Personal Loan vs. Balance Transfer Card: Which Makes More Sense?

If you are carrying a massive credit card balance at a 24% interest rate, doing absolutely nothing is the most expensive mistake you can make. When a quarter of your monthly payment is vaporized by interest charges before it ever touches the principal, you are fighting a mathematical war you cannot win. (Learn the full impact of these high costs by reading What Happens If You Only Pay the Minimum on a Credit Card?).

When it is finally time to consolidate that debt and take back your cash flow, you usually hit a crossroads. You have two distinct exit strategies: you can take out a fixed installment loan, or you can shift that massive balance over to a specialized promotional credit card.

The real question is: which route actually saves you money personal loan vs balance transfer?

⚡ Quick Answer

- A balance transfer card is often the cheaper option because it can temporarily eliminate interest through a 0% APR promotion, provided you pay off the balance before the offer expires.

- A personal loan may be a better fit when you need a fixed payoff schedule, a longer timeline to eliminate debt, or lower monthly payments.

- The Verdict: The right choice depends on your credit profile, your repayment timeline, and your ability to avoid accumulating new debt.

When debating a personal loan vs balance transfer, you have to look past the marketing. Both options can rescue you from toxic interest rates, but under the hood, they operate completely differently. One relies on a strict timeline, while the other relies on a fixed structure. Pick the wrong one, and you will get hit with hidden fees or find yourself stuck in the exact same debt trap two years from now.

Here is the exact operational math behind both strategies, the hidden traps you must avoid, and how to definitively choose between a personal loan vs balance transfer based on your specific financial behavior.

The Cost of Doing Nothing

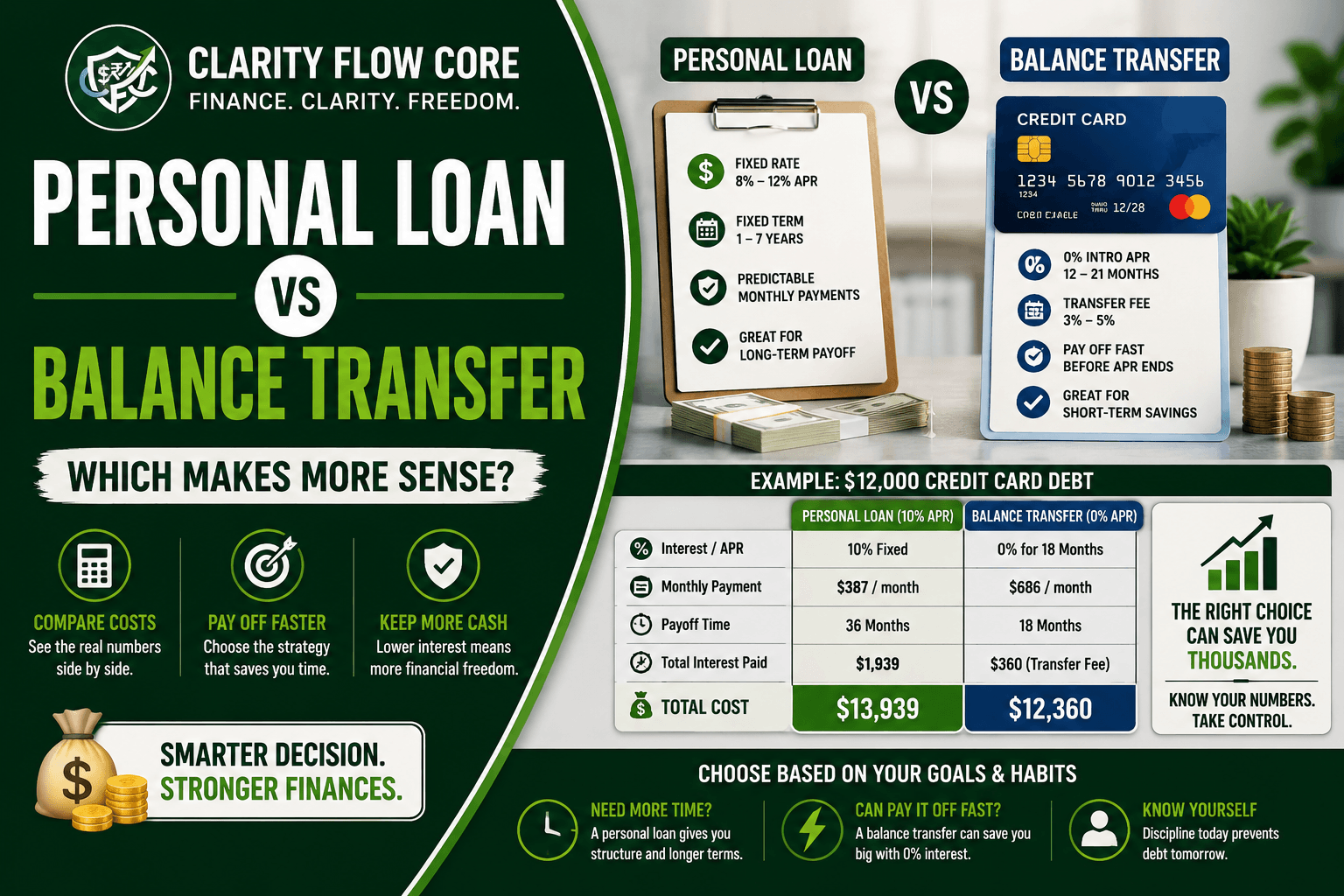

Before we look at the solutions, you have to understand the bleeding. Let’s assume you have a $12,000 credit card balance sitting at a 24% APR. You decide to pay a flat $400 a month toward this debt.

If you leave the debt where it is, it will take you 44 months (nearly four years) to pay it off. Worse, you will hand the bank roughly $5,300 in pure interest charges. You are paying $17,300 for a $12,000 balance. That is why you must intervene.

Option 1: The 0% APR Balance Transfer

When analyzing a personal loan vs balance transfer, the balance transfer is usually the most heavily marketed option. Simply put, you open a new credit card that offers a 0% introductory APR. This grace period usually lasts anywhere from 12 to 21 months. You electronically transfer your old, high-interest debt right onto this new card. (You can read an extensive breakdown of this process in 0% APR Balance Transfers: How They Actually Work).

The Mathematical Advantage

The magic of this strategy is the total pause on compounding interest. While that promotional window is active, every single dollar you send to the bank violently attacks the principal balance. The bank gets nothing extra.

However, banks do not move money for free. They charge an upfront Balance Transfer Fee, which is almost always 3% to 5% of the total amount moved.

Let’s look at the math on that $12,000 debt if you move it to an 18-month 0% APR card with a 3% fee:

- Transfer Fee: $360 (Added to your balance)

- New Principal Balance: $12,360

- Target Monthly Payment (to clear in 18 months): $686/month

- Total Cost to You: $12,360

By paying a one-time $360 fee, you save nearly $5,000 in interest compared to doing nothing.

The Operational Drawbacks

- The Ticking Clock: If you do not clear the balance before the 18-month promo expires, standard, sky-high interest rates immediately kick in on whatever balance is left over.

- Credit Limits: To move a mountain of debt, you need an excellent credit score so the new bank actually approves a limit high enough to hold your transfer.

Option 2: The Personal Consolidation Loan

On the other side of the personal loan vs balance transfer debate is the fixed installment loan. Think of a debt consolidation loan as a lump-sum cash drop from an online lender or a local credit union.

(Note: You can also use this same mechanism for the inverse. See Can You Use a Balance Transfer Card to Pay Off a Personal Loan? to learn how to move an installment balance to a credit card).

The Mathematical Advantage

There is no 0% magic trick here. You still pay interest. However, a personal loan interest rate (often between 8% and 12% for good credit) easily beats a 25% credit card.

Let’s look at the exact same $12,000 debt. You take out a 3-year (36-month) personal loan at a 10% APR.

- Monthly Payment: $387/month

- Total Time to Payoff: 36 Months

- Total Interest Paid: $1,939

- Total Cost to You: $13,939

While this costs you more than the balance transfer, it drops your monthly payment to a highly manageable $387, and still saves you over $3,300 compared to leaving the debt on your original credit card.

The Operational Drawbacks

- Origination Fees: Many personal loan companies skim an “origination fee” (usually 1% to 6%) right off the top.

- You Pay Interest: Unlike a balance transfer, you are still bleeding some cash to the bank every month.

How to Choose: Personal Loan vs Balance Transfer

The winner of the debate comes down to your timeline and self-control.

Choose the 0% Balance Transfer if:

- Your total debt is manageable.

- You have the intense discipline and cash flow required to clear the entire balance in 12 to 18 months.

- You want the absolute cheapest mathematical route to a zero balance.

Choose the Personal Loan if:

- Your debt level cannot realistically be repaid during a typical 0% promotional period.

- You know you struggle with the temptation of open credit limits.

- You need the psychological safety of a fixed, unchangeable monthly payment for the next 3 to 5 years.

If you have multiple types of debt, you might need a broader operational strategy. Check out our deep dive on Debt Avalanche vs. Debt Snowball: Which Debt Payoff Method Works Better? to figure out exactly which account you should attack first.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyFrequently Asked Questions (FAQs)

Can you transfer a personal loan directly to a credit card? Usually not. Most issuers require balance transfer checks or direct deposit transfers rather than direct loan-account electronic transfers.

Does a balance transfer hurt your credit score? It may cause a temporary fluctuation due to a hard inquiry and sudden changes in your credit utilization ratio.

What happens when the 0% APR period ends? Any remaining balance generally begins accruing interest immediately at the card’s standard, variable APR.

Is a balance transfer cheaper than a personal loan? Sometimes. It depends entirely on the transfer fee, the length of the promotional period, and your existing personal loan interest rate.

Can I transfer part of a personal loan balance? In many cases, yes, provided the credit limit on the new card and the specific issuer rules allow it.

References & Trusted Sources

For more information on credit terms, balance transfers, and consumer debt protections, visit:

- Consumer Financial Protection Bureau (CFPB) – Balance Transfers

- Federal Trade Commission (FTC) – Credit Card Terms

- Federal Reserve – Consumer Credit Reports

- Experian Credit Education

- myFICO Credit Education

The Bottom Line

Using a 0% APR credit card to execute a balance transfer personal loan payoff is a brilliant financial hack—but only if you treat it with militant discipline.

It stops the bleeding of high interest charges immediately and forces every dollar you pay to attack the principal balance. If you are currently using the Debt Avalanche vs. Debt Snowball method to clear your accounts, freezing the interest on your largest loan can drastically accelerate your timeline.

Run the math on the transfer fees, calculate your mandatory monthly payment, set up autopay, and use this strategy to recapture your financial freedom. Once your debt is managed, continue to protect your financial profile by understanding What Is Credit Utilization and Why Does It Matter? and monitoring how your choices impact your report with FICO vs. VantageScore: Why Credit Scores Differ Between Apps.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.