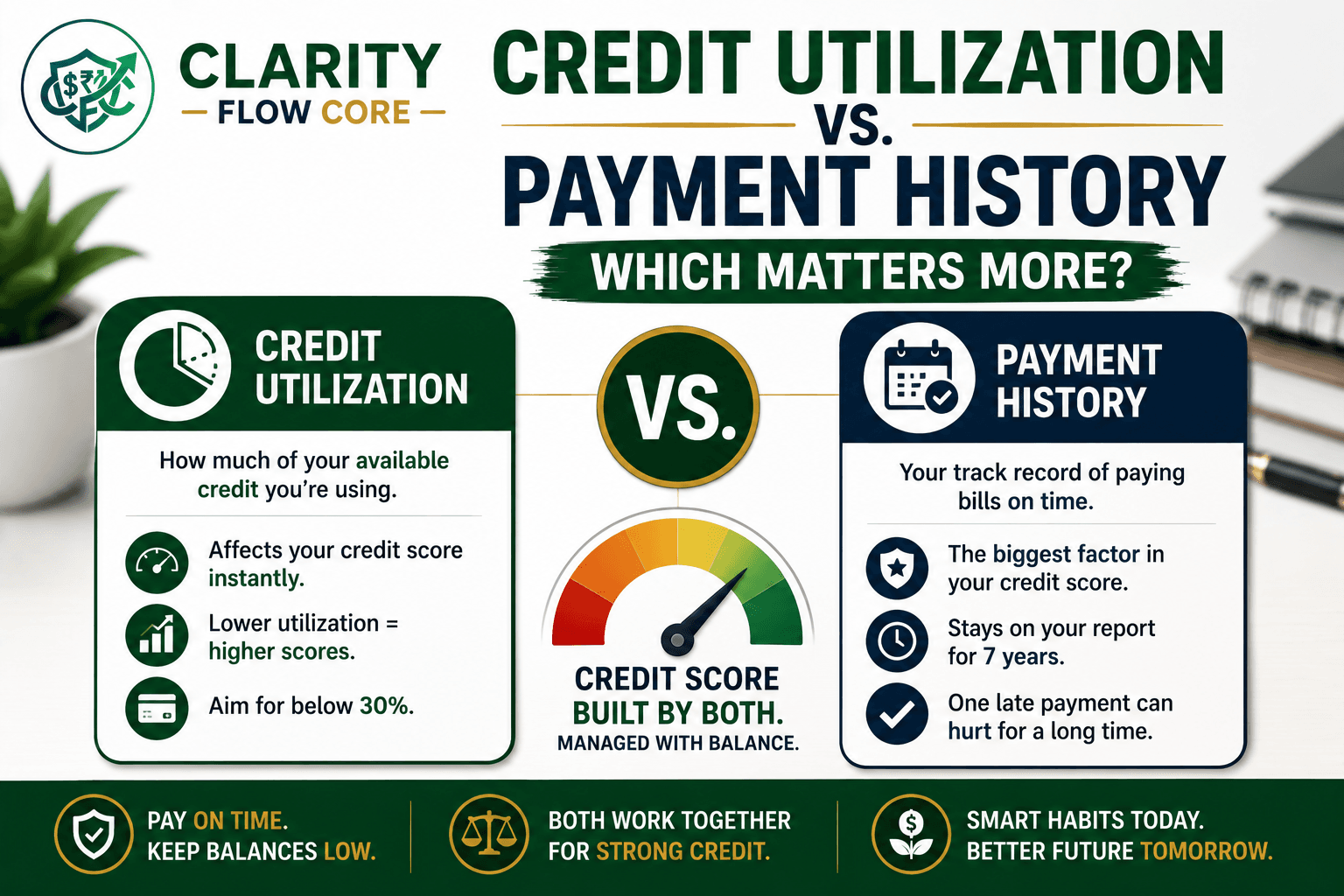

Credit Utilization vs Payment History: Which Matters More?

If you are trying to figure out the exact difference between credit utilization vs payment history, you are definitely not alone.

Picture this: You check your banking app on a Tuesday morning. You see your credit score has randomly dropped by 20 points. Your stomach sinks. You haven’t missed a payment in years. You haven’t opened any new credit cards. You are doing everything “right,” but the credit bureaus are still punishing you.

On the flip side, maybe you are actively trying to rebuild your credit right now. You are throwing extra money at your balances, but that three-digit number refuses to budge.

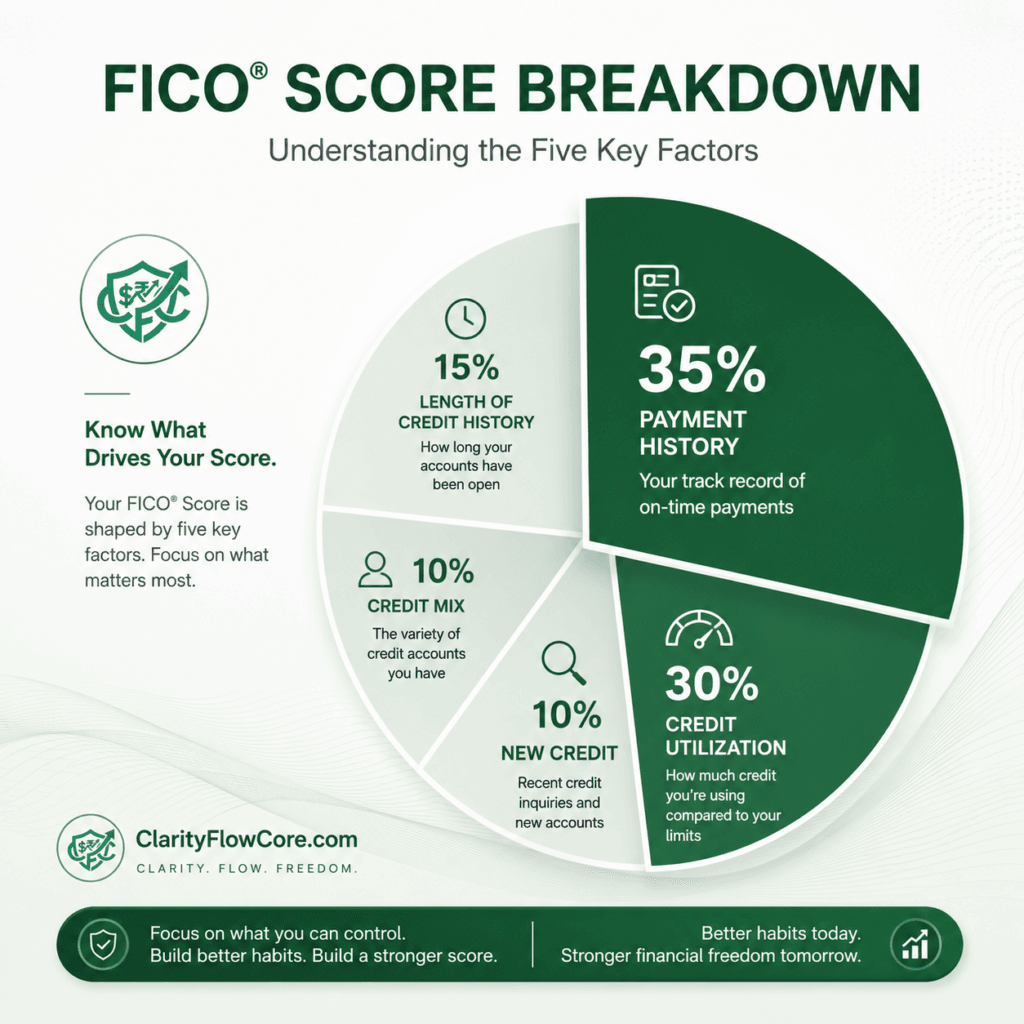

Understanding your credit score can feel like trying to play a board game where the bank keeps changing the rules. But the truth is, your FICO score is just a math equation. And the two biggest, heaviest parts of that equation are your payment history and your credit utilization.

Let’s break down exactly how these two heavyweight metrics work, which one actually matters more, and how you can stop guessing and start taking control of your financial reputation.

The Quick Answer

If you are just looking for the fast, bottom-line difference to understand your credit profile today, here is the visual breakdown of how these two metrics compare:

| Factor | Payment History | Credit Utilization |

| FICO Weight | 35% | 30% |

| Impact Speed | Slow | Fast |

| Recovery Speed | Slow | Fast |

| Can Change Monthly? | No | Yes |

| Most Important? | ✅ Yes | Important |

The Real Problem: Why Credit Feels Like a Rigged Game

When people struggle to grow their credit scores, it usually comes down to a fundamental misunderstanding of what credit bureaus actually care about.

We tend to look at credit cards through an emotional lens. We feel proud when we pay off a big chunk of debt, and we feel guilty when we swipe for a luxury purchase.

The credit bureaus do not care about your feelings, and they don’t care what you bought. They only care about risk. Your credit score is simply a “risk grade” that tells future lenders how likely you are to pay them back.

To determine that risk, they look closely at your past behavior (Payment History) and your current reliance on borrowed money (Credit Utilization).

Deep Dive: Payment History (The Dealbreaker)

Payment history makes up 35% of your FICO score. It is the absolute foundation of your credit profile. If you borrow money, do you pay it back when you promised to? It is a simple “yes” or “no” question for the bank.

Why It Carries So Much Weight

If you were going to loan $500 to a friend, the very first thing you would ask yourself is, “Have they paid me back when they promised to in the past?” Banks ask the exact same question. If you have a history of paying your bills late, you are statistically a much higher risk for defaulting on a loan.

The Real Consequences

A late payment is a massive blow to your credit score. But there is a very important technicality here: A payment is not reported to the credit bureaus as “late” until it is a full 30 days past the due date. If your bill was due on the 1st, and you paid it on the 12th, you will get hit with a highly annoying $35 late fee from your credit card company. But it will not show up on your credit report.

However, if you cross that 30-day threshold, the damage is severe. A single 30-day late payment can significantly reduce an excellent credit score, sometimes by dozens of points or more depending on the overall credit profile. And worse, that mark stays on your credit report for seven years.

🔮 Want to Test a Scenario?

Wondering exactly how many points a single 30-day late payment will knock off your FICO score? Or how much you’ll gain by paying down a specific credit card? Run your numbers through our free Credit Score Simulator to see the exact mathematical impact before it happens.

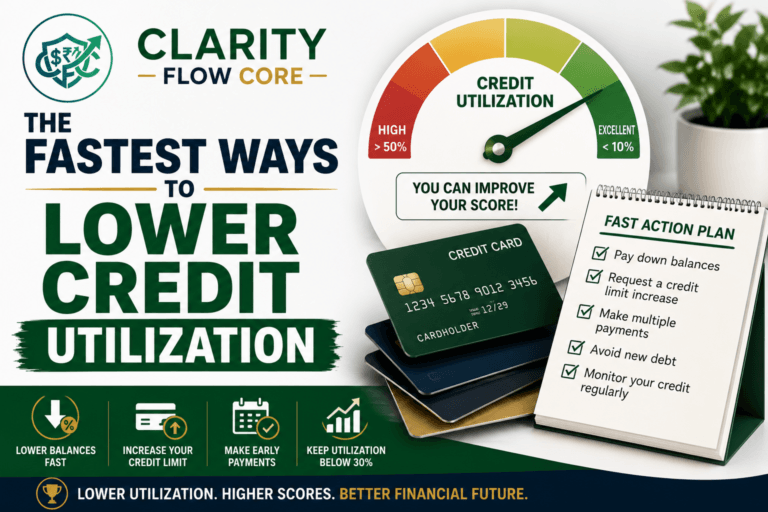

Deep Dive: Credit Utilization (The Wildcard)

Credit utilization makes up 30% of your FICO score. If payment history is the foundation, credit utilization is the steering wheel. It is the factor that makes your score jump up and down from month to month.

What It Actually Means

Credit utilization is simply a ratio. It is the amount of credit you are currently using divided by the total amount of credit you have available.

If you’re new to this concept, What Is Credit Utilization — And Why Does It Matter? explains exactly how credit utilization is calculated, why lenders pay close attention to it, and how it influences your overall credit profile.

Let’s do some simple math. If you have a single credit card with a $5,000 limit, and your current balance is $1,000, your credit utilization is 20%.

Why It Causes So Much Anxiety

Utilization causes immense stress because it fluctuates constantly. Credit card companies report your balance to the credit bureaus once a month—usually on your statement closing date (not your due date).

If you use your credit card to buy a $2,000 couch on Tuesday, and your statement closes on Wednesday, your credit report is going to show a massive spike in utilization, even if you planned to pay off the couch entirely on Friday. This is why you sometimes see your score drop even when you are a responsible spender.

The Showdown: Which Matters More?

Which Matters More?

If you must choose one, payment history matters more because it represents 35% of your FICO score and late payments can damage your credit for years. However, credit utilization is usually the fastest factor to improve because it updates every month. The best strategy is to protect your payment history first and optimize utilization second.

Think of it like building a house. Payment history is the concrete foundation. If the foundation is cracked (you have a history of missed payments), it takes a very long time to repair. You just have to wait it out and stack up years of on-time payments to bury the old mistakes.

Credit utilization is the paint on the walls. If you don’t like the color (your utilization is too high and dragging your score down), you can literally paint over it this weekend. Because utilization has no “memory,” the second you pay down your balances and the credit card company reports the new, lower number, your score will bounce right back.

Example Scenarios

To make this advice concrete, let’s look at how these two factors play out in the real world.

Example 1: The Maximizer

Sarah is incredibly responsible with her money. She pays her credit card bill in full every single month. However, she only has one credit card with a $2,000 limit, and she puts all her monthly living expenses ($1,800) on it to earn cash-back points.

- The Result: Even though Sarah’s payment history is perfect, her credit utilization is 90%. When the bureaus see she is maxing out her card, they view her as a high risk. Her credit score stays artificially low, sitting around 650, simply because of her high utilization.

Example 2: The Forgetful Payer

Mark makes great money and has $30,000 in available credit limits. He rarely uses his cards, keeping his total balances around $500 (a fantastic 1.6% utilization rate). However, Mark is completely disorganized. He forgot to pay a $25 minimum payment on a store credit card for two months in a row.

- The Result: Mark’s utilization is basically perfect, but that 60-day late payment acts as a wrecking ball. His score plummets. Even if he pays off the $500 today, that late mark will haunt his score for years.

Common Mistakes Beginners Make

Before we jump into the action plan, make sure you aren’t falling for these classic credit myths.

- Carrying a balance to “build credit.” This is the single most toxic myth in personal finance. You do absolutely not need to carry a balance and pay interest to build your credit score. Paying your balance in full every month shows perfect payment history and keeps utilization low.

- Closing old credit cards. If you finally pay off a credit card you used to struggle with, your first instinct is to close the account so you can’t use it again. But doing this wipes out that available credit limit. If your limit drops, but your other balances stay the same, your overall credit utilization percentage shoots up, which hurts your score.

- Waiting until the due date to pay. Your credit card company reports your balance to the bureaus on your statement closing date, which is usually about 21 days before your actual due date. If you wait until the due date to pay, a high balance has already been reported.

🎯 Ready to Optimize Your Score?

Are you trying to aggressively lower your balances but aren’t sure where to start? Stop guessing. Plug your current balances and total limits into our free Credit Utilization Recovery System to calculate exactly how much you need to pay down to hit your target credit tier this month.

Your Beginner-Friendly Action Plan

Ready to stop stressing and start optimizing your score? Here are the practical, real-world steps you can take this week.

Step 1: Bulletproof Your Payment History

Human memory is flawed. Do not rely on sticky notes or mental reminders to pay your bills. Log into every single credit card and loan account you have and set up Autopay for the minimum due. You can always log in later and manually pay the full statement balance, but having that minimum payment on autopilot guarantees you will never accidentally suffer a 30-day late mark.

Step 2: Track Down Your Statement Dates

Find out exactly what day of the month your credit card companies report to the bureaus. You can find this by looking at your latest PDF statement and finding the “Statement Closing Date.”

Step 3: Use the “Micro-Payment” Strategy

If you struggle with high utilization like Sarah from our example above, don’t wait until the end of the month to pay your bill. Log into your app every Friday and pay off whatever you spent that week. By keeping the balance artificially low throughout the month, you guarantee that a low number is reported on your statement closing date.

If you’re rebuilding your credit and don’t yet qualify for a traditional credit card, Best Secured Credit Cards for Beginners in 2026 compares beginner-friendly secured cards that report to all three credit bureaus and help strengthen both your payment history and credit utilization over time.

Frequently Asked Questions (FAQs)

Which should I focus on first if my score is low?

Always focus on protecting your payment history first. Missing a payment can cause long-lasting damage to your credit profile. Once all payments are current, lowering credit utilization is often the fastest way to improve your score.

What is a good credit utilization ratio?

General financial advice says to keep your credit utilization below 30%. However, if you are actively trying to optimize your score to buy a house or get a car loan, you should aim to keep your overall utilization below 10%.

How long does a late payment stay on my credit report?

A payment that is 30 days or more late will remain on your credit report for 7 years. However, the impact of that late payment fades over time. A late payment from four years ago will hurt your score significantly less than a late payment from last month.

Does a 0% utilization rate give me a perfect score?

Surprisingly, no. Credit bureaus like to see that you know how to use credit responsibly. If you have absolutely zero utilization across all your cards for months at a time, it looks like you aren’t using credit at all. Having a tiny balance report (like 1% to 3%) and then paying it off in full is actually better than 0%.

Final Thoughts

At the end of the day, comparing credit utilization vs payment history is like comparing the engine of a car to its steering wheel. You absolutely need both if you want to get where you are going.

Clarity Flow Core is built on the belief that financial health should not be a mystery. Your credit score is not a reflection of your worth as a person; it is just a reflection of your current financial habits.

If you have made mistakes in the past and have late payments dragging you down, give yourself some grace. You cannot change the past, but you can automate your payments starting today to ensure it never happens again. Focus on what you can control right now: keep those balances low, pay your bills on time, and watch your financial foundation grow stronger month by month.

Sources & References

The information in this article is based on guidance and educational resources from the following organizations:

- FICO® – What’s in Your FICO® Score?

- FICO® – Payment History and Credit Scores

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores

- Consumer Financial Protection Bureau (CFPB) – What Is a Credit Score?

- Consumer Financial Protection Bureau (CFPB) – What Is a Credit Report?

- AnnualCreditReport.com – Official website for obtaining free credit reports authorized by U.S. federal law.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.