How Much Debt Is Too Much? A Simple Debt-to-Income Ratio Guide

If you are reading this, you probably recently sat down at your kitchen table with a notebook, a calculator, and a rising sense of panic. You pulled up your credit card statements, your car loan, and your student loans, and you added them all together. Staring at that final, massive number can make the air leave your lungs.

When you are looking at a balance that rivals the cost of a luxury car, the first question that pops into your head is usually terrified: how much debt is too much? You start wondering if you are normal. You wonder if you are dangerously behind your peers. You wonder if any bank will ever trust you enough to let you buy a home, or if you are destined to be trapped in the renting cycle forever.

The finance industry does a terrible job of explaining this. They put out scary articles claiming the average American owes tens of thousands of dollars, but they rarely explain what that actually means for your specific life.

Here is the most comforting truth you will read today: your total debt balance is not what actually matters. Banks do not look at your total debt and instantly stamp “DENIED” on your file. Instead, they look at your numbers through a very specific mathematical lens called the Debt-to-Income Ratio (DTI).

If you want to know if your debt is out of control, or if you are perfectly positioned to buy a house next year, you have to stop looking at the raw balance and start looking at the ratio. Let’s break down this simple debt-to-income ratio guide, explore the hidden mistakes beginners make when calculating it, and map out exactly how to fix your numbers before you apply for your next loan.

The Real Problem: Why the Raw Debt Number Lies to You

When we feel financial anxiety, we tend to focus on the overall size of the mountain. We think, “I have $40,000 in debt, my financial life is ruined.”

But let’s look at how a bank views that exact same $40,000.

Imagine two different people, Person A and Person B. Both of them owe exactly $40,000 in a mix of credit cards and auto loans. Their minimum monthly payments add up to $1,000 a month.

- Person A works as a retail manager making $3,000 a month before taxes. That $1,000 debt payment eats up an enormous 33% of their entire gross paycheck. By the time they pay rent and buy groceries, they have zero margin for error. They are highly stressed and financially drowning.

- Person B works as a software engineer making $10,000 a month before taxes. That exact same $1,000 debt payment only takes up 10% of their gross income. They barely even notice it leaving their checking account.

Even though their total debt is completely identical, Person A has “too much debt,” while Person B is considered an incredibly safe borrower.

This is why comparing your total balance to your friends or to national averages is a complete waste of your emotional energy. The only thing that determines if you have “too much” debt is how much of your current paycheck is required to keep it afloat.

What Is Your Debt-to-Income Ratio (DTI)?

Your Debt-to-Income (DTI) ratio is simply a percentage that shows how much of your monthly income goes toward paying mandatory debt obligations. It is the ultimate measure of your financial breathing room.

When you apply for a mortgage, a car loan, or a personal loan, the underwriter uses this exact percentage to decide if giving you more money is a safe bet or a guaranteed disaster.

How to Calculate Your DTI:

You do not need to be a math genius to figure this out. It is a very simple division problem.

- Add up all your monthly debt payments. (This includes your rent/mortgage, auto loans, minimum credit card payments, student loans, and personal loans). Let’s say this equals $1,500.

- Find your Gross Monthly Income. This is the amount of money you make before taxes, health insurance, and retirement contributions are taken out. Let’s say you make $5,000 a month gross.

- Divide your debt by your income. ($1,500 ÷ $5,000 = 0.30).

- Multiply by 100. Your DTI is 30%.

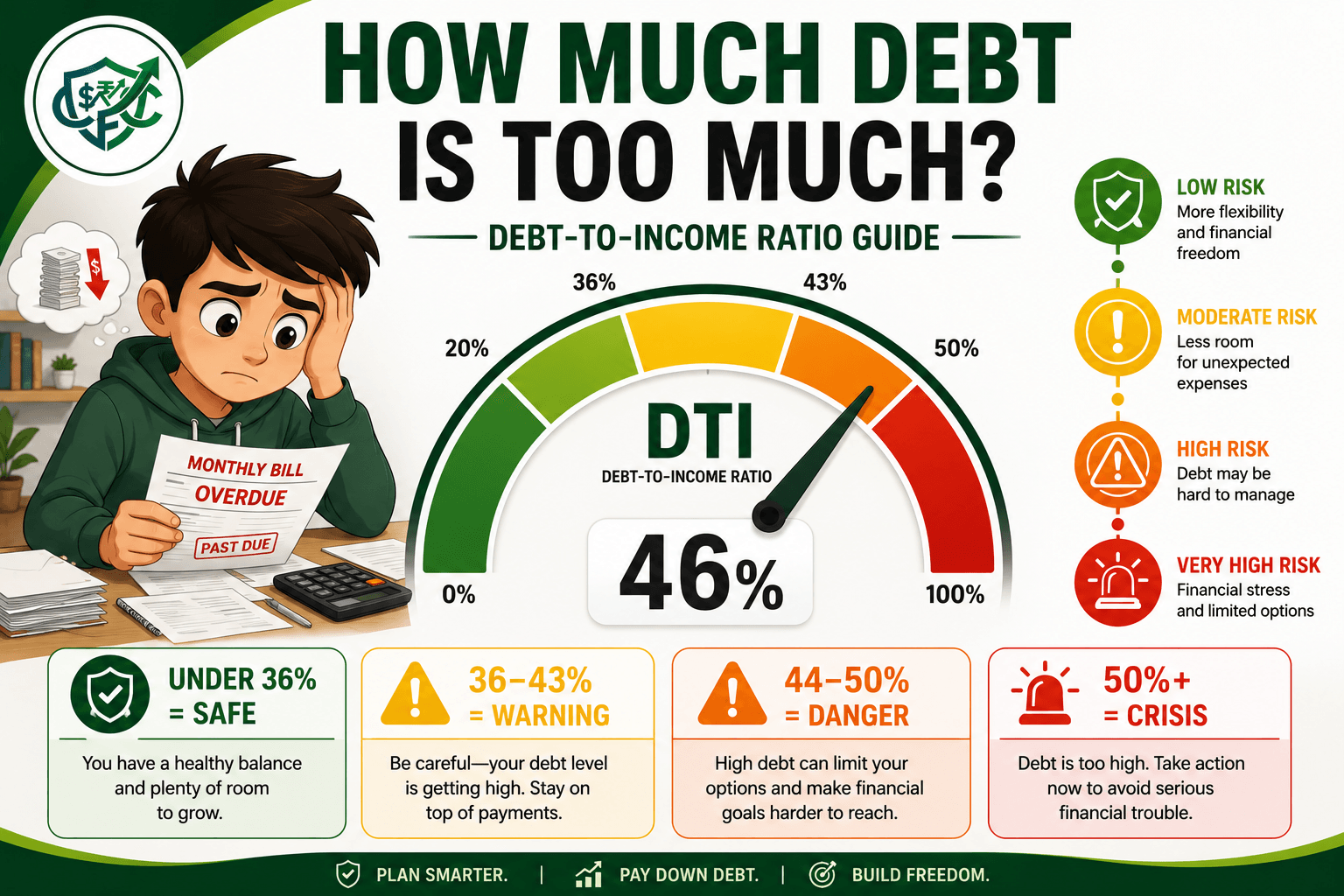

Quick DTI Risk Level Reference

Here is a fast breakdown of exactly how lenders categorize your results once you have your number:

| DTI Ratio | Risk Level |

| Under 36% | Excellent |

| 36% – 43% | Acceptable |

| 44% – 50% | High Risk |

| Over 50% | Severe Risk |

So, How Much Debt Is Too Much? (The Official Benchmarks)

Lenders generally divide your DTI into the four distinct zones shown above. Knowing exactly which zone you fall into will tell you immediately whether you need to panic, or whether you can relax and proceed with your financial plans.

The Safe Zone (Under 36%)

If your DTI is under 36%, you are in an excellent position. Most traditional banks consider this the ideal sweet spot. It means you have plenty of leftover income every month to handle emergencies, invest for the future, and absorb the shock of an unexpected expense. If your credit score is solid, you will have no problem getting approved for the absolute best interest rates on a home or car.

The Warning Zone (36% to 43%)

This is where the vast majority of normal, hardworking Americans live. You are managing your bills, but things might feel slightly tight at the end of the month.

The number 43% is incredibly important. In the mortgage industry, 43% is widely considered the absolute maximum DTI ratio you can have and still qualify for a “Qualified Mortgage” (the safest, most heavily regulated type of home loan). If your ratio creeps above 43%, conventional lenders will start turning you away, and you will have to rely on government-backed loans or higher-interest alternatives.

The Danger Zone (44% to 50%)

If nearly half of your pre-tax income is legally required to be paid to a bank every month, you are officially walking on thin ice. When you factor in taxes, groceries, gas, and utilities, you likely have almost zero cash left over. If you fall into this zone, you probably feel like you can only afford the minimum payments, and one minor medical bill could send you spiraling. Lenders will view you as extremely high risk, and your chances of getting approved for a new loan are very slim.

The Crisis Zone (Over 50%)

When looking at how much debt is too much, crossing the 50% threshold is the ultimate red siren. You are technically insolvent on a monthly basis. You are likely relying on credit cards just to buy groceries because your actual cash is entirely consumed by debt payments. If you are in this zone, taking on any new debt is a terrible idea. Your singular focus must be on aggressively lowering this ratio through balance transfers, non-profit credit counseling, or drastic lifestyle changes.

4 Brutal Beginner Mistakes When Calculating DTI

When people try to figure out their own ratios before going to a bank, they often use the wrong numbers and end up terrifying themselves unnecessarily. If you want an accurate picture, avoid these four common mistakes:

1. Using Your “Take-Home” Pay Instead of Gross Pay

This is the number one mistake beginners make. When you look at your paycheck, you see the money that actually hits your checking account (your net pay). But lenders do not use that number. They use your Gross Pay—the large number at the top of your pay stub before the government takes its share. Because your gross pay is much higher than your take-home pay, using it actually makes your DTI look significantly better.

2. Including Living Expenses as “Debt”

Your DTI is specifically about money you have borrowed. When adding up your monthly debts, do not include your cell phone bill, car insurance, Netflix subscription, electricity, or grocery budget. None of those are debts. The only non-borrowed item you must include in your DTI calculation is your monthly rent payment (or your future estimated mortgage payment).

3. Counting Your Total Balance Instead of Minimum Payments

If you have a $5,000 balance on a credit card, you do not plug $5,000 into the calculator. The algorithm only cares about your required cash flow. You only enter the minimum monthly payment due (for example, $150). The bank just wants to know the baseline amount of cash required to keep your accounts from defaulting.

4. Forgetting the “Future Housing” Swap

If you are calculating your DTI to see if you can buy a house, you have to do a specific mental swap. You must remove your current monthly rent from the calculation, and add in the total estimated monthly cost of your future mortgage (including property taxes, insurance, and HOA fees). If you are paying $1,500 in rent now, but the house you want will cost $2,500 a month, your DTI is going to jump significantly the moment you close on the house.

The Real Consequences of a High DTI

We often talk about the emotional weight of debt, but a high DTI has severe, practical consequences that can completely derail your life plans.

If your DTI is hovering around 48%, even if you have never missed a credit card payment in your entire life, the banking system will lock you out.

- Mortgage Denials: You can spend years saving up a beautiful 20% down payment, have a pristine 780 credit score, and still be flat-out denied for a mortgage because your DTI is too high.

- Vulnerability to Emergencies: A high DTI means you have poor cash flow. When your cash flow is tight, you cannot properly fund your safety net. If a tire blows out on your car, you have no choice but to put it on a credit card, which increases your minimum payments, pushing your DTI even higher. It is a suffocating, self-feeding loop.

- Higher Interest Rates: If a lender is willing to overlook a borderline DTI (say, 45%), they are going to charge you for that risk. You will be hit with much higher interest rates on personal loans and auto loans, meaning the exact same car will cost you thousands of dollars more than it would cost someone with a 30% DTI.

The Beginner-Friendly Action Plan: How to Lower Your DTI

If you just ran the math in your head and realized you are sitting in the Danger Zone, take a deep breath. A high DTI is not a permanent tattoo. Because it is a ratio made of two shifting numbers (Debt and Income), you have multiple ways to attack it and bring it down safely.

Step 1: Face the exact math.

Do not guess. Do not estimate. Get your exact ratio down to the decimal point so you know your starting line. (See the tool below to do this instantly).

Step 2: Attack the smallest monthly payment first (The Top of the Fraction).

To lower your DTI, you need to eliminate minimum payments. Look at all your debts. Which one has the lowest total balance? Maybe it is a small retail store card with a $400 balance and a $35 minimum payment. Throw every extra dollar you have at that card until the balance is $0. The moment that card is paid off, you have eliminated a $35 monthly obligation, which instantly improves your DTI.

When Will You Finally Be Debt-Free?

Stop wasting money on high interest rates. Compare the Debt Avalanche and Debt Snowball methods to build a custom payoff plan and find your fastest path to zero debt.

Build My Payoff StrategyStep 3: Artificially lower the minimums through consolidation.

If your credit score is still strong, look into a personal consolidation loan. If you can combine four different credit cards (with minimum payments totaling $400) into one personal loan with a fixed payment of $250, you just legally wiped $150 off your monthly debt burden without actually paying off the balance yet. Your DTI drops immediately.

Step 4: Increase your gross income (The Bottom of the Fraction).

If you cannot lower the debt fast enough, you have to raise the income. This is where learning to budget as a freelancer or taking on a temporary side hustle becomes incredibly powerful. If you can add just $1,000 a month in gross income by driving for a ride-share app or doing freelance work on the weekends, the denominator of your ratio gets much larger, instantly making your debt look much smaller to the bank.

⚖️ Calculate Your Debt-to-Income Ratio in Seconds

Stop guessing. Enter your income and monthly debt payments to instantly see where you fall on the DTI scale and whether lenders are likely to approve you.

Frequently Asked Questions (FAQs)

Is 40% debt-to-income ratio bad?

Not necessarily. A 40% DTI is within the range many mortgage lenders accept, but it may limit your borrowing options and increase lender scrutiny. You will likely qualify for a loan, but you might not receive the absolute lowest interest rate available on the market.

What is the ideal debt-to-income ratio?

Most financial experts recommend keeping your DTI below 36%, while many mortgage lenders prefer ratios below 43%. Staying below 36% ensures you have enough breathing room to comfortably save for retirement and handle unexpected financial emergencies.

Can increasing my income improve my DTI?

Yes. Since DTI is a ratio, increasing your gross monthly income can lower your DTI even if your debt payments stay exactly the same. Taking on a side hustle or earning a raise makes the “income” half of the equation larger, which instantly drops your overall percentage.

Does my credit score affect my Debt-to-Income ratio?

No, they are completely separate systems. Your credit score measures your reliability (do you pay your bills on time). Your DTI measures your capacity (do you actually have enough money to pay another bill). You can have a perfect 800 credit score and a terrible 55% DTI. You need both numbers to be healthy to get a mortgage.

Do student loans ruin my DTI?

They definitely impact it, but the government and conventional lenders have created special rules to make it easier for people with student loans to buy homes. For example, if your student loans are in deferment or an income-driven repayment plan, lenders will often use a small fractional percentage of the total balance (like 0.5% or 1%) as the assumed monthly payment rather than letting the massive total balance destroy your DTI.

Does my spouse’s debt count toward my DTI?

If you are applying for a loan or a mortgage by yourself, only your income and your debts are calculated. However, if you apply jointly with your spouse to use their income to qualify for a larger house, the lender will combine both of your incomes and both of your debts to create one joint DTI ratio.

Final Thoughts: Your Debt Does Not Define You

When you realize that your debt is officially “too high,” the natural human reaction is shame. You replay all the mistakes you made in your head. You kick yourself for swiping that credit card, for buying a car that was slightly out of your budget, or for taking out those loans when you were eighteen.

Please drop the shame right now. The modern financial system is a minefield, and almost everyone steps on a mine at some point in their twenties or thirties.

Your debt-to-income ratio is simply a gauge on the dashboard of your car. If the engine temperature gauge flashes red, you don’t sit in the driver’s seat crying about what a terrible person you are; you pull over, let the engine cool down, and fix the problem.

Treat your DTI exactly the same way. If you are sitting at 48% today, the bank is just telling you to pull over. Pause the applications. Do not try to figure out what happens after mortgage pre-approval yet. Put your head down, attack your smallest minimum payments, pick up some extra income, and watch that percentage slowly drop back into the safe zone. You have plenty of time to get your numbers right, and you absolutely have the power to fix this.

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Learn how lenders evaluate mortgage applications, including debt-to-income (DTI) ratios, monthly housing costs, and loan affordability.

- Fannie Mae – HomeView® Homebuyer Education – Educational resources explaining debt-to-income ratios, mortgage qualification, budgeting, and preparing for homeownership.

- Federal Housing Administration (FHA) – FHA Loans – Official information about FHA loan eligibility, debt-to-income requirements, and borrower qualification guidelines.

- Consumer Financial Protection Bureau (CFPB) – Managing Debt – Practical guidance on reducing debt, improving financial stability, and understanding repayment options.

- National Foundation for Credit Counseling (NFCC) – Access nonprofit credit counseling services, debt management resources, and personalized budgeting assistance.

- Federal Trade Commission (FTC) – Credit, Loans, and Debt – Consumer education covering borrowing, debt management, and responsible credit decisions.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.