient.

However, freelancers, self-employed professionals, commission-based workers, and small business owners often experience uneven income throughout the year. A slow month or a delayed client payment can temporarily reduce cash flow, even when business is healthy. In those situations, maintaining a slightly larger checking buffer—or even keeping six to twelve months of expenses in savings—can provide valuable peace of mind.

Families with children may also benefit from larger reserves. Unexpected medical bills, school expenses, home repairs, or vehicle breakdowns tend to occur more frequently when multiple people depend on the household budget. A larger emergency fund can prevent these expenses from turning into high-interest credit card debt.

On the other hand, someone living with roommates, carrying very little debt, and working in a stable industry may feel comfortable maintaining the lower end of the recommended range. The key isn’t copying someone else’s numbers—it’s building a cash management system that reflects your own financial risks.

Review your checking and savings balances at least once or twice each year. A new job, salary increase, mortgage, growing family, or career change may require adjusting your targets. As your financial life evolves, your cash management strategy should evolve with it.

Cash Management Calculator

Cash Management Calculator

Find your exact checking buffer and savings vault targets.

When This Backfires: The Operational Traps

When people attempt to balance the checking vs savings equation, human psychology often overrides mathematical logic. If you lean too heavily in one direction, the system collapses. Here is exactly when managing these accounts backfires aggressively:

1. The Zero-Buffer Trap (The Over-Optimizer)

This is the mistake I made early in my career. You read that HYSAs are paying 5%, so you transfer every single spare dollar out of your checking account to maximize your yield. You leave exactly $50 in your checking account.

This is financially reckless. If you earn 5% APY on an extra $1,000, you are making roughly $4.16 a month in interest. If keeping your checking account that low causes you to accidentally overdraft your account just one single time, the bank will hit you with a $35 overdraft fee.

That single fee just wiped out eight months of your hard-earned interest. You must leave the 1.5x buffer in your checking account. The peace of mind is vastly more profitable than chasing four dollars of yield.

2. The Cash Hoarder Trap (The Inflation Victim)

This is the opposite extreme. Some individuals are so terrified of the stock market that they keep $80,000 sitting in their primary checking account. They feel a deep psychological safety seeing a massive number when they log into their banking app.

This is the silent destruction of wealth.

Inflation averages roughly 3% historically (and has spiked much higher recently). If you keep $80,000 in a 0.01% checking account, your purchasing power is actively melting away. After a few years, that cash will buy significantly fewer groceries, gas, and housing than it did the day you deposited it. Once your Checking Buffer and Savings Vault are full, every subsequent dollar must be deployed into the market to outpace inflation.

3. The “Same Bank” Trap (The Commingler)

A massive operational failure in the checking vs savings strategy is opening both accounts at the exact same physical bank.

If your emergency savings account is sitting right beneath your checking account on your mobile app dashboard, the friction to transfer money is zero. When you see a pair of shoes you want, or you want to upgrade your vacation hotel, your brain will rationalize: “I’ll just instantly slide $300 over from savings, and I’ll pay it back next month.”

You will never pay it back.

Your High-Yield Savings Account must be held at an entirely different, online-only banking institution. It should take 1 to 3 business days for an ACH transfer to clear. That 48-hour lag time acts as a psychological cooling-off period, forcing you to determine if you are actually facing a catastrophic emergency, or if you are simply experiencing a fleeting impulse.

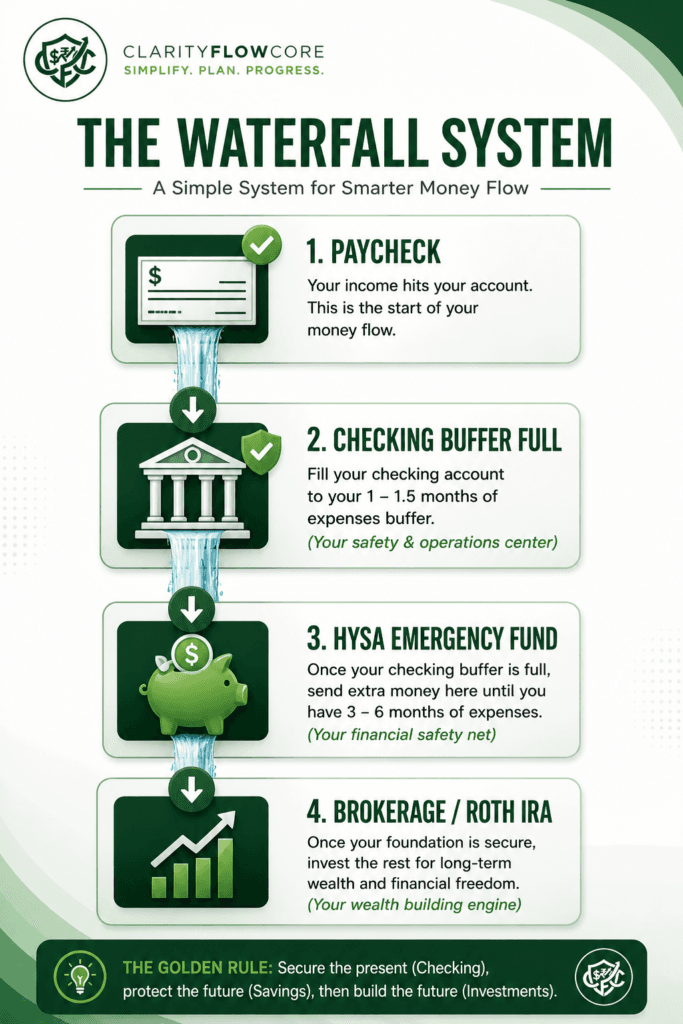

The “Waterfall” System: Automating the Flow

To permanently solve the checking vs savings debate, you must remove human willpower from the equation. If you rely on your own discipline to manually move money around on the 30th of the month, you will inevitably fail. You must build an automated financial waterfall.

Here is exactly how to set up the infrastructure:

Step 1: The Paycheck Landing

Set up your employer’s direct deposit to land 100% of your paycheck into your primary checking account.

Step 2: The Cap

Determine your 1.5x checking account buffer. Let’s assume it is $6,000.

Step 3: The Automated Sweep

Log into your external High-Yield Savings Account portal. Set up an automated recurring “pull” transfer. For example, if you get paid on the 1st and the 15th, schedule the HYSA to automatically withdraw $500 from your checking account on the 3rd and the 17th.

Step 4: The Overflow Route

Once your HYSA hits your 6-month target (e.g., $24,000), you stop the sweep. You then redirect that exact same automated transfer to flow directly into your Roth IRA or your taxable brokerage account to buy index funds.

By utilizing the Waterfall System, you ensure your checking account never drops below its safe buffer, your emergency fund is fully funded, and your excess cash is automatically building generational wealth in the background while you sleep.

🗺️ What Does Your “Overflow” Actually Build?

Once you’ve figured out your checking buffer and savings vault, it’s time to see the big picture. Plug your total debts, cash reserves, and monthly “overflow” rate into our free Financial Freedom Planner to find out if you are actually on track, and map out your custom timeline to true wealth.

Frequently Asked Questions (FAQs)

1. Should I use multiple checking accounts for different purposes?

Many people find success using two checking accounts: one specifically for fixed bills (rent, utilities, car payments) and a separate checking account with a dedicated debit card for variable spending (groceries, restaurants, fun money). This prevents you from accidentally spending your rent money on a Friday night dinner.

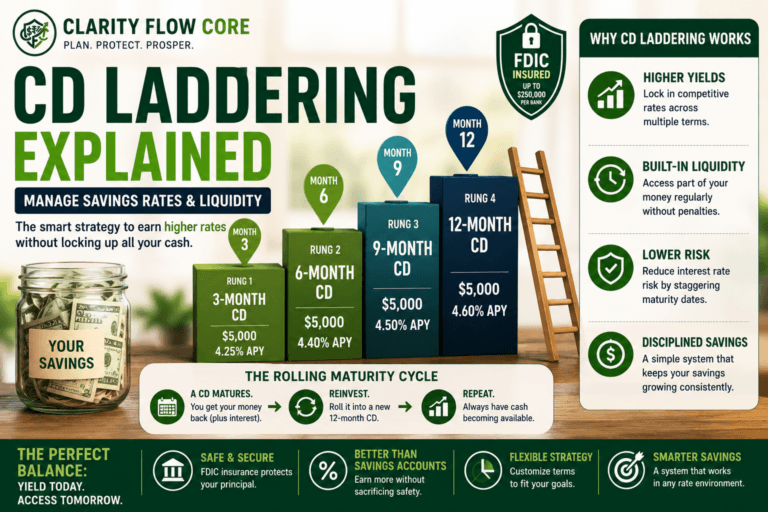

2. Can I keep my emergency fund in a CD instead of a savings account?

Yes, but with extreme caution. A Certificate of Deposit (CD) locks your money up for a specific term in exchange for a higher interest rate. If you face an immediate emergency and need to break the CD early, you will be hit with severe early withdrawal penalties. A better strategy is to keep 1-2 months in a liquid HYSA, and use a CD Laddering strategy for the remainder of your emergency fund.

3. Does moving money between checking and savings hurt my credit score?

Absolutely not. Your credit score is determined entirely by your debt (credit cards, loans, mortgages) and your payment history. The credit bureaus do not have access to your checking or savings account balances, and moving your own cash between institutions has zero algorithmic impact on your FICO score.

4. How fast can I access my money in an online HYSA?

If you need to transfer money from an online High-Yield Savings Account back to your primary traditional checking account, an ACH transfer typically takes 1 to 3 business days to fully clear. This is why maintaining the 1.5x buffer in your checking account is so critical—it bridges the gap while you wait for the emergency funds to arrive.

5. Are online savings accounts safe?

Yes, provided you verify that the online institution is FDIC-insured (or NCUA-insured if it is a credit union). FDIC insurance guarantees that even if the online bank goes completely bankrupt, the federal government will reimburse your deposits up to $250,000 per depositor, per institution.

The Bottom Line

The checking vs savings debate is the absolute bedrock of your financial architecture. If you get this structural math wrong, no amount of advanced investing will save you from daily anxiety.

Stop treating your checking account like a high-score tracker, and stop treating your savings account like a slush fund. Establish your 1.5x operations buffer to eliminate overdraft fees forever. Build your 6-month emergency vault at a completely separate online bank to capture high-yield interest and create a psychological barrier. Once the buckets are full, turn on the automated waterfall and let your money finally go to work.

Learn More About Smart Cash Management

Managing your checking and savings accounts effectively is one of the foundations of long-term financial health. The following resources provide additional guidance on emergency savings, bank account safety, deposit insurance, and cash management best practices.

- Consumer Financial Protection Bureau (CFPB) — Managing Your Checking Account

Practical guidance on avoiding overdrafts, managing checking accounts, and handling everyday banking. - Federal Deposit Insurance Corporation (FDIC) — Deposit Insurance FAQs

Learn how FDIC insurance protects eligible bank deposits and understand current coverage limits. - FDIC Money Smart — Financial Education Program

Educational resources covering budgeting, saving, emergency funds, and responsible money management. - Consumer Financial Protection Bureau (CFPB) — Start With Saving

Information on building emergency savings and creating healthy saving habits. - National Credit Union Administration (NCUA) — Share Insurance Toolkit

Explains how deposits at federally insured credit unions are protected through NCUA insurance. - Investor.gov (U.S. Securities and Exchange Commission) — Compound Interest Calculator & Investor Education

Resources explaining why excess cash may be better invested for long-term growth after maintaining an adequate emergency fund.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.