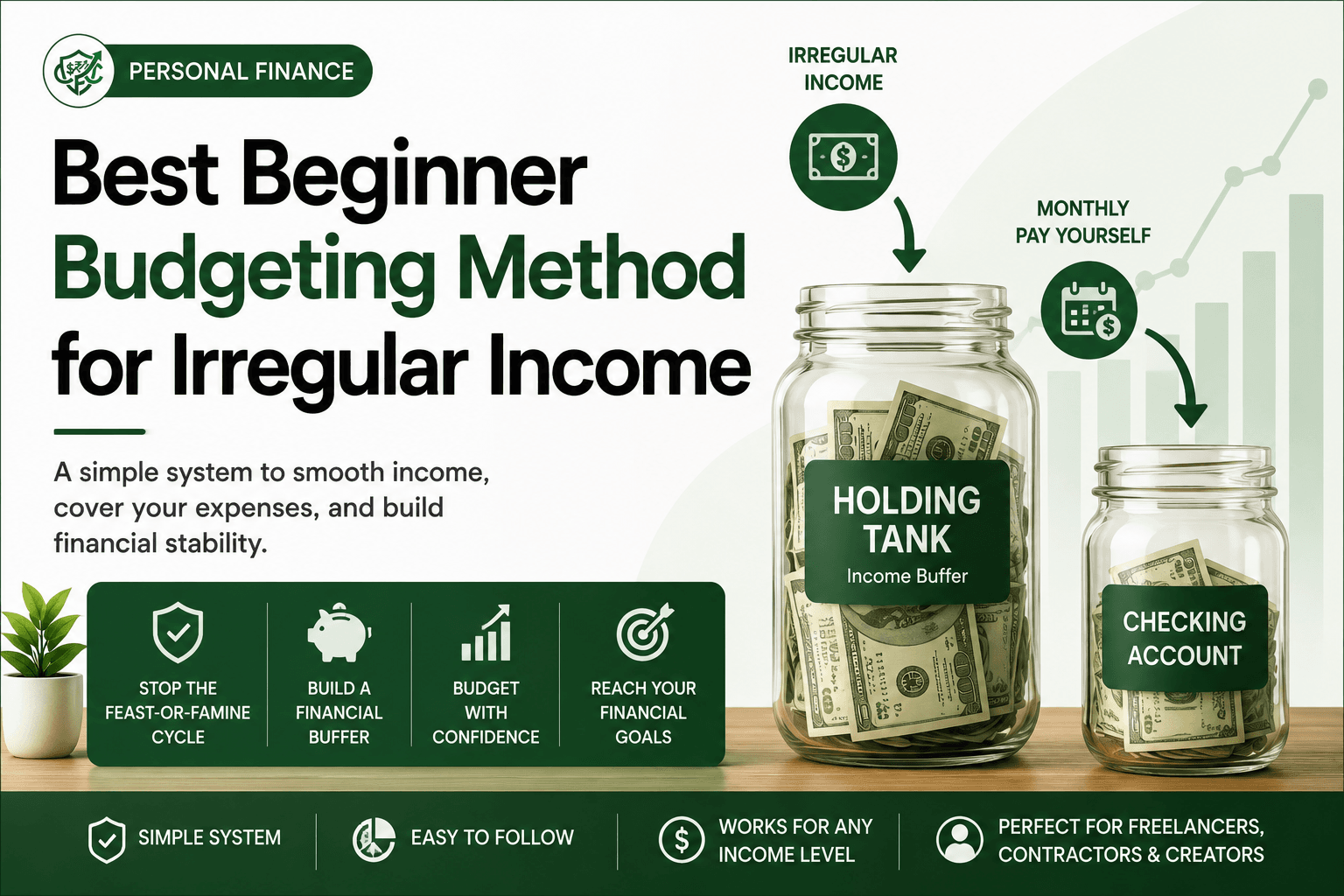

Best Beginner Budgeting Method for Irregular Income

Quick Answer:

Traditional budgeting frameworks fail variable earners because they require a predictable monthly income to work. The best beginner budgeting method for irregular income is the Holding Tank System (also known as the Base-and-Buffer or Revenue-Smoothing model). Instead of depositing client checks directly into your checking account and spending them wildly, all income flows into a dedicated savings account called the “Holding Tank.” You then pay yourself a fixed, unvarying monthly “salary” out of that tank to cover your baseline living expenses. This completely eliminates the dangerous “feast-or-famine” cycle.

You wrap up a massive client project, send over the final invoice, and a few days later, a crisp $7,500 lands in your bank account. You feel completely unstoppable. You book an upscale weekend trip, upgrade your home office setup, and treat your friends to an expensive dinner.

Fast forward forty-five days. A major contract gets unexpectedly delayed, a pipeline of work dries up completely, and your total income for the month hits an insulting $1,200. Suddenly, panic sets in. You find yourself scraping together cash just to clear your basic rent and insurance obligations, desperately regretting the money you spent during the previous month’s high.

This is the classic “feast-or-famine” roller coaster.

If your income bounces around erratically—whether you are a freelance creative, an independent contractor, a commission-driven sales professional, or a gig-economy worker—traditional personal finance advice can feel completely useless. Standard frameworks like the famous 50/30/20 rule assume a uniform, predictable paycheck arriving every second Friday. When your income changes drastically every 30 days, trying to calculate percentages of an unknown number is a fast track to financial anxiety.

Early on in my freelance career, I attempted to budget by simply averaging my annual income and dividing it by twelve. I assumed that since I averaged $5,000 a month across the year, I could safely build a $4,500 monthly lifestyle. The system blew up in my face during a brutal three-month winter drought where my invoices plummeted. I didn’t have a math problem; I had a structural framework problem.

To survive and thrive as a variable earner, you must decouple your monthly spending from your monthly earnings. The solution is the Holding Tank System. Here is the definitive, operational blueprint to implement this framework, smooth out your cash flow permanently, and build an unshakeable financial foundation.

Why Traditional Budgets Destroy Variable Earners

The foundational flaw of standard budgeting advice is its reliance on prediction. If you sit down on the first of the month and write, “I will earn $6,000 this month,” but your actual client retention rates drop and you only collect $3,500, your entire budget is instantly broken.

When income is unpredictable, people usually fall into one of two dangerous behavioral traps:

1. The Wealth Delusion (The Feast Peak)

When a massive check arrives, human psychology triggers a false sense of permanent wealth. You look at a bloated checking account balance and assume your lean days are ancient history. You accelerate your lifestyle spending right at the moment you should be building a strategic reserve.

2. The Survival Freeze (The Famine Valley)

When income drops to zero, spending drops to zero, and your life goes into code-red survival mode. You cut out non-essential activities, pause your retirement contributions, and suffer immense psychological stress.

This constant oscillation between luxury and scarcity makes it impossible to plan long-term financial goals, like buying a home or consistently investing. The goal of an effective beginner budgeting method for irregular income is to build a mathematical shock absorber that stands firmly between your erratic clients and your personal lifestyle.

The Core Strategy: The Holding Tank Mechanics

The Holding Tank System functions by creating an artificial corporate buffer. Think about how a standard corporation manages its money: Apple or Google do not instantly spend 100% of their daily sales revenue on corporate bonuses. They collect revenue, store it in corporate cash reservoirs, and distribute a predictable, steady payroll to their employees every single month, completely regardless of daily market fluctuations.

You must treat your personal life exactly like a corporation treats its staff. You are both the CEO producing the irregular revenue and the W-2 employee demanding a reliable salary to pay rent.

Instead of your income landing directly in your personal checking account where it can be impulsively spent, 100% of your incoming revenue lands in a separate, isolated High-Yield Savings Account: The Holding Tank.

On the first day of every month, you execute an automated transfer to move a fixed, non-negotiable cash amount out of the Holding Tank and into your primary checking account. This transfer is your monthly salary. If your holding tank collects $10,000 in a great month, your salary remains exactly the same. If your holding tank collects $0 in a catastrophic month, your salary still remains exactly the same. The tank absorbs the volatility so your personal life doesn’t have to.

Step 1: Finding Your “Bare-Bones” Baseline vs. Your “Ideal” Salary

To make the Holding Tank work, you have to find your target salary number. This requires identifying two separate operational baselines: your Bare-Bones Budget and your Ideal Target Salary.

The Bare-Bones Budget (The Floor)

This is the absolute minimum amount of cash required to keep your life running safely for 30 days if everything goes completely wrong. It is completely stripped of all luxury, entertainment, and lifestyle creep.

If you’re planning to move into your own apartment or house, calculating this baseline before signing a lease is essential. Read How Much Should You Save Before Moving Out on Your Own? to estimate both your upfront moving costs and the savings cushion you’ll want before living independently.

Your Bare-Bones Budget includes only:

- Housing (Rent or mortgage payments)

- Core Utilities (Electricity, water, basic internet)

- Basic Groceries (Survival food, not high-end dining out)

- Minimum Debt Obligations (Credit cards, student loans, auto loans)

- Critical Insurance Premiums (Health, auto, renters/homeowners)

The Ideal Target Salary (The Ceiling)

This is the number that Funds a comfortable, optimized lifestyle. It includes your bare-bones foundation, plus reasonable discretionary spending, streaming subscriptions, dining out, and consistent allocations toward long-term savings, investments, and tax provisions.

Let’s organize how these numbers look in a clean, comparative framework:

| Budget Category | Bare-Bones Monthly Floor | Ideal Target Monthly Salary |

| Housing & Utilities | $1,800 | $1,800 |

| Groceries & Basic Needs | $400 | $600 |

| Insurance & Minimum Debt | $300 | $300 |

| Discretionary / Entertainment | $0 (Completely Cut) | $500 |

| Savings & Investment Goals | $0 (Paused during crises) | $800 |

| Total Required Cash | $2,500 | $4,000 |

When you launch the Holding Tank System as a beginner, your initial target salary should be set as close to your Ideal Target Salary ($4,000) as your historical revenue permits. If you are entering a known slow seasonal stretch, you can temporarily drop your salary down closer to the Bare-Bones Floor ($2,500) to protect the structural integrity of the tank.

Step 2: Setting Up the Financial Infrastructure

To prevent psychological boundary blurring, you must build a clean, multi-account banking setup. Trying to run this system inside a single checking account is an operational impossibility. You need three completely separate accounts, preferably across two different financial institutions to introduce structural friction.

Account 1: The Revenue Holding Tank (High-Yield Savings)

This account must be opened at a separate, online-only bank to maximize yield and ensure you don’t look at the balance every time you swipe your daily debit card. Every client check, Stripe payment, or cash payment flows directly into this account.

Account 2: The Personal Operations Center (Checking Account)

This is your standard checking account at your primary bank. It handles your automated bills, rent drafts, and daily debit card transactions. This account receives exactly one deposit per month: your calculated salary transfer from the Holding Tank.

Account 3: The Tax Provision Safe (High-Yield Savings)

If you are a 1099 contractor, freelancer, or business owner, taxes are not automatically deducted from your incoming checks. You must maintain an isolated account explicitly to satisfy your quarterly estimated tax obligations.

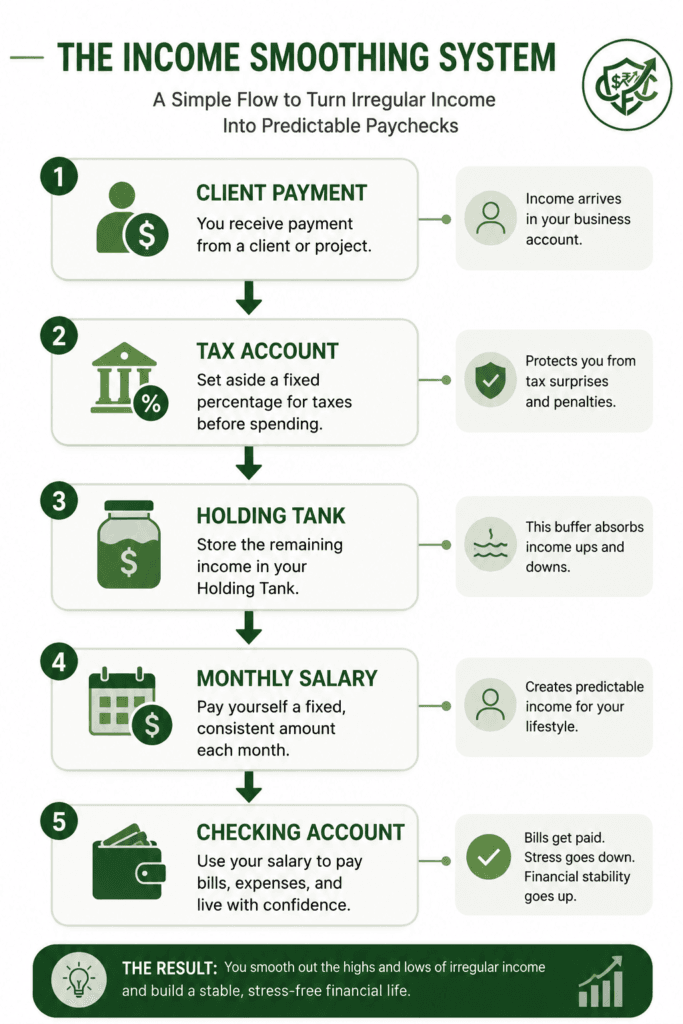

Step 3: Executing the Cash Flow Waterfall

Once your infrastructure is built, you must manage your incoming checks using a strict, automated percentage waterfall system. Every single time a client pays you an invoice, the cash must cascade through these specific operational tiers:

Incoming Invoice Payment

│

├── 1. Tax Account (Set aside 25% to 30% instantly)

└── 2. Remaining Balance ──> Deposited straight into the Holding Tank

The Initial Seed Buffer

The biggest roadblock for beginners starting this system is a lack of initial runway. If your holding tank starts with $0, and you experience a slow month immediately, you cannot pay yourself your designated salary.

To bridge this operational gap, your absolute first goal when experiencing a “feast” month is to aggressively build an Initial Seed Buffer inside the tank equal to one full month of your Ideal Target Salary.

If your target salary is $4,000, your holding tank must be seeded with a baseline $4,000 buffer before you turn on the automated salary drops. Think of this seed money as the physical water required to prime a pump. Once that buffer is locked in, the system becomes entirely self-sustaining.

Case Study: Dismantling the Roller Coaster

Let’s look at a raw, four-month case study to see exactly how the Holding Tank System handles an extremely volatile cash flow in the real world.

Meet Jordan, a freelance service provider. Jordan’s ideal personal monthly salary is set at $4,000. After accounting for a standard 30% tax reserve, Jordan needs to clear a net average of $4,000 a month to stay stable. Jordan manages to secure a $4,000 initial seed buffer in the holding tank before starting the timeline.

Here is exactly how Jordan’s bank accounts interact over a volatile four-month period:

Month 1: The Massive Feast (Gross Income: $9,000)

- Tax Provision (30%): $2,700 moved instantly to the Tax Safe.

- Net Revenue to Holding Tank: +$6,300

- Holding Tank Starting Balance: $4,000 (Seed) + $6,300 = $10,300

- Salary Payout: $4,000 transferred to Personal Checking.

- Ending Holding Tank Balance: $6,300

Month 2: The Average Run (Gross Income: $5,000)

- Tax Provision (30%): $1,500 moved to Tax Safe.

- Net Revenue to Holding Tank: +$3,500

- Holding Tank Starting Balance: $6,300 + $3,500 = $9,800

- Salary Payout: $4,000 transferred to Personal Checking.

- Ending Holding Tank Balance: $5,800

Month 3: The Deep Famine (Gross Income: $1,500)

- Tax Provision (30%): $450 moved to Tax Safe.

- Net Revenue to Holding Tank: +$1,050

- Holding Tank Starting Balance: $5,800 + $1,050 = $6,850

- Salary Payout: $4,000 transferred to Personal Checking.

- Ending Holding Tank Balance: $2,850

Month 4: The Total Drought (Gross Income: $0)

- Tax Provision (30%): $0

- Net Revenue to Holding Tank: $0

- Holding Tank Starting Balance: $2,850

- Salary Payout: Jordan recognizes the drought and drops the salary to the Bare-Bones Floor of $2,500 to protect the ecosystem.

- Ending Holding Tank Balance: $350

Look at the incredible stability of this operational design. Even though Jordan experienced a catastrophic Month 3 and Month 4 where client work nearly vanished, Jordan’s personal life felt completely normal. Jordan never missed a rent payment, never defaulted on a credit card bill, and never experienced a single midnight panic attack. The holding tank quietly absorbed a massive $9,000-to-$0 income collapse without breaking a sweat.

WHEN THIS BACKFIRES: The Operational Pitfalls

The Holding Tank model is a robust piece of financial architecture, but its success relies entirely on user compliance. If you do not respect the strict boundaries of the model, it will backfire aggressively, leaving you in a worse position than when you started.

1. The Gross Revenue Illusion (The Tax Blindspot)

The fastest way to destroy this system is depositing a client’s gross check directly into your holding tank without skimming the tax provision off the top first. If you receive $5,000 and throw all $5,000 into the tank, your buffer looks artificially bloated.

When tax day arrives, you will be forced to execute a massive, emergency withdrawal from the tank to pay the IRS, instantly vaporizing your cash buffer and leaving your personal salary completely unfunded for the next month. Taxes must be paid first at the border; no exceptions.

2. The Creative Compensation Creep

When your holding tank balance climbs to $15,000 after a spectacular quarter, human ego will inevitably whisper: “You’re working incredibly hard. You deserve a big corporate bonus. Let’s transfer an extra $3,000 to checking this month just as a one-time reward.”

The moment you give in to this impulse, you break the system. You have re-coupled your spending to your immediate earnings, exposing yourself to intense vulnerability when the next inevitable downturn occurs. If you want to raise your monthly salary, you must do so based on a rolling 6-month average of sustained revenue growth, not a fleeting spike.

3. The Low-Yield Inertia

If you leave your holding tank cash sitting in a traditional brick-and-mortar savings account earning 0.01% interest, you are actively losing money to inflation. A healthy holding tank should constantly hold several thousand dollars of liquid capital. That capital must be parked in a verified High-Yield Savings Account or a reliable Money Market Fund to capture a competitive return while remaining fully liquid.

Frequently Asked Questions (FAQs)

1. How is a Holding Tank different from a standard emergency fund?

They serve completely separate operational purposes. An emergency fund is designed to sit completely untouched until you face an unpredictable life disaster, like a medical emergency or a broken vehicle transmission. A Holding Tank is an active, working operational clearing account. It is specifically designed to be drawn down and refilled every single month as part of your standard cash flow smoothing process.

2. What should I do if my holding tank runs completely dry?

If a prolonged multi-month famine completely depletes your tank buffer, you must instantly execute your Bare-Bones Budget protocol. You drop your personal salary down to the absolute survival floor, freeze all discretionary spending, and pause your retirement investing. Simultaneously, you must shift 100% of your daily energy away from administrative work and direct it toward active revenue generation—outreach, client pitching, and closing new contracts.

3. Should my business expenses be paid out of the Holding Tank?

No. If you operate as a formal business entity, your business expenses (software subscriptions, marketing, equipment) should be paid out of a dedicated business checking account before the profit is distributed to your personal accounts. The Holding Tank System is strictly a tool to manage your net personal take-home income.

4. Can I use automated apps to manage my variable income budget instead?

While budgeting software can help you track historical spending trends, most traditional budgeting apps fail variable earners because they are built to look forward based on static income inputs. No software can match the reliability of clean banking infrastructure. Manually controlling your allocations builds a deep level of daily financial awareness that apps simply cannot replicate.

5. How many months of salary should I keep in the tank long-term?

For absolute beginners, a 1-month seed buffer is the baseline target to launch the system safely. As your business matures and stabilizes, you should aim to build a 3-to-6-month buffer inside the tank. Having a six-month reservoir means you can survive an entire half-year industry downturn without experiencing a single drop in your personal standard of living.

The Bottom Line

Living with an irregular income does not mean you are condemned to live with permanent financial instability. The roller-coaster lifestyle is not an inevitable byproduct of freelancing or contract work; it is simply the natural result of an outdated budgeting framework.

Stop attempting to force a fluid, dynamic career into a rigid, predictable 50/30/20 rule box. Build your corporate infrastructure. Establish your tax safe, isolate your revenue holding tank at an online bank, and calculate your baseline target numbers with absolute clinical precision. By stepping into the role of a disciplined corporate administrator, you transform your fluctuating income into an elite, wealth-building asset that guarantees long-term financial peace of mind.

Budgeting & Cash Flow Resources

Managing an irregular income requires a different approach than a traditional monthly budget. The following organizations offer practical guidance on budgeting, saving, taxes, and financial planning for self-employed workers and freelancers.

- Consumer Financial Protection Bureau (CFPB) – Managing Your Money – Practical resources for budgeting, saving, building emergency funds, and improving day-to-day money management.

- Internal Revenue Service (IRS) – Self-Employed Individuals Tax Center – Official guidance on estimated taxes, recordkeeping, and tax responsibilities for freelancers, independent contractors, and small business owners.

- MyMoney.gov – Budgeting & Saving – U.S. government financial education covering budgeting strategies, cash flow management, and long-term financial planning.

- SCORE – Free mentoring and educational resources for freelancers and small business owners covering budgeting, cash flow management, and business planning.

- Small Business Administration (SBA) – Manage Your Business Finances – Learn practical strategies for managing business cash flow, forecasting income, and building financial stability.

- Federal Deposit Insurance Corporation (FDIC) – Money Smart – Financial education covering budgeting, saving, banking, and building healthy financial habits.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.