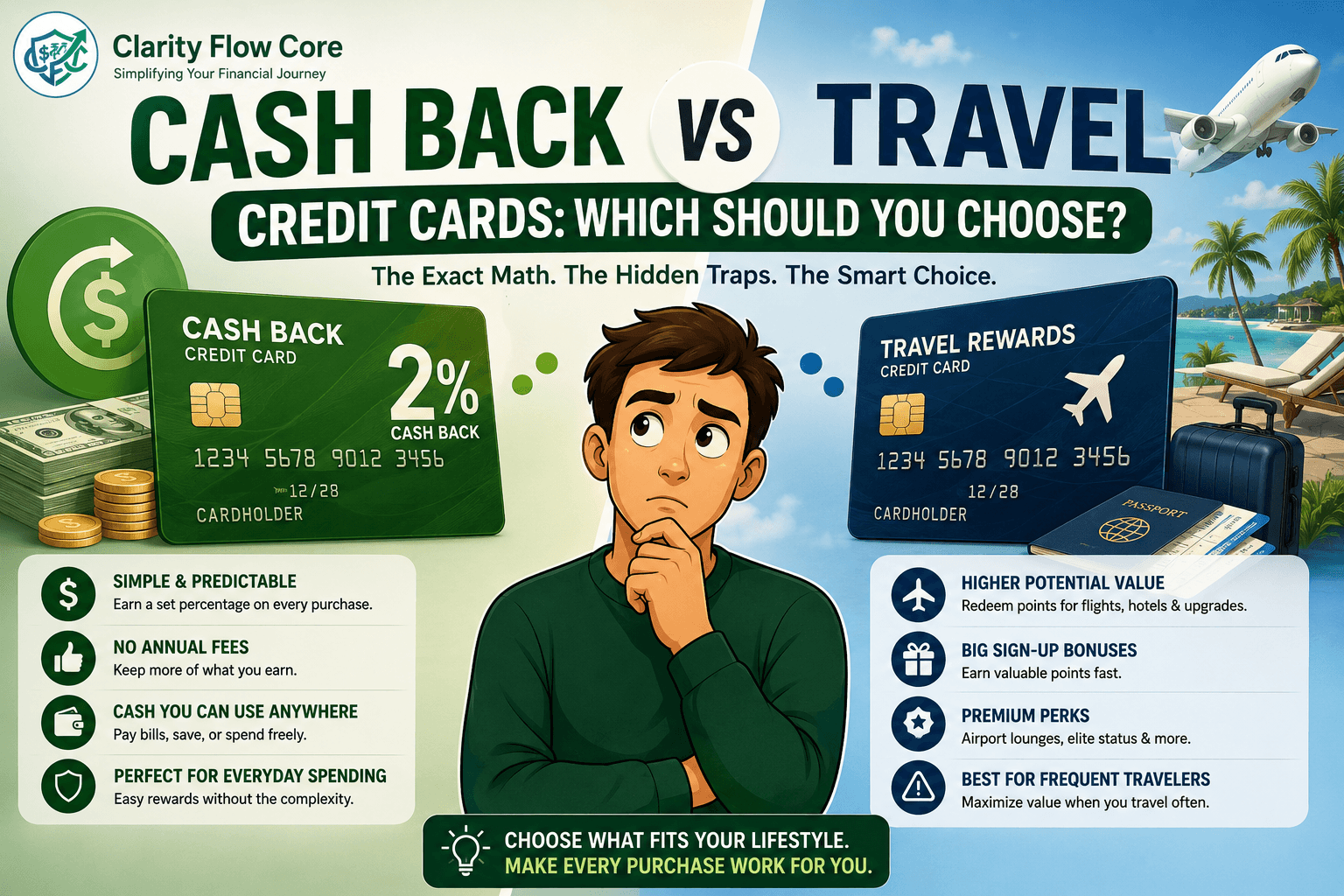

Cash Back vs Travel Credit Cards: Which Should You Choose?

You finally built a pristine credit score, you have zero consumer debt, and you are ready to start making your daily spending work for you. You open a browser to find a rewards card, and immediately hit a massive fork in the road: cash back vs travel credit cards.

The credit card industry spends billions of dollars every year trying to convince you that their specific rewards currency is the best. The airline influencers promise you free first-class flights to Tokyo, while the pragmatists tell you that cash is king.

Many consumers sign up for premium travel cards because the marketing looks incredible, only to realize months later that they are too busy working to actually take a vacation. They optimize for a lifestyle they aren’t actually living, and they lose money to annual fees in the process.

Choosing a rewards system is not about what looks flashiest in your wallet. It is a strict mathematical decision based entirely on your actual cash flow and daily habits. Here is the definitive operational breakdown of the cash back vs travel credit cards debate, the exact math of point valuations, and the hidden traps that cost beginners thousands of dollars.

⚡ Quick Answer

In the cash back vs travel credit cards debate, cash back wins for operational simplicity and predictable value—earning a flat percentage back on everyday spending to artificially lower your monthly bills. Travel cards offer significantly higher potential value (free flights and hotel upgrades) but require mastering complex point transfers, dealing with high annual fees, and traveling organically at least 3-4 times a year to make the math work.

Cash Back vs Travel Credit Cards at a Glance

To quickly visualize the operational differences between the two ecosystems, here is how they stack up against each other:

| Feature | Cash Back | Travel Rewards |

| Ease of Use | Excellent | Moderate to Difficult |

| Annual Fees | Usually low or $0 | Often $95 to $695 |

| Flexibility | Very High | Travel-focused |

| Potential Value | Moderate | Very High |

| Best For | Most everyday consumers | Frequent travelers |

| Complexity | Low | High |

The Foundation: How Rewards Actually Work

Before declaring a winner, you must understand how the banks afford to pay you these rewards in the first place.

Every time you swipe a credit card, the merchant (the grocery store, the gas station, the software company) pays a “swipe fee” or “interchange fee” of roughly 1.5% to 3% to the credit card network (Visa, Mastercard, Amex).

To incentivize you to use their specific card over a competitor’s, the bank takes a portion of that swipe fee and kicks it back to you. They are effectively bribing you to route your spending through their system. In the cash back vs travel credit cards ecosystem, you are simply choosing how you want that bribe delivered: as liquid cash, or as a digital travel currency.

Team Cash Back: The Power of Predictability

If you value simplicity and immediate gratification, cash back is the undisputed heavyweight champion.

A cash back credit card operates on raw, predictable math. You earn a fixed percentage of your purchases back as cash, which you can deposit directly into your checking account or use as a “Statement Credit” to artificially lower your credit card bill.

The Mathematical Advantage

Cash back cards usually fall into two operational categories:

- Flat-Rate Cards: You earn exactly 1.5% to 2% back on every single purchase, whether you are buying a gallon of milk or a $2,000 camera lens. (Examples: Citi Double Cash, Wells Fargo Active Cash, Capital One Quicksilver).

- Tiered Category Cards: You earn 3% to 5% back in specific lifestyle categories (like groceries, gas, or dining) and 1% on everything else.

Let’s look at the operational math for a standard household that spends $3,000 a month on a flat 2% cash back card:

| Monthly Spend | Cash Back Rate | Monthly Cash Earned | Annual Cash Earned |

| $3,000 | 2.0% | $60 | $720 |

By doing absolutely nothing different with your life other than routing your existing expenses through a 2% card, you generate $720 in tax-free, liquid cash every year.

The Pros of Cash Back

- Operational Simplicity: 1 point equals exactly 1 cent. There are no transfer ratios to memorize and no blackout dates to navigate.

- Zero Annual Fees: The vast majority of the best cash back cards on the market charge absolutely $0 in annual fees. It is pure profit.

- Ultimate Flexibility: You cannot use airline miles to pay your car insurance or fund your Emergency Fund Basics. Cash is universally accepted.

The Cons of Cash Back

- Lower Sign-Up Bonuses: Cash back cards usually offer modest welcome bonuses (e.g., “Spend $500, get $200”).

- A Hard Value Ceiling: You will never get “out-sized” value. $100 in cash back will only ever buy you exactly $100 worth of goods.

Team Travel: The Game of Maximizing Value

If cash back is a straightforward savings account, travel rewards are a high-stakes strategy game.

Travel credit cards reward you in “Points” or “Miles.” Unlike cash, the value of a travel point is completely subjective and depends entirely on how you manually redeem it. If you master the system, travel cards offer significantly higher financial returns than cash back ever could. (Popular examples include the Chase Sapphire Preferred, American Express Gold Card, and Capital One Venture Rewards).

The Mathematical Advantage (Cents Per Point)

To understand the cash back vs travel credit cards math, you must understand the concept of “Cents Per Point” (CPP).

If you have 50,000 points on a premium travel card, you usually have two choices:

- The Lazy Redemption: You log into the bank’s portal and redeem those 50,000 points for cash. They will give you 1 cent per point. You get $500.

- The Strategic Transfer: You transfer those 50,000 points directly to a partner airline (like United or Delta) to book a business-class flight that normally costs $1,500 in cash.

The Math of the Transfer:

$1,500 (Value of Flight) ÷ 50,000 Points = 3.0 Cents Per Point (CPP).

By transferring the points, you tripled the value of your rewards. This is the entire allure of travel credit cards. You can unlock luxury experiences that you would never actually pay for with your own cash.

The Pros of Travel Cards

- Massive Sign-Up Bonuses: Premium travel cards regularly offer 60,000 to 100,000 points just for signing up and meeting a minimum spend requirement. That single bonus can easily fund a round-trip international flight.

- Luxury Perks: Travel cards often include aggressive lifestyle benefits: free access to airport lounges, TSA PreCheck credits, free checked bags, and primary rental car insurance.

The Cons of Travel Cards

- Massive Annual Fees: Premium travel cards are incredibly expensive to hold. Annual fees range from $95 up to a staggering $695 a year.

- Complexity: Finding an airline “award ticket” for the exact day you want to travel requires hours of searching, flexibility, and a deep understanding of airline alliances.

- Devaluation: You do not own the points. The airline can decide tomorrow that a flight now costs 80,000 points instead of 50,000. Your rewards instantly lose value.

How Often Do You Need to Travel to Break Even?

If you are struggling to choose a path, analyze your calendar. Travel cards only generate positive ROI if you naturally travel enough to offset the hefty annual fees.

| Trips Per Year | Best Choice |

| 0 to 1 Trip | Cash Back: An annual fee travel card will mathematically lose you money. |

| 2 to 3 Trips | Depends: A low-fee ($95) travel card might work, but cash back is still safer. |

| 4+ Trips | Travel Rewards: The free checked bags and lounge access will quickly pay for the card’s annual fee. |

When This Backfires: The Rewards Traps

Regardless of which side you choose in the cash back vs travel credit cards debate, the banks have meticulously engineered the system so that you lose if you lack discipline. Here is exactly when chasing rewards backfires aggressively:

1. The Annual Fee Deficit (The Platinum Trap)

Beginners frequently fall into the trap of applying for a premium travel card because they want the prestige of a heavy metal card. They pay a $550 to $695 annual fee. If you’re just starting your credit journey and don’t yet qualify for premium rewards cards, Best Secured Credit Cards for Beginners in 2026 compares secured cards that can help you build the credit history needed to qualify for better rewards cards in the future.

However, they only fly once a year to visit their parents for Thanksgiving. If you are paying $695 a year to hold a card, but you are only extracting $200 in value from the travel credits and lounge access, you are in a massive mathematical deficit. You are literally paying the bank to feel rich. If you do not travel at least 3 to 4 times a year organically, you must stick to no-fee cash back cards.

2. The Interest Rate Eraser

This is the single most destructive trap in personal finance. If you carry a balance on your credit card from month to month, the bank will charge you roughly 22% to 28% in interest.

If you are earning 2% cash back, but paying 24% in interest, you are losing massive amounts of money. No rewards program on earth will ever out-earn standard credit card interest. If you cannot follow The 50/30/20 Budget Rule Explained Simply and pay your statement balance in full every single month, you should not be using a rewards credit card at all. (If you are currently carrying a balance, you must address your Credit Utilization immediately before applying for more credit).

3. Point Hoarding (The Devaluation Trap)

Travel points are an inflating currency. If you earn 100,000 airline miles and decide to “save them for retirement,” you are making a fatal error. Airlines constantly devalue their points, meaning it requires more points every year to book the exact same flight. Cash back can be invested in the stock market to grow; travel points only lose value over time. Earn them, and burn them.

Frequently Asked Questions (FAQs)

Can I have both a cash back card and a travel credit card?

Absolutely. Many advanced credit card users employ a hybrid strategy. They use a premium travel card specifically to book flights and dining to maximize points, and they use a flat 2% cash back card for everyday spending like car repairs or software subscriptions.

Are travel credit cards worth the massive annual fees?

They are only mathematically worth it if you organically use the credits the card provides. If a card charges a $300 annual fee, but gives you a $300 annual travel credit that you easily use to book a hotel you were going to book anyway, the effective fee is $0. If you have to force yourself to spend money to use the credits, the card is not worth it.

Do cash back or travel points ever expire?

For most major bank-issued credit cards, your points or cash back do not expire as long as your account remains open and in good standing. However, if you transfer points to a specific airline frequent flyer account, those miles are now subject to the airline’s specific expiration rules.

What does it mean to “transfer points to travel partners”?

Instead of booking a flight directly through your credit card’s website, premium travel cards allow you to move your points directly to a partner airline’s program. For example, transferring 30,000 Chase points directly to your United MileagePlus account to book a United flight. This is almost always how you extract the highest “Cents Per Point” value.

Does applying for multiple rewards cards hurt my credit score?

Yes, temporarily. Every time you apply for a new credit card, the bank initiates a “Hard Inquiry” on your credit report, which usually drops your FICO score by 3 to 5 points. Applying for multiple cards rapidly will severely damage your score. Always wait at least 3 to 6 months between credit card applications.

The Bottom Line

The cash back vs travel credit cards debate does not have a universal winner, but it does have a correct answer for your specific lifestyle.

Do not let travel influencers shame you into paying a $695 annual fee if you spend 50 weeks of the year at home. Cash back is a phenomenal, wealth-building tool that artificially lowers the cost of your daily life. If you have the travel bug and the organizational discipline to navigate transfer portals, travel cards will unlock the world.

Run the math on your actual daily spending, identify your lifestyle goals, and choose the system that actually puts value back into your pocket.

References & Trusted Resources

When you are planning a massive financial purchase, you should rely on data from the organizations that actually regulate the housing market. The guidelines in this article are based on standards from:

- Consumer Financial Protection Bureau (CFPB) – Buying a House

- Federal Housing Administration (HUD/FHA) – Buying a Home Guide

- Fannie Mae – Homebuyer Resources

- Freddie Mac – Down Payment & Closing Costs

- IRS – First-Time Homebuyer IRA Exemptions

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.