How Much Should You Have Saved by Age 30, 40, and 50?

It is the question that keeps millions of adults up at night: Am I falling behind? When you see your peers buying larger houses, taking expensive vacations, or posting about their stock portfolios, it is incredibly easy to feel like you missed a critical financial memo.

But personal finance is not about competing with your neighbors or keeping up appearances; it is about mathematically securing your own future. To do that, you need objective benchmarks. You need to know exactly how much should you have saved by age 30, 40, and 50 so you can track your progress without the emotional anxiety.

If you are constantly wondering if your 401(k) balance is “normal,” or if your savings account is too small for your age, you are in the right place.

In this comprehensive guide, we are going to break down the industry-standard savings targets for every decade of your life. We will also look at the data to reveal the actual median savings of the average American, explain the most common wealth-building mistakes, and give you a concrete action plan to catch up if your accounts are running low.

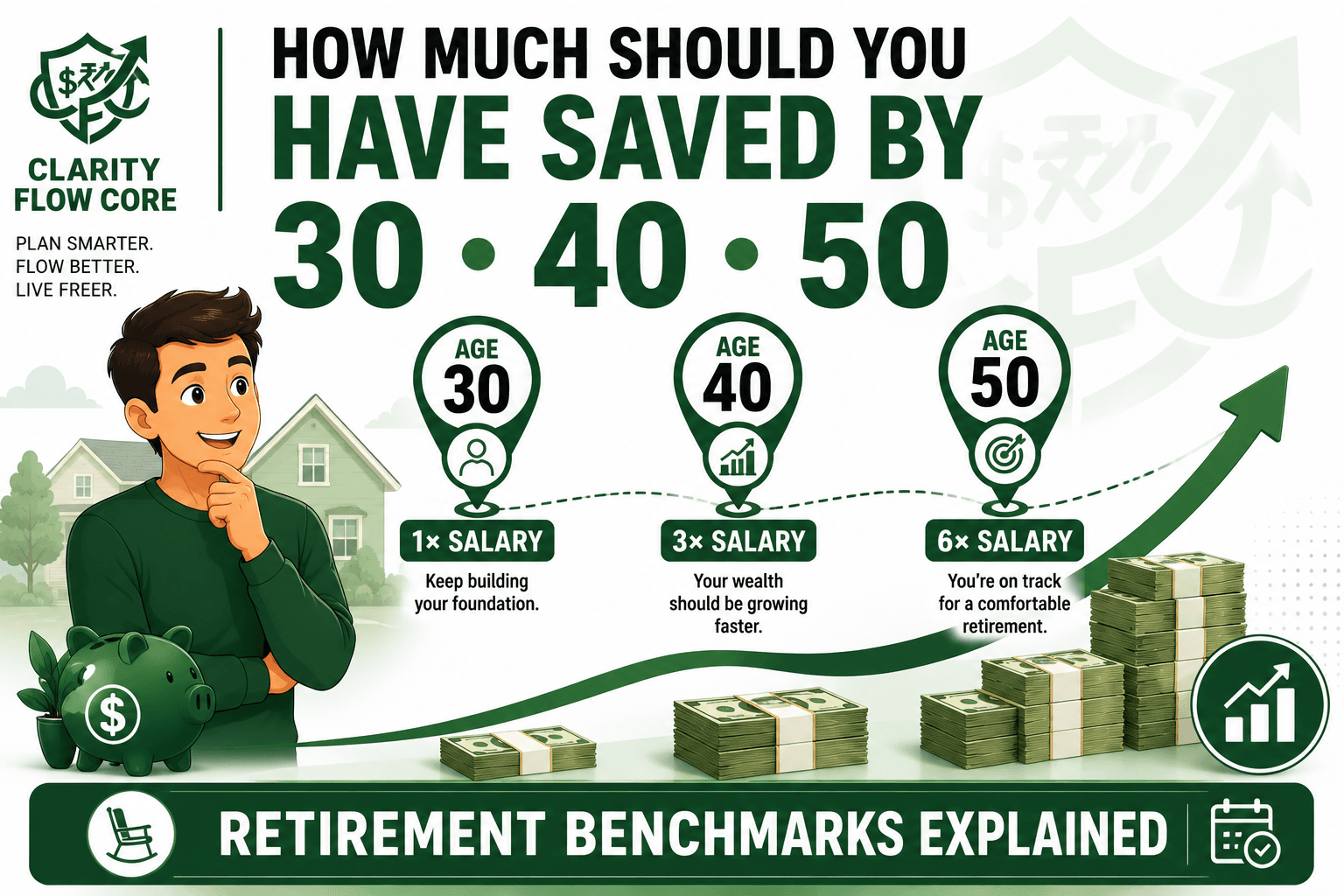

Quick Answer

According to financial experts at Fidelity Investments, you should aim to have 1x your annual salary saved by age 30, 3x your salary by age 40, and 6x your salary by age 50. These benchmarks assume you want to maintain your current lifestyle in retirement and plan to retire around age 67. If you are behind, the fastest way to catch up is to automate your investments, claim your employer match, and aggressively eliminate high-interest consumer debt.

Savings Benchmark by Age

Here is the quick breakdown of exactly what multiple of your salary you should aim to have saved during each phase of your career:

| Age | Target Savings |

| 30 | 1× Salary |

| 40 | 3× Salary |

| 50 | 6× Salary |

| 60 | 8× Salary |

| 67 | 10× Salary |

Important Clarification: These benchmarks refer specifically to retirement and investment savings—not your total net worth. This includes your 401(k), IRA, and brokerage accounts, but generally does not include the equity tied up in your primary home.

The Gold Standard: Fidelity’s Savings Benchmarks

When financial planners talk about retirement readiness, they rarely use flat dollar amounts. Telling a 40-year-old they need exactly “$250,000” is bad advice because everyone’s lifestyle costs are different. Someone accustomed to living on $50,000 a year needs vastly less money to retire than someone accustomed to living on $150,000 a year.

Instead, the industry standard relies on salary multiples.

To make this feel more concrete, let’s look at exactly what these multiples mean in real dollars based on different income levels:

| Salary | Age 30 | Age 40 | Age 50 |

| $50,000 | $50,000 | $150,000 | $300,000 |

| $75,000 | $75,000 | $225,000 | $450,000 |

| $100,000 | $100,000 | $300,000 | $600,000 |

Now, let’s break down each decade, compare the targets to reality, and figure out your next steps.

How Much Should You Have Saved by Age 30?

Your twenties are usually chaotic. You are graduating, entering the workforce, figuring out how to budget, and likely juggling student loan payments. Because your starting salary is usually the lowest it will ever be, your primary goal is simply to build the habit of saving.

The Target: 1x Your Salary

If you earn $60,000 a year on your 30th birthday, the benchmark suggests you should have $60,000 saved in your retirement and investment accounts.

The Reality

Are most 30-year-olds actually hitting this target? Not even close. According to the Federal Reserve’s most recent Survey of Consumer Finances, the median retirement savings for Americans under age 35 is just $18,880.

If you have less than a year’s salary saved at age 30, you are completely normal. Do not panic. You have over three decades of compound interest ahead of you.

Your Focus for This Decade:

- Capture the Match: If your employer offers a 401(k) match, contribute at least enough to get 100% of that match. It is literally free money.

- Build a Cash Buffer: Before aggressively investing in the stock market, you need a liquid safety net to keep you out of credit card debt when emergencies happen. Not sure how much cash to keep on hand? Run your monthly expenses through our Advanced Emergency Fund Analyzer to find your exact target.

- Kill Toxic Debt: If you have high-interest credit card balances, knocking them out is your highest financial priority.

How Much Should You Have Saved by Age 40?

Your thirties are often defined by major life transitions. You might be buying a house, getting married, or starting a family. This is also the decade where your earning potential usually begins to climb significantly.

The Target: 3x Your Salary

If you earn $85,000 a year at age 40, your target savings goal is $255,000.

The Reality

Once again, the actual data paints a different picture than the ideal benchmark. The Federal Reserve reports that the median retirement savings for Americans aged 35 to 44 is $45,000. The gap between the recommended benchmark and reality begins to widen significantly in this decade.

Your Focus for This Decade:

- Combat Lifestyle Creep: As you get promotions and raises in your thirties, it is tempting to upgrade your car, your house, and your vacations. This is called lifestyle creep. To hit your 3x target, you must commit to investing a large portion of every raise you get, rather than spending it all.

- Watch Your Ratios: If you decide to buy a home or upgrade to a larger house in your thirties, ensure your mortgage does not suffocate your ability to invest. Use our Debt-to-Income Analyzer & Loan Readiness Planner to verify that a new mortgage payment still leaves you with enough free cash flow to fund your retirement accounts.

- Aim for 15%: By this decade, you should ideally be directing 15% of your gross income toward retirement.

What If I’m Starting From Zero at 40?

This is an incredibly common scenario. Between paying off student loans, surviving recessions, and raising children, many people arrive at age 40 with little to nothing saved for retirement.

If this is you, do not let regret stop you from taking action today. Even if you’ve saved nothing by age 40, you can still make meaningful progress by:

- Maximizing employer matches: Never leave free 401(k) money on the table.

- Increasing your savings rate: You will likely need to save 20% or more of your income instead of the standard 15%.

- Reducing debt: Eliminate every high-interest payment so all your extra cash flow can be funneled into investments.

- Delaying retirement a few years: Retiring at 70 instead of 65 gives your money five extra years of compound growth and drastically lowers the amount you need to withdraw.

How Much Should You Have Saved by Age 50?

Your forties are typically your peak earning years. You have established your career, and hopefully, your earlier investments are beginning to snowball through the power of compound interest. In this decade, the growth of your portfolio might actually start outpacing the physical cash you are putting in.

The Target: 6x Your Salary

If you earn $100,000 a year by age 50, your benchmark target is $600,000.

The Reality

The Federal Reserve data shows that the median retirement savings for Americans aged 45 to 54 is $115,000. While this is a significant jump from the previous decade, it still falls short of the recommended target for a comfortable, traditional retirement.

Your Focus for This Decade:

- Take Advantage of Catch-Up Contributions: The IRS recognizes that many people fall behind on their savings. Starting at age 50, federal tax rules allow you to make “catch-up contributions.” This means you are legally allowed to contribute extra thousands of dollars above the standard annual limits to your 401(k) and IRA accounts.

- Model Your Future: At 50, retirement is no longer a vague concept in the distant future; it is a fast-approaching reality. It is time to start running hard numbers. Use our Financial Freedom Planner to map out exactly how your current savings, projected returns, and future timeline align with your long-term goals.

- Avoid Borrowing Against Your Future: Do not cash out your 401(k) or stop investing to pay for your children’s college tuition. Your children can take out loans for their education; you cannot take out a loan for your retirement.

Why Do I Feel So Behind? (The Median vs. Average Trap)

If you read financial news, you might see headlines claiming the “average” 50-year-old has over $300,000 saved. This contradicts the $115,000 number we cited above. Why? Because of the difference between “average” (mean) and “median.”

When calculating an average, ultra-wealthy individuals drastically skew the numbers upward. If nine people have $10,000 saved and one CEO has $10 million saved, the “average” savings for that group is over a million dollars. But that doesn’t reflect reality.

The median finds the exact middle point of the data—meaning half the country has more, and half the country has less. Always look at the median. The median data proves a crucial point: If you feel behind, you are in the vast majority. The best time to start investing was ten years ago; the second best time is today.

Common Mistakes When Saving for the Future

As you work toward these age-based milestones, be careful to avoid these common traps that routinely derail wealth-building:

1. Confusing Savings with Investing

Keeping $50,000 sitting in a standard checking account is not building wealth; it is slowly losing purchasing power to inflation. Cash is for emergencies and short-term purchases (less than 3 to 5 years away). Money meant for your 50s and 60s must be invested in assets like index funds, stocks, or real estate so it can outpace inflation.

2. Letting High-Interest Debt Eat Your Wealth

You cannot out-invest a credit card. If you are earning an 8% return in your 401(k) but paying 24% interest on a revolving credit card balance, you are going backward mathematically. If you are struggling to manage your balances, use our Credit Utilization Calculator & Recovery System to build a strategic payoff plan.

3. Waiting Until “Things Calm Down”

Many people tell themselves they will start saving as soon as they get a raise, as soon as the car is paid off, or as soon as the kids are out of daycare. The truth is, life rarely calms down. There will always be an excuse not to save. You have to start where you are, even if you can only afford to invest $50 a month.

Your Action Plan: What to Do If You’re Behind

If you looked at the Fidelity targets and realized you are severely off track, take a deep breath. You can fix this. Follow this specific action plan to get moving in the right direction today.

Step 1: Calculate Your Gap

Write down your current gross salary. Multiply it by the benchmark for your age. Subtract your current total retirement savings. This is your gap. Write the number down so you have a clear, unemotional target.

Step 2: Audit Your Budget

You cannot save money if you don’t know where it is going. Review your last three months of bank statements. Group your spending into Needs, Wants, and Savings/Debt Payoff. If you don’t have a system, read our guide on how to Budget as a Freelancer When Income Changes Every Month. Cut the subscriptions and eating out habits that do not actually bring you joy.

Step 3: Automate Your Contributions

Willpower is a terrible financial strategy. Do not wait until the end of the month to see what money is “left over” to invest. Log into your payroll provider or your bank and set up automatic transfers. Have 10% to 15% of your income automatically routed into your 401(k) or IRA the moment your paycheck hits. If you never see the money in your checking account, you won’t spend it.

Step 4: Boost Your Income

At a certain point, you cannot cut your way to wealth. If your budget is incredibly tight, you need an income shovel. Focus on getting a promotion, switching companies for a pay bump, or starting a weekend side hustle to generate pure profit that you can funnel directly into your investment accounts.

Frequently Asked Questions (FAQ)

1. Is it ever too late to start saving for retirement?

No. Starting later requires more aggressive saving, but improving your financial position is always possible. Even if you start in your late 40s or 50s, compounding interest and catch-up contributions can significantly boost your retirement readiness.

2. Does my house equity count toward these savings benchmarks?

Generally, no. Fidelity’s 1x, 3x, and 6x rules are designed for liquid retirement savings and investment accounts. While home equity is great for your overall net worth, you cannot easily pay your daily utility bills with house equity unless you sell the property or take out a reverse mortgage.

3. Do these numbers include my spouse’s income?

If you manage your finances jointly, yes. You should calculate the target based on your total household gross income and measure it against your total combined household retirement accounts.

4. What if I changed careers and took a pay cut?

These benchmarks are based on your current salary. If you made $100,000 at age 35, but switched to a lower-stress career making $60,000 at age 40, your new target is 3x your new salary ($180,000). Because you plan to live on less in retirement, your total required savings number drops.

5. Should I pay off debt or save for retirement first?

It depends on the interest rate. If your employer offers a 401(k) match, always contribute enough to get the match—it is a 100% immediate return. After that, focus entirely on paying off high-interest toxic debt (like credit cards with 20%+ rates). Once toxic debt is gone, you can shift your focus back to aggressive investing.

6. What if I plan to retire early (FIRE)?

If your goal is Financial Independence, Retire Early (FIRE), the standard Fidelity guidelines will not work for you. Because you plan to stop working at 40 or 50, you need significantly more money saved significantly faster. You will likely need to save and invest 30% to 50% of your income rather than the standard 15%.

7. Does having a pension change how much I need to save?

Yes. If you are one of the rare workers who still qualifies for a guaranteed employer pension (like a teacher, firefighter, or government employee), your personal savings targets will be significantly lower. The pension will cover a large portion of your monthly expenses, meaning your personal portfolio doesn’t have to work as hard.

8. Can a bad credit score stop me from investing?

Your credit score has absolutely no direct impact on your ability to open an investment account, buy stocks, or contribute to a 401(k). However, poor credit often means you are paying higher interest rates on your loans, which drains the cash you could be using to invest. If you need to fix your score, check out our Credit Score Simulator & Improvement Planner.

Conclusion

Looking at massive savings targets like “3x your salary” or “6x your salary” can feel incredibly intimidating, especially if you are starting from zero. But remember, wealth is not built overnight. It is built through decades of small, consistent habits.

If you are behind the benchmarks, do not let regret paralyze you. The average American is also behind. The difference between you and everyone else is that you now have the knowledge and the framework to change your trajectory. Start capturing your employer match, automate your savings, attack your high-interest debt, and let compound interest do the heavy lifting. You have the power to take control of your financial future starting today.

References & Trusted Resources

- Fidelity Investments: Retirement Savings Guidelines and Age-Based Milestones

- Federal Reserve: Survey of Consumer Finances (SCF) 2022/2023 Data

- Internal Revenue Service (IRS): Retirement Topics – Catch-Up Contributions

- Consumer Financial Protection Bureau (CFPB): Planning for Retirement

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be construed as professional financial, legal, or tax advice. Every individual’s financial situation is unique. Please consult with a certified financial planner or tax professional regarding your specific circumstances before making major financial decisions. For more detailed information, please review our full Disclaimer.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.