First-Time Homebuyer Guide: How Much House Can You Really Afford?

If you are currently asking yourself, “how much house can I afford,” you are entirely normal. For decades, buying a house has been the ultimate symbol of financial stability. It represents adulthood, equity, and a place to finally paint the walls whatever color you want without asking a landlord for permission.

But in the modern housing market, the process feels less like a dream and more like a financial obstacle course. With property values sitting at historic highs and mortgage interest rates remaining stubborn, the excitement of browsing real estate apps can quickly turn into a panic attack when you look at the estimated monthly payments.

The most common, devastating mistake first-time homebuyers make isn’t buying the wrong house in the wrong neighborhood—it is buying too much house. If you drain your savings and stretch your monthly budget to the absolute breaking point just to get the keys, you end up “house poor.” You have a beautiful kitchen with granite countertops, but you cannot afford to buy groceries to put in the fridge.

If you are ready to stop renting and buy a home, you cannot rely on guesswork. Here is the ultimate first-time homebuyer guide to understanding the operational math, uncovering the hidden costs of property ownership, and figuring out exactly “how much house can I afford” without destroying your cash flow.

⚡ Quick Answer

- How much house you can afford depends on your income, debts, down payment, property taxes, insurance costs, and maintenance expenses.

- Many financial professionals use the 28/36 rule, which recommends spending no more than 28% of gross income on housing and no more than 36% on total debt payments.

The Danger of the Bank’s Math vs Your Reality

When people ask, “how much house can I afford,” they usually start by going to a bank or a mortgage broker to get a “Pre-Approval Letter.” The bank looks at your W-2 income, your credit score, and your debts, and then hands you a piece of paper saying, “Congratulations! You are approved to buy a $450,000 house!”

Do not take the bait.

The bank’s pre-approval number is the absolute, mathematical maximum they are legally allowed to lend you based on their corporate risk tolerance. The bank does not care if you want to take a vacation next year. They do not care if you want to put money into your Roth IRA for retirement. They do not care if you like eating at restaurants on the weekend.

Furthermore, the bank’s math is based on your gross income—the massive number before the IRS takes out taxes. (To understand your true take-home pay, read our guide on W-4 Form Explained: How Tax Withholding Actually Works). But you pay your mortgage with your net income (the much smaller number that actually lands in your checking account).

If you borrow the absolute maximum the bank offers you, your mortgage payment will consume your entire life. A good starting point is determining what percentage of your income should realistically be allocated to housing before shopping for homes. See How Much of Your Income Should Go Toward Housing Costs? for practical budgeting guidelines. You must set your own personal, operational budget ceiling before you ever step foot into an open house.

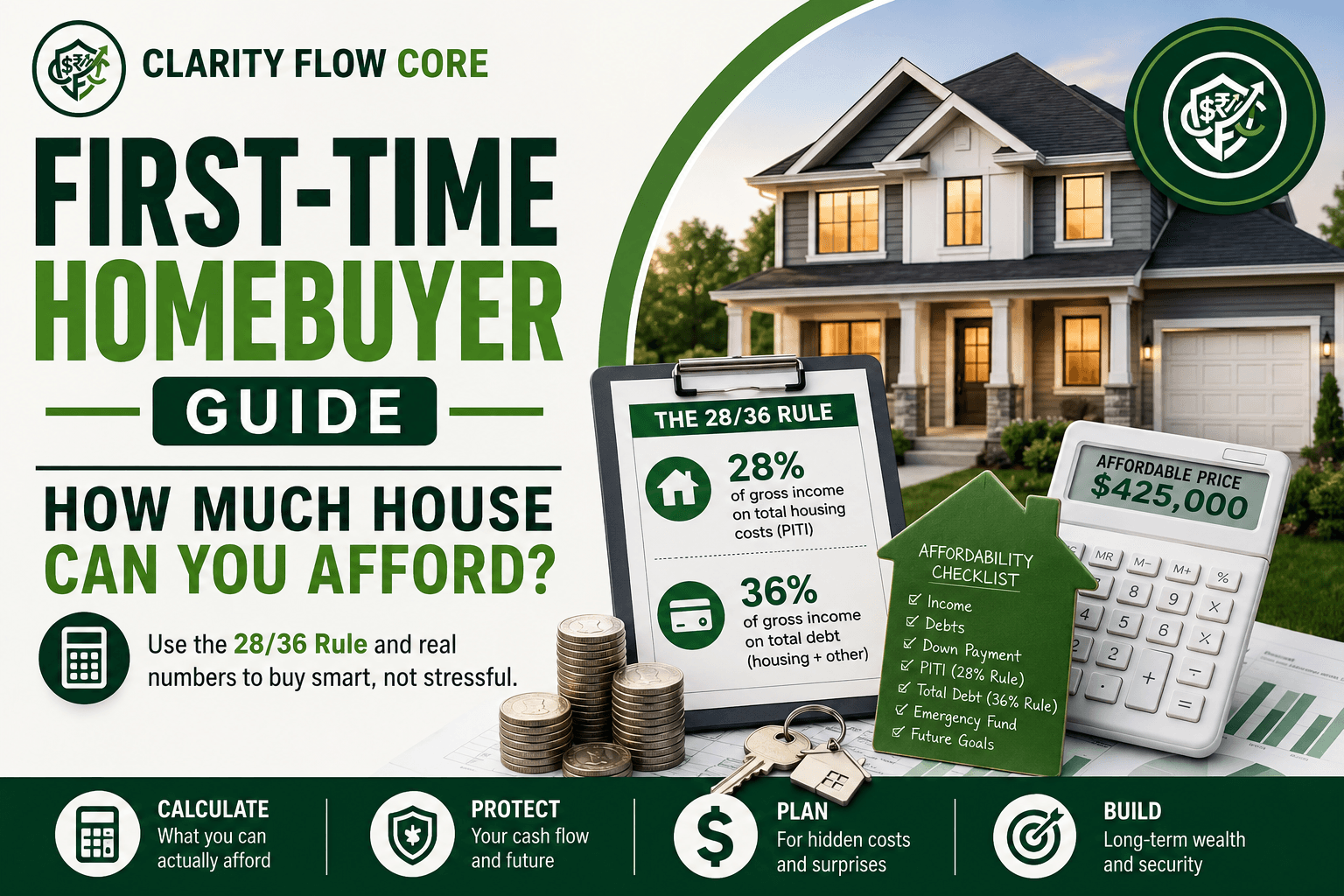

The Golden Standard: The 28/36 Rule Explained

If you shouldn’t listen to the bank’s maximum number, how do you calculate a safe budget? Financial experts rely on a classic, mathematically sound formula called the 28/36 Rule. It acts as a set of financial guardrails to keep you safe from foreclosure. The true mathematical answer to “how much house can I afford” relies entirely on these two percentages.

The 28% Front-End Rule (The Housing Limit)

This rule states that your total housing costs should never exceed 28% of your gross monthly income. If you’re wondering whether this percentage is appropriate for your own situation, read How Much of Your Income Should Go Toward Housing Costs? for a deeper breakdown of how housing budgets vary based on income, debt, and financial goals.

Notice it says total housing costs, not just the principal mortgage. This 28% limit must include your principal loan payment, the interest, your property taxes, and your homeowner’s insurance (collectively known in the banking world as PITI).

The Math: If your household makes $100,000 a year before taxes, your gross monthly income is $8,333. Multiply that by 0.28, and your absolute maximum housing budget is $2,333 per month.

The 36% Back-End Rule (The Debt Limit)

This rule states that your total housing costs plus all of your other monthly debt payments should never exceed 36% of your gross monthly income. This includes your new mortgage, plus your student loans, car payments, and minimum credit card payments.

The Math: Using that same $100,000 household income ($8,333 a month), your total combined debt payments cannot exceed $3,000 per month (36%).

If your targeted new mortgage is $2,333, but you also have a $500 car payment and a $400 student loan payment, your total monthly debt is $3,233. You have broken the 36% rule. To calculate “how much house can I afford” safely in this scenario, you either need to look at cheaper homes, use the Debt Avalanche vs. Debt Snowball method, or leverage 0% APR Balance Transfers: How They Actually Work to wipe out your high-interest debt before you apply for a mortgage.

Here is how the 28/36 Rule scales based on household income:

| Gross Annual Income | Monthly Gross | Max Housing Payment (28%) | Max Total Debt (36%) |

| $60,000 | $5,000 | $1,400 | $1,800 |

| $100,000 | $8,333 | $2,333 | $3,000 |

| $150,000 | $12,500 | $3,500 | $4,500 |

(Note: Instead of running these percentages by hand, you can use our interactive affordability calculators to plug in your exact numbers).

The Down Payment Dilemma

Our parents’ generation was taught that you absolutely must have a 20% down payment before buying a house. Today, saving 20% on a $400,000 starter home means scraping together $80,000 in liquid cash. For most first-time buyers, that is incredibly unrealistic and drastically changes the calculation for “how much house can I afford.”

The good news is that you do not need 20% down. You have heavily subsidized options:

- FHA Loans: Backed by the Federal Housing Administration, these allow you to put down as little as 3.5% for qualified borrowers. (This is the same vehicle investors use in How to House Hack: The FHA Loan Strategy Explained).

- Conventional Loans: Many modern lenders offer first-time buyer programs for just 3% to 5% down if your credit score is strong.

- VA Loans: Eligible veterans, active-duty service members, and certain surviving spouses may qualify for VA loans with no down payment requirement.

The Catch: Private Mortgage Insurance (PMI)

If you put down less than 20%, the bank views you as a slightly higher risk of default. To protect themselves, they will force you to pay for Private Mortgage Insurance (PMI) every single month. This is an extra fee rolled into your mortgage that protects the bank (not you) if you stop paying.

PMI can easily add $100 to $300 to your monthly payment. Therefore, when asking “how much house can I afford,” you must deduct this extra insurance cost from your 28% housing limit. You literally get less house because you are paying for the bank’s insurance policy.

Beyond the Mortgage: The Hidden Costs of Homeownership

When you are renting an apartment and the refrigerator dies, you call the landlord. It is their problem, and it is their money. When you own a house, you are the landlord. Every broken pipe, every leaky roof, and every dead HVAC system is a direct hit to your bank account.

Before you finalize your budget, you must account for the hidden costs of property ownership. If you fail to account for these costs, you can place significant strain on your budget and long-term financial goals.

1. The 1% Maintenance Rule

Financial planners universally recommend setting aside 1% of your home’s total value every single year for repairs and maintenance. If you buy a $300,000 home, you should expect to spend roughly $3,000 a year (or $250 a month) fixing things. One year you might spend nothing, but the next year the central air conditioning might blow out, costing $6,000.

2. HOA Fees

If you buy a condo, a townhouse, or a home in a modern planned community, you will be forced to join a Homeowners Association (HOA). These monthly fees pay for community landscaping, roof maintenance, and neighborhood pools. HOA fees can range from $50 a month to over $600 a month. This fee drastically alters the math of “how much house can I afford,” because HOA fees legally count toward your 28% housing limit.

3. Closing Costs (The Big Shock)

This is the biggest shock for first-time buyers. The down payment is not the only cash you need on closing day. You also have to pay “closing costs,” which are fees for the real estate lawyers, title searches, municipal taxes, appraisals, and loan origination fees.

Closing costs typically run between 2% and 5% of the total loan amount. On a $300,000 house, be prepared to write an entirely separate check for $6,000 to $15,000 just to close the deal. Make sure your buffer is fully funded and ready by reading Emergency Fund Basics: How Much Cash Should You Keep?.

When This Backfires: The Operational Traps

Even if the math looks perfect on paper, homeownership carries massive operational risk. Here is exactly when buying a house backfires and ruins your net worth:

1. The Property Tax Reassessment Trap

This destroys thousands of new homeowners every year. When you look at a house on Zillow, it shows you what the previous owner paid in property taxes. You run your math based on that number.

However, when you buy the house for a new, much higher price, the local municipality will reassess the property value. The following year, your property taxes might double. Your $2,000 mortgage suddenly becomes a $2,600 mortgage because of an “Escrow Shortage.” Re-evaluating “how much house can I afford” after a tax crisis is a nightmare. Always run your math based on the purchase price of the home, not the previous owner’s tax bill.

2. Dual-Income Dependency

If it takes 100% of both your income and your spouse’s income to safely afford the mortgage, you are in a highly fragile financial position. The most dangerous answer to “how much house can I afford” is the one that assumes nothing will ever go wrong. If one of you loses a job, takes a pay cut, or decides to stay home with a new baby, you will instantly default on the loan. Ideally, you should aim to afford the mortgage on just one income, or keep a massive 6-month cash reserve to buffer against job loss.

The Stress-Test: How to Practice Your Mortgage

If you have run all the math and you think you have found your magic number, there is one final test you should run before calling a real estate agent. You need to “practice” your new mortgage.

Let’s say you currently pay $1,500 a month in rent, but your estimated new mortgage payment will be $2,400. For the next three months, take that $900 difference and automatically transfer it into your High-Yield Savings Account on the 1st of every month.

Live your life as if that $900 is gone forever. This is the only way to determine “how much house can I afford” in real life.

Do you feel completely broke? Are you constantly stressed about buying groceries? Did you have to put an emergency expense on a credit card because your cash was too tight? If the answer is yes, you cannot comfortably afford the house, regardless of what the 28/36 rule says.

If the answer is no, and you easily adapted to the tighter budget without racking up consumer debt, you are financially ready to buy. Plus, at the end of the three-month experiment, you will have an extra $2,700 saved up to help cover your closing costs.

Frequently Asked Questions (FAQs)

How much should I put down on my first home?

While 20% down can help avoid PMI, many first-time buyers purchase homes with significantly smaller down payments through FHA, VA, or conventional loan programs.

What credit score do I need to buy a house?

Requirements vary by lender and loan type, but stronger credit profiles generally qualify for better interest rates.

Should I buy a house with less than 20% down?

Many buyers do. However, you should understand PMI costs and maintain adequate emergency savings.

What is included in a monthly mortgage payment?

Mortgage payments often include principal, interest, property taxes, homeowners insurance, and sometimes mortgage insurance.

How much should I keep in savings after closing?

Many financial planners recommend maintaining an emergency fund of 3 to 6 months of expenses even after making a down payment.

References & Trusted Sources

Buying a home is one of the largest financial decisions most people will ever make. These trusted government agencies and nonprofit organizations provide reliable information on mortgage affordability, loan programs, homebuyer education, and consumer protections.

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Learn how to compare mortgage offers, understand closing costs, estimate monthly payments, and navigate every stage of the homebuying process.

- Consumer Financial Protection Bureau (CFPB) – Your Home Loan Toolkit – A practical guide covering mortgage shopping, loan estimates, closing disclosures, and common mistakes first-time buyers should avoid.

- U.S. Department of Housing and Urban Development (HUD) – Access homebuyer education, HUD-approved housing counseling agencies, and resources for first-time homebuyers.

- Federal Housing Administration (FHA) – Learn about FHA loan requirements, minimum down payments, mortgage insurance, and eligibility guidelines for qualified borrowers.

- Fannie Mae – HomeView® – Free online homebuyer education covering budgeting, mortgage qualification, debt-to-income ratios, and preparing to purchase a home.

- Freddie Mac – My Home – Educational resources explaining affordability, down payments, mortgage options, appraisals, closing costs, and responsible homeownership.

- Federal Reserve – Household debt and consumer finance reports that provide insight into mortgage debt, borrowing trends, and the U.S. housing market.

The Bottom Line

Buying your first home is one of the most exciting milestones of your life, but a house should be a blessing, not a financial prison. Do not let a real estate agent pressure you into a bigger budget, and do not let FOMO (Fear Of Missing Out) cause you to drain your retirement accounts.

Calculate your 28/36 ratios, factor in the hidden costs of maintenance and property tax reassessments, and run the 90-day stress test. Ensure your daily finances are structured properly by understanding The 50/30/20 Budget Rule Explained Simply and determining How Much Should You Keep in Checking vs Savings?. By knowing exactly “how much house can I afford” before you start shopping, you guarantee that your new home will be a place of peace, not a daily source of panic.

Take the time to do this math today, run your numbers, and step into homeownership with complete confidence.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

4 Comments

Comments are closed.