How to Pay Estimated Taxes for the First Time: A Step-by-Step Guide

Figuring out how to pay estimated taxes for the first time is a rite of passage for every new freelancer, independent contractor, and small business owner. But let’s be honest: that doesn’t mean it isn’t terrifying.

When you leave a traditional W-2 job to start working for yourself, you gain total control over your schedule, your clients, and your income. But you also lose the automated safety net of an HR department. Suddenly, no one is withholding 20% of your paycheck and sending it to the government on your behalf. You receive your gross pay in full, and the responsibility of giving the Internal Revenue Service (IRS) their cut falls entirely on your shoulders.

If you wait until April to deal with your taxes, you are going to be hit with a massive, unexpected tax bill—and likely several hundred dollars in underpayment penalties. To avoid this, the IRS requires you to make payments four times a year.

Learning how to navigate the quarterly estimated tax system is one of the most important administrative skills you can build. It keeps you compliant with the law, protects your cash flow, and removes the dreaded “tax season anxiety” from your life.

In this comprehensive guide, we are going to break down exactly who needs to pay, how to calculate the right amount without a math degree, and a literal step-by-step walkthrough of how to physically send the IRS your money. Let’s get started.

Quick Answer

If you expect to owe more than $1,000 in taxes for the year from freelance or self-employment income, you generally must make quarterly estimated tax payments. These are due on April 15, June 15, September 15, and January 15. The easiest way to calculate your payment is to use the “Safe Harbor” rule: look at your total tax bill from last year, divide it by four, and pay that amount each quarter. You can submit your payment securely online for free using IRS Direct Pay.

Quick IRS Deadlines

If you just need to know when your money is due, here is the official IRS quarterly payment schedule:

| Payment Period | Due Date |

| Jan 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| Sept 1 – Dec 31 | January 15 |

(Note: If a due date falls on a Saturday, Sunday, or legal federal holiday, the deadline is automatically pushed to the next business day.)

Why Does the IRS Want Money Four Times a Year?

To understand estimated taxes, you first have to understand how the United States tax system is legally structured. The US operates on a “pay-as-you-go” system.

This means the federal government expects to receive tax revenue as you earn the income throughout the calendar year, not in one giant lump sum the following April.

When you work a traditional job as an employee, your company calculates your expected tax burden based on the Form W-4 you filled out on your first day. They automatically deduct income taxes, Social Security, and Medicare from every single paycheck and route it to the IRS. You never even see the money.

When you become self-employed, you become both the employee and the employer. The IRS still expects to be paid as you earn the money, but since there is no payroll software automatically deducting it, they require you to manually send in “estimated” payments at the end of each financial quarter.

These estimated payments cover two main obligations:

- Federal Income Tax: Your standard income tax based on your tax bracket.

- Self-Employment Tax: A 15.3% tax that covers your Medicare and Social Security contributions. (W-2 employees split this 50/50 with their employer, but self-employed individuals must pay the entire 15.3% themselves).

Do You Actually Need to Pay Estimated Taxes?

Not everyone who earns a few extra dollars on the side needs to worry about quarterly deadlines. The IRS has a very specific threshold that triggers the estimated tax requirement.

You generally must pay estimated taxes if you meet both of the following conditions:

- You expect to owe at least $1,000 in tax for the current year, after subtracting any withholding and refundable credits.

- You expect your withholding (if you have a day job) and credits to be less than 90% of the tax you will owe for the current year, or less than 100% of the tax shown on your prior year’s tax return.

Who This Usually Applies To

- Full-time freelancers, consultants, and independent contractors.

- Small business owners (Sole Proprietors, LLC members, S-Corp owners).

- Gig economy workers (Uber, DoorDash, Instacart) who drive regularly.

- Investors who sold assets and realized massive capital gains.

- Landlords generating significant rental income.

The W-2 Loophole for Side Hustlers

If you have a traditional day job and run a side hustle on the weekends, you might be able to avoid the quarterly estimated tax hassle entirely.

If you realize your side hustle is going to generate enough profit to trigger a $1,000 tax liability, you can simply submit a new Form W-4 to your day job’s HR department. You can request that they withhold an extra $100 or $200 from your regular paycheck to cover the taxes on your side business. Because the IRS treats W-2 withholding as being paid evenly throughout the year, this completely satisfies the “pay-as-you-go” requirement and saves you from tracking quarterly deadlines.

Need help budgeting varying income? Managing a mix of W-2 pay and unpredictable side hustle cash is difficult. Read our guide on How to Budget as a Freelancer When Income Changes Every Month to stabilize your cash flow.

Skip Quarterly Taxes with Your W-4

Have a day job? You can avoid the hassle of quarterly estimated payments entirely. Use our optimizer to figure out exactly how much extra to withhold from your W-2 paycheck to automatically cover your side hustle taxes.

Optimize My W-4The IRS Quarterly Schedule (Which Makes No Sense)

When you hear the phrase “quarterly taxes,” you reasonably assume that the year is divided into four equal three-month blocks, with a payment due at the end of each.

The IRS does not use logic here. The estimated tax calendar is heavily skewed, and the second quarter only covers two months of income. Do not wait until the last minute. The first quarter tax payment is due on the exact same day that your annual tax return for the previous year is due (April 15). This catches many beginners off guard, as they end up having to pay their remaining balance for last year and their first quarter estimate for the new year on the exact same day.

How to Calculate What You Owe (Without a Math Degree)

This is where beginners freeze. If your income fluctuates wildly from month to month, how are you supposed to accurately predict your total tax bill for the entire year?

You don’t have to be perfect. The IRS knows you are estimating. To figure out how much to send, you can use one of three methods, ranging from extremely simple to highly accurate.

Method 1: The Safe Harbor Rule (Best for Beginners)

The IRS does not expect you to have a crystal ball. To protect taxpayers whose income fluctuates, they created the “Safe Harbor” rule.

The rule states that you will not face any underpayment penalties as long as your estimated payments (plus any W-2 withholding) equal at least:

- 100% of the tax you owed last year, OR

- 90% of the tax you will owe this year.

Note: If your Adjusted Gross Income (AGI) last year was over $150,000 (or $75,000 if married filing separately), you must pay 110% of last year’s tax to meet the Safe Harbor requirement.

How to use it: Look at your tax return from last year (Form 1040). Find the line for “Total Tax.” Let’s say your total tax last year was $6,000. To meet the Safe Harbor rule, you simply divide $6,000 by four. You pay the IRS $1,500 every quarter. Even if your business explodes and you make triple the income this year, you are protected from penalties. You will still have to pay the remaining balance next April, but you won’t be fined for underpaying during the year.

Method 2: The 30% Rule of Thumb (Best for Predictable Cash Flow)

If this is your very first year in business, you don’t have a prior year’s tax return to base your estimates on.

In this case, the safest administrative method is to simply open a dedicated, high-yield business savings account. Every time a client pays an invoice, immediately transfer 25% to 30% of the gross payment into that tax account.

When a quarterly deadline approaches, simply send the IRS whatever amount has accumulated in that account over the last three months. While 30% might seem high, it ensures you cover both your 15.3% self-employment tax and your standard federal income tax. If you overpay, you simply get a refund when you file your annual return.

Need a big-picture view? Once your tax money is separated, what do you do with the rest? Use our Financial Freedom Planner to estimate how much of your freelance income you can safely invest for retirement.

Method 3: The Annualized Income Method (Best for Seasonal Workers)

If you make 80% of your income during the summer (e.g., a wedding photographer or landscaper), paying equal quarterly installments based on last year’s total doesn’t make sense. You would be draining your bank account in April before you’ve even made any money.

The Annualized Income Method allows you to calculate your estimated tax based strictly on the actual income you earned during that specific quarter. You use IRS Form 2210 and the worksheets in IRS Publication 505 to essentially calculate a mini-tax return four times a year. It is highly complex, and if you have highly seasonal income, it is highly recommended to hire a CPA to calculate these quarter-by-quarter adjustments for you.

Which Method Should I Use?

- Use Safe Harbor if: You have last year’s return, your income fluctuates, and you want complete simplicity.

- Use the 30% Rule if: It is your first year freelancing, you have no prior tax return, and you want a simple cash-flow system.

- Use the Annualized Method if: You have highly seasonal income (e.g., you are a wedding photographer, landscaper, or run an event-based business).

Real-Life Example: Running the Math

Let’s look at a concrete example so you can see how this works in practice.

Meet Marcus. Marcus is a freelance copywriter. This is his second year in business. He operates as a Sole Proprietor.

- Last year, Marcus’s total tax liability (found on his Form 1040) was $8,000.

- This year, his business is growing, and he expects to owe around $12,000 in taxes.

Marcus is nervous about penalties and decides to use the Safe Harbor Rule.

Because his income is under $150,000, he only needs to pay 100% of last year’s tax to avoid fines.

- Last year’s tax: $8,000

- Divided by 4 quarters = $2,000 per quarter.

Here is what Marcus does:

- April 15: Marcus logs into the IRS website and pays $2,000.

- June 15: Marcus pays $2,000.

- September 15: Marcus pays $2,000.

- January 15: Marcus pays $2,000.

What happens next April? When Marcus files his official tax return for the year, his accountant calculates his actual tax liability as $12,000. Because Marcus already sent the IRS $8,000 in estimated payments, he simply writes a check for the remaining $4,000 balance.

Did he owe a lot of money in April? Yes. But because he met the Safe Harbor requirement (paying 100% of last year’s liability), the IRS does not charge him a single penny in underpayment penalties or interest.

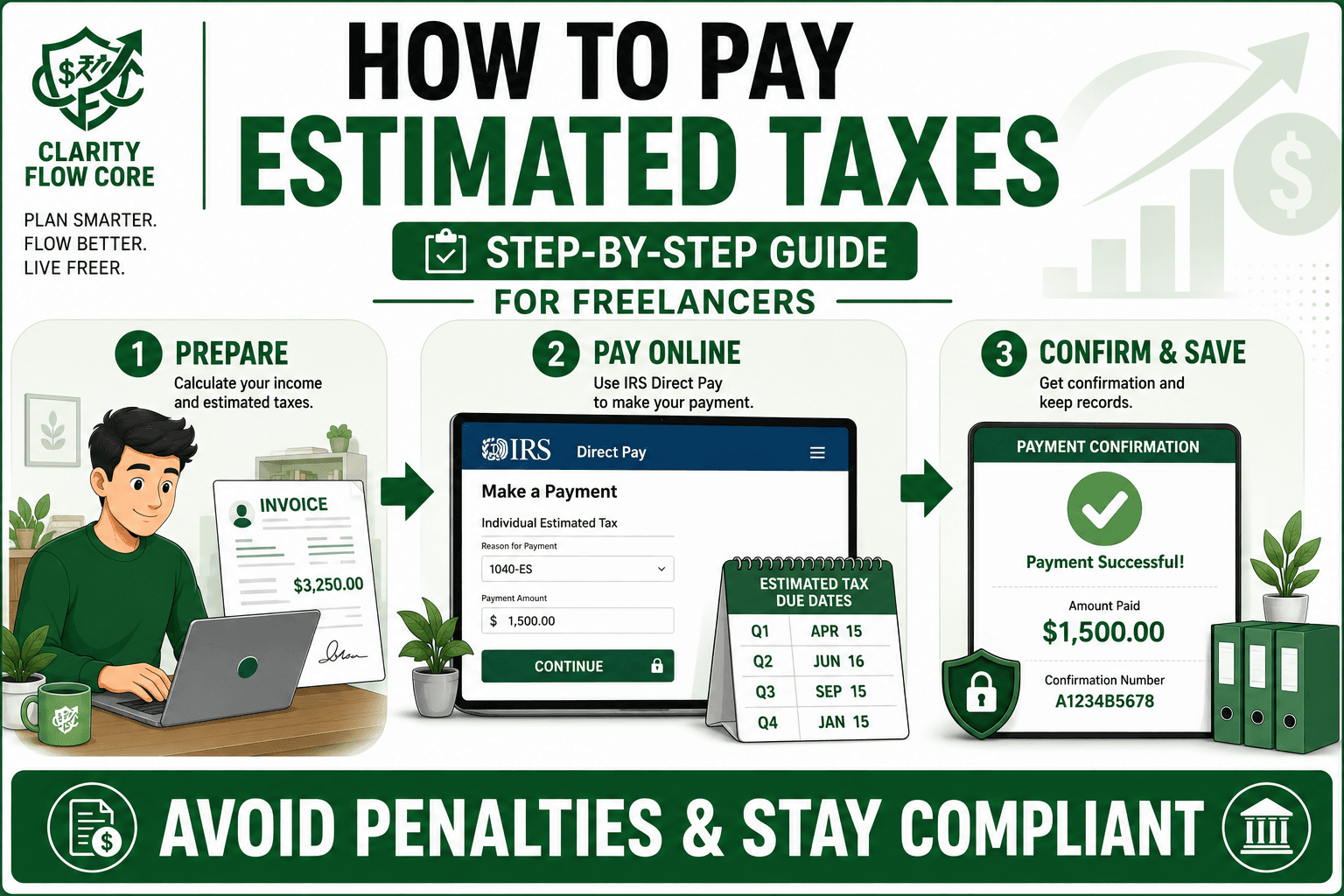

Step-by-Step: How to Pay Estimated Taxes for the First Time

You have done the math. You know exactly how much you need to send. Now, how do you physically get the money to the federal government?

You do not need to print out paper forms and buy stamps unless you really want to. The IRS has modernized their payment systems, making it incredibly easy to pay online.

Here are the three best ways to pay:

Option 1: IRS Direct Pay (The Best Option for Beginners)

IRS Direct Pay is a free, secure service on the official IRS website that allows you to pay directly from your personal checking or savings account.

Step-by-Step Instructions:

- Go to IRS.gov/directpay and click “Make a Payment.”

- Reason for Payment: Select “Estimated Tax” from the dropdown menu.

- Apply Payment To: Select “1040ES (for 1040, 1040A, 1040EZ).”

- Tax Period for Payment: Select the current tax year.

- Verify Identity: The IRS will ask you to verify your identity using information from a previous tax return. You will need to select a prior tax year (e.g., last year) and input your filing status, name, address, and Social Security Number exactly as it appeared on that return.

- Enter Payment Amount: Type in the amount you calculated and enter your bank routing and account numbers.

- Save the Confirmation: Once the payment processes, the IRS will give you a confirmation number. Print this page or save it as a PDF. You will absolutely need this number when you file your annual return to prove you made the payment.

Option 2: The EFTPS System (The Best Option for Established Businesses)

The Electronic Federal Tax Payment System (EFTPS) is a free system operated by the US Department of the Treasury. While Direct Pay is great for one-off payments, EFTPS allows you to create an account, schedule payments up to 365 days in advance, and easily view your entire payment history in one dashboard.

The Catch: You cannot use EFTPS immediately. You have to enroll on EFTPS.gov. The Treasury Department will then mail a physical letter to your home address containing a secure PIN. This process takes about a week. Once you have the PIN, you can log in, link your business bank account, and schedule your quarterly estimated taxes on autopilot.

Option 3: By Debit or Credit Card

You can pay via a card using third-party payment processors linked on the IRS website (like payUSAtax or ACI Payments).

Do not do this unless it is an absolute emergency. The IRS does not charge a fee, but the third-party processors charge a convenience fee of roughly 1.8% to 2% for credit cards, and a flat flat fee (around $2.50) for debit cards. Giving up 2% of your tax payment to processing fees is a terrible financial decision. Stick to the free bank transfers.

Business Structure Warning: If you recently formed a Limited Liability Company, you still pay these estimated taxes using your personal Social Security Number via IRS Direct Pay (unless you elected S-Corp status). Want to learn more? Read our guide: Sole Proprietor vs LLC: Which Is Best for a Side Hustle?

Don’t Forget Your State Taxes

The IRS only handles federal taxes. If you live in a state that has a state income tax (which is the vast majority of US states), you are legally required to make quarterly estimated tax payments to your state’s Department of Revenue as well.

The deadlines for state estimated taxes generally mirror the federal deadlines (April 15, June 15, Sept 15, Jan 15), but the rules vary wildly depending on where you live.

For example, California requires you to pay 30% of your estimated tax in Q1, 40% in Q2, 0% in Q3, and 30% in Q4. Other states simply require four equal 25% installments.

You must visit your specific state’s Department of Revenue or Franchise Tax Board website, create an online account, and submit your state payments separately. Do not mix them up; the IRS will not forward your money to your state government.

What Happens If You Miss a Payment?

If you are reading this in May and realize you completely missed the April 15th deadline for Quarter 1, do not panic, but do act quickly.

⚠️ Important

The IRS generally charges interest and underpayment penalties on late estimated tax payments. Rates change periodically, so always check current IRS guidance rather than relying on older percentages.

The IRS charges an underpayment penalty if you do not pay enough tax throughout the year. Think of this penalty as an interest charge on a loan. The IRS essentially views your missed payment as money you “borrowed” from them.

How to Fix It: Do not wait until the Quarter 2 deadline to catch up. The penalty grows every single day the money is late. Log into IRS Direct Pay immediately and make a payment for the quarter you missed. The sooner you get the money into the system, the smaller the penalty will be.

When you file your annual tax return next April, your tax software (or your CPA) will use IRS Form 2210 to calculate the exact penalty you owe based on how many days late your specific quarterly payments were.

Common Mistakes Beginners Make When Paying Estimated Taxes

Navigating the quarterly system takes practice. Avoid these common financial traps that routinely derail self-employed professionals:

1. Raiding the Tax Savings Account

When your business hits a slow month, it is incredibly tempting to look at the thousands of dollars sitting in your tax savings account and “borrow” it to pay your rent or buy groceries. This is a fatal error. That money does not belong to you; it belongs to the government. Keep your tax savings in a completely separate bank at a different institution so you are not tempted to transfer it into your checking account.

If you are struggling to keep enough cash on hand for personal bills, you need a stronger safety net. Run your numbers through our Advanced Emergency Fund Analyzer to figure out how much operational cash your freelance business actually needs.

2. Forgetting to Claim the Payments on Your Annual Return

When you file your annual Form 1040 in April, there is a specific line to input “Estimated tax payments and amount applied from prior year return.” If you forget to enter the thousands of dollars you sent the IRS via Direct Pay over the last four quarters, the IRS will assume you paid nothing, and you will be billed for the full amount again. Always give your CPA a detailed list of the exact dates and amounts of every estimated payment you made.

3. Paying on Gross Revenue instead of Net Profit

You do not pay taxes on every dollar that enters your business. You only pay taxes on your net profit.

- Gross Revenue – Legitimate Business Deductions = Net Profit.If you make a $5,000 payment from a client, but you spent $1,000 on software and travel to complete the job, you only owe taxes on $4,000. Do not overpay the IRS by estimating taxes on your top-line revenue.

4. Over-Relying on Credit Cards for Cash Flow

If you don’t have the cash to pay your estimated taxes, do not put a $4,000 IRS payment on a credit card charging 24% interest. You cannot out-earn high-interest toxic debt. It is generally better to set up a payment plan with the IRS (who charges significantly lower interest) than to swipe a high-interest credit card. If you are already struggling with high balances, use our Credit Utilization Calculator & Recovery System to map a strategic way out.

Your Action Plan for This Quarter

You now have the knowledge to handle the IRS like a professional business owner. Turn that knowledge into action by following these exact steps this week:

- Find Your Safe Harbor Number: Pull out last year’s tax return. Find your “Total Tax” liability. Divide it by four. Write that number on a post-it note.

- Open a Dedicated Tax Account: If you haven’t already, open a free, high-yield business savings account. Set an automatic rule to transfer 25% of all incoming revenue into this account immediately.

- Set Calendar Reminders: Open your phone calendar right now. Create recurring, high-priority alerts for April 10, June 10, September 10, and January 10. Setting the alert five days early gives you time to transfer funds without rushing.

- Sign Up for EFTPS: Go to EFTPS.gov and register for an account today. By the time the next quarter rolls around, your PIN will have arrived in the mail, and you can automate your payments entirely.

Frequently Asked Questions (FAQ)

1. Do I need to mail a form with my online payment?

No. If you pay electronically using IRS Direct Pay, EFTPS, or a tax software portal, you do not need to mail physical copies of Form 1040-ES. The digital transaction acts as your official record.

2. What if my business doesn’t make any money in a quarter?

You only pay taxes on the income you actually earn. If you have a terrible quarter and make zero profit, you do not have to make an estimated payment for that specific period (unless you are choosing to make equal installments based on the Safe Harbor rule to cover high earnings from a previous quarter).

3. Are quarterly payments exact?

No, they are simply estimates. When you file your official tax return in April, you will reconcile what you paid versus what you actually owed for the year. If you overpaid your estimates, you will get a tax refund. If you underpaid, you will owe the remaining balance.

4. Can I just wait and pay the penalty in April?

Technically, yes, but it is a terrible financial strategy. The underpayment penalty acts like an interest charge. Furthermore, waiting until April means you will have to come up with a massive five-figure lump sum all at once, which bankrupts many first-year freelancers. Pay as you go to protect your cash flow.

5. Do I have to pay estimated taxes in my very first year of freelancing?

If you had absolutely no tax liability in the previous year (meaning you owed $0 in total tax for a full 12-month period), you are technically exempt from estimated payments for your first year. However, if you worked a W-2 job last year and owed taxes, you are still bound by the Safe Harbor rules and should make estimated payments on your new freelance income.

6. What if my income is too unpredictable to calculate 90% of current year taxes?

This is exactly why the IRS created the 100% of Prior Year Safe Harbor rule. If your income fluctuates wildly, completely ignore trying to predict the current year. Just look at last year’s final tax bill, divide it by four, and pay that. You will be 100% protected from penalties, no matter how much your income spikes.

7. Can I apply my tax refund to next year’s estimated taxes?

Yes. When you file your annual return, instead of having the IRS deposit your refund into your bank account, you can elect to have them “apply it to your next year’s estimated taxes.” This is a brilliant way to instantly cover your Q1 and Q2 obligations without having to move cash around.

Conclusion

Paying estimated taxes for the first time is a psychological hurdle more than a mathematical one. It forces you to realize that you are running a real business with real legal obligations.

While the IRS schedule is confusing and calculating the exact math can feel daunting, the system is designed to be manageable. By utilizing the Safe Harbor rule, opening a dedicated savings account to hold your tax money, and leveraging the free IRS Direct Pay portal, you can handle your quarterly obligations in less than fifteen minutes.

You worked incredibly hard to build your independent income. Don’t let administrative fear hold you back. Set your calendar reminders, save a portion of every check, and pay the government what they are owed. Once your tax foundation is solid, you can focus 100% of your energy on what actually matters: growing your business and building your wealth.

References

- Internal Revenue Service (IRS): Estimated Taxes (Form 1040-ES)

- Internal Revenue Service (IRS): Pay As You Go, So You Won’t Owe

- Internal Revenue Service (IRS): Underpayment of Estimated Tax by Individuals Penalty

- Taxpayer Advocate Service (TAS): Making Estimated Tax Payments

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.