Closing Costs Explained: What Home Buyers Actually Pay

If you are preparing to buy a house, getting closing costs explained clearly and early in the process is one of the most important financial steps you can take. For most first-time home buyers, the down payment takes all the focus. You spend years diligently saving tens of thousands of dollars, carefully tracking your progress, and celebrating when you finally hit your target number.

But then, you find a house, get your offer accepted, and receive a document from your lender that causes your stomach to drop. Along with your down payment, the lender expects an additional $10,000, $15,000, or even $20,000 on closing day.

Where did this extra expense come from? These are your closing costs.

Closing a real estate transaction requires a small army of professionals. You have the lender who processes the loan, the appraiser who values the property, the title company that ensures the legal transfer of ownership, and the local government that records the deed. None of these entities work for free.

In this comprehensive guide, we are going to pull back the curtain on the home buying process. We will break down exactly what these fees are, who gets the money, how much you should expect to pay, and—most importantly—how you can negotiate these fees to keep more cash in your pocket.

Quick Answer: How much are closing costs on a house?

Most home buyers pay between 2% and 5% of the loan amount in closing costs. On a $300,000 mortgage, this typically equals $6,000 to $15,000. Closing costs are separate from the down payment and include lender fees, title fees, appraisal costs, prepaid taxes, and homeowners insurance.

Estimated Closing Costs by Home Price

To give you an immediate idea of what to expect, here is a breakdown of average closing costs based on typical home purchase prices:

| Home Price | Estimated Closing Costs (2%–5%) |

| $200,000 | $4,000 – $10,000 |

| $300,000 | $6,000 – $15,000 |

| $400,000 | $8,000 – $20,000 |

| $500,000 | $10,000 – $25,000 |

What Are Closing Costs?

At its core, “closing costs” is an umbrella term for the various administrative, legal, and setup fees required to execute a real estate transaction and finalize your mortgage.

When you buy a home, you aren’t just handing cash to a seller and taking the keys. Ownership of real property is a strict legal process. The lender needs to guarantee they are making a safe investment, the state needs to record the transaction for tax purposes, and you need legal assurance that the seller actually has the right to sell the home to you.

Important Distinction: Your closing costs are not your down payment. Your down payment is the equity you are putting into the home upfront to reduce the size of your loan. Closing costs are the non-refundable fees paid to actually process the transaction. You must have cash saved for both.

Before committing to these upfront costs, make sure your future monthly housing expenses fit comfortably within your budget by reading How Much of Your Income Should Go Toward Housing Costs?

Closing Costs by Loan Type

The exact percentage you pay depends heavily on the type of mortgage you are using. Government-backed loans often have specialized upfront fees that standard conventional loans do not.

| Loan Type | Typical Closing Costs | Notes |

| Conventional | 2% – 5% | Standard fees; heavily dependent on your lender and credit profile. |

| FHA | 2% – 6% | Includes an Upfront Mortgage Insurance Premium (UFMIP) of 1.75%. |

| VA | 1% – 5% | Zero down payment required, but includes a VA Funding Fee (1.25% to 3.3%). |

| USDA | 2% – 5% | Includes an upfront guarantee fee of 1%. |

| Cash Purchase | ~1% | No lender fees, just title, government, and legal recording fees. |

Unsure which loan is right for you? Read our breakdown on FHA vs Conventional Loan: Which Mortgage is Better for You?

A Breakdown of What Home Buyers Actually Pay

To make sense of the final bill, it helps to group your closing costs into four distinct categories: Lender Fees, Property-Related Fees, Title and Legal Fees, and Prepaid Expenses.

1. Lender Fees

These are the fees your mortgage company charges to process, underwrite, and fund your loan. Because different lenders charge different amounts, this is the category where you have the most room to shop around and negotiate.

- Loan Origination Fee: This is the lender’s primary charge for evaluating your application and preparing your loan. It usually costs between 0.5% and 1% of the loan amount.

- Application Fee: A non-refundable fee some lenders charge simply to process your initial application.

- Underwriting Fee: Underwriters are the financial detectives who verify your income, debt, and credit history to ensure you are a safe borrower. This fee usually ranges from $400 to $900.

- Credit Report Fee: The lender will charge you roughly $30 to $50 to pull your tri-merge credit report from the major bureaus. (Wondering if your score is high enough? Check out What Credit Score Do You Need to Buy a House in 2026?)

- Discount Points (Optional): You can pay money upfront to artificially lower your interest rate for the life of the loan. One “point” usually costs 1% of your loan amount and lowers your interest rate by roughly 0.25%.

2. Property-Related Fees

Before a bank lends you hundreds of thousands of dollars, they need to ensure the property is actually worth the purchase price and structurally sound.

- Appraisal Fee: A third-party appraiser will visit the home to determine its fair market value. Appraisals typically cost $400 to $700 and are often paid via credit card weeks before closing.

- Home Inspection: While technically not always rolled into your final closing document, you will pay a professional inspector $300 to $600 to check the home’s roof, foundation, HVAC, and plumbing.

- Survey Fee: Some states require a professional surveyor to verify the legal property lines and boundaries before a sale. This generally costs $400 to $600.

3. Title and Government Fees

The title process ensures that the person selling the home actually owns it and that there are no secret liens or unpaid contractor bills attached to the property.

- Title Search Fee: The title company scours public records to ensure the home has a “clear title.” This usually costs $200 to $400.

- Lender’s Title Insurance: This insurance policy protects the lender’s financial investment if a title defect is found later. You, the buyer, are required to pay for this policy.

- Owner’s Title Insurance (Optional but Recommended): This policy protects your financial investment if a title dispute arises after you buy the home.

- Recording Fees & Transfer Taxes: Your local government will charge fees to officially record the new deed. Some states also charge a hefty tax when a property changes hands.

4. Prepaid Expenses and Escrow Setup

When you close on a home, your lender establishes an “escrow account.” This is a holding account where the lender stores a portion of your monthly payment to pay your property taxes and homeowners insurance on your behalf. To open this account, you must “pre-fund” it.

- Prepaid Property Taxes: Lenders usually require you to deposit 2 to 6 months of property taxes upfront.

- Prepaid Homeowners Insurance: You will typically be required to pay for your first entire year of homeowners insurance upfront, plus deposit an additional 2 months’ worth into the escrow account.

- Prepaid Daily Interest: You will pay “per diem” (daily) interest for the remaining days of the month in which you close.

Escrow Surprises: Fast forward a year after buying, and your mortgage payment might unexpectedly go up. Learn why this happens in our guide: Why Your Escrow Payment Increased Suddenly (And What to Do).

Real-World Scenario: The True Cost of Buying

Meet David and Elena. They are buying their first home for $350,000. They have saved up $17,500 for a 5% down payment. Their total loan amount is $332,500.

Their lender estimates their closing costs at 3% of the loan amount, which comes out to roughly $9,975.

Here is what their closing cost breakdown might look like:

Lender Fees:

- Origination & Underwriting: $1,600

- Credit Report & Flood Certification: $75

Property Fees:

- Appraisal: $500 (Paid in advance)

- Home Inspection: $450 (Paid in advance)

Title & Government Fees:

- Title Search & Settlement Fee: $800

- Lender’s Title Insurance: $900

- Owner’s Title Insurance: $600

- Government Recording Fees: $150

Prepaids & Escrow Setup:

- 1 Year Homeowners Insurance Upfront: $1,200

- Escrow Buffer (2 Months Insurance): $200

- Escrow Buffer (4 Months Property Tax): $2,400

- Prepaid Daily Interest: $600

- Total Closing Costs: $9,475

When David and Elena go to the closing table, they must bring a cashier’s check for their down payment plus their closing costs, meaning they actually need $26,975 to finalize the purchase.

Calculate Your True Cash Needed

Don’t get blindsided on closing day. Use our free Mortgage Affordability Calculator to input your target home price and instantly see your estimated closing costs and total cash required.

Can You Negotiate or Lower Your Closing Costs?

If seeing that $26,975 total made you nervous, take a deep breath. While you cannot change government taxes or third-party appraisal fees, there are several powerful ways to reduce your out-of-pocket burden.

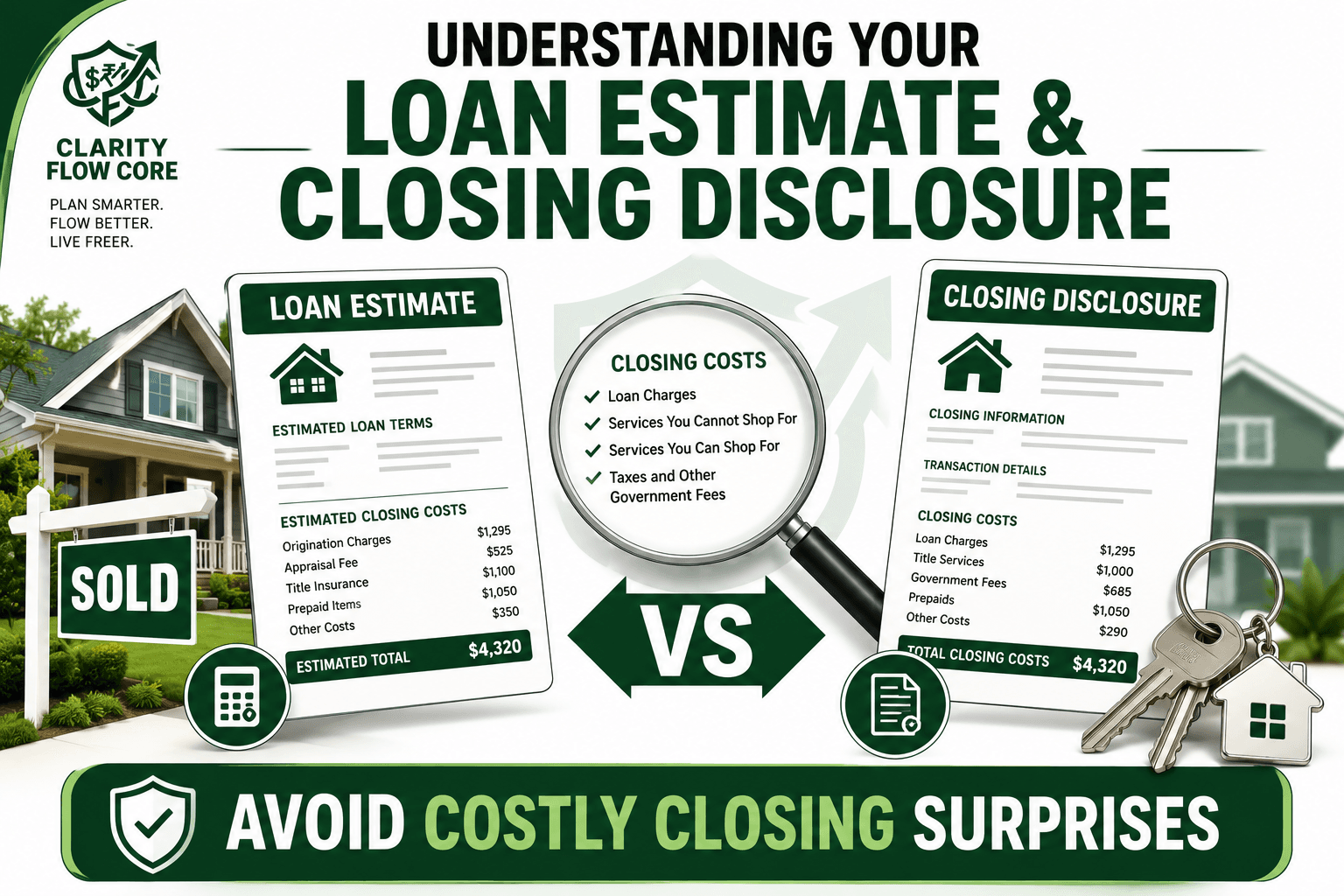

1. Shop Around and Compare Loan Estimates

This is the single biggest mistake home buyers make. By law, within three days of applying for a mortgage, a lender must provide you with a Loan Estimate (LE). Apply with at least three different lenders on the exact same day and put their Loan Estimates side-by-side. One lender might charge a $1,500 origination fee, while another charges $0.

2. Ask for Seller Concessions (Seller Credits)

You can ask the seller to pay for a portion of your closing costs as part of your purchase offer. For example, instead of offering $350,000 for a home, you might offer $355,000 but ask the seller to provide $5,000 in “seller credits” toward your closing costs. The seller still nets the same amount, but you roll $5,000 of your upfront cash requirement into your mortgage.

3. Opt for Lender Credits

If you are incredibly tight on cash, you can ask your lender for a “lender credit.” The lender covers a large portion of your closing costs upfront. In exchange, you agree to take a higher interest rate for the life of the loan.

4. Shop for Your Own Title Company

On page two of your Loan Estimate, you will see a section titled “Services You Can Shop For.” You do not have to use the title company your lender recommends. Calling a few local, independent title companies can often save you hundreds of dollars.

Common Beginner Mistakes

The weeks leading up to closing day are stressful. To ensure the transaction doesn’t fall apart, avoid these common pitfalls:

- Mistake 1: Draining Your Bank Account to Zero. Never empty your savings entirely to cover closing costs. You need an emergency fund intact on day one. Run your numbers through our Advanced Emergency Fund Analyzer.

- Mistake 2: Taking Out New Debt Before Closing. Do not buy new furniture on a credit card or finance a new car. Your lender will pull your credit one final time before closing. If your debt-to-income ratio spikes, they will deny the loan. Read What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline to understand this sensitive window.

- Mistake 3: Overestimating Affordability. Being approved for a loan does not mean you can comfortably afford the monthly payment. Use our First-Time Homebuyer Guide: How Much House Can You Really Afford? alongside the Debt-to-Income Analyzer & Loan Readiness Planner to verify your actual lifestyle budget.

- Mistake 4: Believing in “No-Closing-Cost” Mortgages. Zero-closing-cost loans are an illusion. The lender is simply paying the fees upfront and then baking the cost into your loan by giving you a much higher interest rate.

Your Action Plan: How to Prepare for Closing Day

You found the house. Your offer is accepted. Here is exactly what you need to do to handle your closing costs smoothly:

- Scrutinize Your Loan Estimate (LE): Review it immediately. Check the origination fees and ensure the interest rate matches what you locked in.

- Wait for the Closing Disclosure (CD): By federal law, your lender must provide a Closing Disclosure at least three business days before closing. Compare it side-by-side with your original Loan Estimate. Demand an explanation if fees drastically increased.

- Finalize Your Funds: The title company will tell you the exact amount needed. You must arrange a wire transfer or get an official Cashier’s Check. Personal checks are not accepted.

- Beware of Wire Fraud: Hackers frequently intercept real estate emails and send fake wiring instructions. Never wire money based solely on an email. Always call your title company using a verified phone number to verbally confirm the routing numbers.

Still on the fence about buying? Check out our updated guide on Renting vs Buying a Home in 2026: The Math You Need to Know before you commit to a 30-year mortgage.

Frequently Asked Questions (FAQ)

Can I negotiate closing costs?

Yes. While you cannot negotiate government taxes or third-party fees (like the appraiser), you can heavily negotiate “Lender Fees” such as origination and application charges. You can also negotiate with the seller to pay a portion of your costs through seller concessions.

What closing costs are paid by the seller?

The seller typically pays 6% to 10% of the home’s sale price in closing costs. The vast majority of this covers the real estate agent commissions for both the buyer’s and seller’s agents. Sellers also pay their share of property taxes up to the closing date, and specific state transfer taxes.

Are closing costs included in the down payment?

No. Closing costs and your down payment are completely separate expenses. The down payment goes toward your equity in the home. Closing costs go to the professionals processing the loan and title transfer. You must have enough cash to cover both on closing day.

When do I pay closing costs?

The bulk of your closing costs are paid on “closing day” (the day you sign the final paperwork and get the keys). You pay this as one lump sum (down payment + closing costs) via a cashier’s check or wire transfer to the title company. A few minor costs, like the appraisal and inspection, are usually paid a few weeks prior via credit card.

Can closing costs be rolled into the mortgage?

For standard Conventional loans, generally no. However, if you are using an FHA loan, USDA loan, or VA loan, some specific upfront funding fees can be added to your total loan balance. Alternatively, you can use “lender credits” (taking a higher interest rate) to offset the cash requirement on any loan type.

Are closing costs tax-deductible?

Most closing costs for buying a personal residence are not tax-deductible (e.g., appraisal fees, title insurance, origination fees). However, you can usually deduct prepaid mortgage interest and any prepaid property taxes you funded at closing. If you bought “discount points,” those are also often deductible. Always consult a CPA for tax advice.

Conclusion

Getting closing costs explained before you start house hunting is the ultimate stress-reliever. When you know exactly what fees are coming and why they exist, the mystery of the mortgage process disappears.

Remember, knowledge is your best negotiating tool. Do not accept the first Loan Estimate you receive without question. Shop around, compare origination fees, and ask your real estate agent about the possibility of seller concessions. By actively managing your closing costs and protecting your cash reserves, you ensure that closing day remains a moment of celebration, not a moment of financial panic. You’ve worked incredibly hard to reach the milestone of homeownership—now you have the blueprint to protect your money at the finish line.

References

- Consumer Financial Protection Bureau (CFPB): Understanding your Loan Estimate and Closing Disclosure

- U.S. Department of Housing and Urban Development (HUD): Buying a Home Guide

- Federal Reserve: Consumer Guide to Mortgages and Settlement Costs

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.