Leasing vs. Buying Used Cars: Which Actually Costs Less?

When you walk into a car dealership, the salesperson will ask you one question before you even look at a vehicle: “What monthly payment are you looking for?”

If you answer that question, you have already lost the negotiation.

Dealerships want you to focus on the monthly payment because it hides the total cost of the vehicle. By stretching out the loan term or switching you to a lease, they can make a $40,000 car look exactly like a $20,000 car on paper.

To stop overpaying for depreciating assets, you have to completely ignore the monthly payment and look at the total lifecycle cost.

Here is the exact math behind leasing vs. buying used, how the financing actually works, and where most buyers bleed cash without realizing it.

The Monthly Payment Illusion

A car is not an investment. It is an expense. From the moment you drive it off the lot, it loses value.

Because of this, your goal is not to buy a car that makes you money. Your goal is to buy a reliable vehicle that drains as little of your net worth as possible over the next decade.

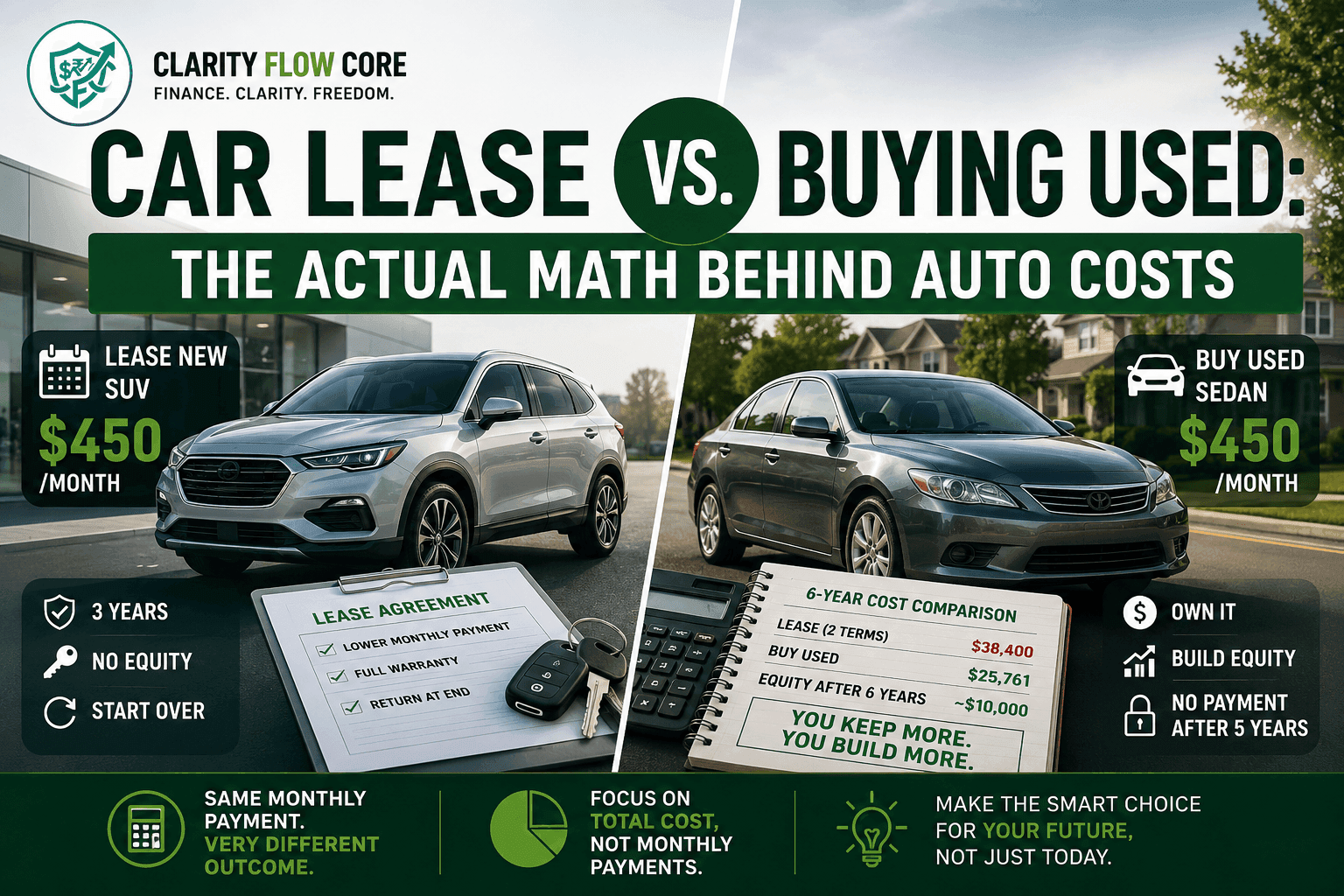

Let’s assume you have a firm rule based on The 50/30/20 Budget Rule Explained Simply. You know you can only afford to allocate $450 a month to a vehicle.

If you tell a dealership your budget is $450, they will present you with two options:

- Lease a brand-new, $35,000 SUV for 3 years.

- Finance a 4-year-old, $22,000 used sedan for 5 years.

Both result in a $450 monthly payment. They feel identical to your checking account right now. But over a six-year timeline, one of these options destroys your wealth, and the other leaves you with a paid-off asset.

To see why, we have to run the hard numbers.

Scenario A: The Used Car Math

Let’s look at buying the $22,000 used car.

You put down $2,000 in cash. You finance the remaining $20,000 with a traditional bank auto loan. Because used car interest rates are slightly higher than new car rates, you secure a 5-year (60-month) loan at a 7% interest rate.

Here is what that actually costs you:

Used Car Financing (5 Years)

| Item | Amount |

| Purchase Price | $22,000 |

| Down Payment | $2,000 |

| Monthly Payment | $396 |

| Total Interest Paid | $3,761 |

| Total Out-of-Pocket Cost | $25,761 |

For 60 months, you pay $396. It feels like a standard bill. But the magic happens in month 61.

Your loan is gone. You now own the car free and clear. (You might even notice a temporary dip in your credit score, which is completely normal—you can read Why Your Credit Score Dropped After Paying Off Your Car Loan for why that happens).

If you keep driving this car for three more years without a payment, you save almost $15,000 in cash flow that you can redirect toward investments or housing. Furthermore, even as a depreciating asset, an 8-year-old sedan is still worth around $8,000 to $10,000 if you decide to sell it.

You have equity.

Scenario B: The New Car Lease Math

Now let’s look at the lease for the $35,000 new SUV.

Leasing feels incredibly attractive because you get a vehicle under full warranty, with zero miles, for a lower monthly payment than buying it outright.

But a lease is not a loan. A lease is simply a long-term rental agreement where you are paying the dealership specifically for the vehicle’s depreciation.

When you sign a 3-year lease, the bank estimates what the car will be worth at the end of the term. This is called the Residual Value. If the $35,000 SUV will be worth $21,000 in three years, it will lose $14,000 in value while you drive it.

Your lease payment is simply that $14,000 divided by 36 months, plus a hefty interest charge (called a “Money Factor” in leasing terms) and dealership fees.

New Car Lease (3 Years)

| Item | Amount |

| Vehicle Price (Capitalized Cost) | $35,000 |

| Down Payment (Due at Signing) | $3,000 |

| Monthly Payment | $450 |

| Total Out-of-Pocket Cost | $19,200 |

You pay $19,200 over three years. Then, you hand the keys back to the dealership. You walk away with absolutely nothing. You have zero equity.

To keep driving, you have to start the cycle completely over.

Leasing vs Buying Used: The 6-Year Comparison

To truly compare leasing vs buying used, you cannot look at a single 3-year snapshot. You have to look at a longer timeline—let’s use 6 years.

The Leaser’s 6-Year Reality:

You sign a 3-year lease. When it ends, you need a car, so you sign another 3-year lease.

- You pay a $3,000 down payment twice.

- You make a $450 payment for 72 consecutive months.

- Total Cost over 6 years: $38,400.

- Asset Value Owned at Year 6: $0.

The Buyer’s 6-Year Reality:

You buy the $22,000 used car. You put $2,000 down. You pay $396 a month for 5 years. In year 6, you have no car payment.

- Total Cost over 6 years: $25,761.

- Asset Value Owned at Year 6: ~$10,000.

When you factor in the retained value of the used car, the person who leases spends roughly $22,000 more over a six-year period to get from point A to point B. That is a massive hit to your net worth just to have a newer dashboard and the smell of fresh upholstery.

The Hidden Costs of Both Options

The monthly payment to the bank is only half the story. Both strategies come with ongoing operational costs that you must factor into your budget.

1. Insurance Premiums

If you lease a car or finance it through a bank, you are legally required to carry full coverage insurance (Comprehensive and Collision). However, insuring a brand-new $35,000 SUV will almost always cost significantly more than insuring a 4-year-old sedan. If you are trying to cut costs, you need to read Practical Ways to Lower Insurance Costs Without Cutting Coverage before you step onto the lot.

2. Maintenance and Tires

When you lease, the car is under warranty. If the transmission blows, the dealership pays for it. When you buy a used car, you are the warranty. You have to pay for oil changes, brake pads, and eventually, new tires.

Many people use “maintenance costs” as an excuse to lease. They say, “I don’t want to deal with a $1,000 repair bill, so I’ll just lease.”

This is terrible math. You are guaranteeing a $19,000 loss over three years to avoid a potential $1,000 repair. Instead of leasing, just use your bank’s automation tools to set aside money specifically for car repairs. If you understand How Sinking Funds Protect Your Emergency Savings, a $600 brake job on a used car is a minor inconvenience, not a financial crisis.

3. Mileage Penalties

Leases come with strict mileage caps—usually 10,000 to 12,000 miles per year. If you change jobs and suddenly have a longer commute, you will be penalized heavily at the end of the lease, often paying 25 cents for every mile you go over the limit. When you own the car, you can drive it as much as you want.

When Leasing Actually Makes Sense

When debating leasing vs buying used, remember that while buying used is mathematically superior for 90% of people, there are specific scenarios where a lease is the right operational move.

1. You are a Freelancer or Business Owner

If you use your car for business, a lease can offer massive tax advantages according to the IRS. In many cases, you can write off a large percentage of your lease payment, gas, and insurance as a business expense. (If you earn 1099 income, cross-reference this with your Freelancer Tax Deductions: Common Expenses You May Be Able to Claim guide to see if you qualify).

2. Cash Flow is Exceptionally High

If you have a high income, no high-interest consumer debt, fully funded retirement accounts, and you simply value driving a new, ultra-safe car every three years—leasing is fine. It is a luxury expense. As long as you treat it like a luxury expense and not a “savvy financial hack,” there is nothing wrong with paying for convenience.

3. Electric Vehicle (EV) Technology

The EV market is evolving incredibly fast. A used EV from four years ago might have half the battery range of a new one today, and replacing EV batteries out-of-pocket can cost $10,000 to $15,000. Leasing an EV protects you from being stuck with obsolete battery technology while the market stabilizes.

When Buying Used Backfires

Buying used is the safest financial path, but it can blow up in your face if you make these common mistakes:

- Buying Used Luxury: Buying a 6-year-old BMW or Mercedes because it “fits your monthly payment” is a catastrophic mistake. Luxury cars depreciate rapidly for a reason. Once the warranty expires, the parts and specialized labor required to fix them are incredibly expensive. A $3,000 suspension repair will instantly wipe out the money you saved by buying used. Stick to highly reliable brands like Toyota or Honda.

- Stretching the Loan to 72 or 84 Months: Dealerships will try to get your monthly payment down by offering you a 7-year loan on a used car. Never do this. The car will break down or need replacing long before you finish paying it off. You will end up “underwater”—meaning you owe the bank more money than the car is actually worth. If you cannot afford the 48-month or 60-month payment, you cannot afford the car. You can learn more about safe loan structures via the Consumer Financial Protection Bureau (CFPB).

- Skipping the Pre-Purchase Inspection (PPI): Never trust a dealership’s “150-point inspection.” Before you sign the paperwork on a used car, take it to an independent mechanic. Pay them $150 to inspect it on a lift. That $150 will save you from buying a vehicle with a hidden transmission leak or a rusted frame.

The Actionable Takeaway

Dealerships are highly optimized sales environments designed to extract maximum profit by confusing you with monthly payment math.

To win, you must calculate the total cost of the vehicle over a 5 to 7-year horizon.

If you want to build wealth, your primary objective should be entirely eliminating your car payment as fast as possible. Buy a reliable used car. Secure your financing from a local credit union before you walk into the dealership. Pay it off. Then, keep driving it for years while you redirect that $450 a month into assets that actually pay you back.

Sources & References

Whenever applicable, articles published on Clarity Flow Core are reviewed using publicly available information from official financial institutions, government resources, and trusted industry publications.

Common reference sources include:

- Edmunds

- Kelley Blue Book

- Internal Revenue Service (IRS)

- Consumer Financial Protection Bureau (CFPB)

- Consumer Reports

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Always consult with a qualified financial professional before making major purchasing or financing decisions.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.