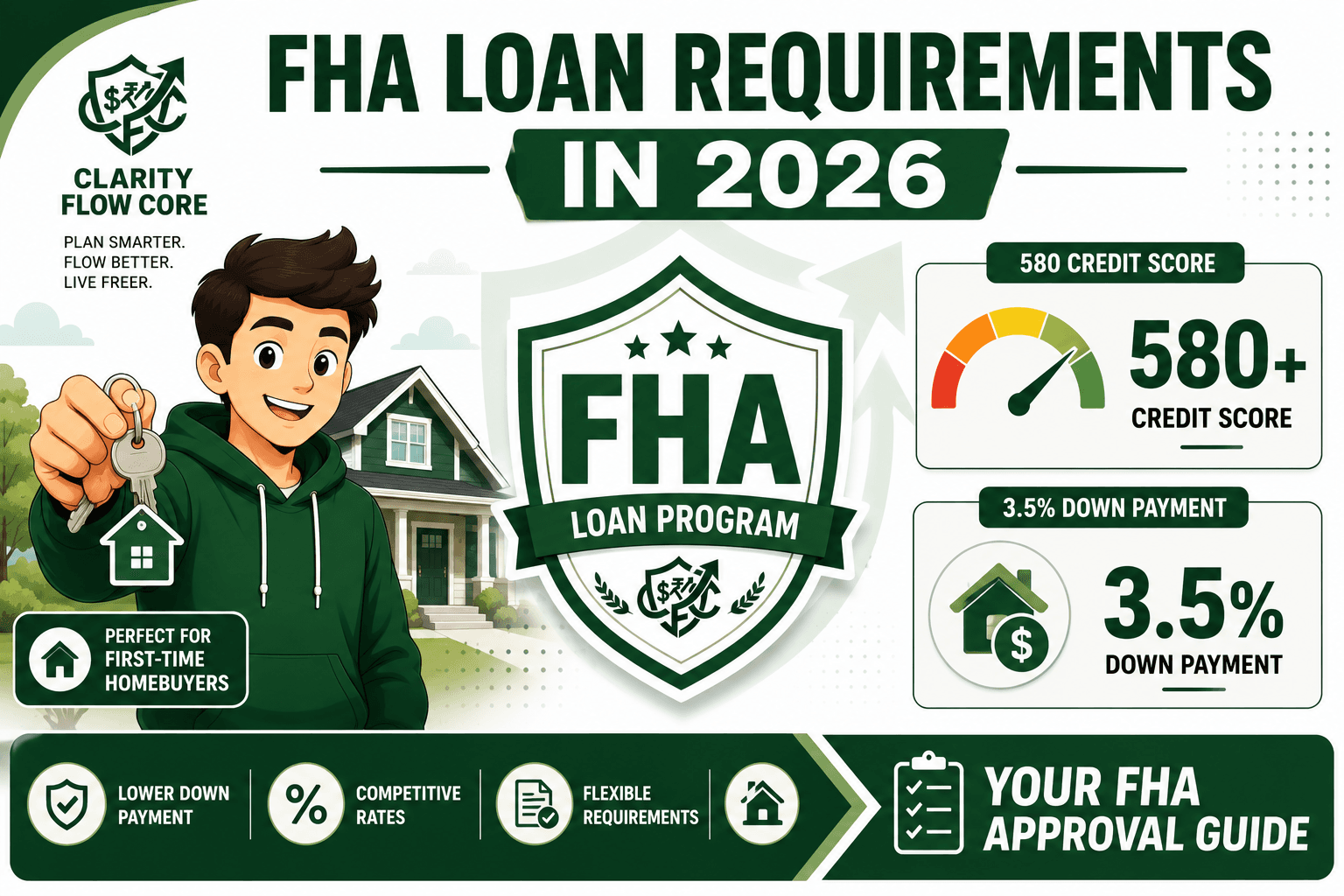

FHA Loan Requirements 2026: Everything You Need to Know

When you start looking at home prices, the math can feel incredibly discouraging. If you follow the old-school financial advice of putting 20% down, buying a $350,000 starter home means you need to scrape together $70,000 in cash—and that doesn’t even include closing costs. For most average earners, saving that amount of money while simultaneously paying rent feels like trying to run a marathon in quicksand.

Fortunately, that old-school advice is outdated. You do not need a 20% down payment, and you do not need a perfect 800 credit score to buy a house.

The Federal Housing Administration (FHA) created a specialized mortgage program designed specifically to help moderate-income earners and first-time buyers get their foot in the door. FHA loans are backed by the federal government, which drastically reduces the risk for lenders. Because the risk is lower, the lenders can offer you highly forgiving qualification standards.

However, “forgiving” does not mean “free money.” The FHA has strict rules regarding who qualifies, how much debt you can carry, and what kind of condition the house must be in. In this guide, we will break down the exact FHA loan requirements 2026, explain how the hidden mortgage insurance fees work, and show you exactly what you need to do to get approved.

Quick Answer: What are the FHA loan requirements for 2026?

To qualify for an FHA loan, you need a minimum credit score of 580 to qualify for the low 3.5% down payment. If your score is between 500 and 579, you must put 10% down. You must use the home as your primary residence, have a steady two-year employment history, and maintain a Debt-to-Income (DTI) ratio generally below 43%. The property must also pass a strict health and safety appraisal.

At a Glance: FHA Loan Requirements 2026

Before getting into the details, here is a high-level summary of the minimum benchmarks you need to hit to get an FHA loan approved this year:

| Requirement | Minimum Standard |

| Credit Score (3.5% Down) | 580 or higher |

| Credit Score (10% Down) | 500 to 579 |

| Debt-to-Income (DTI) Ratio | Typically 43% (Can go up to 50%+ with strong compensating factors) |

| Employment History | 2 years of verifiable, steady income |

| Property Type | Primary residence only (1 to 4 units) |

| Mortgage Insurance | Upfront premium (1.75%) + Annual premium required |

Quick Qualification Checklist

- ✓ Credit score 580+

- ✓ 3.5% down payment

- ✓ Stable income

- ✓ DTI under 43%

- ✓ Primary residence

If you checked all five boxes, you may be a strong FHA candidate.

The Core Financial Requirements

Getting approved for a mortgage comes down to proving to the bank that you are a safe bet. The lender will look at three primary financial pillars: your credit, your cash, and your debt.

1. Credit Score and Down Payment Rules

Unlike Conventional loans that heavily penalize you for average credit, FHA loans are incredibly lenient. The amount of cash you need to bring to the closing table is directly tied to your credit score:

- The 580 Benchmark: If your FICO credit score is 580 or higher, you qualify for maximum FHA financing. This means you only need a 3.5% down payment. On a $300,000 house, your down payment is just $10,500.

- The 500 to 579 Range: If your credit score has taken a few hits and sits in the 500s, you are not disqualified. However, the FHA requires you to put down a 10% down payment to offset the added risk. On that same $300,000 house, you would need $30,000.

Need a credit boost? If your score is hovering around 570, it is usually worth delaying your home purchase by a few months to raise your score past 580, saving you thousands in upfront cash. You can use our Free Credit Score Simulator & Improvement Planner to map out the fastest route to a 580+. You can also read more about general credit requirements in our guide: What Credit Score Do You Need to Buy a House in 2026?.

2. Debt-to-Income (DTI) Limits

Your credit score proves your willingness to pay; your Debt-to-Income ratio proves your ability to pay.

DTI is the percentage of your gross monthly income (before taxes) that goes toward paying your monthly debts (car loans, student loans, minimum credit card payments) plus your new estimated mortgage payment.

- The FHA prefers your back-end DTI to be 43% or lower.

- However, lenders can push this limit up to 45%, or even 50%, if you have “compensating factors”—such as a large savings account, a high credit score, or steady residual income.

If you make $5,000 a month before taxes, the FHA wants to see that your total debt obligations (including the new house) stay under $2,150 per month. If you are unsure where you stand, run your numbers through our Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner.

While meeting the FHA’s DTI limits is important for loan approval, it’s equally important to make sure your housing costs fit comfortably within your personal budget. Our guide How Much of Your Income Should Go Toward Housing Costs? explains how to choose a sustainable housing payment instead of simply borrowing the maximum amount a lender allows.

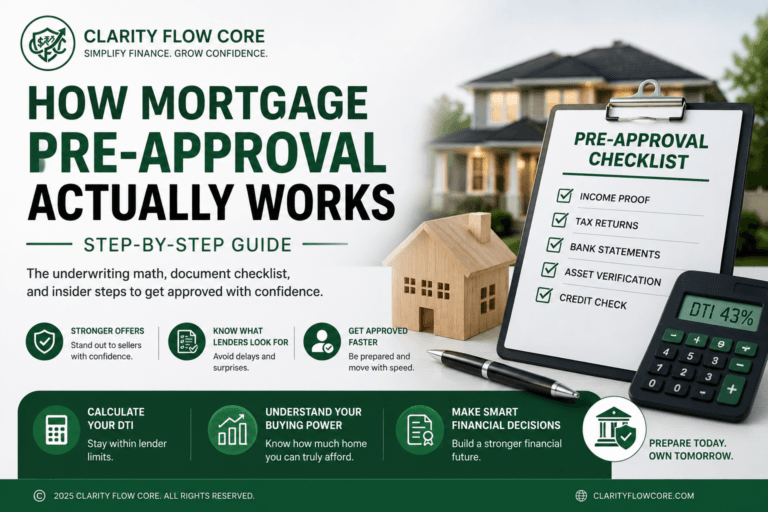

3. Employment and Income Verification

Lenders want stability. To qualify for an FHA loan, you generally need to show a continuous two-year employment history.

- W-2 Employees: You will need to provide two years of W-2 forms and your most recent 30 days of pay stubs.

- Freelancers and Gig Workers: If you are self-employed, getting approved is slightly harder but entirely possible. You must provide two years of full tax returns, and the lender will average your net business income over those two years to determine your qualifying income.

- Job Hopping: Changing jobs is fine as long as there are no massive, unexplained gaps in your employment and your income has remained steady or increased.

The Catch: FHA Mortgage Insurance Premiums (MIP)

Here is the trade-off. The FHA allows you to buy a house with a low credit score and just 3.5% down, but in exchange, they require you to pay for Mortgage Insurance Premiums (MIP). This insurance does not protect you if you lose your job; it protects the lender if you default on the loan.

With an FHA loan, you have to pay MIP twice:

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time fee equal to 1.75% of your base loan amount. On a $300,000 loan, this is a $5,250 fee. Most buyers choose to roll this fee into their loan balance rather than paying it out of pocket at closing. (Curious about other upfront fees? Read our guide on Closing Costs Explained: What Home Buyers Actually Pay).

- Annual Mortgage Insurance Premium: This is an ongoing fee divided by 12 and added to your monthly mortgage payment. For most typical FHA loans (30-year term, 3.5% down), the annual premium is 0.55% of the loan amount. That adds roughly $137 a month to your housing bill.

Important Note: If you put down less than 10%, FHA mortgage insurance lasts for the entire life of the loan. The only way to remove it is to refinance into a Conventional loan once you build up 20% equity in the home.

FHA vs Conventional Loan Comparison

| Feature | FHA | Conventional |

| Minimum Score | 580 | Typically 620+ |

| Minimum Down Payment | 3.5% | 3–5% |

| Mortgage Insurance | Required | Depends on equity |

| Appraisal Standards | Strict | Less strict |

| Best For | Lower credit buyers | Strong credit buyers |

Strict Property Requirements

FHA loans are intended to help people buy safe, livable homes to reside in, not to help real estate investors buy cheap fixer-uppers to flip for a profit. Therefore, the property itself must meet strict guidelines.

Primary Residence Only

You must move into the property within 60 days of closing and live there as your primary residence for at least one full year. You cannot use an FHA loan to buy a vacation home or an instant rental property.

(There is one major exception: You can use an FHA loan to buy a multi-family property up to 4 units, as long as you live in one of the units and rent out the others. This is a brilliant wealth-building strategy. Read more in our guide on House Hacking Explained: Using an FHA Loan to Lower Housing Costs.)

The FHA Appraisal: Health and Safety Standards

When you buy a home with an FHA loan, the appraiser is acting as a strict inspector for the government. The home must meet the FHA’s Minimum Property Standards (MPS) for health and safety.

An FHA appraiser will fail a home if they find:

- Peeling or chipping paint (especially in homes built before 1978, due to lead hazards).

- A roof with less than 2 years of life remaining.

- Missing handrails on staircases.

- Major plumbing or electrical issues.

- Foundation cracks or severe water damage.

If the appraiser flags these items, the seller must fix them before the FHA will allow the loan to close. In a highly competitive market, some sellers prefer Conventional buyers simply because FHA appraisals are so picky.

FHA Loan Limits

The government will not fund a luxury mansion. The FHA sets maximum loan limits that change annually based on the cost of living in your specific county. You can look up your specific county’s limit on the official HUD website.

Example FHA Limits

- Low-Cost Areas: ~$500,000

- High-Cost Areas: $1.1M+

- Alaska & Hawaii: Even higher limits may apply.

Real-World Scenario: FHA vs. Conventional

To understand how FHA loans work in practice, let’s look at a buyer named Marcus.

Marcus wants to buy a $300,000 home. He earns a good income, but his credit score is 640. He has $15,000 saved up.

Option A: The Conventional Loan

Because his credit score is 640 (which is relatively low for conventional standards), a Conventional lender will likely hit Marcus with a high interest rate and very expensive private mortgage insurance (PMI). Furthermore, many conventional programs for this score require a 5% down payment ($15,000). If he puts down $15,000, he has zero cash left for closing costs and moving expenses. The conventional loan is too tight for his budget.

Option B: The FHA Loan

Marcus applies for an FHA loan. Because his score is over 580, he only needs 3.5% down ($10,500). His interest rate is generally lower than the conventional quote because the government backs the loan. He uses his remaining $4,500 to help cover closing costs. While he does have to pay the FHA mortgage insurance, the flexible down payment allows him to safely get into the house without draining his bank account.

Comparing Your Options: Not sure which path to take? Read our comprehensive breakdown on FHA vs Conventional Loan: Which Mortgage is Better for You?

Check Your FHA Eligibility

Don’t just guess your approval odds. Use our free Mortgage Affordability Calculator to instantly check your FHA eligibility, calculate a 3.5% down payment, and estimate your monthly mortgage insurance (MIP).

Common Mistakes Beginners Make With FHA Loans

The FHA process is highly regulated. Avoid these massive pitfalls as you prepare to buy:

- Mistake 1: Draining Your Savings for the Down Payment. You need cash for closing costs, moving expenses, and the inevitable broken appliance in your first month. Never drop your bank account to zero. Use our Advanced Emergency Fund Analyzer to figure out your post-purchase safety net.

- Mistake 2: Taking on New Debt Before Closing. After you get pre-approved, do not finance a new couch, buy a new car, or put $2,000 on a credit card. The lender will check your credit one final time before closing. If your DTI spikes, they will revoke your loan. Understand this timeline by reading What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline.

- Mistake 3: Looking at Fixer-Uppers. Unless you are applying for a specialized FHA 203(k) rehab loan, standard FHA loans will not let you buy a severely run-down house. Save yourself the heartbreak and tell your realtor to only show you move-in-ready homes that will pass FHA safety standards.

Your Action Plan: Steps to Get Approved

Ready to start the process? Here is exactly what you need to do this month:

- Check Your Credit Score: Pull your official FICO scores. If you are below 580, pause your home search and focus entirely on paying down credit card balances to boost your score.

- Calculate Your Affordability: Look at your gross monthly income. Multiply it by 0.43. This is roughly the absolute maximum amount of total monthly debt (including the new house) the FHA will allow you to have.

- Gather Your Documents: Start a digital folder. Collect your last two years of W-2s, your last two years of tax returns, 60 days of bank statements, and 30 days of pay stubs.

- Find an FHA-Approved Lender: Not all banks offer FHA loans. Search for an FHA-approved mortgage broker in your area and ask for a pre-approval to see exactly how much house you qualify for.

Frequently Asked Questions (FAQ)

1. Do you have to be a first-time homebuyer to get an FHA loan?

No. This is the biggest myth in real estate. While FHA loans are incredibly popular with first-time buyers, anyone can use an FHA loan, provided they meet the financial requirements and intend to use the home as their primary residence.

2. Can I have more than one FHA loan at a time?

Generally, no. The FHA usually restricts borrowers to one FHA loan at a time. However, there are rare exceptions (such as relocating for work or outgrowing your current home due to an increase in family size) where a lender might approve a second FHA loan.

3. Does a seller hate FHA loans?

“Hate” is a strong word, but in a highly competitive market with multiple offers, a seller might prefer a Conventional or Cash buyer over an FHA buyer. This is strictly because the FHA appraisal process is stricter, and sellers fear they will be forced to make costly repairs (like fixing peeling paint or broken stairs) before the deal can close.

4. How do I get rid of FHA mortgage insurance (MIP)?

If you make a down payment of less than 10%, FHA MIP stays on your loan for the entire duration of the term (usually 30 years). It does not automatically fall off. The only way to remove it is to refinance your FHA loan into a Conventional loan once you reach 20% equity in the property. If you put down 10% or more, the MIP will drop off after 11 years.

5. Can I use gift money for my FHA down payment?

Yes! The FHA allows 100% of your down payment to come from a gift from a family member, employer, or approved charitable organization. The donor must sign a “gift letter” legally stating that the money is not a secret loan that you have to pay back.

6. Are closing costs rolled into an FHA loan?

Typically, you cannot roll standard closing costs into the base balance of an FHA loan. You must pay them out of pocket on closing day. However, you can negotiate “seller concessions” where the seller agrees to pay some of your closing costs, or you can take a higher interest rate from the lender in exchange for “lender credits” to cover the fees.

7. Can FHA loans be used for manufactured homes?

Yes, FHA loans can be used for certain manufactured homes that meet FHA guidelines, are permanently attached to a foundation, and serve as the borrower’s primary residence.

Conclusion

Buying a house in today’s market is undeniably challenging, but the FHA loan program is one of the most powerful tools available to help you break out of the renting cycle. By allowing credit scores as low as 580 and down payments as low as 3.5%, the FHA makes homeownership a realistic goal rather than an impossible dream.

Yes, the mortgage insurance premiums add to your monthly cost, and yes, the appraisal standards are strict. But when utilized correctly, an FHA loan is a brilliant stepping stone. Take control of your credit, calculate your debt-to-income ratio accurately, and start building your down payment fund. Your future home is closer than you think.

References & Trusted Resources

- U.S. Department of Housing and Urban Development (HUD): FHA Mortgage Limits

- Federal Housing Administration (FHA): Single Family Housing Policy Handbook

- Consumer Financial Protection Bureau (CFPB): Mortgage Insurance and FHA Loans

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.