Debt-to-Income (DTI) Analyzer & Loan Readiness Planner

If you’re planning to buy a home, finance a vehicle, refinance debt, or apply for a personal loan, your credit score is only part of the equation. Before applying, you should use a debt-to-income ratio analyzer to determine whether your current debt obligations fit within strict lending guidelines and whether you can comfortably handle a new monthly payment.

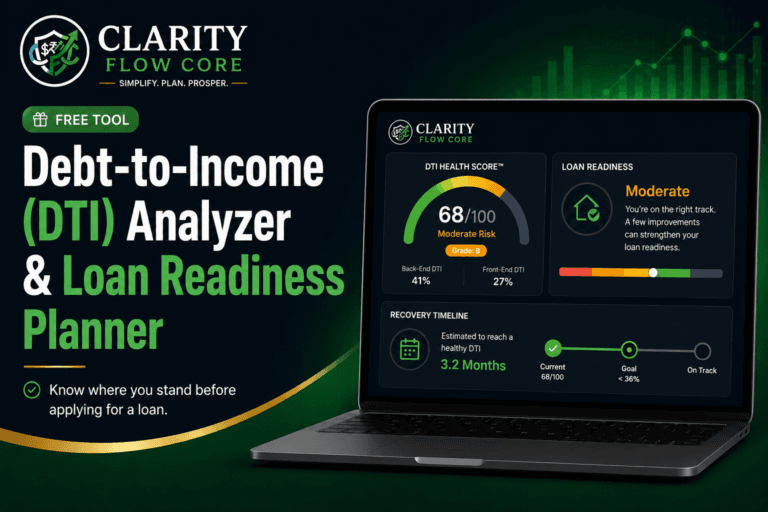

Use our free debt-to-income ratio analyzer below to calculate your exact DTI Health Score™, evaluate your current debt-to-income ratio, understand how lenders may view your application, and discover practical ways to improve your loan readiness before applying for credit.

- ✓ DTI Health Score™ Analysis

- ✓ Mortgage & Loan Readiness Assessment

- ✓ Borrowing Capacity Evaluation

- ✓ Personalized Improvement Recommendations

What You’ll Learn From This Debt-to-Income Ratio Analyzer

This Debt-to-Income Ratio Analyzer goes beyond simply calculating a debt-to-income ratio. It helps you understand:

- Whether lenders are likely to view your application favorably

- How much borrowing capacity you currently have

- Which debts are hurting your approval odds the most

- How close you are to common mortgage and loan qualification thresholds

- What practical actions can improve your DTI ratio fastest

Whether you’re preparing to buy a home, finance a vehicle, refinance debt, or simply improve your financial health, understanding your DTI ratio can help you make better borrowing decisions.

Why Credit Score Alone Doesn’t Determine Loan Approval

Imagine this scenario: You have spent the last three years obsessing over your credit score. You pay every credit card in full. You never miss a payment. Your FICO score is sitting at a beautiful 760. You walk into a bank to get pre-approved for a mortgage, feeling completely confident.

Despite having an excellent credit score, borrowers may still be denied if their income and debt obligations do not meet lender requirements.

For most normal people, this is a completely baffling and deeply embarrassing moment. How can you be denied a loan when your credit score is excellent?

The answer is your Debt-to-Income (DTI) ratio.

If you’re not sure whether your current debt level is healthy, read our guide: How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide.

While your credit score tells a lender how reliably you pay back your debts, your DTI tells them how much cash you actually have left over every month to take on a new payment. You can have a perfect track record of paying your bills, but if too much of your paycheck is already promised to other banks, lenders will view you as a much higher lending risk.

Here is the honest, practical truth about how the DTI system works, why it traps so many hard-working people, and exactly how to reverse-engineer the math to improve your borrowing readiness.

Understanding your DTI is only one part of becoming loan-ready. Your credit profile also plays a major role. Learn more in our guide: What Credit Score Do You Need to Buy a House in 2026?.

The Core Math Behind Our Debt-to-Income Ratio Analyzer

The DTI calculation is just a simple fraction, but lenders generally evaluate it in two distinct ways.

The Front-End Ratio (The Housing Ratio)

This only looks at your housing costs. It takes your proposed monthly mortgage payment (including property taxes and home insurance) and divides it by your gross monthly income (your income before taxes are taken out).

- Most traditional lenders prefer this number to remain below 28%.

The Back-End Ratio (The Total Debt Ratio)

This is the number that affects most loan applications. The back-end ratio includes your housing payment plus every other minimum monthly debt obligation you have. This includes student loans, auto loans, personal loans, and credit card minimum payments.

- Most lenders generally prefer a back-end DTI between 36% and 43%.

Why We Get Blind-Sided by DTI

The main reason people get trapped by their DTI is that we calculate our own affordability differently than the bank does.

When you sit down at your kitchen table to figure out if you can afford a new car payment, you probably look at your checking account. You see that after you pay for groceries, gas, utilities, Netflix, and daycare, you have $600 left over. Logically, you assume you can afford a $400 car payment.

Traditional DTI calculations generally focus on debt obligations relative to gross income and may not account for many day-to-day living expenses. The algorithm does not factor in groceries, utility bills, or daycare costs. It strictly looks at your gross income versus the minimum payments reported on your credit file.

This creates a massive disconnect. You might feel totally broke because childcare is expensive, but the bank thinks you are a great candidate because your official debt payments are low. Conversely, you might feel rich because you live frugally, but if you have a massive student loan payment sitting on your credit report, the bank will reject you.

Common Beginner Mistakes That Tank Your Borrowing Power

When you do not understand how DTI works, it is very easy to accidentally sabotage a major life milestone like buying a house. Here are the traps you need to watch out for.

Mistake 1: Financing a Car Right Before Buying a Home

This is the most common and devastating mistake young adults make. Let’s say you make $6,000 a month. You decide to buy a reliable car and take on a $500 monthly auto loan.

That single $500 payment just ate up roughly 8% of your total borrowing capacity. When you go to apply for a mortgage three months later, the bank subtracts that $500 from what they are willing to lend you for a house. A new auto loan can increase your DTI ratio, which may reduce the mortgage amount you qualify for a home. Always secure the mortgage first, then worry about the car.

Before house hunting, it’s important to understand the full approval process. See our guide: What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline.

Mistake 2: Ignoring the Minimum Payment Math

When looking at your debts, a debt-to-income ratio analyzer relies on the minimum monthly payment required by your card issuer—not the total balance, and not what you actually pay.

If you have a credit card balance of $5,000, but the minimum payment is only $85 a month, the bank only hits your DTI calculation for $85. Many financially stressed borrowers panic and dump all their cash into paying off a credit card right before a loan application. While getting out of debt is great, paying a $5,000 balance down to $2,000 might only lower your minimum payment by $30. Depending on how the lender calculates minimum payments, reducing balances may have a limited impact on DTI compared with eliminating a monthly payment entirely.

Mistake 3: The Hidden Concentration Risk

Sometimes, your overall DTI looks perfectly fine, but the type of debt you have terrifies the lender. While DTI is important, lenders may also review factors such as loan type, payment history, credit score, and overall credit profile.

What Numbers Do Lenders Actually Want to See?

Every lending institution has slightly different rules, and some government-backed loans are more forgiving than others. However, if you want to qualify for the absolute best interest rates, here is the exact scorecard you should aim for:

| Loan Type | Excellent DTI | Acceptable DTI | High Risk DTI |

| Conventional Mortgage | Under 36% | Up to 43% | 45%+ |

| FHA Mortgage | Under 43% | Up to 50% | 55%+ |

| Auto Loan | Under 30% | Up to 40% | 50%+ |

| Personal Loan | Under 20% | Up to 35% | 40%+ |

Actual DTI requirements vary by lender, loan program, compensating factors, and underwriting guidelines.

For example, according to the Consumer Financial Protection Bureau (CFPB), 43% is typically the absolute highest ratio a borrower can have and still get a Qualified Mortgage.

Your DTI ratio is only one factor lenders evaluate. Learn more in our guide: What Credit Score Do You Need to Buy a House in 2026?.

Common Ways to Improve Your Debt-to-Income Ratio

If you ran your numbers through the debt-to-income ratio analyzer above and landed in the “High Risk” or “Caution” tier, do not panic. DTI is a highly fluid metric. You can change it dramatically in just a few months using two specific levers.

Strategy 1: Consider Reducing High Monthly Debt Obligations

When most people try to get out of debt, they focus on the total balance or the interest rate (the Debt Avalanche method). But if your strict goal is to lower your DTI to get approved for a house, the math changes.

You need to eliminate the debt that is eating up the largest monthly payment.

If you have a $2,000 auto loan balance with a $400 monthly payment, and a $8,000 student loan balance with a $150 monthly payment, pay off the car. Eliminating that $2,000 car note frees up $400 of monthly breathing room, which massively improves your DTI ratio overnight.

Strategy 2: Increasing Qualifying Income

DTI is a fraction. If you cannot make the top number (your debt) smaller, you have to make the bottom number (your income) bigger.

If you are planning to apply for a major loan in six months, taking on a side hustle or freelance work can drastically improve your ratio. If your income changes from month to month, see our guide: How to Budget as a Freelancer When Income Changes Every Month.

Just remember that lenders usually want to see a consistent track record of this extra income (often two years of tax returns for self-employment) before they will count it toward your official DTI.

Strategy 3: Strategic Debt Consolidation

If you have five different credit cards, all with $60 minimum payments, you are losing $300 a month in DTI capacity.

If your credit score is still healthy, you can take out a single debt consolidation personal loan to pay off all five cards. If the new personal loan has a monthly payment of $150, you just freed up $150 of DTI capacity without actually paying off the underlying principal yet. (Note: Only do this if you have addressed the spending habits that caused the credit card debt in the first place).

| DTI Ratio | General Interpretation |

| Under 20% | Excellent |

| 20% – 36% | Good |

| 36% – 43% | Acceptable |

| 43% – 50% | Elevated |

| Above 50% | High Risk |

Improve Your Loan Readiness: Recommended Next Steps

Your debt-to-income ratio is one of the most important numbers lenders evaluate, but it is not the only factor that determines whether you qualify for a loan. Your credit score, payment history, savings, down payment, and overall financial profile all play important roles.

Understand Your Debt Situation

- How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide

- Debt Consolidation vs Debt Settlement: Which Actually Saves More Money?

- I Can Only Afford the Minimum Payments — Now What?

- Credit Utilization vs Payment History: Which Matters More?

Improve Your Credit Profile

- 10 Credit Score Mistakes That Can Cost You 100+ Points

- What Credit Score Do You Need to Buy a House in 2026?

- How to Increase Your Credit Limit Without Hurting Your Credit Score

- How Long Do Late Payments Stay on Your Credit Report?

Planning to Buy a Home?

- FHA Loan Requirements 2026: Everything You Need to Know

- FHA Loan vs USDA Loan vs Conventional Loan

- PMI Explained: When Mortgage Insurance Is Required

- What Happens After Mortgage Pre-Approval? A Step-by-Step Timeline

- Closing Costs Explained: What Home Buyers Actually Pay

- How Much Down Payment Do You Really Need to Buy a House?

Related Financial Planning Tools

- Mortgage Affordability Calculator & Home Buying Planner

- Credit Score Simulator & Improvement Planner

- Financial Freedom Planner

- Advanced Emergency Fund Analyzer

Frequently Asked Questions

Does my DTI affect my credit score?

No. Your DTI ratio is never explicitly calculated into your FICO credit score. The credit bureaus do not know your income, so they cannot mathematically calculate your DTI. Lenders pull your credit report to see your debts, and then ask for your pay stubs to calculate the DTI themselves.

Do rent, utilities, or cell phone bills count toward my DTI?

No. Only debts that report to the major credit bureaus are included in your back-end DTI. Utilities, groceries, cell phone plans, and health insurance premiums are completely ignored by the algorithm.

What is considered a good debt-to-income ratio?

Most lenders prefer a DTI below 36%, though acceptable ranges vary by loan type and lender.

How do I calculate my debt-to-income ratio?

Divide your total monthly debt payments by your gross monthly income and multiply by 100.

Example: $2,000 debt payments ÷ $6,000 income = 33.3% DTI.

Can I get a mortgage with a 50% DTI?

Some loan programs may allow higher DTI ratios, but approval depends on lender guidelines, credit profile, down payment, and compensating factors.

Does paying off a car loan lower DTI?

Yes. Eliminating a monthly loan payment reduces your monthly debt obligations, which may lower your DTI ratio.

What if I have a co-borrower?

If you apply for a loan with a spouse or partner, the bank calculates a combined DTI. They add both of your monthly gross incomes together, and they add both of your individual debt obligations together. A co-borrower with zero debt and a high income can completely rescue your DTI. Conversely, a co-borrower with massive student loans can tank your chances of approval.

The Bottom Line

Your debt-to-income ratio is one of the clearest indicators of your financial capacity from a lender’s perspective. While a strong credit score demonstrates responsible borrowing behavior, your DTI ratio helps lenders determine whether you realistically have room in your budget for additional debt.

The good news is that DTI is highly flexible. Reducing high monthly debt payments, increasing qualifying income, and improving your overall financial profile can significantly improve your borrowing power over time.

Use the debt-to-income ratio analyzer above to understand exactly what lenders see, identify potential roadblocks before applying, and create a practical plan to improve your approval odds. Whether you’re preparing to buy a home, finance a vehicle, refinance debt, or simply strengthen your financial foundation, understanding your DTI ratio is one of the smartest steps you can take.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.