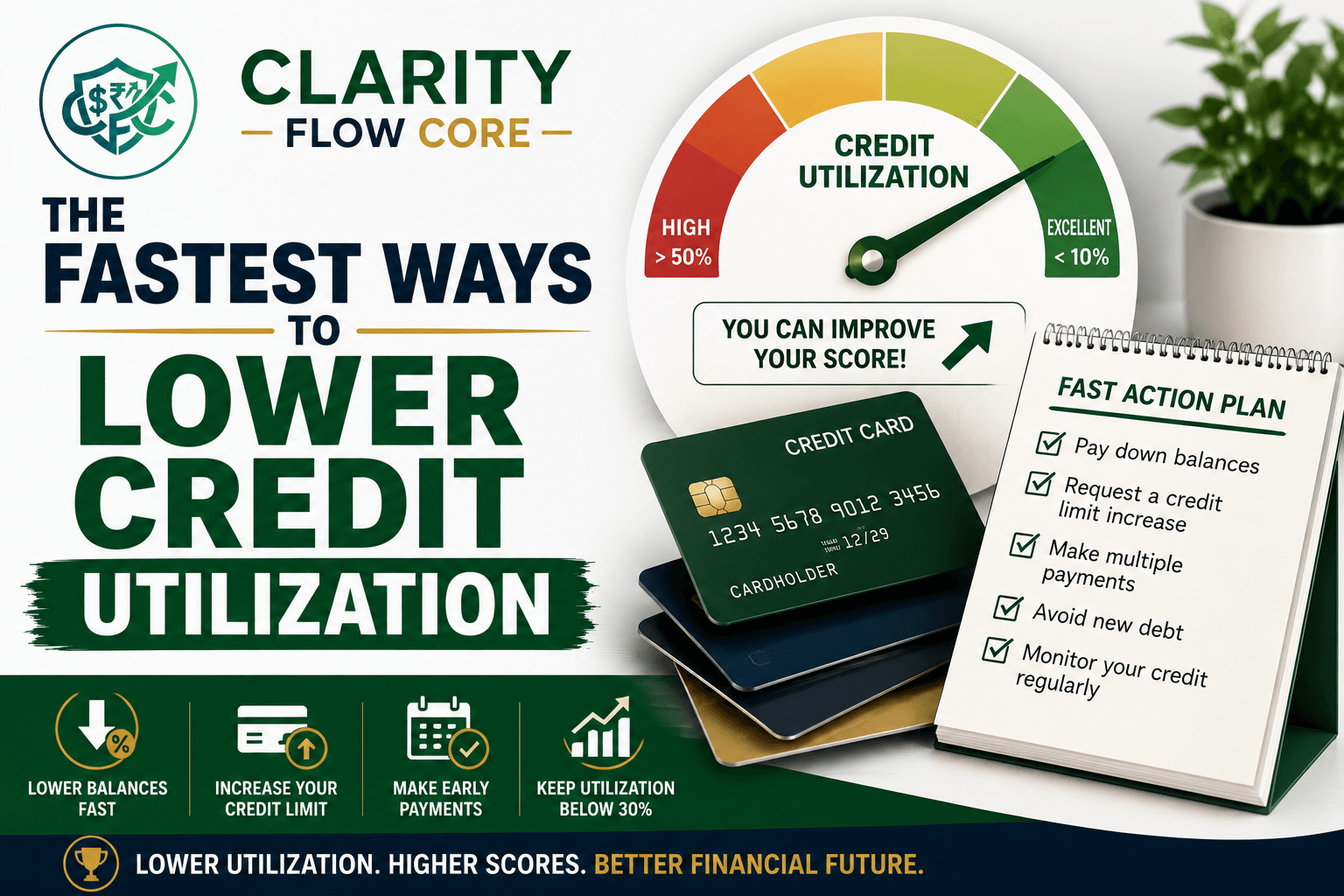

The Fastest Ways To Lower Credit Utilization (And Boost Your Score)

You log into your banking app, feeling pretty good about yourself. You just made your credit card payment right on time, just like you always do. You tap the little button to check your free credit score, expecting to see a nice, steady number.

Instead, your score has plummeted by 35 points.

Your heart skips a beat. You panic, assuming someone stole your identity or a bill you forgot about just went to collections. You frantically scroll down to the “Credit Factors” section, only to see a bright red alert next to a phrase that sounds like pure financial jargon: High Credit Utilization.

If you have ever experienced this exact scenario, you know how incredibly frustrating it is. You are playing by the rules. You are making your payments. Yet, the credit algorithms are actively punishing you. It feels unfair, confusing, and completely out of your control.

But here is the good news: unlike a missed payment or a bankruptcy that haunts your credit report for years, high credit utilization is highly fixable. In fact, it is the single fastest way to manipulate your credit score legally and see a massive boost in a matter of weeks.

Quick Answer The fastest ways to lower credit utilization are paying down balances before your statement closing date, requesting a credit limit increase, making multiple payments throughout the month, and avoiding new credit card spending. Most experts recommend keeping utilization below 30%, while staying under 10% often produces the best credit score results.

Today, we are going to strip away the corporate banking speak. We will look at exactly what this mathematical ratio is, why the credit bureaus care so much about it, the common mistakes that accidentally spike your numbers, and the fastest, most realistic ways to lower your utilization so you can get your score back where it belongs.

What Is Credit Utilization and Why Does It Matter?

Before we can fix the problem, we have to understand the math behind it. Don’t worry, we are going to keep this incredibly simple.

Credit utilization is just a percentage. It is the amount of money you currently owe on your credit cards divided by the total amount of credit you have been given.

Imagine you have exactly one credit card to your name, and the bank gave you a $10,000 credit limit. If you currently have a $4,000 balance on that card, your credit utilization is 40%.

That is the entire formula. The major credit scoring models (like FICO) look at this number in two different ways:

- Per-Card Utilization: How much of the limit you are using on each individual credit card.

- Overall Utilization: Your total combined balances divided by your total combined credit limits across every card you own.

Why does this matter so much? Because your “Amounts Owed” (which is almost entirely dictated by your utilization ratio) makes up a massive 30% of your total FICO credit score. It is the second most important factor in your entire financial profile, sitting right behind your payment history.

Credit scoring models generally reward lower utilization ratios, and many experts recommend staying below 30% whenever possible. Here is exactly how the algorithm judges your percentages:

| Utilization Rate | Impact on Credit Score |

|---|---|

| 0% | Good, but not optimal |

| 1%–9% | Excellent |

| 10%–29% | Good |

| 30%–49% | Moderate impact |

| 50%–74% | Significant impact |

| 75%+ | Major negative impact |

If you cross that 30% threshold, the algorithm automatically flags you as a higher risk. If you push past 50%, 70%, or start maxing out your cards, your score will go into a violent freefall, even if you have never missed a single payment in your life.

Why It Happens: The Cash Flow Trap

Very few people max out their credit cards because they are irresponsible shopaholics buying designer clothes they can’t afford. In the real world, high credit utilization happens because normal people experience cash flow problems.

Life in the US is increasingly expensive, and income is rarely perfectly stable. If you are a freelancer juggling different client projects, your income might be completely unpredictable. You might have $5,000 worth of invoices pending, but if the client takes 45 days to cut the check, you still have to eat. So, you put your groceries, your software subscriptions, and your utility bills on your credit card to survive the month.

Even if you fully intend to pay it off the second your client pays you, the credit bureaus don’t know that. They just see your balance rising closer and closer to your limit, and they hit the panic button.

High utilization is also frequently caused by sudden emergencies. A blown car transmission, an unexpected trip to the vet, or a surprise medical emergency will instantly eat up a $3,000 credit limit. (If you are currently juggling massive health expenses, check out our guide on What To Do If Medical Bills Are Destroying Your Budget).

It is a survival mechanism. You use the credit card because you have to. But the algorithm only sees the math, not the context.

The Panic Trap: Common Beginner Mistakes

When people see their credit score drop due to high utilization, they usually try to fix it quickly. Unfortunately, misunderstanding how the system reports data leads to three very common mistakes that actually make the problem much worse.

Mistake 1: Waiting Until the Due Date to Pay This is the biggest trap in personal finance. You get your credit card statement, it says your payment is due on the 24th of the month, so you pay your balance in full on the 23rd. You think you are doing everything perfectly. Here is the secret: credit card companies usually report your balance to the credit bureaus on your Statement Closing Date, which is usually three weeks before your actual Due Date. If you spend $2,000 on a card with a $3,000 limit, the bank reports a 66% utilization to the bureaus on your statement date. Even if you pay it down to zero a week later before the due date, the credit bureaus already recorded the high balance. Your score drops, and you are left completely confused.

Mistake 2: Closing Old, Unused Credit Cards Let’s say you finally pay off a credit card that has been stressing you out for years. You hate that card. You want it out of your life, so you call the bank and cancel the account. You just accidentally spiked your overall utilization. Remember, utilization is your total debt divided by your total limit. If you close a card with a $5,000 limit, you just permanently removed $5,000 from the bottom of your math equation. Your overall available credit shrinks, which means any remaining debt you have on other cards now takes up a much larger percentage of your overall limit.

Mistake 3: Putting Rent on a Credit Card for “Points” It sounds like a great life hack. You use a third-party service to pay your $2,000 rent with your rewards credit card to earn points, planning to pay it off over time. However, if your credit limit is only $3,000, that rent payment instantly spikes your utilization to 66%. The tiny amount of cash back or travel points you earn will never outweigh the massive damage done to your credit score, especially if you carry that balance and get hit with 25% interest.

Real Consequences: Why 30% Is the Magic Line

Why does the algorithm freak out when you cross 30%? Because statistical data shows that people who max out their credit lines are significantly more likely to default on their debts in the near future.

To a lender, high utilization screams, “This person is running out of their own money and is surviving on borrowed cash.”

The consequences of this label are heavy:

- Plummeting Scores: Going from 10% utilization to 80% utilization can drop an excellent credit score by 50 to 100 points almost overnight.

- Loan Denials: If you apply for a mortgage or an auto loan, the underwriter will manually look at your utilization. Even with a decent score, maxed-out revolving debt is a massive red flag that can result in an instant denial.

- Higher Interest Rates: If you do get approved for a car loan, a low score caused by high utilization will force you into a subprime interest tier, costing you thousands of extra dollars over the life of the loan.

- Account Closures: In extreme cases, if you max out multiple cards simultaneously, credit card issuers might view you as a “flight risk” and abruptly lower your credit limits or close your accounts entirely to limit their exposure. (If this has already happened to you, read How Long Does It Really Take To Rebuild Bad Credit? for your next steps).

How Long Does It Take Credit Utilization To Update?

If you are ready to fix this, you are probably wondering how long you have to wait for the results.

Most credit card issuers report balances to the credit bureaus every 30 days, usually around your statement closing date. Once a lower balance is reported, credit score improvements can often appear within a few weeks. Because utilization has no “memory” in standard scoring models, the moment the new, lower balance hits your report, your score bounces back.

Practical Solutions: The Fastest Ways to Lower Credit Utilization

Alright, the financial lecture is over. Let’s talk strategy. If your score has tanked and you need to get your utilization down as fast as humanly possible, here are the most effective, proven methods.

Method 1: The “Statement Date” Hack

Remember Mistake #1? We are going to flip that and use it to our advantage.

Log into your credit card portal and find your last PDF statement. Look for the “Statement Closing Date” (this is different from your Payment Due Date).

If you want to lower your reported utilization without actually changing how much money you spend, simply pay your credit card balance down to zero two days before the Statement Closing Date.

When the bank takes their snapshot to send to the credit bureaus, they will see a zero balance. They will report 0% utilization, and your credit score will shoot up, even if you start using the card again the very next day. You are simply beating the bank’s reporting system to the punch.

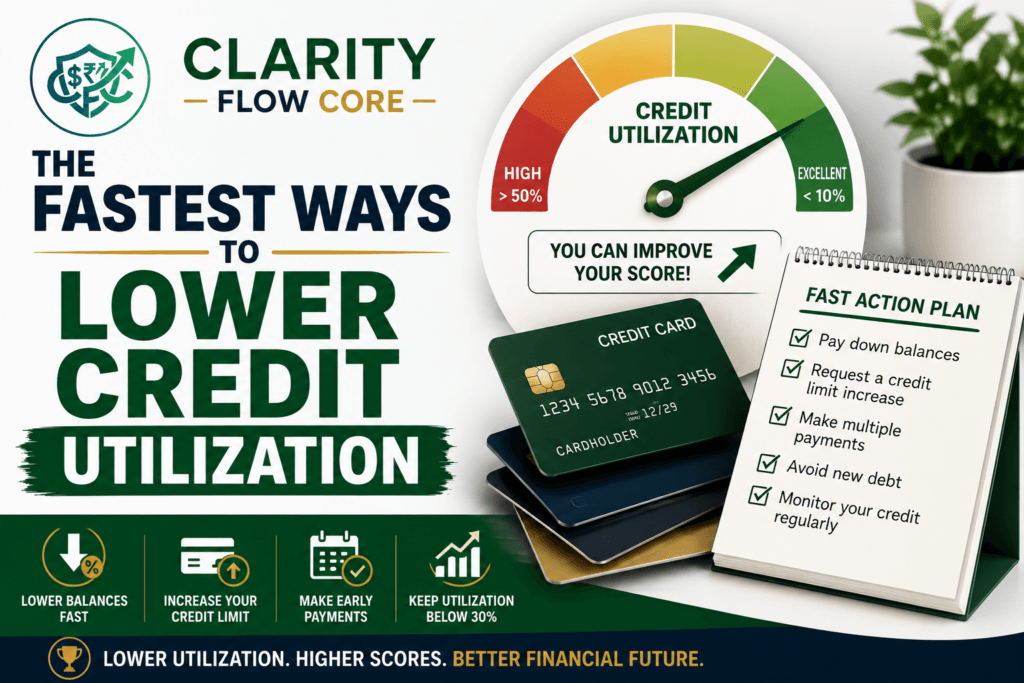

Method 2: Ask for a Credit Limit Increase

This is a pure math hack. Since utilization is Debt divided by Credit Limit, you can lower the percentage by either decreasing the debt (paying it off) or increasing the limit.

Call your credit card company or log into your app and request a credit limit increase. If you have been a good customer and have a decent history with them, they will often grant this instantly.

If you have a $2,500 balance on a $5,000 card, your utilization is 50%. If you ask for a limit increase and they bump your limit to $10,000, your balance is still exactly $2,500, but your utilization instantly drops to a perfect 25%. You fixed your credit score without spending a single dollar.

(Warning: Only do this if you have the discipline not to spend the new limit. Also, ensure the bank only does a “soft pull” on your credit to grant the increase; a “hard pull” will temporarily ding your score).

Method 3: Make Micro-Payments Throughout the Month

If you don’t have the cash to pay the card down to zero before the statement closes, change the frequency of your payments.

Instead of waiting until the end of the month to make one big payment, make weekly micro-payments. Every Friday, transfer whatever spare cash you have—$50, $100, $20—directly to your credit card.

By constantly chipping away at the balance throughout the month, you ensure that whenever the credit card company decides to report your balance to the bureaus, the number will be significantly lower than if you had let the purchases stack up for 30 days.

Method 4: The Debt Avalanche or Snowball

If your utilization is high because you are trapped in legitimate, long-term credit card debt, you cannot hack your way out of it. You have to pay the piper.

You need a structured debt payoff strategy.

- The Debt Avalanche: You list all your cards and put every spare dollar toward the card with the highest interest rate. This saves you the most money mathematically.

- The Debt Snowball: You list all your cards and pay off the one with the smallest balance first to get a quick psychological win.

Whichever method keeps you motivated is the right one. The goal is to aggressively attack the balances to free up your utilization. If you are struggling to figure out where the money will come from, review our guide on Behind on Bills? Which Payments Should You Prioritize First?.

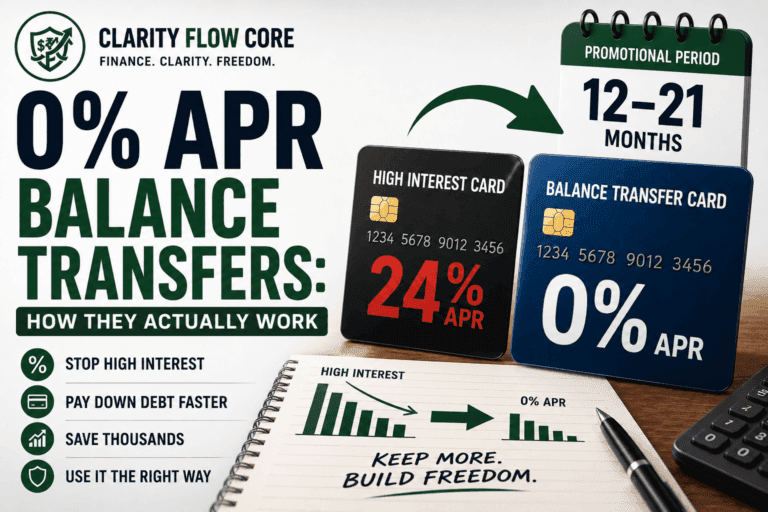

Method 5: Strategic Balance Transfers (Proceed with Caution)

If you have a maxed-out card sitting at 25% interest, your monthly payment is barely covering the interest charges, making it impossible to lower the utilization.

If your credit score is still decent, you can apply for a 0% APR Balance Transfer Credit Card. You transfer the heavy debt from your high-interest card to the new 0% card.

How does this help utilization? First, it stops the interest from compounding, allowing your payments to actually reduce the principal balance. Second, opening a new card increases your overall available credit limit, which mathematically lowers your overall utilization ratio.

Crucial Warning: This only works if you do not add new debt to the old card you just emptied out. If you transfer the balance and then run up the original card again, you have just doubled your debt and completely ruined your finances.

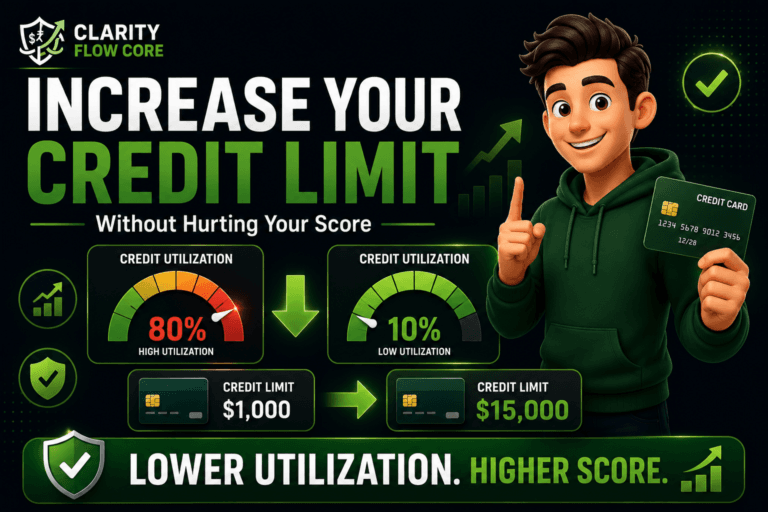

Your Beginner-Friendly Action Plan

Information is useless without execution. If you are stressed about your credit utilization today, here is exactly what you are going to do over the next 30 days.

Step 1: Map Your Deadlines Log into every credit card account you own. Write down the Due Date, and more importantly, the Statement Closing Date for every single card. Put these dates in your phone calendar with reminders.

Step 2: Request the Soft-Pull Increases Log into the apps for your oldest, best-standing credit cards. Look for the “Request Credit Limit Increase” button. Make sure it explicitly says it will not impact your credit score (soft pull), and submit the request.

Step 3: Shift to the Pre-Statement Payoff Look at the calendar you just made. For the cards you actively use for daily expenses (like groceries or gas), schedule your monthly payment to clear your bank account three days before the statement closing date.

Tool Suggestion: Use our free Credit Utilization Target Calculator to plug in your current limits and find out the exact dollar amount you need to pay down this week to hit that golden 10% or 30% threshold.

Step 4: Stop the Bleeding If you have a card that is carrying a heavy, revolving balance, take it out of your wallet. Remove it from your Apple Pay. Delete the card number from your Amazon account. You cannot lower the utilization on a card if you are still actively spending money on it.

Frequently Asked Questions (FAQs)

Will paying off a credit card immediately raise my score? Not instantly. Your score usually updates after the credit card issuer reports your new balance to the credit bureaus. Depending on the issuer, this can take anywhere from a few days to several weeks.

Does credit utilization have a memory? Under the most widely used scoring models today (like FICO 8), credit utilization has zero memory. This is incredible news for you. It means that if you have been maxed out at 90% utilization for two years, but you pay the card off tomorrow, your score will bounce back entirely the moment the new 0% balance is reported. The algorithm does not care about your past high balances, only what your balance is right now. (Note: Newer models like FICO 10T are starting to look at “trended data” over 24 months, but FICO 8 is still the standard for most consumer lending).

What is the perfect credit utilization number? While keeping it under 30% is the standard advice to avoid being penalized, the absolute optimal zone for a perfect credit score is between 1% and 9%.

Is a 0% credit utilization bad? Surprisingly, yes. Having a 0% reported utilization across every single card you own can actually result in a slightly lower score than having a 1% or 2% utilization. To the algorithm, 0% looks like you aren’t using credit at all. The sweet spot is to use the card for a small purchase (like a $10 Spotify subscription) and let that small amount post to the statement before paying it off.

Can becoming an Authorized User lower my utilization? Yes. If you have a trusted family member with an old credit card that has a massive limit and a zero balance, they can add you as an “Authorized User.” That card’s massive, empty credit limit will suddenly appear on your credit report, dramatically lowering your overall utilization ratio without you having to do anything.

A Final Word on Your Financial Peace

Watching your credit score drop is incredibly disheartening, especially when you feel like you are working so hard just to keep your head above water. It is easy to look at a three-digit number and feel like a financial failure.

Please remember that your credit score is not a reflection of your character, your work ethic, or your worth. It is a highly sensitive, robotic math formula that only sees a tiny snapshot of your life.

Credit utilization is a mathematical game. By understanding the rules—knowing when your statement closes, asking for limit increases, and strategically timing your payments—you can take the power away from the algorithm and put it back in your own hands.

It might take a few weeks for the reporting cycles to catch up, but if you execute the plan, that score will climb back up. Be patient with the process, be kind to yourself, and take it one statement date at a time.

Trusted Resources

To help ensure the information in this guide is accurate and up to date, we reviewed educational materials from leading consumer finance organizations, credit reporting agencies, and official government resources.

- FICO® — What’s in Your FICO® Score? (Explains how credit utilization influences FICO® Scores.)

- Experian — Credit Utilization Ratio: What It Is and Why It Matters

- Equifax — Understanding Credit Utilization and Credit Scores

- Consumer Financial Protection Bureau (CFPB) — Credit Reports and Scores

- AnnualCreditReport.com — The federally authorized website where U.S. consumers can obtain free credit reports from Equifax, Experian, and TransUnion.

- Consumer.gov — Building a Better Credit Report

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

2 Comments

Comments are closed.