How Much Should Freelancers Save for Taxes? A Complete Guide

You just landed a massive freelance contract. The client pays your $5,000 invoice in full, the money hits your checking account, and you feel a massive wave of relief. You immediately start mentally spending the money: paying off a credit card, booking a weekend trip, and covering next month’s rent.

But there is a catch. That $5,000 is not entirely yours.

If you are transitioning from a traditional W-2 job to the world of freelancing, independent contracting, or side hustling, you are about to encounter the single biggest trap in personal finance: the freelance tax bill. When you work for an employer, they automatically withhold your taxes from every paycheck. You never see the money, so you never miss it.

When you work for yourself, the IRS relies on you to withhold that money manually. If you spend your entire gross income, you will be hit with a catastrophic tax bill next April, complete with underpayment penalties and late fees.

So, exactly how much should freelancers save for taxes? You need a system. In this guide, we will break down exactly how much you need to set aside, how the self-employment tax actually works, and how to protect your cash flow so you never fear tax season again.

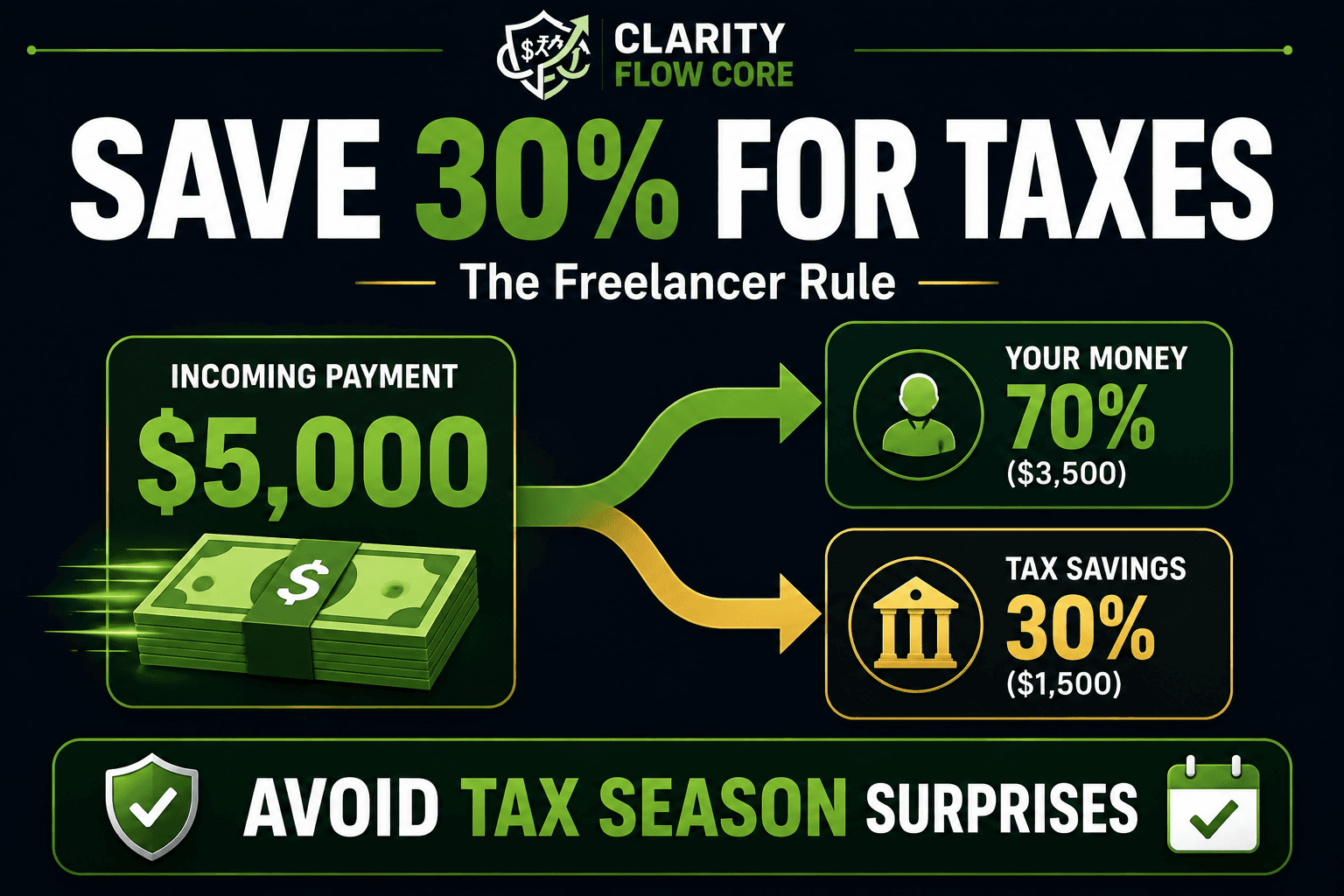

⚡ Quick Answer How much should freelancers save for taxes? As a general rule of thumb, you should save 25% to 30% of your net income (your profit after business expenses). This covers your 15.3% Self-Employment tax, your federal income tax, and your state income tax. To be perfectly safe, automatically transfer 30% of every client payment into a separate High-Yield Savings Account the moment it clears.

The Freelancer Tax Formula

To keep things incredibly simple as you scale your business, just memorize this equation:

Net Income × 30% = Tax Savings Goal Example: $4,000 Net Income × 30% = $1,200

The Tale of Two Freelancers: System vs. No System

To truly understand why this matters, let’s look at what happens when you do not respect the math.

Life Without a Tax System

- You finish a project, and the client pays your $5,000 invoice.

- You spend the full $5,000 on rent, credit card debt, and lifestyle upgrades.

- April 15th arrives.

- Your accountant informs you that you owe $1,500 for that project.

- You have no cash left. Panic sets in, and you are forced to put the IRS bill on a high-interest credit card, kicking off a cycle of debt.

Life With a Tax System

- You finish a project, and the client pays your $5,000 invoice.

- You immediately calculate your profit and transfer $1,500 to a separate Tax Holding account.

- The money sits in a High-Yield Savings Account, earning you interest.

- Quarterly tax deadlines arrive. You log into the IRS portal, transfer the money easily, and sleep perfectly fine that night.

This emotional contrast is why a system is non-negotiable.

🚨 The Biggest Freelancer Tax Mistake The single fastest way to destroy your freelance business is thinking that Gross Income = Spendable Income. If you sell a website for $3,000, you did not just make $3,000. Until you subtract your business expenses and set aside your 30% for taxes, you cannot safely spend a single dollar of that invoice on your personal life.

Why Freelance Taxes Feel So Expensive

To understand why you need to save so much, you first have to understand why freelance taxes operate differently than traditional W-2 employee taxes. The sticker shock most new freelancers feel is not an illusion; you are genuinely paying a new type of tax you have never had to pay out-of-pocket before.

The Hidden 15.3% Self-Employment Tax

When you work as a standard W-2 employee, you are required to pay FICA taxes, which fund Medicare and Social Security. The total FICA tax rate is 15.3%.

However, as an employee, you only pay half of that (7.65%). Your employer secretly pays the other half (7.65%) on your behalf as a cost of doing business. You never even see it on your pay stub.

When you become a freelancer or a sole proprietor, you are both the employee and the employer. Therefore, the IRS requires you to pay the entire 15.3% yourself. This is known as the Self-Employment (SE) Tax. This 15.3% is charged on your net profit, and it is calculated before your standard federal and state income taxes are even applied.

(For a deeper dive on how specific gig-economy structures impact your filings, check out our guide on 1099 Taxes Explained.)

The Triple Tax Burden

When you put it all together, a freelancer is essentially saving for three completely separate tax buckets:

- Self-Employment Tax (15.3%): Funds your Social Security and Medicare.

- Federal Income Tax (10% to 37%): Based on your total household income tax bracket.

- State Income Tax (0% to 13.3%): Depending on exactly where you live. (If you live in Texas or Florida, you skip this bucket. If you live in California or New York, this bucket is significant).

When you combine a 15.3% SE tax, a 12% federal income tax bracket, and a 5% state tax, you quickly see why saving 30% of your profit is mathematical survival.

How Much Should Freelancers Save for Taxes? (Calculating Your Target)

While the 30% rule is fantastic for quick math and everyday withholding, you will eventually want to calculate your actual projected tax burden to avoid severely underpaying or over-withholding. Here is the four-step process to calculate what you will actually owe.

Step 1: Calculate Your Gross Income

Your gross income is every single dollar that enters your bank account from a client.

Step 2: Subtract Your Business Expenses (To Find Net Income)

You do not pay taxes on your gross income. You only pay taxes on your profit.

If you made $3,000 shooting a wedding, but you spent $500 renting camera lenses and $100 on travel, your total expenses are $600. $3,000 (Gross) – $600 (Expenses) = $2,400 (Net Income).

The IRS only taxes that $2,400. (If you are in video production, you can find industry-specific write-offs in our Freelance Video Editor Tax Guide.)

Step 3: Calculate Your Self-Employment Tax

Apply the 15.3% Self-Employment tax to your Net Income. (The IRS allows a slight adjustment here, but for estimation, 15.3% of your net income is safest). 15.3% of $2,400 = $367.

Step 4: Calculate Your Income Taxes

Finally, estimate your federal and state income tax on that $2,400 profit. If your effective federal tax rate is 12%, and your state tax rate is 4%: 16% of $2,400 = $384.

Total Estimated Tax on the Project: SE Tax ($367) + Income Tax ($384) = $751.

In this scenario, $751 is exactly 31% of the $2,400 net profit. As you can see, the 30% rule of thumb is highly accurate.

Where to Keep Your Tax Savings

A major mistake beginners make is leaving their tax savings in their primary checking account. If you do this, you will look at your balance, feel artificially wealthy, and use the IRS’s money to pay for a vacation. You must separate the money physically and psychologically.

- Open a Dedicated Business Checking Account: All client payments must go here. All business expenses are paid from here. Never commingle personal and business funds.

- Open a High-Yield Savings Account (HYSA): Link this HYSA to your business checking. Label the account “IRS TAX HOLDING.”

- Automate the Transfer: Every Friday, log into your business account, calculate your profit for the week, and immediately transfer 30% of that profit into the HYSA.

A Note for High-Tax States: If you live in a state with high income taxes—like California, New York, or New Jersey—many freelancers find it incredibly helpful to open two separate savings accounts: one labeled “Federal Taxes” and one labeled “State Taxes.” This prevents you from accidentally sending your entire tax savings to the IRS and having nothing left for the state department of revenue.

The US tax system is “pay-as-you-go.” If you expect to owe more than $1,000 in freelance taxes for the year, you are legally required to make quarterly estimated tax payments. You cannot wait until April 15th to pay your entire bill in one lump sum.

The quarterly deadlines typically fall on:

- April 15

- June 15

- September 15

- January 15 (of the following year)

When these dates approach, you pull the money you have been saving in your HYSA and make a direct payment to the IRS through their official portal. For a full breakdown of the forms required and how to submit payments, read our comprehensive guide on Quarterly Estimated Taxes Explained for Freelancers and Side Hustlers.

Hate Quarterly Tax Deadlines?

If you have a W-2 day job alongside your freelance business, you can skip quarterly estimated payments entirely. Use our optimizer to adjust your W-4 and let your employer automatically cover your side hustle tax bill.

Optimize My W-4The Safe Harbor Rule

If your income fluctuates wildly and you have no idea how much to send the IRS each quarter, use the Safe Harbor Rule. The IRS will not penalize you if you pay at least 100% of the total tax you owed last year (or 110% if your income was over $150,000). Look at your previous tax return, divide the total liability by four, and send that exact amount each quarter.

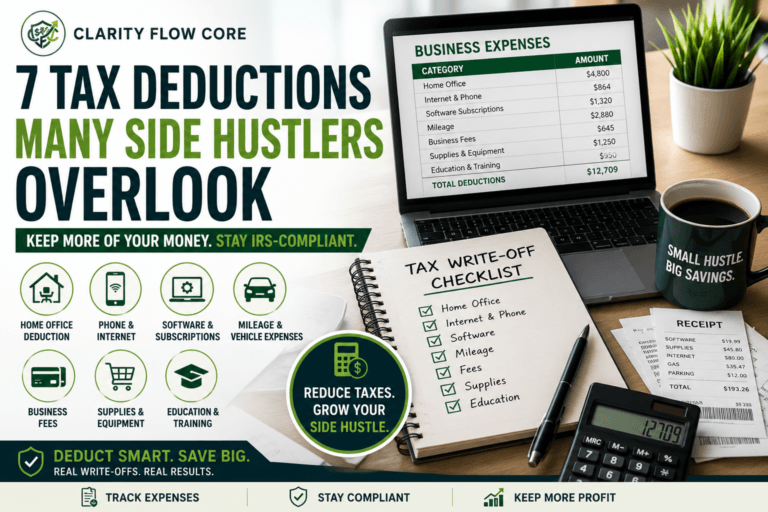

The 80/20 Rule: Biggest Tax Wins for Freelancers

If you want to keep more of your own money legally, you have to optimize your deductions. Following the 80/20 rule of finance, focus your energy on these major areas.

- The Home Office Deduction: If you use a specific area of your home exclusively for business, you can deduct a portion of your rent and utilities.

- Mileage and Vehicle Expenses: Every mile driven for business is deductible at the standard IRS rate (typically around 65 to 67 cents per mile).

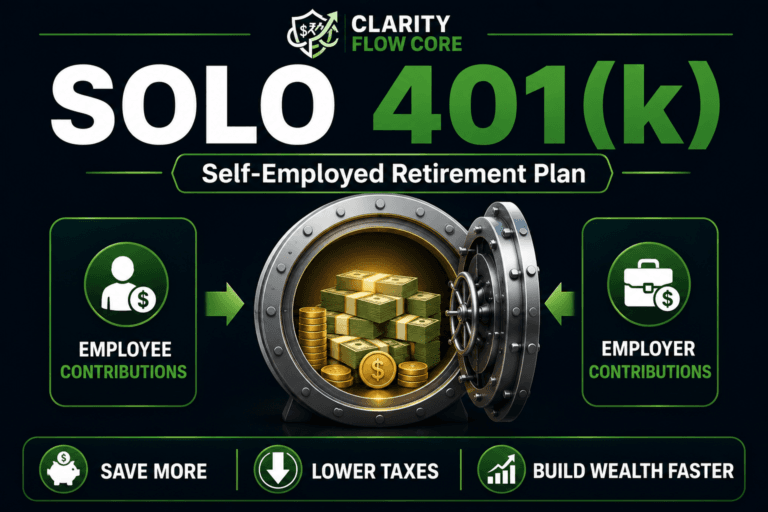

- Solo 401(k) Contributions: If you want to drastically slash your tax bill while building wealth, a Solo 401(k) is the ultimate freelancer hack. Because you are both employer and employee, you can shelter massive amounts of revenue from current-year taxes. Learn how to set one up in our guide: What Is a Solo 401(k) and How Does It Work?.

Common Mistakes When Managing Freelance Taxes

Even with a solid plan, freelancers often trip up on a few common mistakes that derail their tax strategy. Watch out for these errors:

- Saving Based on Gross Income (Over-saving): If you run a high-overhead business (like buying physical inventory), saving 30% of your gross revenue will bankrupt your daily cash flow. Always save based on your net profit.

- Using Tax Money for Business Emergencies: Your laptop dies, so you dip into your tax savings HYSA to buy a new one, promising to “pay it back.” You rarely do. You must have a separate business emergency fund. Run your numbers through the Advanced Emergency Fund Analyzer to build a proper buffer.

- Ignoring State Taxes: Many freelancers perfectly calculate their federal taxes but completely forget their state wants a cut, leading to underpayment penalties from the state department of revenue.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetAction Plan: Set Up Your Tax System Today

Do not wait until the end of the month to fix your accounting. Follow these steps today.

- Open the Right Accounts: Open a dedicated business checking account and a linked High-Yield Savings Account.

- Determine Your Percentage: Commit to the 30% rule for your first year.

- Automate the Process: Put a recurring appointment on your calendar for every Friday at 4:00 PM. Use this time to transfer 30% of your week’s profit into your tax holding account.

- Mark the Deadlines: Put the four quarterly estimated tax deadlines in your calendar with a 7-day reminder attached.

Next Steps

Once your tax system is running on autopilot, your next priority is optimizing the rest of your freelance finances. If your income fluctuates wildly from month to month, traditional budgeting advice will not work for you.

Related Guides to Read Next:

- How to Budget as a Freelancer When Income Changes Every Month

- Emergency Fund Basics

- Quarterly Estimated Taxes Explained for Freelancers and Side Hustlers

- Sole Proprietor vs LLC: Which Is Best for a Side Hustle?

Frequently Asked Questions

Do I have to pay taxes if I make less than $400? According to the IRS, if your net earnings from self-employment are $400 or more, you must file a tax return and pay self-employment tax. If you make $399, you are technically exempt from the SE tax, but you still must report the income for standard federal income tax purposes.

Can I write off my home internet bill? Yes, but only the percentage you use for your business. If your internet bill is $100, and you use it 50% for freelance work, you can deduct $50 a month as a business expense.

What happens if I miss a quarterly estimated tax payment? If you miss a deadline, pay it as soon as you realize the error. The IRS calculates underpayment penalties based on how many days the payment is late. Paying it a month late is far better than waiting until April.

Does an LLC save me money on taxes? A standard single-member LLC does absolutely nothing to lower your taxes. The IRS views it as a “disregarded entity,” meaning you are taxed exactly the same as a Sole Proprietor. An LLC is formed for legal liability protection, not tax reduction.

Do I pay self-employment tax on passive income? Generally, no. Self-employment tax applies to earned income (money you actively worked for). Passive income from rental properties or stock dividends is subject to regular income tax, but it is typically exempt from the 15.3% SE tax.

References and Resources

To ensure you have the most accurate and up-to-date information regarding self-employment regulations, we recommend exploring these official resources:

- Internal Revenue Service (IRS): The definitive source for all self-employment tax rules, including official forms and current standard mileage rates. Review the IRS Self-Employed Tax Center.

- IRS Estimated Taxes: Detailed breakdowns of how to calculate quarterly taxes and avoid underpayment penalties using the safe harbor rules. Read IRS guidelines on Estimated Taxes.

- Small Business Administration (SBA): The SBA offers exceptional free resources, local mentorship, and cash flow templates for new freelancers and sole proprietors. Explore the SBA business guide.

- Consumer Financial Protection Bureau (CFPB): Offers robust educational materials on managing variable income and separating personal and business finances. Visit the CFPB resources.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.