How Capital Gains Taxes Work for Beginners: A Simple Guide

Quick Answer:

Capital gains taxes are fees you pay to the government when you sell an asset—like a stock, cryptocurrency, or property—for more than you paid to acquire it. The tax is calculated entirely on your net profit, not the total sale amount.

- Short-Term Capital Gains: If you hold the asset for one year or less, your profit is taxed at your standard ordinary income tax rate.

- Long-Term Capital Gains: If you hold the asset for more than one year, you qualify for a heavily discounted capital gains rate of 0%, 15%, or 20%, depending entirely on your total taxable income.

You click the “Sell” button inside your brokerage app, locking in a sweet $2,000 profit on a stock you bought a few months ago. You feel an immediate wave of financial accomplishment. You made a smart play, beat the market, and the cash is sitting safely in your account.

Then, a cold realization sets in. The IRS saw that transaction.

For many beginner investors, the excitement of booking a winning trade is rapidly overshadowed by the fear of the unknown tax bill waiting for them the following April. The tax code is intentionally written to look like an intimidating wall of jargon, leaving millions of everyday people completely confused about how their investment profits are actually evaluated.

When I first started building an investment portfolio, I accidentally triggered a series of completely unnecessary tax penalties simply because I didn’t understand the reporting timeline. I assumed that as long as I kept the cash inside my investment account and didn’t transfer it to my personal bank, I didn’t owe any taxes. I was completely wrong, and the IRS corrected my mistake with an expensive penalty notice.

Understanding how capital gains taxes work is not an advanced wealth management strategy reserved exclusively for corporate executives. It is foundational financial literacy that determines exactly how much cash you actually get to keep in your pocket. Here is the definitive operational breakdown of capital gains mechanics, the timeline math you must master, and the exact strategies to legally minimize your tax burden.

The Core Concept: What is a Capital Gain?

Before running the calculations, we must define what the government is actually targeting. A capital gain occurs when you sell a “capital asset” for more than its adjusted acquisition price (known in tax terms as your Cost Basis).

A capital asset includes almost everything you own for investment or personal purposes:

- Stocks and index funds

- Bonds

- Cryptocurrency and NFTs

- Real estate (including rental properties and your primary home)

- Collectibles (like fine art, vintage cars, or rare coins)

The IRS does not care about your lifestyle or the choices you make; they focus strictly on the math of the transaction. The equation is straightforward:

Final Sale Price − Initial Cost Basis = Capital Gain (or Loss)

Realized vs. Unrealized Gains

This is the single biggest point of confusion for beginner investors. You only trigger a tax liability when you realize a gain.

Suppose you buy $1,000 worth of an index fund, and over the next twelve months, the market spikes, turning your investment into $3,000. On paper, you have a $2,000 gain. This is an unrealized gain (often called a “paper profit”). You do not owe a single penny of tax on this money. You can watch that balance grow for thirty years, and as long as you do not sell the asset, you owe $0.00 to the government.

The exact second you click the “Sell” button and convert that index fund back into cash, that paper profit becomes a realized gain. The transaction is locked into the ledger, the brokerage firm generates a Form 1099-B, and you are officially on the hook for capital gains taxes.

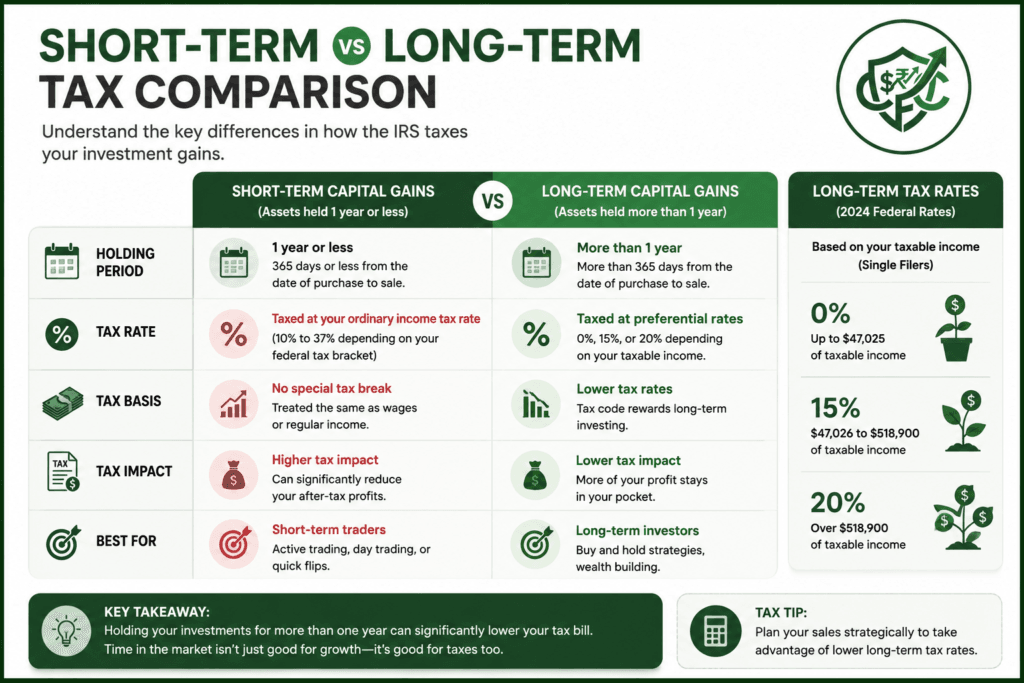

The Great Fork in the Road: Short-Term vs. Long-Term

To understand how capital gains taxes work, you must realize that the IRS uses a strict, 365-day clock to categorize your profits. The moment you execute a sale, your asset is thrown into one of two distinct categories, and the tax implications are wildly different.

1. Short-Term Capital Gains (The Punishment Zone)

If you buy an asset and sell it after holding it for one year or less, your profit is flagged as a short-term capital gain.

The government treats short-term gains with zero leniency. The IRS views this behavior as active trading or speculation, rather than long-term investing. Therefore, short-term capital gains receive absolutely no tax discounts. They are piled directly on top of your regular day-job wages and taxed at your standard Ordinary Income Tax Bracket (ranging from 10% to 37%).

If you are a single professional making $60,000 a year at your day job, you sit in the 22% federal tax bracket. If you day-trade crypto or flip a stock for a $5,000 profit within six months, that $5,000 is taxed at that full 22% rate.

2. Long-Term Capital Gains (The Incentive Zone)

If you have the discipline to hold your asset for one year and one day or longer, your profit transforms into a long-term capital gain.

The US tax code is intentionally engineered to reward long-term capital investment because it stabilizes the broader economy. To incentivize this behavior, the government grants massive, highly lucrative tax discounts on long-term gains. Instead of your standard income tax rate, your profits are evaluated using entirely separate, heavily discounted capital gains brackets: 0%, 15%, or 20%.

The Long-Term Capital Gains Tax Brackets

Your long-term capital gains bracket is determined entirely by your total taxable income for the year (which includes your day-job wages plus your investment profits).

Here is the exact operational layout of the long-term capital gains tax brackets for the current filing cycle:

| Filing Status | 0% Tax Rate | 15% Tax Rate | 20% Tax Rate |

| Single | Income up to $47,025 | Income between $47,026 and $518,900 | Income over $518,900 |

| Married Filing Jointly | Income up to $94,050 | Income between $94,051 and $583,750 | Income over $583,750 |

| Head of Household | Income up to $63,000 | Income between $63,001 and $551,100 | Income over $551,100 |

Look closely at the 0% bracket. If you are a single professional or freelancer earning a total taxable income under $47,025, you can legally sell long-term stocks or crypto and pay exactly 0% in federal taxes on your investment profits. This is the single most powerful legal loophole in the tax code for lower- and middle-income Americans.

Case Study: The True Cost of a 365-Day Mistake

To fully appreciate the real-world impact of how capital gains taxes work, let’s look at an emotionless, mathematical comparison of two identical investments with two slightly different holding timelines.

Meet Mark and Jessica. Both are single professionals earning a salary of $85,000 a year from their day jobs, putting them squarely in the 22% federal ordinary income tax bracket. Both Mark and Jessica bought $10,000 worth of shares in the exact same technology company. Over the course of months, the stock surged, and their shares became worth $20,000, leaving each with a $10,000 profit.

Mark’s Strategy (The Short-Term Sale)

Mark gets excited and decides to lock in his winnings early. He sells all his shares exactly 11 months after buying them. Because he held the stock for less than a year, his $10,000 profit is classified as a short-term capital gain.

- Tax Rate Applied: 22% (Ordinary Income Rate)

- Tax Bill Owed: $2,200

- Mark’s Net Cash Kept: $7,800

Jessica’s Strategy (The Long-Term Sale)

Jessica reviews the tax calendar and chooses a more patient approach. She waits and sells her shares exactly 12 months and two weeks after buying them. Because she crossed the one-year threshold, her $10,000 profit converts into a long-term capital gain. Looking at the tax brackets, her $85,000 income places her in the 15% long-term capital gains bracket.

- Tax Rate Applied: 15% (Long-Term Rate)

- Tax Bill Owed: $1,500

- Jessica’s Net Cash Kept: $8,500

The Operational Verdict:

By simply waiting an extra 45 days to execute the exact same trade, Jessica legally blocked the IRS from taking an extra $700 of her money. Jessica didn’t have to work harder, take more investment risk, or uncover a complex accounting loophole. She simply used the chronological layout of the tax system to optimize her capital efficiency.

The Hidden Variable: Manipulating Your Cost Basis

When beginners calculate how capital gains taxes work, they often look strictly at the raw purchase price of the asset. However, the tax code allows you to legally alter your Cost Basis to lower your taxable gains.

Your cost basis is not just the sticker price of the asset; it is the total amount of money it cost you to acquire, hold, and finalize the investment.

What Can You Add to Your Cost Basis?

- Brokerage & Transaction Fees: If your platform charges a commission to buy or sell a stock, crypto asset, or piece of real estate, those transaction fees are added directly to your cost basis. If you buy a stock for $1,000 and pay a $10 brokerage fee, your cost basis is $1,010. If you later sell it for $1,500, you are only taxed on a gain of $490, not $500.

- Real Estate Capital Improvements: If you buy a rental property or physical real estate for $250,000, and you spend $30,000 to replace the rotting roof and install modern plumbing, your legal cost basis expands to $280,000. If you eventually sell the property for $350,000, your taxable capital gain shrinks from $100,000 down to $70,000. You must maintain impeccable receipts to justify these adjustments to an auditor.

Defensive Wealth Tactics: Legal Ways to Drop the Bill

You do not have to sit back and accept whatever tax bill the IRS hand-delivers to you. If you understand the structural rules of asset management, you can deploy a highly effective operational defense to shield your investments.

1. The Tax-Loss Harvesting System

The IRS allows you to use your failures to completely eliminate the tax burden of your successes. This is a system called Tax-Loss Harvesting.

If you realize a $5,000 capital gain by selling a winning stock this year, but you also own a losing stock that has dropped by $3,000, you can intentionally sell that losing asset before December 31st to “harvest” the loss.

The Offsetting Math:

$5,000 (Capital Gain) − $3,000 (Capital Loss) = $2,000 (Net Taxable Gain)

Instead of paying taxes on $5,000, you are now only evaluated on a net $2,000. If your total losses exceed your total gains for the year, you can use the remaining losses to offset up to $3,000 of your ordinary day-job income, and roll any leftover losses into future tax years indefinitely.

2. Maximize Tax-Advantaged Accounts

The single cleanest way to win the capital gains game is to completely refuse to play it. You achieve this by routing your capital through specialized tax-sheltered accounts:

- Roth IRA / 401(k): You fund these accounts with after-tax cash. Once inside the perimeter, all your trading activity is 100% immune to capital gains taxes. You can buy, sell, flip, and rebalance assets inside a Roth IRA for forty years, and you will never owe a single dollar of tax when you withdraw the wealth in retirement.

- Traditional IRA / 401(k): You fund these accounts with pre-tax cash, lowering your current income today. All capital gains inside the account compound completely tax-deferred until you make standard withdrawals later in life.

3. The Section 121 Primary Residence Exclusion

If you own real estate, the tax code provides a massive capital gains shield for your primary home. Under Section 121, if you own and live in your house for at least two out of the five years immediately preceding the sale, you qualify for a massive tax exclusion.

- If you are Single, you can exclude up to $250,000 in pure capital gains profit from your taxes.

- If you are Married Filing Jointly, you can exclude up to $500,000 in pure capital gains profit.

If you bought a home for $300,000 and sell it years later for $700,000, your $400,000 profit is completely tax-free, provided you met the residency requirement.

WHEN THIS BACKFIRES: The Dangerous Tax Traps

Chasing tax reduction strategies without understanding the explicit fine print of the Internal Revenue Code will land you in severe financial distress. Here is exactly when trying to manage your capital gains backfires aggressively:

1. The Wash-Sale Rule Trap

This is the most common trap that catches beginner investors trying to harvest tax losses.

Suppose you sell shares of a popular tech stock on December 15th to harvest a $4,000 loss and lower your tax bill. However, you still love the company long-term, so you log back into your app on December 20th and buy those exact same shares back.

The IRS caught this maneuver decades ago and instituted the Wash-Sale Rule.

If you sell an asset for a loss and purchase a “substantially identical” asset within 30 days before or after that sale, your harvested loss is completely disallowed. The IRS will reject your tax write-off entirely, leaving you with a standard tax bill and a messy accounting headache.

2. The Net Investment Income Tax (NIIT) Cliff

If you are a high-earning professional, you must watch out for a silent financial penalty called the Net Investment Income Tax (NIIT).

The second your modified adjusted gross income crosses a specific legislative threshold ($200,000 for single filers, $250,000 for married couples), the government levies an extra 3.8% surtax on top of your existing capital gains rate. If you are in the 15% long-term bracket and cross this cliff, your real operational tax rate automatically jumps to 18.8%.

3. Letting the Tax Tail Wag the Investment Dog

This is a core behavioral trap in market strategy. Investors frequently watch a stock completely tank on the charts, but they refuse to sell it simply because they want to avoid paying the capital gains tax on their earlier profits.

This is logical insanity. It is always mathematically superior to sell an asset, pay a 15% tax on your gains, and pocket the remaining 85% of real cash than to hold an asset out of pure stubbornness and watch the entire investment drop 50% on the open market. Never let tax avoidance ruin a sound investment strategy.

Frequently Asked Questions (FAQs)

1. Do I owe capital gains taxes if I reinvest the money immediately?

Yes. Many beginner investors believe that if they instantly use the profits from selling Stock A to buy Stock B inside the same brokerage account, they don’t owe taxes. This is false. The moment an asset is sold for liquid cash, a taxable event is finalized. The only way to avoid this is by trading inside a tax-sheltered retirement account like a Roth IRA.

2. How are cryptocurrency profits taxed compared to traditional stocks?

The IRS officially classifies cryptocurrency as “property” rather than currency. Because of this classification, crypto assets are subject to the exact same capital gains rules as stocks. Buying Bitcoin and selling it within a year triggers short-term capital gains; holding it for over a year unlocks discounted long-term rates. Every crypto-to-crypto trade (e.g., swapping Ethereum for a stablecoin) also counts as a taxable sale.

3. What happens if I have a capital loss instead of a capital gain?

If you sell an asset for less than your initial cost basis, you register a capital loss. Capital losses are incredibly valuable because they can be used to directly offset your capital gains for the year. If your losses exceed your gains, you can use the remaining deficit to write off up to $3,000 of your ordinary job income, and roll the remaining balance into the next calendar year.

4. Do children or students have to pay capital gains taxes?

Yes, anyone who realizes an investment profit can owe capital gains taxes, regardless of age. Furthermore, parents must be highly careful of the “Kiddie Tax” rules. If a dependent child generates more than a specific threshold of unearned income (typically around $2,600), the IRS will automatically tax the remaining profits at the parents’ maximum ordinary income tax rate to prevent families from hiding wealth in children’s accounts.

5. How do capital gains taxes work when you inherit stocks or property?

Inheriting assets unlocks one of the most lucrative benefits in the tax code: the Stepped-Up Basis. If your relative bought a house forty years ago for $40,000, and it is worth $500,000 the day they pass away, your new cost basis is automatically “stepped up” to that current $500,000 market value. If you sell the property the next week for $500,000, you owe exactly $0.00 in capital gains taxes.

The Bottom Line

Mastering the mechanics of how capital gains taxes work is the ultimate separation between standard savings habits and real, institutional wealth acceleration.

Stop treating your investments like a series of erratic, short-term bets. Approach your portfolio with structural intentionality. Pay attention to the 365-day holding clock, protect your capital velocity by using tax-sheltered accounts like IRAs, and optimize your adjustments to cost basis. By understanding the operational rules of taxation, you guarantee that your hard-earned profits remain exactly where they belong: fueling your long-term financial freedom.

Tax Resources Worth Bookmarking

Whether you’re selling stocks, cryptocurrency, real estate, or other investments, these trusted resources can help you better understand capital gains taxes, reporting requirements, and legal tax-saving strategies.

- Internal Revenue Service (IRS) – Topic No. 409: Capital Gains and Losses

- Internal Revenue Service (IRS) – Publication 550: Investment Income and Expenses

- Investor.gov (U.S. Securities and Exchange Commission) – Educational resources on investing, taxes, and long-term investing principles.

- IRS – Frequently Asked Questions on Virtual Currency Transactions

- FINRA Investor Education Foundation – Learn how taxes, investing, and brokerage accounts work before making investment decisions.

- IRS – Publication 544: Sales and Other Dispositions of Assets

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.