High-Yield Savings Account vs Traditional Savings Account

If you are currently keeping your hard-earned savings in a standard account at a major national bank, you are likely losing money every single day. While your balance might not physically drop, the purchasing power of that money is being quietly eroded by inflation, all while the bank pays you practically nothing in return.

When deciding where to store your cash, the debate between a high-yield savings account vs traditional savings account is one of the most impactful financial choices you will make. The difference between the two can literally mean thousands of dollars in free, passive income over the course of a decade.

⚡ Quick Answer

The primary difference between a high-yield savings account (HYSA) and a traditional savings account is the interest rate (APY) and physical access. HYSAs are typically offered by online-only banks and pay 10x to 15x more interest than traditional brick-and-mortar banks. You should use a traditional bank for your daily checking and cash deposits, but keep your emergency fund and long-term savings in a high-yield savings account to maximize growth.

Choosing the right account type is not about loyalty to a bank; it is about maximizing your money’s potential while keeping it perfectly safe. In this comprehensive guide, we will break down exactly how both accounts work, the hidden fees to watch out for, and the exact strategy you should use to structure your cash.

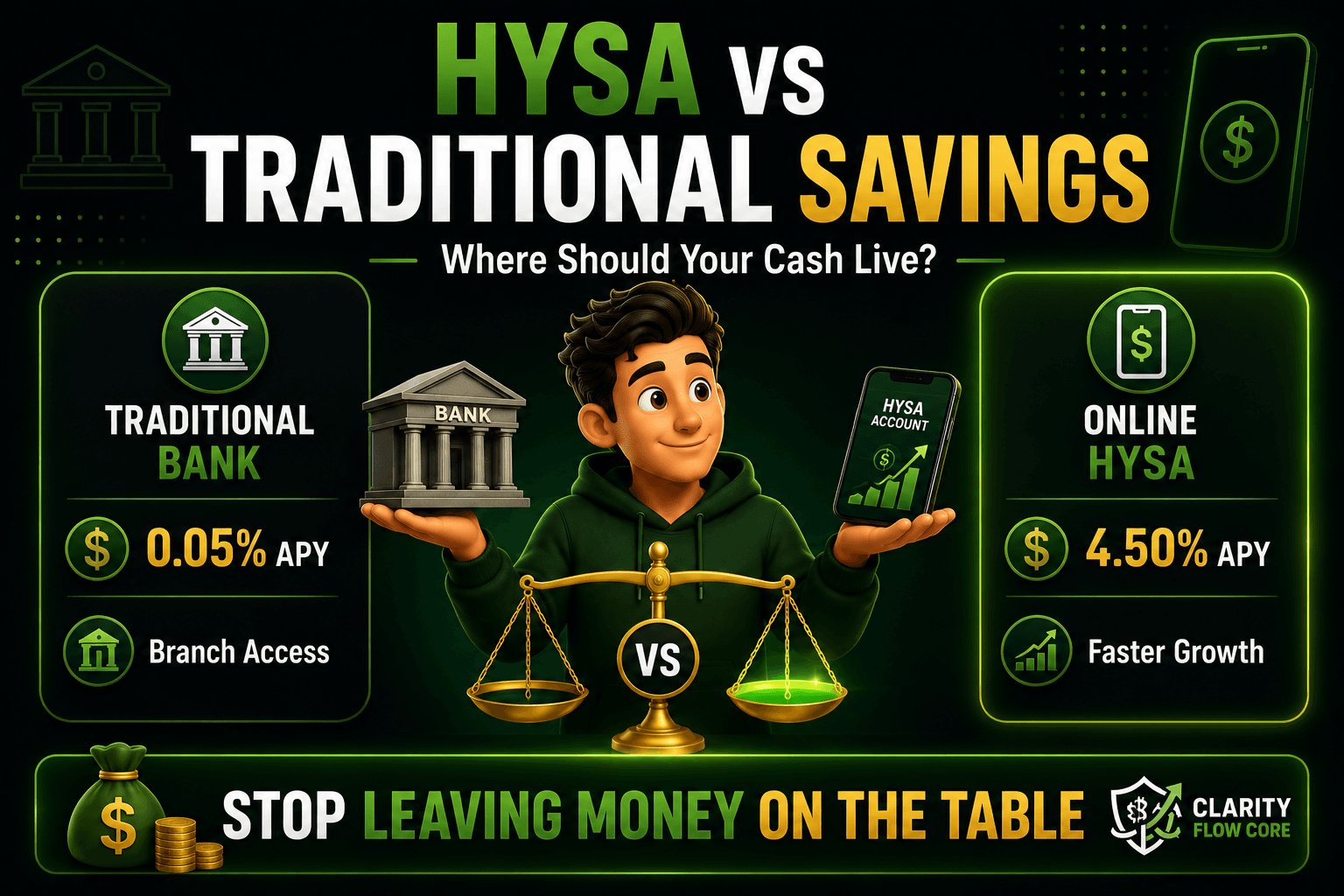

The Core Difference: Visualizing the Numbers

To understand why this choice matters, you have to look at the math. The primary metric used to compare savings accounts is the Annual Percentage Yield (APY), which is the total amount of interest you earn in a year, including compound interest.

Most traditional mega-banks offer an APY hovering around 0.01% to 0.05%. In contrast, online high-yield savings accounts frequently offer APYs between 4.00% and 5.00%.

Here is what happens if you park a $10,000 emergency fund in both accounts for 5 years, assuming you make zero additional contributions:

| Feature | Traditional Savings (0.01% APY) | High-Yield Savings (4.50% APY) |

| Initial Deposit | $10,000 | $10,000 |

| Interest Earned (Year 1) | $1.00 | $450.00 |

| Total Balance (Year 5) | $10,05.00 | $12,461.82 |

| Monthly Fees | Often $4 to $5 (if minimums not met) | Typically $0 |

| Physical Branches | Yes | No (Online Only) |

By choosing the traditional account, you effectively left over $2,400 of free money on the table.

What is a Traditional Savings Account?

A traditional savings account is the standard, baseline account offered by massive national banks (like Chase, Bank of America, or Wells Fargo) and local credit unions. These institutions have physical branches in your neighborhood, complete with tellers, ATMs, and drive-throughs.

Because these banks spend billions of dollars maintaining physical real estate and paying thousands of tellers across the country, they pass those overhead costs onto you by offering incredibly low interest rates.

The Pros of Traditional Savings Accounts

- Physical Branch Access: If you prefer speaking to a human being face-to-face to resolve an issue, or if you need to get a cashier’s check immediately, you can walk right into a branch.

- Cash Deposits: If you work in a cash-heavy industry (like serving or contracting), you can easily deposit a thick envelope of physical cash through an ATM or teller.

- Instant Transfers: If you hold both your checking and savings accounts at the same traditional bank, moving money between them happens instantaneously.

- Relationship Banking: Holding multiple accounts at a large bank can sometimes qualify you for relationship perks, such as waived fees on premium checking accounts or slight discounts on mortgage rates.

The Cons of Traditional Savings Accounts

- Terrible Interest Rates: An APY of 0.01% means your money is functionally stagnant. Inflation averages 2% to 3% a year, meaning money in a traditional savings account is actually losing purchasing power over time.

- Monthly Maintenance Fees: Many large banks charge a monthly “maintenance fee” (usually around $4 to $15) simply to keep the account open unless you maintain a specific minimum daily balance.

- Minimum Balance Requirements: You are often penalized if your balance drops below $300 or $500, making these accounts actively hostile to people who are just starting their savings journey.

What is a High-Yield Savings Account (HYSA)?

A high-yield savings account functions exactly like a traditional savings account, but it is typically offered by online-only banks or fintech companies (such as Ally, Marcus by Goldman Sachs, Discover, or SoFi).

Because these banks do not have to pay for expensive downtown real estate, maintain physical branch networks, or hire thousands of local tellers, their overhead costs are dramatically lower. They take the money they save on real estate and pass it directly back to you in the form of massively higher interest rates.

If you’re ready to open your first HYSA but aren’t sure which features actually matter, read How to Choose Your First High-Yield Savings Account for a practical checklist covering FDIC insurance, fees, APY, and account selection.

The Pros of High-Yield Savings Accounts

- Maximum Growth: The interest rates are generally 10 to 15 times higher than the national average. This turns your emergency fund into an active income-generating asset.

- Zero Monthly Fees: The vast majority of reputable HYSAs charge absolutely no monthly maintenance fees, period.

- No Minimum Balances: Most online banks allow you to open an account and earn the highest advertised APY with just $1.

- FDIC Insurance: Just like traditional banks, legitimate online banks are FDIC insured. This means the US government guarantees your deposits up to $250,000 per depositor, per institution. Your money is just as safe online as it is in a brick-and-mortar vault.

The Cons of High-Yield Savings Accounts

- No Physical Branches: You cannot walk into a building to speak with a teller. All customer service is handled via phone, email, or live chat.

- Cash Deposits are Difficult: You generally cannot deposit physical cash directly into an HYSA. You have to deposit the cash into a traditional checking account first, and then electronically transfer it.

- Transfer Times: When you need to move money from an online HYSA back to your traditional checking account to pay a bill, the Electronic Funds Transfer (ACH) usually takes 1 to 3 business days to clear. It is not instantaneous.

Interactive: See the HYSA Difference

To truly grasp how much a traditional bank is costing you in lost opportunity, use this interactive calculator. Enter your current savings balance and see exactly how much you would earn in an HYSA versus a standard account over time.

You are losing $0 by staying with a traditional bank!

Move your emergency fund to a High-Yield Savings Account to stop leaving money on the table.

Trad. Bank Interest

HYSA Interest

The Hybrid Strategy: Where Should You Keep Your Money?

When evaluating a high-yield savings account vs traditional savings account, you do not have to pick just one. In fact, the most robust and secure personal finance strategy involves utilizing both.

You should build a two-bank system that separates your spending money from your savings. Here is the blueprint for optimizing your cash flow:

1. The Local Traditional Bank (Your Spending Hub)

Keep a checking account at a local, traditional brick-and-mortar bank. This account is the operational hub of your financial life. Your paycheck is directly deposited here, and you use this account to pay your rent, cover your credit card bills, and withdraw cash from local ATMs.

- Keep Here: One month of living expenses to act as a buffer against accidental overdrafts.

- Why: You get the convenience of physical branches, easy cash deposits, and immediate access to funds for daily life.

(Read more about dialing in these exact balances in our guide on How Much Should You Keep in Checking vs Savings?.)

2. The Online HYSA (Your Financial Fortress)

Open a high-yield savings account at a separate, online-only bank. Link this account to your traditional checking account so you can transfer funds electronically.

- Keep Here: Your fully-funded 3-to-6-month emergency reserve and any sinking funds for mid-term goals (like a house down payment, a wedding, or a new car).

If you’re planning to move into your own apartment or house, an HYSA is also an excellent place to build your moving fund while earning interest. Read How Much Should You Save Before Moving Out on Your Own? to estimate how much you’ll want saved before signing a lease.

- Why: Your large sums of money are earning 4.00%+ APY while remaining safely out of sight. Because it takes 1 to 3 days to transfer money back to your checking account, this physical separation acts as a psychological barrier, preventing you from impulse-spending your emergency fund.

If you haven’t calculated exactly how much cash needs to be inside that fortress, run your numbers through our Advanced Emergency Fund Analyzer and read the core principles in our Emergency Fund Guide 2026.

Is Your Emergency Fund Actually Big Enough?

Stop guessing how much cash you need for a rainy day. Calculate your exact savings target based on your baseline living expenses, income stability, and personal risk factors.

Calculate My Savings TargetCommon Mistakes When Opening a Savings Account

Whether you are sticking with a traditional bank or moving your money to a high-yield account, avoid these three costly traps:

Some banks offer an aggressively high APY (like 6.00%) to attract new customers, but read the fine print. Often, these teaser rates only apply to the first $1,000 you deposit, and then the rate drops to 0.10% for the rest of your balance. Alternatively, the rate might only be guaranteed for three months before plummeting. Look for established online banks that offer a consistent, competitive rate across your entire balance without gimmicks.

2. Keeping Too Much Cash in Savings

While an HYSA is fantastic for protecting your emergency fund from inflation, it is still not a true wealth-building investment vehicle like the stock market. If you have $50,000 sitting in an HYSA but you only need $15,000 for your 6-month emergency fund, you are holding too much cash. The excess $35,000 should be routed into a Roth IRA or a brokerage account where it can grow at a higher historical rate. Balance your accounts using The 50/30/20 Budget Rule Explained Simply.

3. Ignoring Transfer Limits (Regulation D)

Historically, a federal rule called Regulation D limited all savings accounts (both traditional and high-yield) to a maximum of six withdrawals or outgoing transfers per month. If you exceeded this, the bank would charge you a penalty fee or forcefully convert your savings account into a checking account. While the Federal Reserve paused the mandatory enforcement of this rule during the pandemic, many individual banks still enforce their own six-withdrawal limit. Always treat your savings account as a vault, not a daily spending tool.

Your Action Plan: How to Switch to an HYSA

If you are tired of earning pennies on your traditional savings account, it is time to make the switch. Follow this chronological timeline to safely transition your emergency fund without missing a beat.

1.Select a Reputable Online Bank:Look for FDIC insurance and zero fees.

Research top-tier online banks like Ally, Discover, Marcus by Goldman Sachs, or Capital One 360. Verify that the bank has no monthly maintenance fees, no minimum balance requirements, and is officially FDIC-insured.

2.Open and Link the Accounts:Have your ID ready.

Apply for the HYSA online (it takes about 5 minutes). Once approved, you will be prompted to link your existing traditional checking account by providing your routing and account numbers.

3.Execute the Initial Transfer:Leave a small buffer behind.

Do not transfer your entire savings balance at once if it will drop your traditional account below its minimum balance requirement (triggering a monthly fee). Transfer the bulk of your emergency fund to the new HYSA, but leave enough in the traditional bank to keep it fee-free.

4.Automate Your Contributions:Make it passive.

Log into your new HYSA dashboard and set up an automatic monthly transfer from your checking account. Moving just $100 or $200 a month automatically ensures your emergency fund continues to grow without you having to think about it.

Frequently Asked Questions (FAQ)

Can I lose my money in a high-yield savings account?

No. As long as the bank offering the HYSA is FDIC-insured (or NCUA-insured for credit unions), your deposits are federally protected up to $250,000 per depositor. You cannot lose your principal balance to market crashes, unlike money invested in the stock market.

Does the APY on a high-yield savings account change?

Yes. Savings account interest rates are variable, meaning they are subject to change at any time without prior notice. The rates are heavily tied to the Federal Reserve’s benchmark interest rate. If the Fed raises rates, your HYSA yield will likely go up. If the Fed cuts rates, your yield will drop.

Do I have to pay taxes on the interest I earn in an HYSA?

Yes. The interest you earn in any savings account (traditional or high-yield) is considered taxable income by the IRS. At the beginning of tax season, your bank will send you a 1099-INT form detailing exactly how much interest you earned. You must report this amount when you file your state and federal taxes.

Is it hard to get my money out of an online savings account?

Not at all, but it is not instantaneous. To access your funds, you log into your online portal and initiate an electronic transfer (ACH) to your linked traditional checking account. This process typically takes 1 to 3 business days. If you face a true same-day emergency, use a credit card to pay the bill immediately, and then use the HYSA transfer to pay off the credit card a few days later.

Why would anyone keep a traditional savings account?

The only practical reason to maintain a traditional savings account is if your bank requires it to waive the monthly maintenance fees on your primary checking account, or if you regularly need to deposit large sums of physical cash. Otherwise, they offer no financial benefit compared to an HYSA.

Conclusion

When comparing a high-yield savings account vs traditional savings account, the winner is mathematically clear. Traditional savings accounts are a relic of the past, offering interest rates so low that your money actively loses value to inflation. By moving your emergency reserve and long-term cash goals into an online HYSA, you unlock hundreds or even thousands of dollars in passive, zero-risk income.

Do not let inertia or misplaced loyalty to a massive national bank hold your finances back. Keep your checking account local for daily convenience, but build your financial fortress online where your money is respected and rewarded.

References

- Federal Deposit Insurance Corporation (FDIC): Details on deposit insurance limits and how to verify if an online bank is officially insured.

- Consumer Financial Protection Bureau (CFPB): Consumer guidance on understanding banking fees, overdraft protection, and variable interest rates.

- Federal Reserve Board: Historical data on average national savings rates and the mechanics of Regulation D limits.

- Internal Revenue Service (IRS): Guidelines regarding the taxation of interest income and the usage of Form 1099-INT.

Disclaimer: The information provided in this guide is for educational purposes only and does not constitute financial, investment, or tax advice. All financial products and offers are subject to individual credit approval and specific lender terms. Please consult with a qualified financial professional to determine if the strategies or products discussed in this guide are the right fit for your personal financial situation.

About Author

Rishabh Nigam

Rishabh Nigam founded Clarity Flow Core to make personal finance easier to understand for everyday readers. He covers credit scores, debt repayment, credit utilization, loan readiness, taxes, and financial planning through practical guides, calculators, and educational resources. His content focuses on turning complex financial concepts into clear, actionable steps that readers can apply in real life.