FICO vs. VantageScore: Why Credit Scores Differ Between Apps

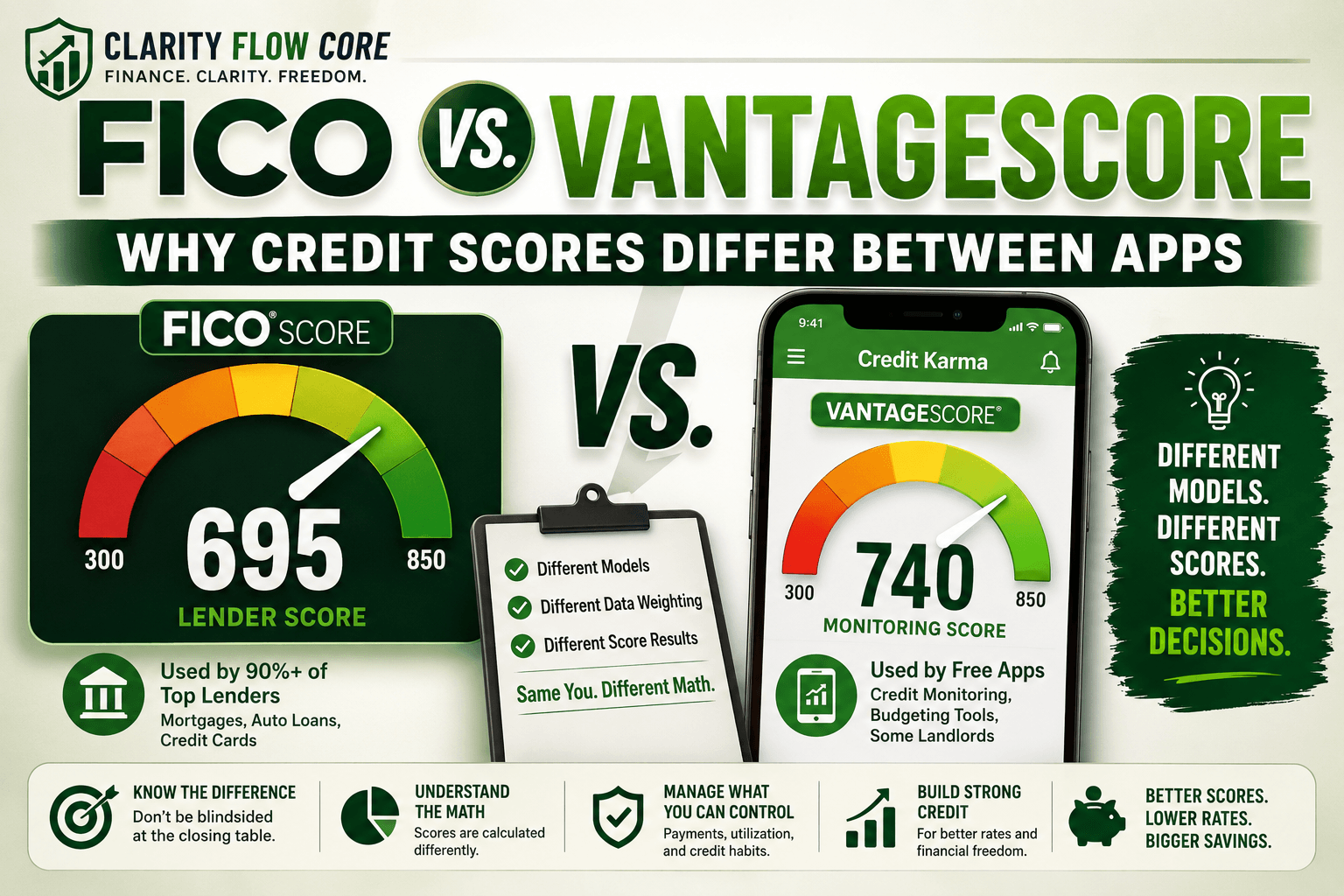

I remember the exact moment I realized the American credit system was broken. I was at a dealership, ready to buy a used Honda. I had checked my Credit Karma app that morning — it proudly showed a 740. I felt untouchable.

I sat down, the finance manager ran my credit, and he pushed a piece of paper across the desk. “Your score is 695,” he said. “That’s going to bump your interest rate by about 3%.”

I felt like I was being scammed. How could 45 points vanish in three hours? The reality is that my score didn’t “drop” — the dealership and my phone were simply using different math. If you want to buy a home or get a car loan in 2026, understanding the friction between FICO vs VantageScore is the only way to avoid being blindsided at the closing table.

You Don’t Have One “Credit Score”

Most people assume their credit score is a single, static number stored in a government vault. It isn’t. You actually have dozens of scores.

Think of Experian, Equifax, and TransUnion as massive libraries. They store the raw data of your financial life — every payment, every debt, and every inquiry. But they don’t do the “grading.” They sell that data to analytics companies like FICO or VantageScore, which apply their own proprietary algorithms to turn your history into a three-digit number.

When comparing FICO vs VantageScore, you are looking at two different companies competing to tell a story about how likely you are to pay back a loan.

The Heavyweight: The FICO Score

The Fair Isaac Corporation (FICO) is the undisputed industry standard. FICO scores remain the most widely used scoring models among mortgage, auto, and credit card lenders. If you are checking Best Credit Cards for Beginners: What Actually Matters, the bank is almost certainly looking at a FICO model.

FICO weights your information into five distinct buckets:

| Component | Weight | What it actually measures |

| Payment History | 35% | Did you pay on time? One 30-day late payment can tank a score by 80 points. |

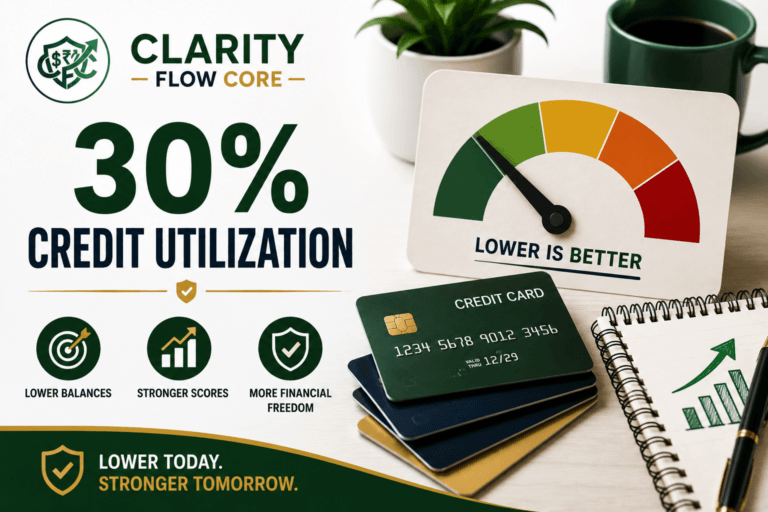

| Amounts Owed | 30% | Your “utilization.” If your limit is $10k and you owe $9k, you look high-risk. |

| Credit Age | 15% | How long have your accounts been open? This is why you should never close your oldest card. |

| New Credit | 10% | Hard inquiries. Applying for three cards in a month makes you look desperate for cash. |

| Credit Mix | 10% | Do you have both revolving credit (cards) and installment loans (auto/student)? |

Credit utilization is one of the biggest factors affecting both FICO and VantageScore models. What Is Credit Utilization — And Why Does It Matter? explains exactly how this ratio is calculated and why lenders pay so much attention to it.

The Challenger: What is a VantageScore?

VantageScore was created jointly by the three credit bureaus themselves to compete with FICO. They wanted their own model so they wouldn’t have to pay FICO licensing fees.

Here is the big catch: Most free monitoring apps (like Credit Karma) use the VantageScore algorithm. It is much cheaper for these apps to provide, which is why it’s free for you. It’s a great tool for tracking your general credit health, but the number you see there is rarely the exact number a traditional lender sees.

When analyzing FICO vs VantageScore, it’s important to realize that VantageScore is often more “volatile.” It might jump 30 points because you paid off a $500 balance, whereas FICO might only move 10 points.

Before we dive into the new mortgage standards, explore exactly how the two models weigh your financial habits differently:

Scoring Model Weight Comparison

Both scoring models heavily penalize late payments, though they may weigh individual credit behaviors differently.

Key insight: VantageScore can generate a credit score with just one month of credit history, making it highly accessible for beginners. FICO requires at least six months of history.

“Trended Data” is the New Standard

The debate of FICO vs VantageScore is moving toward a revolutionary concept called “Trended Data.”

Previously, your score was a snapshot. If you paid off a massive $8,000 credit card bill the day before your score was run, you looked like a hero. Today, newer models — specifically FICO 10T and VantageScore 4.0 — look at the last 24 months of your behavior.

They can see if you are a “Transactor” (someone who pays off their balance in full every month) or a “Revolver” (someone who carries debt and pays interest). If you only make minimum payments, your score will reflect that behavior, even if you are never late. This is why many people see a Credit Score Drop After Paying Off Your Car Loan — the algorithm sees a change in your long-term payment trend.

The mortgage industry has been gradually evaluating newer scoring models, including FICO 10T and VantageScore 4.0. However, many lenders still rely on older mortgage-specific FICO models today.

When the Math Backfires

Trusting your free app blindly is the biggest risk in the FICO vs VantageScore battle.

- The Utilization Illusion: You might think you’re safe at 30% utilization. Lower utilization rates generally correlate with higher scores, and many consumers see the strongest results when utilization remains well below 30%.

- The “Soft Pull” Myth: Checking your own score is always a “soft inquiry” and never hurts you. But letting five different dealerships run a “Hard Inquiry” to shop your rate will definitely cause a temporary dip in both models (though both models do offer a 14-to-45-day “grace period” where multiple auto-loan pulls are counted as one).

- Collection Accounts: VantageScore 4.0 ignores unpaid medical collections entirely. Some older FICO models still penalize you heavily for them.

Practical Steps to Raise Both Scores

Regardless of which model your lender uses, the raw data comes from the same place. Here is how I manage my own score to ensure both numbers stay high:

- Pay Balances Before Statement Closing: If your goal is to reduce reported utilization, paying down balances before your statement closing date can lower the balance reported to the credit bureaus and may improve your score.

- Request a Higher Limit: Call your credit card company and ask for a limit increase. If your limit goes from $5,000 to $10,000 but your spending stays the same, your utilization drops by 50% instantly. Just ensure they aren’t doing a “hard pull” to check.

- Audit Your File: If your scores are wildly different between apps, there is likely a reporting error. You need to know how to read your credit report to ensure a phantom bill isn’t dragging down one specific model.

If you’re still building credit and don’t qualify for a traditional unsecured card, Best Secured Credit Cards for Beginners in 2026 compares beginner-friendly secured cards that report to all three credit bureaus and can help establish a positive payment history.

Which Score Should You Pay Attention To?

If you’re:

- Applying for a mortgage → Focus on mortgage-specific FICO scores.

- Applying for a credit card → Most lenders will use some version of FICO.

- Monitoring general credit health → VantageScore is usually sufficient.

The exact number matters less than the overall trend. Consistent on-time payments and low utilization improve both scoring systems over time.

Frequently Asked Questions (FAQs)

Why is my Credit Karma score different from my lender’s score?

Credit Karma uses VantageScore, while many lenders use FICO models. Both use credit bureau data but calculate scores differently.

Is VantageScore accurate?

Yes. VantageScore is a legitimate credit-scoring model, though it may not be the score used by your lender.

Which credit score do mortgage lenders use?

Many mortgage lenders still rely on mortgage-specific FICO models rather than the VantageScore shown in free apps.

Can checking my own credit score hurt my score?

No. Checking your own score creates a soft inquiry, which does not affect your credit score.

References & Trusted Sources

- FICO Credit Education Center

- VantageScore Resources

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores

- Federal Trade Commission (FTC) – Credit Reports Guide

The Founder-Led Bottom Line

Don’t treat your credit app as a pixel-perfect reality. Treat it as a weather vane. It tells you which way the wind is blowing, but it doesn’t tell you the exact temperature.

If you are getting ready for a major life event — like buying a house or using [How 0% APR Balance Transfers Work — And When They’re Worth It] to clear debt — you need to see your real numbers. Go to myFICO.com and pay the fee to see your actual mortgage and auto scores before applying.

Stop obsessing over a 5-point move on a free app. In the battle of FICO vs VantageScore, the winner is always the person who pays on time, keeps their balances near zero, and understands that the math is just a tool, not a reflection of their worth.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

5 Comments

Comments are closed.