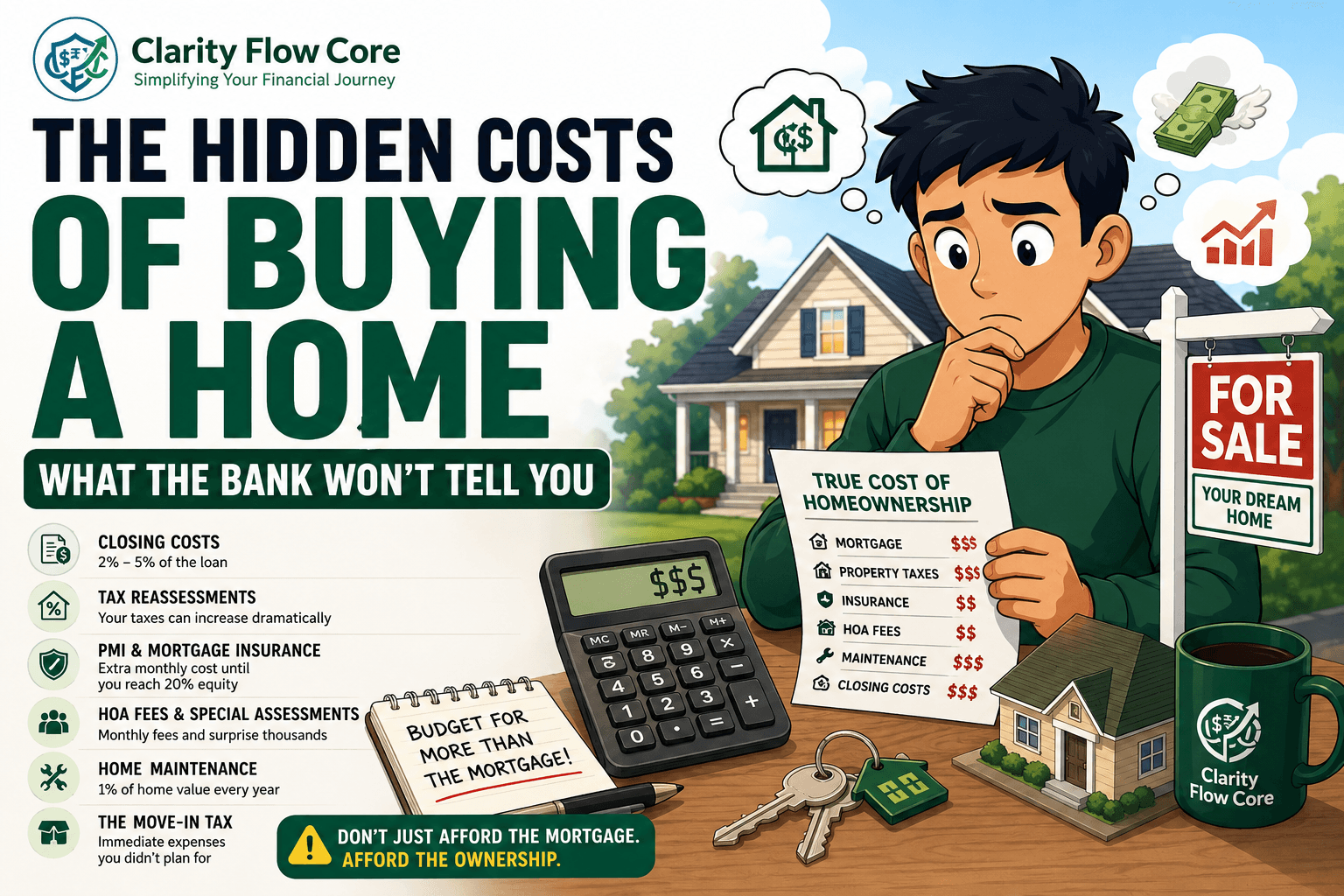

The Hidden Costs of Buying a Home: What the Bank Won’t Tell You

You saved the down payment, you got the pre-approval letter, and you finally found a house you love. You run the estimated mortgage payment through an online tool like our Debt-to-Income (DTI) Analyzer & Loan Readiness Planner, smile, and think, “I can afford this.”

⚡ Quick Answer

The mortgage payment is just the baseline. The true hidden costs of buying a home include upfront closing costs (2% to 5% of the loan), brutal property tax reassessments, Private Mortgage Insurance (PMI), mandatory HOA fees, and the relentless 1% annual maintenance rule. Failing to budget for these silent expenses is the number one reason first-time buyers become “house poor.”

The most dangerous lie in real estate is that your monthly mortgage payment is the only number that matters.

When I bought my first property, I made this exact mistake. I calculated my monthly payment down to the penny and completely drained my savings account to cover the down payment. Within the first 90 days, I was hit with a supplemental tax bill, a broken water heater, and a mandatory fence repair. I was immediately pushed to the financial brink because I was completely blind to the operational realities of property ownership.

A house is a massive, living liability before it ever becomes an asset. If you are preparing to exit the rental market, you cannot rely on Zillow’s basic estimates. You must run the hard operational math. Here is the definitive guide to the hidden costs of buying a home, the exact dollar amounts you need to expect, and the specific traps that bankrupt first-time buyers.

The Upfront Shock: Closing Costs

The first major blow in the hidden costs of buying a home hits you before you even get the keys. Most beginners assume the down payment is the only cash they need to bring to the closing table. It isn’t.

You must also pay “Closing Costs”. This is a blanket term for the massive collection of administrative fees required to legally transfer a property into your name and secure the mortgage.

Closing costs typically run between 2% and 5% of the total loan amount.

If you are buying a $400,000 house, you must prepare to write an entirely separate check for $8,000 to $20,000 just to close the deal. Here is exactly what those fees cover:

| Closing Cost Fee | What It Actually Is | Estimated Cost |

| Loan Origination Fee | What the bank charges you to process the mortgage. | 0.5% to 1% of the loan |

| Appraisal Fee | A third-party assessment to prove the house is actually worth the price. | $400 – $800 |

| Home Inspection | Paying a professional to find everything physically wrong with the house. | $300 – $600 |

| Title Search & Insurance | Guaranteeing no one else legally owns the property or has liens on it. | $1,000 – $2,500 |

| Prepaid Escrow | The bank forcing you to pay 2-6 months of taxes and insurance upfront. | $2,000 – $4,000 |

If you drain your entire cash reserve just to hit your 5% down payment, the bank will deny your loan at the finish line because you lack the liquid cash to cover these administrative fees.

The Stealth Trap: Property Tax Reassessments

This is the most destructive of all the hidden costs of buying a home. It catches almost every single first-time buyer completely off guard.

When you browse real estate apps, the platform usually displays the current owner’s property tax bill. You naturally use that exact number to calculate your future monthly payment.

This is a fatal mathematical error.

The previous owner may have purchased the house 15 years ago for $150,000. Their property taxes are legally capped and based on that old valuation. You are buying the house today for $450,000.

A few months after you close the deal, the local municipal government will run a “Tax Reassessment” based on the new, highly inflated purchase price. Your property taxes will skyrocket to match the new value.

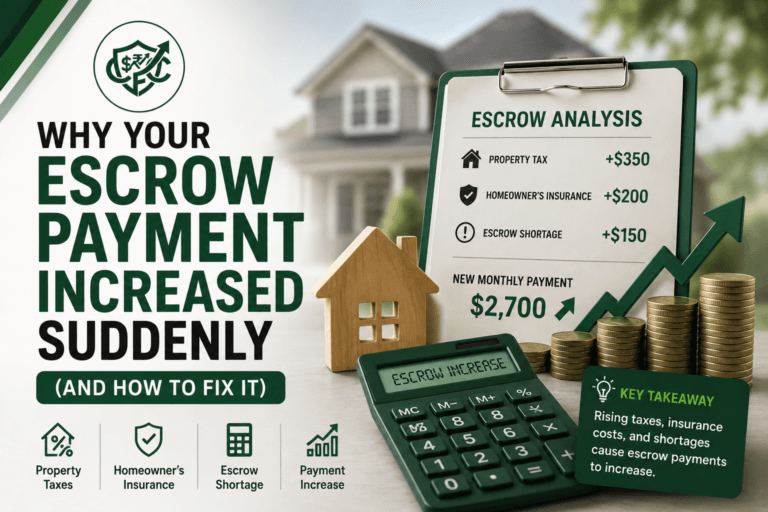

The Escrow Shortage Nightmare

Your mortgage payment is usually made up of four things: Principal, Interest, Taxes, and Insurance (PITI). The bank collects the tax money every month and holds it in an “Escrow Account” to pay the city at the end of the year.

When the city suddenly doubles your tax bill due to the reassessment, your escrow account will fall into a massive negative deficit.

The bank will send you a terrifying letter declaring an “Escrow Shortage.” They will demand that you either write them a massive lump-sum check for $3,000 to cover the shortage immediately, or they will forcefully raise your monthly mortgage payment by $300 to $500 a month to compensate. Your affordable $2,200 mortgage is suddenly a $2,700 mortgage. (If you are currently facing this exact crisis, read our operational guide on Why Your Escrow Payment Increased Suddenly (And How to Fix It) to learn how to fight back).

When calculating the hidden costs of buying a home, never use the previous owner’s tax history. Always calculate your estimated taxes using the local tax rate multiplied by your actual purchase price.

The Low-Down-Payment Penalty: PMI

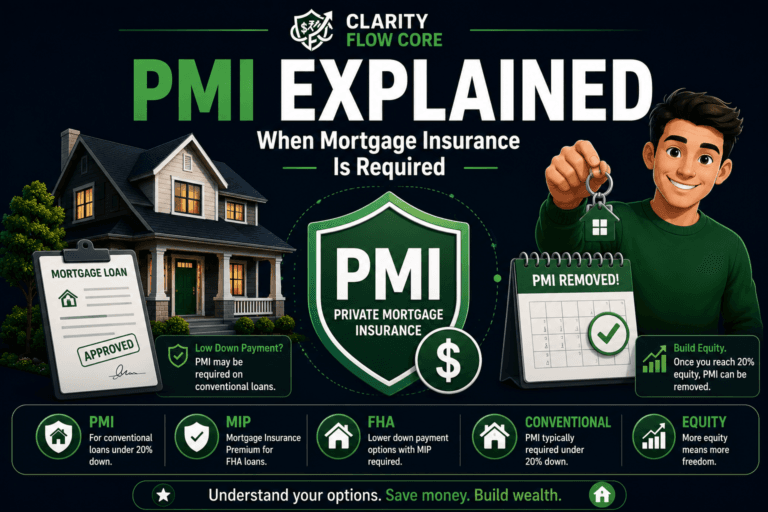

If you do not have a massive 20% down payment (which most first-time buyers do not), you will face one of the most frustrating hidden costs of buying a home: Private Mortgage Insurance (PMI).

If you put down 3.5% or 5%, the bank views you as a high-risk borrower. If you lose your job and stop paying the mortgage, the bank will lose money trying to foreclose and sell the house. To protect themselves, they force you to pay for an insurance policy that protects them.

PMI generally costs between 0.5% and 1.5% of your total loan amount per year.

The Math: On a $350,000 loan, a 1% PMI rate means you are paying an extra $3,500 a year (or roughly $290 every single month).

This $290 does not go toward paying off your house. It does not build equity. It is pure vanished cash. You must factor this monthly bleed into your budget until you eventually build up 20% equity in the property and can legally petition the bank to remove the PMI constraint.

The 1% Maintenance Rule

When you rent an apartment and the refrigerator dies, you call the landlord. It is their problem, and it is their capital. When you own a house, you are the landlord. Every broken pipe, every leaky roof, and every dead HVAC system is a direct hit to your personal checking account.

A critical pillar of understanding the hidden costs of buying a home is budgeting for relentless deterioration. Houses are actively rotting the moment they are built.

Financial planners universally recommend the 1% Maintenance Rule: You must set aside 1% of your home’s total value every single year for repairs and upkeep.

If you buy a $400,000 home, you must expect to spend roughly $4,000 a year (or $333 a month) fixing things.

One year you might spend absolutely nothing. The next year, the central air conditioning condenser blows out in the middle of July, costing you $6,500 to replace. If you do not have this maintenance fund baked into your monthly operational budget, you will be forced to put home repairs on a 24% interest credit card, sparking a dangerous cycle of consumer debt. (If you are already trapped in this cycle, use our Credit Utilization Calculator & Recovery System to build a mathematical way out).

The Immediate “Move-In” Tax

There is a bizarre phenomenon that occurs during the first 30 days of homeownership. I call it the Move-In Tax, and it is one of the most consistently ignored hidden costs of buying a home.

When you walk into your new house, it is completely empty. You suddenly realize you lack the basic infrastructure required to maintain a property. Within the first month, you will inevitably spend thousands of dollars on unglamorous necessities:

- Security: Changing all the exterior locks and deadbolts ($150 – $300).

- Privacy: Buying custom window blinds and curtains for 12 different windows because the previous owners took theirs ($400 – $1,000).

- Lawn Care: Buying a lawnmower, a string trimmer, a rake, and a snow shovel ($500 – $800).

- Basic Fixes: Paint, drywall patch, new toilet seats, and deep cleaning supplies ($300).

If you do not have $2,000 in liquid cash allocated specifically for week one, your first month in the house will be incredibly stressful.

Homeowners Association (HOA) Traps

If you buy a condo, a townhouse, or a single-family home in a modern planned community, you will be forced to join a Homeowners Association (HOA).

The base monthly fee (ranging from $100 to $600 a month) covers community landscaping, snow removal, and neighborhood pool maintenance. While annoying, this monthly fee is usually disclosed upfront.

The true danger in the hidden costs of buying a home lies in the Special Assessment.

If you own a condo and the building needs a new $200,000 roof, but the HOA does not have enough cash in its reserve fund to pay for it, they will issue a Special Assessment. The HOA board will legally mandate that every single unit owner write a one-time check for $5,000 to cover the shortfall. You cannot decline. If you refuse to pay a special assessment, the HOA can legally foreclose on your home.

Before buying into an HOA, you must demand to see their “Reserve Study” to ensure they have hundreds of thousands of dollars in cash saved up for inevitable structural repairs.

When This Backfires: The “House Poor” Trap

Understanding the hidden costs of buying a home is not meant to scare you away from real estate; it is meant to keep you out of the “House Poor” trap. Here is exactly when and why ignoring these costs backfires aggressively on first-time buyers:

1. Maxing Out Consumer Debt

You use every penny of your cash for the down payment and closing costs. Two months later, a pipe bursts in the kitchen. Because you have zero cash reserves, you put the $3,000 plumbing bill on a credit card. Because your mortgage is eating 50% of your income, you can only afford to make the minimum payment on that credit card. You are now trapped in a high-interest debt spiral.

2. Deferred Maintenance Rot

If you cannot afford the 1% maintenance rule, you will start deferring repairs. You notice a small leak in the roof, but you don’t have the $800 to fix it. You ignore it for two years. That small leak slowly rots the wooden trusses and causes black mold in the attic insulation. When you go to sell the house, the buyer’s inspector finds it, and you are forced to pay $15,000 for a massive structural remediation. Deferring maintenance always multiplies the cost.

3. The Relationship Toll

Financial stress is the leading cause of divorce and relationship fracture. If you and your spouse are constantly arguing because the escrow shortage wiped out your grocery budget, the house is no longer a sanctuary; it is a financial prison.

The Operational Defense Strategy

You can easily survive the hidden costs of buying a home if you build an operational defense strategy before you make an offer.

- Calculate Debt Affordability: Never borrow the absolute maximum the bank approves you for. Ensure your total housing costs (Mortgage + Taxes + Insurance + PMI + HOA) stay below 28% of your gross monthly income. Try running your numbers through our Free Debt-to-Income (DTI) Analyzer & Loan Readiness Planner.

- Build a Separate House Fund: Do not merge your home maintenance money with your standard emergency fund (use the Advanced Emergency Fund Analyzer to make sure your baseline emergency cash is fully funded first). Keep a dedicated High-Yield Savings Account strictly for the 1% maintenance rule and escrow shortages.

- Run the Math on Reassessments: Look up the exact millage (tax rate) for the specific county you are buying in. Multiply that rate by your purchase price. That is your true tax burden. Ignore Zillow’s “tax history” chart entirely.

Frequently Asked Questions (FAQs)

1. Can I roll closing costs into my mortgage?

Sometimes, but it is a mathematical trap. Some lenders will allow you to finance the closing costs, but they will charge you a higher interest rate on the entire loan to compensate. You end up paying thousands of dollars in extra interest over 30 years just to save $10,000 upfront. It is always better to pay closing costs in cash.

2. Does the seller ever pay for the hidden costs?

In a “buyer’s market,” you can negotiate for “Seller Concessions,” where the seller agrees to pay a percentage of your closing costs to help get the deal done. However, in a highly competitive market, asking for seller concessions will often cause the seller to reject your offer immediately.

3. When does PMI finally go away?

If you have a Conventional Loan, PMI automatically drops off when you hit 22% equity in the home (meaning your loan balance drops to 78% of the original purchase price). You can also petition the bank to remove it at 20%. Warning: If you use an FHA loan with a low down payment, the Mortgage Insurance Premium (MIP) usually stays on the loan for the entire 30 years unless you completely refinance the house into a conventional loan.

4. What is a Home Warranty, and does it cover these costs?

A home warranty is a service contract you can buy (usually $500–$800 a year) that claims to repair or replace major appliances and HVAC systems. However, they are notoriously difficult to use. They often require $100 “service call” fees, and the warranty companies frequently use loopholes to deny claims or replace premium appliances with cheap, low-tier models. They are not a replacement for a liquid cash maintenance fund.

The Bottom Line

Buying real estate is one of the greatest wealth-building vehicles on the planet, but it requires cold, emotionless arithmetic.

Do not let a real estate agent pressure you into stretching your budget. Do not let the fear of missing out cause you to ignore the hidden costs of buying a home. Run your property tax reassessment math, pad your cash reserves for the immediate move-in tax, and embrace the 1% maintenance rule. By anticipating the friction, you guarantee that your first home will be a place of absolute peace, rather than a source of daily financial panic.

(Setting a realistic housing budget before you buy is one of the best ways to avoid becoming house poor. Our guide How Much of Your Income Should Go Toward Housing Costs? explains how to determine a sustainable monthly housing budget).

Sources & References

- Consumer Financial Protection Bureau (CFPB) – Owning a Home – Learn about mortgages, closing costs, escrow accounts, and the financial responsibilities of homeownership.

- U.S. Department of Housing and Urban Development (HUD) – Buying a Home – Official guidance for homebuyers, including home inspections, mortgage options, and first-time buyer resources.

- Fannie Mae – HomeView® Homebuyer Education – Free educational resources covering budgeting for homeownership, closing costs, property taxes, and ongoing maintenance expenses.

- Freddie Mac – My Home by Freddie Mac – Practical information on buying a home, mortgage affordability, PMI, homeowners insurance, and preparing for long-term ownership costs.

- Internal Revenue Service (IRS) – Publication 530: Tax Information for Homeowners – Learn about homeowner tax responsibilities, deductible expenses, and other tax considerations related to owning a home.

- Federal Housing Administration (FHA) – FHA Loans – Understand FHA mortgage requirements, mortgage insurance premiums (MIP), and financing options for first-time homebuyers.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be construed as professional financial, legal, or tax advice. Every individual’s financial situation is unique. Please consult with a certified financial planner or tax professional regarding your specific circumstances before making major financial decisions. For more detailed information, please review our full Disclaimer.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.

One Comment

Comments are closed.