1099 Taxes Explained for Freelancers and Side Hustlers

Welcome to the club if you started a side business this year. To keep up with the soaring cost of living, millions of working professionals are driving for Uber, selling digital templates on Etsy, or securing freelance consulting contracts on Upwork. It is a fantastic method to accelerate your savings and execute the Debt Avalanche vs. Debt Snowball payoff strategy faster.

But anyone who has successfully built an independent income stream will tell you a harsh truth: the instant you find out how side hustle taxes actually work, it is terrifying.

When you have a regular W-2 job, your employer magically takes care of the taxes behind the scenes before the money even hits your checking account. You get a paycheck, and you know exactly how much money you have to safely spend.

When you work as an independent contractor, you are completely on your own. When it comes to your side hustle taxes, the IRS expects you to act like a Chief Financial Officer. They expect you to track your revenue, do the complex arithmetic, and voluntarily send them their cut four times a year. If you ignore your side hustle taxes, the financial penalties are incredibly harsh and compound rapidly.

This is the exact operational framework for handling 1099 income without going crazy, and how you can avoid a massive, surprise tax bill next April.

What is a 1099-NEC?

The foundation of managing side hustle taxes is understanding exactly how the government tracks your money.

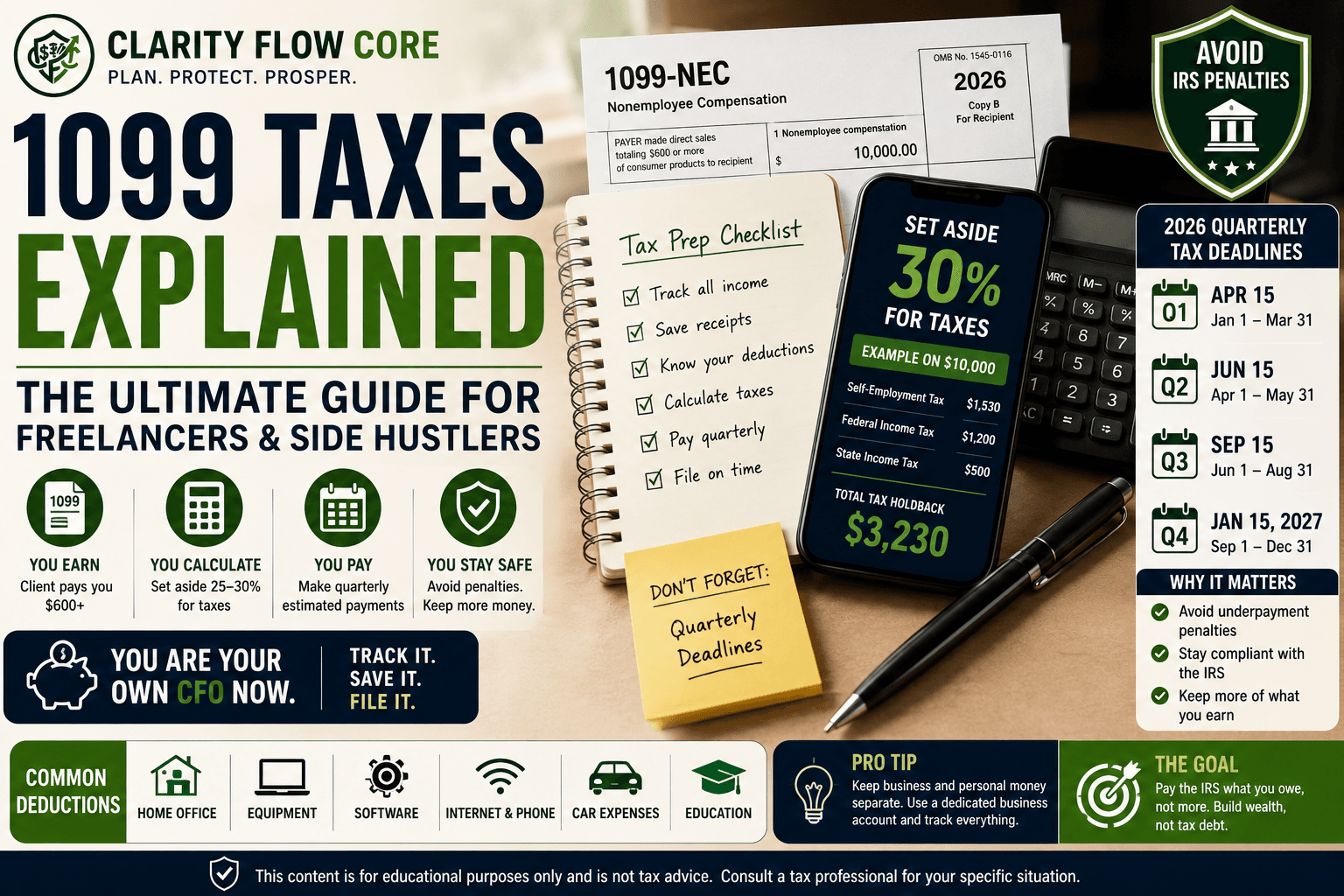

Let’s start with the absolute fundamentals. If a business, agency, or platform pays you more than $600 in a calendar year for work you performed, they are legally required to issue you a document called a 1099-NEC (Nonemployee Compensation). You will usually receive this form in the mail or via email by the end of January of the following year.

This is where beginners get incredibly confused: this form does not just go to you.

The client sends one copy to you, and they send an identical copy straight to the IRS. That means that before you even sit down to start filing your paperwork, the federal government already knows exactly how much money you made. Do not attempt to hide this income.

- The $600 Myth: What if you earned $500 from a client and they did not send you a form? You are still required by law to report that income when filing your side hustle taxes. The $600 mark is simply the threshold that forces the client to generate the paperwork. It does not mean you get to illegally overlook smaller payments.

What If I Never Receive a 1099?

Many freelancers panic when a client forgets to send a 1099-NEC. The important thing to remember is that you must report all business income, regardless of whether you receive a tax form. The IRS requirement applies to the income itself, not the paperwork. Keep your own records throughout the year and report the full amount earned.

The Math: The Double Whammy of Self-Employment

This is the mathematical reality that surprises every first-time freelancer and leaves them owing thousands of dollars.

If you work a corporate W-2 job for someone else, you pay 7.65% of your income to Social Security and Medicare. These are known as FICA taxes. Your employer then legally matches the other 7.65% on your behalf behind the scenes.

When you work for yourself? You are both the boss and the employee.

That means you are legally required to pay the entire 15.3% Self-Employment Tax on your net business income. And yes, this 15.3% is charged on top of the standard federal and state income taxes you already pay. It hurts your cash flow aggressively.

Let’s look at the operational math. If you made $10,000 in pure profit from freelance writing this year:

| Tax Category | The Operational Math | Amount Owed |

| Freelance Profit | Your net income after write-offs | $10,000 |

| Self-Employment Tax | 15.3% flat rate | -$1,530 |

| Federal Income Tax | Assumes a 12% tax bracket | -$1,200 |

| State Income Tax | Assumes a 5% state bracket | -$500 |

| Total Tax Holdback | Roughly 32% of your profit | -$3,230 |

This completely changes the math on your side hustle taxes. If you spend that full $10,000 to upgrade your lifestyle, you will be financially crushed in April. This is exactly why you must route at least 25% to 30% of every single freelance payment into a separate High-Yield Savings Account the very day it clears.

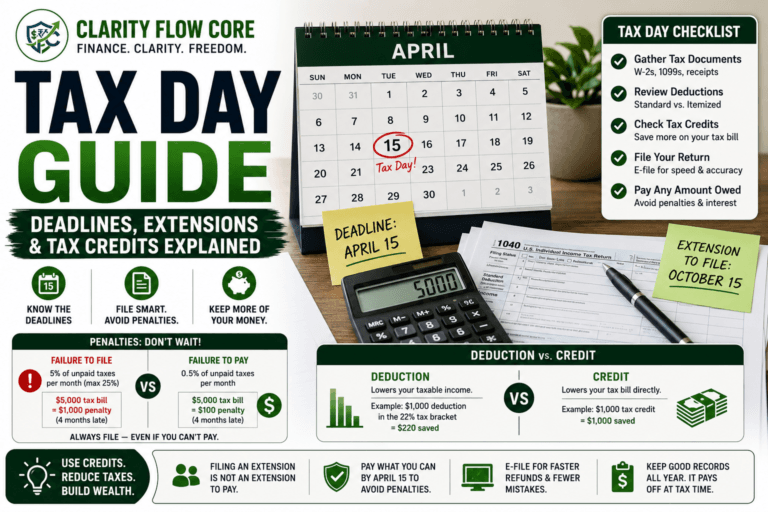

The Deadline Trap: Quarterly Estimated Taxes

The IRS does not want to wait until April to get paid. Because no employer is withholding taxes from your freelance checks, the IRS requires you to pay as you go.

If you estimate that you will owe more than $1,000 in side hustle taxes for the year, you are legally required to make Quarterly Estimated Tax Payments. If you do not pay your total side hustle taxes throughout the year and wait until Tax Day, the IRS will hit you with an Underpayment Penalty.

You must sear this schedule into your calendar:

| Payment Quarter | Income Earned During | IRS Deadline |

| Q1 (First Quarter) | January 1 – March 31 | April 15 |

| Q2 (Second Quarter) | April 1 – May 31 | June 15 |

| Q3 (Third Quarter) | June 1 – August 31 | September 15 |

| Q4 (Fourth Quarter) | September 1 – December 31 | January 15 (Following Year) |

Pro tip: Set a recurring calendar alarm on your phone two weeks prior to each of these dates. You do not need to mail a physical check; you can pay directly online using the IRS Direct Pay portal.

The “Safe Harbor” Rule for Beginners

It is incredibly difficult to predict exactly how much money your freelance business will make this year, which makes guessing your quarterly payments stressful.

To avoid all underpayment penalties, use the IRS “Safe Harbor” rule. As long as you pay the IRS 100% of the total tax liability you owed last year (or 110% if your income is over $150,000), they will not charge you a single penalty, even if your side business explodes and you owe massively more this year. You simply pay the remaining balance in April.

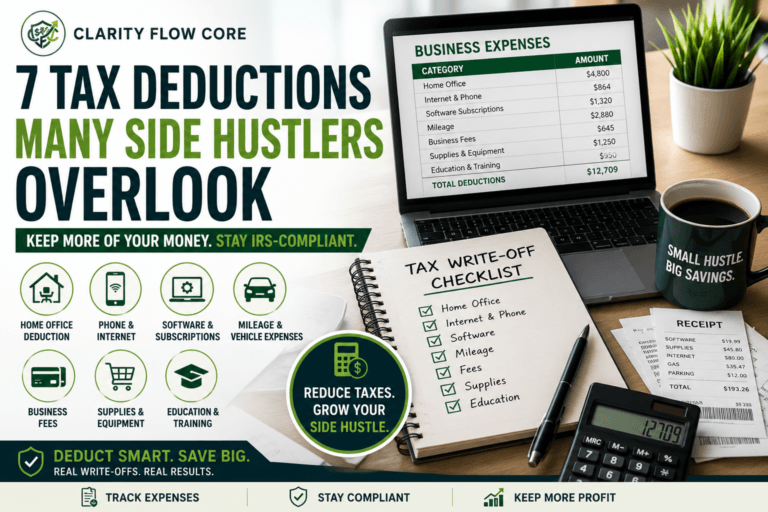

How to Cut Your Bill: The Power of Write-Offs

Now for the profitable part. Unlike W-2 employees, 1099 independent contractors are legally allowed to deduct the cost of doing business from their income. When calculating your side hustle taxes, you do not pay taxes on your gross revenue; you only pay taxes on your net profit (Revenue minus Expenses).

To drastically reduce your side hustle taxes legally, you must track these write-offs:

- The Home Office Tax Break: If you have a dedicated area used regularly and exclusively for business purposes, you may qualify for the home office deduction. To avoid complex math, the IRS offers a “simplified method” allowing you to deduct $5 for every square foot of your office space (up to 300 sq ft).

- Business Mileage: If you drive to meet clients, pick up supplies, or deliver for DoorDash, track your miles. The IRS standard mileage rate is updated periodically. Check the current IRS mileage rate before filing your return. Use a GPS tracking app (like MileIQ) to automate this so you don’t have to keep a messy paper logbook.

- Software & Subscriptions: Do you pay a monthly fee for Adobe Creative Cloud, Squarespace web hosting, Canva Pro, or Zoom? Those are direct operational costs and are 100% deductible.

- The QBI Deduction: This is a massive loophole. The Qualified Business Income (QBI) deduction allows eligible self-employed individuals to deduct up to 20% of their net business income right off the top before income taxes are applied.

(For a deeper dive into maximizing these deductions, read our complete guide on 7 Tax Deductions Many Side Hustlers Overlook.)

When Side Hustle Taxes Backfire

Mastering your side hustle taxes requires a strict operational system. If you treat your freelance income like a casual hobby, the IRS will eventually catch up with you. Here is exactly when and why this system backfires on beginners:

1. The Commingling Trap

If you deposit your freelance checks into the exact same personal checking account you use to buy groceries and pay for Netflix, your accounting will be a disaster. Poor recordkeeping and commingled funds can make it much harder to substantiate deductions during an audit. To survive side hustle taxes, you must open a dedicated Business Checking Account and run all 1099 income and business expenses exclusively through it.

2. The “Write-Off” Fallacy

A common myth is that a tax write-off makes an item “free.” It doesn’t. A write-off simply means you do not pay taxes on the money used to buy the item. If you spend $2,000 on a new laptop just to save $500 on your side hustle taxes, your bank account is still down $1,500. Never buy gear just for the tax deduction.

3. The Hobby Loss Rule

The IRS generally presumes an activity is carried on for profit if it shows a profit in at least three of five consecutive years. Activities that continually generate losses may receive additional scrutiny. Once you are legally classified as a hobby, you are permanently barred from claiming business deductions, but you still have to report the income. You must operate with a legitimate profit motive.

Protecting Your Assets: Sole Proprietor vs. LLC

The moment you accept your first dollar of freelance income, the IRS automatically classifies you as a “Sole Proprietor.” It is simple and requires zero paperwork. However, if your side business starts generating serious revenue, you should consider forming a Limited Liability Company (LLC).

Here is the truth about LLCs: A single-member LLC is taxed the exact same way as a sole proprietorship. An LLC does not magically lower your side hustle taxes. You still file a Schedule C and you still pay the 15.3% self-employment tax.

So why do it? Legal Protection. An LLC can provide important liability protection, but that protection is not absolute. Personal guarantees, negligence, fraud, or improper business practices can still expose personal assets.

(For a complete breakdown of the paperwork and pros/cons, review our comparison: Sole Proprietor vs LLC: Which Is Best for a Side Hustle?)

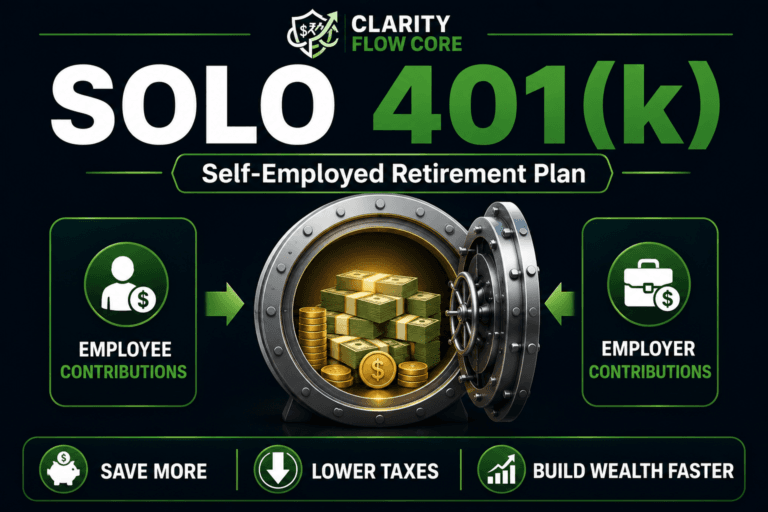

The Ultimate Tax Shield: Solo 401(k) and SEP IRA

If your side job is generating massive cash flow, you can open specialized retirement accounts that standard W-2 employees can only dream of.

Because you are the “employer” of your side hustle, you can open a Solo 401(k) or a Simplified Employee Pension (SEP) IRA. These accounts allow you to shield massive amounts of your freelance income from taxes. With a SEP IRA, you can contribute up to 25% of your net self-employment income entirely pre-tax.

Putting money into these specific accounts directly decreases your taxable income for the year. You legally shrink your side hustle taxes today, while simultaneously building compound wealth that will fund your future. It is the ultimate financial win-win.

Frequently Asked Questions (FAQs)

Do I need to pay taxes if I only made $500 freelancing?

Yes. All self-employment income must generally be reported, even if you do not receive a 1099 form.

How much should freelancers save for taxes?

Many freelancers set aside 25%–30% of their net income, though the correct amount depends on income level, state taxes, and deductions.

Can I deduct my internet bill?

If part of your internet service is used for business purposes, a business-use portion may be deductible.

What happens if I miss a quarterly tax payment?

You may owe penalties and interest, though the amount varies based on circumstances and how much tax was underpaid.

References & Trusted Sources

To ensure your side hustle remains fully compliant, refer to these official IRS guidelines and forms:

- IRS Schedule C (Form 1040): The official form and instructions for reporting profit or loss from a business.

- IRS Publication 334 (Tax Guide for Small Business): The comprehensive tax guide for individuals who use Schedule C.

- IRS Form 1040-ES (Estimated Taxes): The forms, worksheets, and rules for calculating and paying your quarterly estimated tax.

- IRS Self-Employment Tax: A breakdown of exactly how the 15.3% Social Security and Medicare tax is calculated via Schedule SE.

- IRS Home Office Deduction: The official rules for the regular and simplified methods of calculating your workspace write-offs.

- IRS Qualified Business Income (QBI) Deduction: Guidelines on how eligible self-employed individuals can deduct up to 20% of their qualified business income.

The Bottom Line

The first time you have to deal with 1099 side hustle taxes, it is going to feel incredibly stressful. But once you build the operational system, it becomes entirely predictable background noise.

Open a separate business bank account. The moment a client pays you, immediately transfer 30% of that money into a separate tax savings account. Pay your estimated quarterly taxes on time, track your miles, and keep your software receipts. Treat your side hustle like a legitimate business enterprise, and you will never fear the month of April again.’

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

9 Comments

Comments are closed.