How Much Emergency Fund Do You Really Need?

How much emergency fund do you need? If you’ve ever watched your car’s Check Engine light suddenly turn on while your checking account was nearly empty, you’ve probably asked yourself that exact question.

You are driving home from a long day at work, mentally reviewing what you have in the fridge for dinner, when you hear it. A weird, grinding noise coming from the front of your car. A few seconds later, the dreaded Check Engine light clicks on, glowing bright orange on your dashboard.

For a lot of people, a glowing dashboard light is just a frustrating inconvenience. But if your checking account is hovering near zero until Friday, that light is terrifying.

It triggers an immediate, physical stress response. You start doing frantic mental math. How much is a mechanic going to charge? Will my credit card go through? If I put this on the card, how will I pay rent next week?

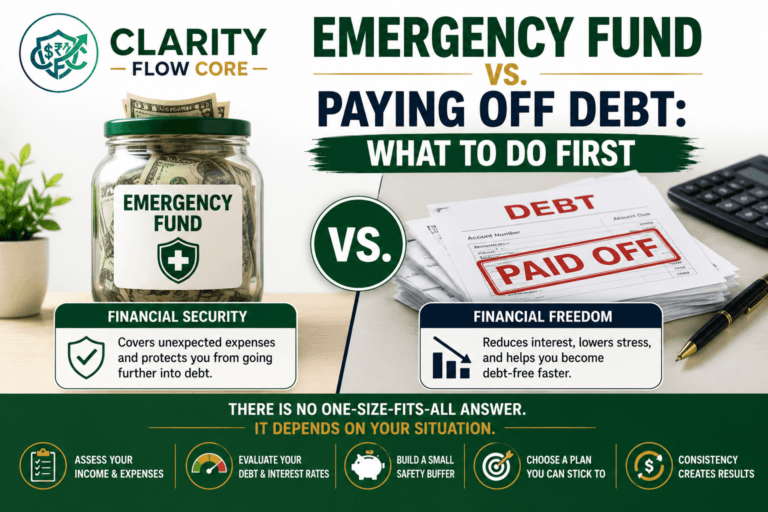

This is the exact moment when you realize why every financial expert on the planet preaches about having an emergency fund. But let’s be brutally honest for a second: the traditional advice surrounding emergency funds is incredibly discouraging.

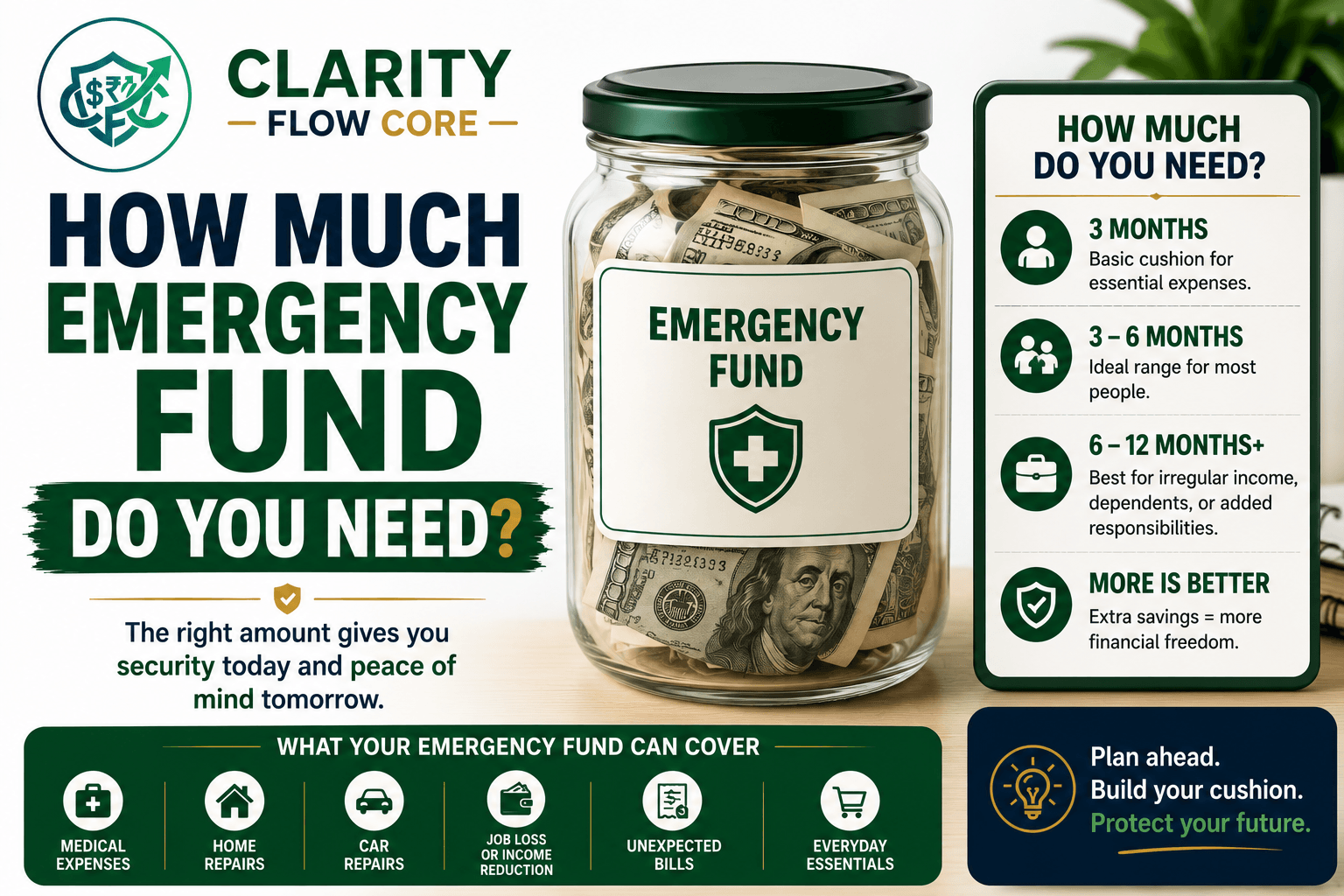

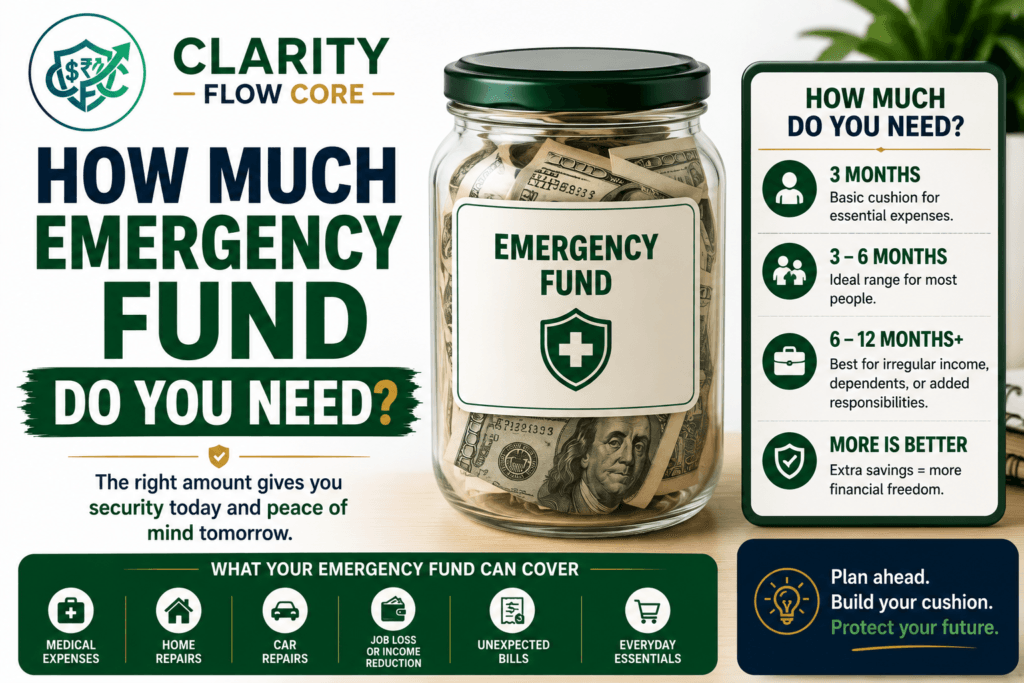

If you do a quick Google search, you will find hundreds of articles telling you to “save three to six months of living expenses.” If your basic expenses are $3,000 a month, these experts are casually telling you to scrape together $9,000 to $18,000 and just let it sit in a bank account.

When you are fighting to pay off student loans, dealing with soaring grocery prices, or trying to manage credit card minimum payments, hearing that you need $10,000 stashed away feels like a bad joke. It feels so impossible that a lot of people just throw their hands up and don’t save anything at all.

Let’s strip away the unrealistic expectations and the textbook finance jargon. If you are wondering exactly how much emergency fund do you need, we are going to break down your personal target number and how to start building your safety net this week—even if you only have $20 to spare.

⚡ Quick Answer

If the traditional “3 to 6 months of expenses” rule feels impossible, start with a Tier 1 Starter Fund of $500 to $1,000. This small cash buffer is enough to cover many common financial emergencies without forcing you to use a credit card. Once that is built, you can slowly work your way up to 1 month of bare-bones living expenses, and eventually, the full 3-to-6 month safety net.

| Situation | Suggested Emergency Fund Goal |

| High-interest debt + tight budget | $500–$1,000 Starter Fund |

| Stable job, renter, no dependents | 3 Months of Expenses |

| Homeowner or single income household | 4–6 Months of Expenses |

| Freelancer or variable income | 6+ Months of Expenses |

| High layoff risk industry | 6+ Months of Expenses |

The Real Problem: The “All or Nothing” Trap

The biggest problem with emergency funds isn’t that people don’t want them. It’s that the goalposts are set so far away that normal people get discouraged before they even begin.

When you are living paycheck to paycheck, or you are a freelancer dealing with fluctuating income, your financial margin of error is razor-thin. Every dollar already has a job. When financial media tells you that your safety net isn’t “complete” until it has five figures in it, it creates an all-or-nothing mindset.

You think, “If I can’t save $10,000, what is the point of saving $50?”

But personal finance is not all-or-nothing. It is a game of incremental progress. An emergency fund is simply a shock absorber between you and the unpredictable nature of life. A small shock absorber is infinitely better than no shock absorber at all.

Why It Happens: The Illusion of “Leftover” Money

Why is it so incredibly hard to build this cash buffer? It usually comes down to a fundamental misunderstanding of how saving actually works in the real world.

Most people try to save money by paying all their bills, buying their groceries, paying for their subscriptions, going out on the weekends, and then promising themselves they will save whatever is “left over” at the end of the month.

Here is the hard truth: There is never anything left over.

Human beings have a psychological tendency called Parkinson’s Law, which states that work expands to fill the time allotted for it. The financial equivalent is that your spending will always expand to consume your available income. If you see $300 sitting in your checking account on a Thursday, your brain subconsciously finds a way to justify spending it by Sunday.

You aren’t failing to save because you are irresponsible. You are failing to save because you are relying on willpower at the end of the month instead of automation at the beginning of the month.

Common Mistakes People Make with Emergency Funds

When people finally decide to get serious about building their cash reserves, they often step into a few predictable traps. Before we look at the right way to build your fund, let’s look at the mistakes you need to avoid.

Mistake 1: Keeping the money in your primary checking account.

If your emergency fund is sitting right next to your debit card balance, it is doomed. You will log into your banking app, see a “healthy” balance of $1,500, and suddenly feel totally fine about ordering a $40 pizza or buying concert tickets. You have to create visual and physical friction between your spending money and your emergency money.

Mistake 2: Confusing a predictable expense with an emergency.

Christmas happens on December 25th every single year. It is not an emergency. Your car registration is due the same month every year. It is not an emergency. A true emergency is unexpected, necessary, and urgent. If you dip into your emergency fund to pay for a friend’s wedding flight because you forgot to budget for it, you are draining your safety net for a predictable life event.

Mistake 3: Trying to save while drowning in high-interest debt.

If you have $5,000 in credit card debt costing you 25% in interest, it makes zero mathematical sense to put $5,000 into a savings account earning 4%. You are losing money every single day. (I Can Only Afford the Minimum Payments — Now What?). You need a small starter fund, but after that, your priority must be killing the high-interest debt before you build the massive 6-month safety net.

The Real Consequences: The Debt Spiral

What actually happens if you just ignore the idea of an emergency fund and rely on your credit cards instead?

It leads directly to the debt spiral. Let’s say your water heater breaks, and it costs $1,200 to replace. Because you have no cash, you put it on a credit card. If you can only afford to pay $50 a month toward that balance, the high interest rate is going to eat you alive.

By the time you finally pay off that $1,200 water heater, it might end up costing you $1,800. And while you are paying it off, something else will break. Your dog will need a trip to the vet. You will get a flat tire.

Without an emergency fund, every single bump in the road becomes a semi-permanent financial burden. You end up making minimum payments on yesterday’s disasters for years into the future. Cash protects your income. Credit cards mortgage your future.

🗺️ Map Your Escape from the Debt Spiral

Trying to build an emergency fund while fighting high-interest debt can feel like a losing battle. Stop guessing what to prioritize. Plug your current cash reserves, monthly expenses, and total debt into our free Financial Freedom Planner to check your overall Financial Health Score and map your exact debt-free date.

How Much Emergency Fund Do You Need?

The right emergency fund size depends on three core factors:

- Income stability

- Number of people depending on your income

- Monthly essential expenses

Someone with a highly stable, salaried job may feel totally comfortable with three months of living expenses stashed away. On the flip side, freelancers, business owners, and homeowners often benefit from six months or more because their income fluctuates and their emergency costs (like a broken furnace) are typically higher.

Practical Solutions: The Tiered Approach to Saving

Let’s drop the overwhelming “six months of expenses” rule for a minute. Instead, we are going to build your emergency fund in three distinct tiers. This gives you clear, realistic milestones to celebrate.

Tier 1: The Starter Fund ($500 to $1,000)

Your first goal is to simply get $500 to $1,000 into a separate savings account as fast as humanly possible.

Why this amount? Because a starter fund of this size can cover many common financial emergencies, such as minor car repairs, urgent care visits, or unexpected travel.

If you have high-interest credit card debt, stop here. (Emergency Fund vs Paying Off Debt: Which Should You Do First?) Build this $1,000 firewall, and then throw every other extra dollar you have at your debt. Once the toxic debt is gone, you can move to Tier 2.

Tier 2: The Baseline Fund (1 Month of Bare-Bones Expenses)

Once your high-interest consumer debt is cleared, it’s time to step up your security. Your goal here is to save exactly one month of your “bare-bones” living expenses.

What does “bare-bones” mean? It does not mean your current lifestyle. It means the absolute minimum amount of money you need to survive for 30 days if you suddenly lost your income.

To calculate this, add up your:

- Housing (Rent or Mortgage)

- Basic utilities (Water, electricity, gas, internet)

- Basic groceries (No restaurants, no takeout)

- Transportation to keep looking for work (Gas or bus pass)

- Minimum payments on debt (To keep your credit intact)

- Essential insurances and medications

If your normal monthly budget is $4,000, your bare-bones budget might only be $2,200. Hitting that $2,200 mark in your savings account is a massive psychological victory. It means you are officially one month ahead of disaster.

If you’re preparing to move into your own place, include this emergency cushion alongside your moving budget—not after you’ve already signed a lease. Our guide How Much Should You Save Before Moving Out on Your Own? explains how much you’ll likely need for deposits, moving expenses, and your first few months of independent living.

Tier 3: The Fully Funded Safety Net (3 to 6 Months)

This is the holy grail. Once you have your one-month baseline, you simply multiply that bare-bones number by 3, 4, 5, or 6.

But how do you know if you need three months or six months? It comes down to how risky your life is.

You probably only need a 3-Month Fund if:

- You are single with no dependents.

- You rent an apartment (no surprise roof repairs).

- You have a highly stable, salaried job in an in-demand field.

- You have two steady incomes in your household, and you could survive on just one if someone lost their job.

You absolutely need a 6-Month Fund if:

- You are a freelancer, contractor, or side-hustler with highly irregular income.

- You own a home (furnaces break, and they are expensive).

- You have children or dependents who rely on your income.

- You work in an unstable industry that is prone to layoffs.

- You have a chronic medical condition that could force you to miss work.

🛡️ Calculate Your Exact Bare-Bones Number

Take the guesswork out of your savings target. Plug your monthly expenses into our free Advanced Emergency Fund Analyzer to instantly calculate your bare-bones baseline and get a personalized 3-to-6 month safety net goal based on your exact life situation.

A Beginner-Friendly Action Plan

You know the tiers. Now, how do you actually get the money into the account? Here is your step-by-step game plan to start building your Tier 1 fund this week.

Step 1: Open a High-Yield Savings Account (HYSA)

Do not keep this money in your normal bank. Go online and open a High-Yield Savings Account. General US banks like Ally, Marcus by Goldman Sachs, Discover, or Capital One offer these accounts for free.

A traditional brick-and-mortar bank usually pays you 0.01% in interest. A HYSA usually pays around 4.00% to 5.00% Annual Percentage Yield (APY). Furthermore, keeping it at a completely different bank creates a delay. If you want to spend that money, it takes 1 to 3 business days to transfer it to your checking account. That delay kills impulse purchases.

If you’re opening your first HYSA, How to Choose Your First High-Yield Savings Account explains how to compare APYs, account fees, FDIC insurance, and other important features before selecting a bank.

Step 2: Automate It (Pay Yourself First)

Remember Parkinson’s Law? To beat it, you have to save your money before you have a chance to see it.

Log into your company’s payroll portal, or set up an automatic transfer with your bank. Set it so that the day your paycheck hits, $25, $50, or $100 moves immediately into your new HYSA. Treat this transfer exactly like your electric bill. It is non-negotiable.

Step 3: Sell Something or Pick Up a Gig

If you want to hit your $1,000 Tier 1 goal quickly, don’t just rely on pinching pennies. Look around your living room. What electronics, old clothes, or furniture can you list on Facebook Marketplace or eBay? Can you drive for a ride-share app or do gig work for exactly three weekends? Earning an extra $500 is often much faster than trying to cut $500 out of a tight grocery budget.

Step 4: Audit the Subscriptions

Look at your bank statement from last month. Cancel every streaming service, app subscription, and membership you haven’t used in 14 days. Take the $40 you just freed up and add it to your automated savings transfer. (Behind on Bills? Which Payments Should You Prioritize First?)

Frequently Asked Questions

Where should I keep my emergency fund?

Most people keep emergency funds in a High-Yield Savings Account (HYSA) because the money remains easily accessible while earning significantly more interest than a traditional checking account. Your emergency fund should generally stay out of the stock market, cryptocurrency, and other investments that can lose value exactly when you need the money most.

What actually counts as an emergency?

Ask yourself three questions before touching the money: Is it unexpected? Is it absolutely necessary? Is it urgent? If your car breaks down and you need it to get to work, that is a “yes” to all three. If a flight to Hawaii goes on sale for 50% off, it is unexpected and urgent, but it is not necessary. That is not an emergency.

Should I stop investing in my 401(k) to build my emergency fund?

If your employer offers a 401(k) match (meaning they give you free money for investing), you should generally try to contribute exactly enough to get that match, because that is a 100% return on your money. Divert everything else toward building your Tier 1 starter fund and paying off high-interest debt.

Does my emergency fund lose value to inflation?

Yes, technically. If inflation is 3% and your bank pays you 0.01%, your money is losing purchasing power. This is exactly why you must use a High-Yield Savings Account. A HYSA paying 4% or 5% helps your cash keep pace with inflation so you aren’t quietly losing money over time.

You Deserve Peace of Mind

Financial stress is exhausting. When you don’t have an emergency fund, you are walking a tightrope without a net. Every unexpected bill feels like a personal attack from the universe, and the constant anxiety can drain the joy right out of your life.

But you have the power to change the narrative.

You do not need $15,000 to start feeling safe. You just need to start. Opening a separate savings account today and transferring $25 into it might not feel like a life-changing event, but it is the first brick in the wall that will eventually protect you and your family.

Don’t let the perfection of a fully-funded six-month safety net stop you from building a scrappy, $500 starter fund. The goal isn’t to be perfect. The goal is to be a little bit more secure today than you were yesterday.

You deserve to sleep soundly at night, knowing that if the car breaks down or the dog gets sick, it will just be an inconvenience, not a catastrophe. Start building your net. You’ve got this.

Research & Financial Guidance

This article draws on guidance from consumer protection agencies, financial education organizations, and banking regulators that publish recommendations on emergency savings, household financial resilience, and safe cash management.

- Consumer Financial Protection Bureau (CFPB) — Managing Your Money

Practical guidance on budgeting, emergency savings, and building long-term financial stability. - FDIC Money Smart — Financial Education Program

Educational resources covering emergency savings, budgeting, banking, and responsible money management. - Federal Deposit Insurance Corporation (FDIC) — Deposit Insurance & Consumer Resources

Information about FDIC-insured bank accounts and protecting your emergency savings. - MyMoney.gov — Saving & Investing

U.S. government financial education resources covering emergency funds, saving strategies, and financial planning. - Investor.gov (U.S. Securities and Exchange Commission) — Saving and Investing

Educational guidance on balancing cash reserves with long-term investing after establishing an adequate emergency fund. - National Foundation for Credit Counseling (NFCC) — Financial Education Resources

Guidance on emergency preparedness, budgeting, debt management, and building stronger financial habits.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.