SEP IRA vs Solo 401(k): Which Retirement Plan is Best for Freelancers?

Leaving the traditional corporate world to become a freelancer, consultant, or small business owner is one of the most liberating decisions you can make. You control your schedule, you choose your clients, and you keep the profits. But a few months into your new self-employed life, you realize you left something critical behind: the company 401(k) plan and the employer match.

As a freelancer, no one is going to automatically deduct 5% of your paycheck and invest it for your future. No HR department is going to set up your retirement accounts. If you want to stop working one day, the responsibility falls entirely on your shoulders.

The good news? The IRS offers self-employed individuals access to retirement accounts that are vastly superior to what most corporate employees receive. Because you are both the “employee” and the “employer” of your own business, you can funnel massive amounts of your income into tax-sheltered accounts, drastically lowering your annual tax bill while building long-term wealth.

The two heavyweights in the self-employed retirement space are the SEP IRA and the Solo 401(k).

Choosing between these two accounts is a major financial decision. It dictates how much you can invest, how much administrative paperwork you have to do, and whether you can hire employees in the future. In this comprehensive guide, we will break down the exact differences between a SEP IRA and a Solo 401(k), run the real-world math on both, and help you decide which account is the smartest move for your business.

Quick Answer: SEP IRA vs Solo 401(k)

Both accounts offer massive tax benefits for self-employed individuals. A SEP IRA is best if you want a ridiculously simple setup, no annual IRS paperwork, or if you plan to hire W-2 employees soon. A Solo 401(k) is best if you are a solo operator with no employees (other than a spouse) and want to maximize your savings on a moderate income, need a Roth option, or want the ability to take a loan from your retirement account.

At a Glance: SEP IRA vs Solo 401(k)

If you are looking for the high-level differences before we dive into the math, here is how the two accounts compare:

| Feature | SEP IRA | Solo 401(k) |

| Best For | Extreme simplicity, higher earners, businesses planning to hire. | Maximizing contributions on moderate income, solo operators. |

| Who Can Open It? | Any business owner, even those with employees. | Only business owners with NO W-2 employees (except a spouse). |

| Contribution Types | Employer contributions only. | Both Employee AND Employer contributions. |

| Roth Option Available? | Generally no (though SECURE 2.0 allows it, few brokers support it yet). | Yes, Roth contributions are widely available for the employee side. |

| Age 50+ Catch-Up? | No. | Yes. |

| Loans Permitted? | No. | Yes, you can borrow up to $50,000 or 50% of the balance. |

| Administrative Burden | Zero annual IRS reporting. | Form 5500-EZ required once assets exceed $250,000. |

The Freelancer’s Retirement Dilemma

Before choosing an account, you must understand how the IRS views your freelance income.

When you work as a W-2 employee, your employer pays half of your Medicare and Social Security taxes, and you pay the other half. When you are self-employed—whether you operate as a sole proprietor or an LLC—you are responsible for the full 15.3% self-employment tax, plus your standard federal and state income taxes.

Need a refresher on your tax obligations? Read our complete guide on Quarterly Estimated Taxes Explained for Freelancers and Side Hustlers to ensure you aren’t hit with IRS penalties.

Because your tax burden as a freelancer is so high, contributing to a tax-advantaged retirement account is the most effective legal way to shield your money from the government. Every dollar you contribute to a Traditional SEP IRA or Traditional Solo 401(k) reduces your taxable income for the year.

If you make $100,000 and contribute $20,000 to one of these accounts, the IRS taxes you as if you only made $80,000. That alone can save you thousands of dollars in a single tax year.

Deep Dive: What is a SEP IRA?

A Simplified Employee Pension (SEP) IRA is exactly what it sounds like: a simplified retirement plan designed for small businesses and self-employed individuals.

How It Works

The most important thing to understand about a SEP IRA is that all contributions are considered employer contributions. Even if you are a solo freelancer with no formal payroll, the IRS views you as the employer making a contribution to your own employee account.

The Contribution Math

Because you are making employer contributions, the amount you can put into a SEP IRA is strictly limited to a percentage of your income.

You can contribute up to 25% of your net adjusted self-employment earnings, up to a maximum limit set by the IRS each year (which hovers around $69,000 for recent tax years).

Note: The math on “net adjusted earnings” is tricky. Because you must deduct half of your self-employment tax before calculating the 25%, the effective maximum contribution for a sole proprietor or single-member LLC is actually 20% of your net profit.

Pros of a SEP IRA

- Zero Administration: There is no annual reporting requirement to the IRS. You open the account at a brokerage (like Vanguard, Fidelity, or Schwab), deposit the money, and claim the deduction on your taxes. That is it.

- Dead-Simple Setup: You can open a SEP IRA in about five minutes online.

- Flexible Deadlines: You can open and fund a SEP IRA all the way up until tax day (usually April 15) and still claim the deduction for the previous year. If you file a business tax extension, you have until October 15 to fund it.

- You Can Hire Employees: If your freelance business explodes and you decide to hire three W-2 employees next year, you can keep your SEP IRA. (However, there is a massive catch to this, which we will cover below).

Cons of a SEP IRA

- Lower Contributions for Moderate Earners: Because you are strictly limited to roughly 20% of your net profit, you have to make a very high income to maximize this account. If you net $50,000 from freelancing, the absolute most you can put into a SEP IRA is roughly $10,000.

- No Catch-Up Contributions: If you are over age 50, the IRS does not allow you to put “catch-up” money into a SEP IRA like they do with standard IRAs or 401(k)s.

- No Loans: You cannot borrow against a SEP IRA under any circumstances. If you take the money out early, you will pay heavy taxes and a 10% penalty.

Deep Dive: What is a Solo 401(k)?

A Solo 401(k)—also known as an Individual 401(k) or One-Participant 401(k)—is a traditional corporate 401(k) stripped down and designed specifically for a business owner with no employees.

How It Works

The magic of the Solo 401(k) is that you get to act as both the employee and the employer. This allows you to make two entirely separate types of contributions to the same account, allowing you to stash away massive amounts of cash even on a moderate income.

The Contribution Math

Because you wear two hats, you contribute money in two ways:

- The Employee Contribution (Elective Deferral): As the “employee,” you can contribute 100% of your freelance compensation up to the standard IRS 401(k) limit (which sits at $23,000 for recent tax years, or $30,500 if you are age 50 or older).

- The Employer Contribution (Profit Sharing): On top of your employee contribution, you—acting as the “employer”—can contribute an additional 25% of your net adjusted self-employment income (effectively 20% of net profit), just like a SEP IRA.

Combined, your total employee and employer contributions cannot exceed the absolute IRS maximum (around $69,000, or $76,500 if over 50).

Pros of a Solo 401(k)

- Maximum Contributions on Lower Income: Because you get that massive $23,000 employee deferral right off the bat, you can save drastically more money than a SEP IRA if your income is under $150,000.

- The Roth Option: Most brokerages offer a “Roth Solo 401(k).” This allows you to make your employee contributions with after-tax money. The money grows completely tax-free, and you pay zero taxes when you withdraw it in retirement.

- Catch-Up Contributions: If you are 50 or older, you get an extra $7,500 in employee deferral space to aggressively catch up on your retirement timeline.

- You Can Borrow From It: A Solo 401(k) generally allows you to take out a loan of up to $50,000 or 50% of your account balance. You pay the loan (and the interest) back into your own account. It is a powerful emergency safety valve.

Cons of a Solo 401(k)

- Strict “No Employee” Rule: You cannot open or maintain a Solo 401(k) if you have any W-2 employees. The only exception is your spouse. If your spouse helps run the business, they can actually participate in the Solo 401(k) too, essentially doubling your family’s savings limits.

- Administrative Burden: Once your Solo 401(k) balance reaches $250,000, the IRS requires you to file Form 5500-EZ every single year. If you forget to file this form, the penalties are incredibly steep.

- Strict Deadlines: To make an employee contribution for the current tax year, you must formally establish the Solo 401(k) plan by December 31st of that year. You cannot wait until April like you can with a SEP IRA.

Plan Your Timeline: Want to know exactly how much you need to invest every month to reach your goals? Run your numbers through our Financial Freedom Planner to build your customized wealth roadmap.

Map Your Freelance Retirement

As a business owner, you don’t have a corporate pension to fall back on. Use our interactive analyzer to project your self-employed investments, calculate your exact target, and build a concrete plan to retire on your own terms.

Plan My RetirementThe Real-World Math: Which Should You Choose?

The abstract rules are confusing. The easiest way to decide between a SEP IRA and a Solo 401(k) is to look at a side-by-side math example.

Let’s look at a freelance graphic designer named Sarah. She operates as a sole proprietor and has $60,000 in net profit for the year. Sarah wants to save as much money as legally possible to lower her tax bill.

Scenario A: Sarah Uses a SEP IRA

Because the SEP IRA only allows employer contributions, Sarah is limited to roughly 20% of her net profit.

- Maximum SEP IRA Contribution: ~$11,150

Scenario B: Sarah Uses a Solo 401(k)

Sarah gets to act as the employee and the employer. First, she maxes out her employee deferral. Then, she adds the employer profit-sharing portion (roughly 20% of her net profit).

- Employee Contribution: $23,000

- Employer Contribution: ~$11,150

- Maximum Solo 401(k) Contribution: ~$34,150

The Verdict for Sarah: On a $60,000 income, the Solo 401(k) allows Sarah to save over three times as much money as the SEP IRA. For freelancers making under $150,000 who want to aggressively invest, the Solo 401(k) is the undisputed winner.

When Does the SEP IRA Win?

The math flips when two things happen:

- Your income is incredibly high (over $300,000). At that income level, the 20% employer contribution maxes out the IRS limits entirely on its own, rendering the Solo 401(k)’s employee deferral advantage irrelevant.

- You want extreme simplicity and refuse to ever deal with filing an IRS Form 5500-EZ.

The Employee Dilemma: A Crucial Warning

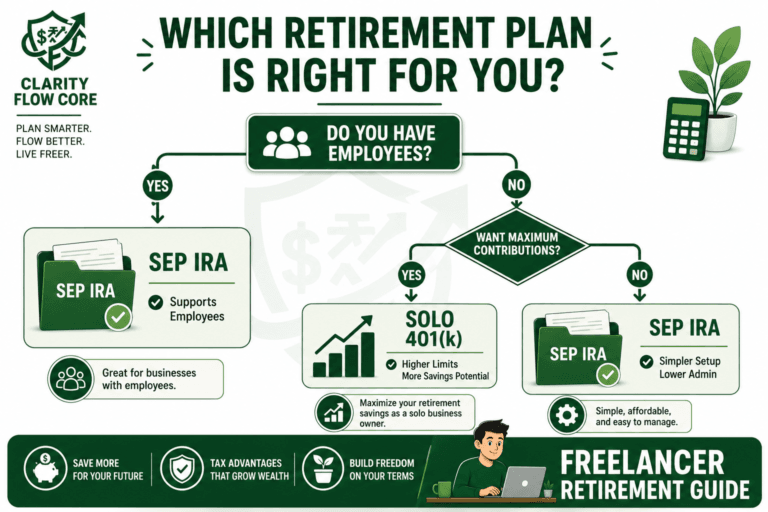

There is one factor that overrides all the math: Do you plan to hire employees?

If you run a one-person consulting business and intend to keep it that way forever, the Solo 401(k) is brilliant. But if you think you might open a physical office or hire W-2 staff in the next few years, you must be careful.

The Solo 401(k) Rule: The moment you hire an eligible W-2 employee (who works more than 1,000 hours a year), your Solo 401(k) is invalidated. You will have to restructure the plan into a standard corporate 401(k), which involves high administrative fees, strict non-discrimination testing, and hiring a third-party administrator.

The SEP IRA Rule: You can keep a SEP IRA if you hire employees. However, you must treat your employees exactly how you treat yourself. If you contribute 15% of your income into your own SEP IRA, you are legally required to contribute 15% of your employee’s salary into their SEP IRA—out of your own business profits. This can become staggeringly expensive for a small business owner.

(Note: Independent contractors or freelancers you hire via a 1099 do not count as employees. You do not have to buy retirement plans for your 1099 contractors).

Business Structure Matters: Unsure if you should remain a Sole Proprietor or formally incorporate before hiring? Read our breakdown: Sole Proprietor vs LLC: Which Is Best for a Side Hustle?

Common Beginner Mistakes

When setting up your first self-employed retirement account, avoid these costly errors:

- Mistake 1: Missing the Solo 401(k) Deadline. You must sign the plan documents to establish your Solo 401(k) by December 31st if you want to make employee deferrals for that tax year. If you wait until tax season in April, it is too late. You will be forced to use a SEP IRA instead.

- Mistake 2: Having Both a W-2 Job and a Solo 401(k). If you work a traditional day job and run a side hustle, you can have a Solo 401(k) for your side hustle. But, the $23,000 employee limit applies to you as a person, not the accounts. If you contribute $10,000 to your day job’s 401(k), you can only contribute $13,000 as the “employee” to your Solo 401(k).

- Mistake 3: Forgetting the Form 5500-EZ. We mentioned it above, but it bears repeating. If your Solo 401(k) balance exceeds $250,000 at the end of the year, you must file Form 5500-EZ. The IRS penalty for failing to file this form can reach $250 per day, up to a maximum of $150,000. Do not ignore your paperwork.

- Mistake 4: Not Keeping an Emergency Fund. Putting 100% of your extra cash into a retirement account is mathematically great, but practically dangerous. Freelance income is volatile. You need liquid cash. Run your basic expenses through our Advanced Emergency Fund Analyzer to ensure you have 3 to 6 months of cash on hand before you aggressively lock your money away in a 401(k).

Your Action Plan: How to Get Started This Week

Do not let analysis paralysis stop you from securing your future. If you are ready to open an account, follow these exact steps:

- Evaluate Your Hiring Plans: Ask yourself honestly: Will I hire a W-2 employee in the next three years? If yes, lean toward the SEP IRA. If no, lean toward the Solo 401(k).

- Get Your EIN: Even if you operate as a sole proprietor without an LLC, you will likely need an Employer Identification Number (EIN) from the IRS to open a Solo 401(k). It is completely free and takes 10 minutes to generate on the IRS website.

- Choose a Brokerage: Look for a low-cost brokerage that offers free Solo 401(k) or SEP IRA setups. Vanguard, Fidelity, and Charles Schwab are the industry leaders. If you want a Roth Solo 401(k), verify that the brokerage actually supports the Roth option (Vanguard and Fidelity both do).

- Open the Account by December 31st: Even if you do not have the cash to fully fund the account yet, get the plan established before the end of the calendar year to lock in your eligibility.

- Automate Your Contributions: Treat your retirement like a utility bill. Every time a client pays an invoice, immediately transfer 10% to 15% of the payment directly into your retirement account.

Frequently Asked Questions (FAQ)

1. Can I have a traditional IRA and a SEP IRA at the same time?

Yes. You can contribute to both a personal Traditional/Roth IRA and a business SEP IRA or Solo 401(k) in the same year. However, if your income is high, your ability to legally deduct the personal Traditional IRA contribution may be phased out since you are covered by a workplace retirement plan.

2. What if I make a mistake and overcontribute?

If you accidentally contribute more than the IRS math allows for your net profit, you must remove the excess contributions (and any earnings they generated) before you file your tax return. If you fail to remove the excess, the IRS will hit you with an ongoing 6% penalty tax every year until it is fixed.

3. Does an LLC change my retirement limits?

No. Whether you operate as a Sole Proprietor or a Single-Member LLC, the IRS treats you identically for tax purposes (as a “disregarded entity”). Your contribution limits are based strictly on your net business profit, not your legal structure.

(Note: If you have elected for your LLC to be taxed as an S-Corporation, the math changes completely. Your contributions will be based on your W-2 salary drawn from the S-Corp, not the total business profit).

4. Can I roll my old corporate 401(k) into a Solo 401(k)?

Yes! This is one of the best features of a Solo 401(k). If you have old 401(k)s from previous employers sitting around, you can roll them directly into your new Solo 401(k). This consolidates your accounts, gives you total control over the investments, and immediately boosts your balance.

5. Are SEP IRA and Solo 401(k) contributions tax-deductible?

Yes. Traditional contributions to both a SEP IRA and a Solo 401(k) are “above-the-line” deductions. They reduce your Adjusted Gross Income (AGI) for the year, which lowers your final federal and state income tax bill.

6. Do I pay taxes when I withdraw the money?

Yes. Because you took a tax deduction when you put the money in, the IRS will tax the money as ordinary income when you withdraw it in retirement (after age 59 ½). If you use a Roth Solo 401(k) for your employee contributions, you pay the taxes upfront, and the withdrawals in retirement are completely tax-free.

Conclusion

When you become a freelancer, you take total control over your career, your income, and your time. It is only fitting that you take total control of your retirement as well.

The choice between a SEP IRA and a Solo 401(k) ultimately comes down to your income level, your administrative tolerance, and your future business plans. For the vast majority of solo operators, the Solo 401(k) is the undisputed champion, allowing you to stash away incredible amounts of money on a modest freelance income.

Do not let the IRS jargon intimidate you. Pick the account that matches your business model, open it at a reputable brokerage, and start transferring a percentage of every client invoice into the market. You are building the ultimate safety net for your future self—one freelance check at a time.

References

- Internal Revenue Service (IRS): Simplified Employee Pension Plan (SEP)

- Internal Revenue Service (IRS): One-Participant 401(k) Plans

- Internal Revenue Service (IRS): Form 5500-EZ Requirements

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.