How Mortgage Pre-Approval Actually Works

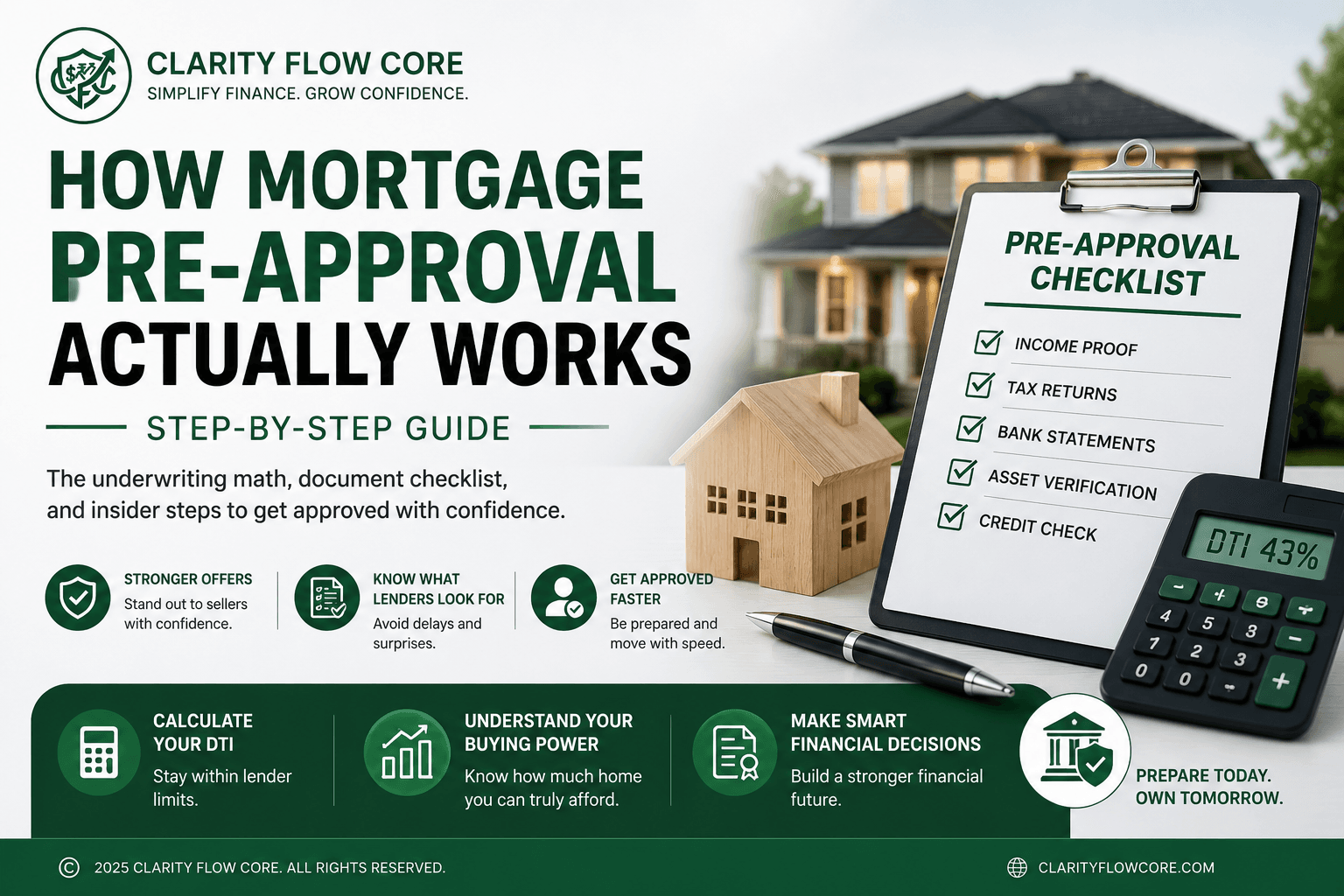

Quick Answer How mortgage pre-approval actually works: A mortgage pre-approval is a formal, written commitment from a lender stating exactly how much money they are willing to lend you. To get it, an underwriter verifies your W-2s, tax returns, bank statements, and executes a hard credit pull. It is valid for 60 to 90 days. Without this letter in hand, real estate agents will not show you houses, and sellers will instantly reject your offers.

You spend three weeks scrolling through real estate apps. You finally find the perfect property—the right neighborhood, a massive backyard, and a price that fits your budget. You rush to call a real estate agent to put in an offer.

The agent asks you one simple question: “Do you have your pre-approval letter?”

You say no, assuming you can just figure out the financing after the seller accepts your offer. The agent sighs, tells you they can’t submit an offer without one, and by the time you scramble to contact a bank two days later, the house is already sold to someone else.

This is the brutal reality of the modern real estate market.

Buying a house is not like buying a car. You do not shop first and secure financing second. The entire operational sequence is reversed. You must prove you have the capital before you are allowed to step foot on the playing field.

If you are preparing to buy a home, you cannot afford to misunderstand this process. Here is the definitive, step-by-step breakdown of how mortgage pre-approval actually works, the exact math the bank uses to judge you, and the critical mistakes that will cause your lender to pull your funding at the last minute.

The Great Delusion: Pre-Qualified vs. Pre-Approved

The single biggest mistake first-time homebuyers make is confusing “pre-qualification” with “pre-approval.” Banks intentionally use these terms interchangeably in their marketing, but in the operational world of real estate, they are completely different animals.

Prequalification (The Guess)

Prequalification is a superficial estimate. You log onto a bank’s website, type in a few numbers (e.g., “I make $80,000 a year and have a 720 credit score”), and the algorithm instantly spits out a certificate saying you are “pre-qualified for $400,000.”

Nobody verified your income. Nobody checked your tax returns. It is based entirely on the honor system. Because of this, a pre-qualification letter is completely worthless to a home seller. It carries zero financial weight.

Pre-Approval (The Verification)

Pre-approval is a rigorous, invasive audit of your financial life.

When you apply for a pre-approval, a human being (the underwriter) or a highly sophisticated automated underwriting system demands physical proof of every single claim you make. They pull your official credit report, scrutinize your bank statements for weird deposits, and verify your employment directly with your HR department.

When a lender hands you a pre-approval letter, they are legally signaling to the market: “We have audited this buyer’s life, and we guarantee we will lend them $400,000, provided the house they choose passes an appraisal.”

The Operational Timeline: Step-by-Step

Understanding how mortgage pre-approval actually works requires looking at the actual chronological timeline of the bank’s internal processes. Here is exactly what happens when you hit “Submit” on a mortgage application.

Step 1: The Document Dump

The moment you apply, the loan officer will request a massive stack of financial documents. Do not wait until the last minute to find these. You should have a digital folder on your desktop containing:

- Income Proof: The last 30 days of pay stubs and the last two years of W-2 forms.

- Tax Returns: The last two years of your full 1040 federal tax returns. (Note: If you are a freelancer, independent contractor, or business owner, this is where the audit gets intense. The bank will require your Schedule C and potentially a year-to-date Profit & Loss statement to verify your irregular income).

- Asset Verification: The last 60 days of bank statements (checking, savings, and investment accounts) to prove you actually have the cash required for the down payment and closing costs.

- Identification: Your driver’s license and Social Security number.

Step 2: The Hard Credit Pull

Once the documents are submitted, the bank executes a “hard inquiry” on your credit report. They pull data from all three major bureaus (Experian, Equifax, TransUnion) and use the median score to determine your mortgage interest rate. This hard pull will temporarily drop your credit score by 3 to 5 points, but it is a necessary, unavoidable step in the process.

Step 3: The Underwriting Math (DTI Calculation)

This is the most critical stage of the entire process. The underwriter takes your verified income and compares it against your existing debt to calculate your Debt-to-Income (DTI) Ratio.

The bank wants to know exactly how much of your monthly paycheck is eaten up by debt obligations before they allow you to take on a massive new mortgage.

Most conventional lenders enforce a strict 43% to 45% DTI ceiling. If your total monthly debt payments (including the proposed new mortgage, property taxes, car loans, and minimum credit card payments) exceed 45% of your gross (pre-tax) monthly income, you will be instantly denied, regardless of how high your credit score is.

Advanced Mortgage DTI Calculator

Enter your monthly numbers to see exactly how an underwriter views your profile.

Front-End DTI

27.5%

(Housing Only)Total Back-End DTI

37.5%

*This calculator provides educational estimates only and does not guarantee mortgage approval.

Step 4: The Issuance of the Letter

If your DTI is safe, your cash is verified, and your credit is solid, the loan officer issues the golden ticket: The Pre-Approval Letter.

This letter will state your maximum loan amount, the specific type of loan you are approved for (Conventional, FHA, VA), and an expiration date. Pre-approval letters are typically valid for 60 to 90 days. If you do not find a house within that window, the bank will have to refresh your credit report and request updated pay stubs to issue a new letter.

Case Study: The $500 Car Payment Disaster

To truly grasp how mortgage pre-approval actually works, we have to look at how fiercely the Debt-to-Income (DTI) math impacts your purchasing power.

Meet Mark and Sarah. They have a combined gross income of $10,000 per month. They have excellent credit, $60,000 saved for a down payment, and zero credit card debt. They want to buy a $450,000 house, which would result in a total estimated monthly housing payment of $3,200.

Scenario A: Debt-Free If Mark and Sarah have no other debts, their DTI calculation is simple:

- Proposed Mortgage: $3,200

- Total Monthly Debt: $3,200

- Gross Income: $10,000

- DTI Ratio: 32%

- The Verdict: They easily clear the 45% ceiling. The bank happily issues a pre-approval letter for the $450,000 home.

Scenario B: The Luxury Car Trap Now, let's rewind. Six months before applying for the mortgage, Mark decided to lease a luxury SUV, locking in an $800 monthly car payment. Sarah also has a $400 monthly student loan payment. They still make the exact same $10,000 a month, and they still want that same $450,000 house.

Let's run the bank's operational math:

- Proposed Mortgage: $3,200

- Auto Loan: $800

- Student Loans: $400

- Total Monthly Debt: $4,400

- Gross Income: $10,000

- DTI Ratio: 44%

- The Verdict: They are dangerously close to the 45% maximum cutoff. If property taxes or homeowner's insurance rates in that neighborhood are slightly higher than expected, pushing the housing payment to $3,400, their DTI hits 46%.

The underwriter denies the loan. Because Mark wanted to drive a luxury SUV, the bank legally barred them from buying their dream home. Every $100 you carry in monthly consumer debt permanently destroys roughly $15,000 to $20,000 of mortgage purchasing power.

WHEN THIS BACKFIRES: The Operational Traps

A pre-approval letter is not a bulletproof guarantee; it is a conditional promise. Between the day you receive the letter and the day you finally close on the house, your financial life is under a microscope. If you make any sudden moves, the bank will revoke your pre-approval days before closing, causing you to lose the house and your earnest money deposit.

Here is exactly when this process backfires aggressively:

1. The "New Furniture" Credit Trap

You finally get an offer accepted on a house. You are so excited that you drive straight to a furniture store and finance $8,000 worth of new couches and bedroom sets using their "0% Down for 12 Months" store credit card.

You just committed real estate suicide.

When you financed that furniture, you opened a new line of credit. Three days before you close on your house, your mortgage lender will do a final "soft pull" on your credit report to ensure nothing has changed. They will see the new $8,000 debt. The underwriter will rerun your DTI math. Because the new furniture payment pushed your DTI over the 45% limit, the bank cancels your mortgage. You lose the furniture, you lose the house, and you lose your deposit. Never open new credit while under contract.

2. The Job Change Trap

Your pre-approval was based on the specific salary and stability of your current job. If you quit your job to become a freelancer, or move to a completely different industry two weeks before closing, the bank's risk model completely shatters.

Even if your new job pays more money, underwriters hate unpredictability. They typically require two years of consistent history in the same industry. If you change your employment structure during the home buying process, your pre-approval is instantly voided.

3. The Mattress Money Deposit (Unsourced Funds)

Under federal anti-money laundering laws, banks must verify the exact origin of every single dollar you use for your down payment.

If you receive your pre-approval, and then suddenly deposit $15,000 of physical cash that you had hidden in a safe, or a random $20,000 Venmo transfer from an uncle, the underwriter will halt the loan. Any large, unusual deposit that cannot be directly traced to your payroll requires a formal "Letter of Explanation" and a deeply invasive audit. Keep your money exactly where it is until the bank tells you to move it.

The Strategic Fix: Protecting Your Letter

To ensure your pre-approval seamlessly transitions into a final "Clear to Close," you must place your financial life into a cryogenic freeze.

From the day you submit your initial application until the day the keys are placed in your hand, you must follow the Four Iron-Clad Rules of Underwriting:

- Do not apply for a single new credit card, auto loan, or personal loan.

- Do not close any old credit accounts (this shrinks your available credit and spikes your utilization ratio).

- Do not change jobs, quit your job, or switch from W-2 to 1099 contractor status.

- Do not move large amounts of cash between different bank accounts without notifying your loan officer first.

Frequently Asked Questions (FAQs)

1. Does getting pre-approved commit me to using that specific bank? No. A pre-approval letter is not a binding contract on your end. It simply proves your purchasing power to a seller. Once your offer on a house is accepted, you have a window of time to "shop your rate" and apply with other lenders or mortgage brokers to see who offers you the lowest interest rate and closing costs.

2. Will multiple mortgage inquiries destroy my credit score? No, provided you do them quickly. The credit bureaus understand that smart consumers shop around for the best mortgage rate. If you apply for pre-approval with three different lenders within a 14-to-45-day window (depending on the scoring model), the algorithm groups all three hard pulls together and counts them as a single inquiry, resulting in only one minor ding to your score.

3. Should I max out my pre-approval amount? Absolutely not. The bank's underwriter calculates the absolute maximum mathematical threshold you can survive without defaulting on the loan. They do not factor in your desire to travel, save for retirement, or eat at restaurants. If the bank pre-approves you for $500,000, your personal target budget should safely be around $350,000 to $400,000 to ensure you don't end up entirely "house poor."

4. How long does the pre-approval process take? If you have all your W-2s, bank statements, and tax returns digitized and ready to upload, a modern digital lender can issue a fully verified pre-approval letter within 24 to 48 hours. If you are self-employed or have a highly complex corporate income structure, manual underwriting can take up to a week.

5. What is a "Conditional Approval"? When you go under contract on a house, your pre-approval upgrades to a "Conditional Approval." This means the bank has formally approved the loan, on the condition that the house appraises for the purchase price, the title is clear of liens, and you provide a few final updated pay stubs before closing day.

The Bottom Line

Understanding how mortgage pre-approval actually works shifts the power dynamic of real estate back into your hands.

Stop viewing the bank as an adversary and start treating the underwriter as your operational partner. By proactively gathering your tax documentation, protecting your credit utilization, and understanding the strict boundaries of your Debt-to-Income ratio, you eliminate the stress of the home-buying process. Secure the letter before you ever step foot into an open house, freeze your financial activity, and walk into negotiations with the absolute certainty that your capital is locked and loaded.

Home Financing Resources

Mortgage pre-approval is one of the most important steps in the homebuying process. These trusted resources explain how lenders evaluate borrowers, what documents you'll need, and how to prepare for a successful mortgage application.

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Learn about mortgage pre-approval, loan estimates, closing costs, and the complete homebuying process.

- Consumer Financial Protection Bureau (CFPB) – Your Home Loan Toolkit – A practical guide covering mortgage shopping, loan comparisons, underwriting, and what to expect before closing.

- Fannie Mae – HomeView® – Free homebuyer education covering mortgage qualification, debt-to-income ratios, budgeting, and preparing to purchase a home.

- Freddie Mac – My Home – Educational resources explaining mortgage pre-approval, credit requirements, down payments, appraisals, and closing.

- U.S. Department of Housing and Urban Development (HUD) – Find homebuying guidance, HUD-approved housing counselors, and resources for first-time buyers.

- Federal Housing Administration (FHA) – Learn about FHA loan requirements, borrower qualifications, down payment options, and mortgage insurance.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.